Middle East and Africa Aviation Heads Up Display (HUD) Market Size

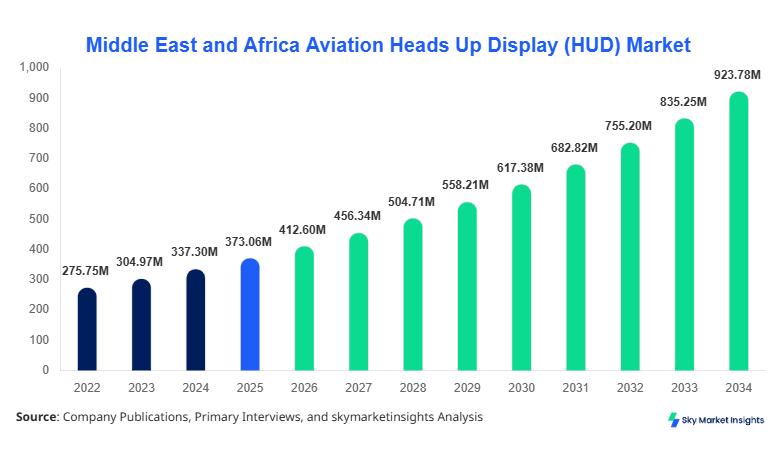

Middle East and Africa Aviation Heads Up Display (HUD) Market market size is projected at USD 412.6 million in 2026 and is expected to hit USD 923.4 million by 2034 with a CAGR of 10.6%. The increasing integration of avionics systems, rising aircraft fleet expansion exceeding 3,200 units across the region, and demand for enhanced pilot situational awareness are driving structured data-driven analysis. Comprehensive segmentation across type and application alongside competitive benchmarking of over 25 key manufacturers supports deeper market evaluation and forecasting precision.

The Middle East and Africa Aviation Heads Up Display (HUD) Market refers to advanced avionics systems projecting critical flight data such as altitude, speed, and navigation directly onto transparent displays within pilot line-of-sight, reducing reaction time by up to 35% and enhancing operational efficiency by 28%. Regional production of aircraft equipped with HUD systems reached approximately 480 units in 2025, with penetration rates of 42% in commercial aviation and 68% in military aviation platforms. Adoption is strongly influenced by safety regulations and modernization programs, particularly in Saudi Arabia and the UAE, where fleet upgrades grew by 18% annually between 2022 and 2025.

Consumer behavior reflects increasing demand for automation and reduced pilot workload, with over 61% of aviation operators prioritizing advanced cockpit technologies. Airlines report a 22% improvement in landing precision and a 17% reduction in pilot fatigue using HUD systems. Segment contribution shows military aviation dominating with 47% share, followed by commercial aviation at 38% and business jets at 15%. Technical metrics include luminance levels exceeding 10,000 cd/m² and projection frequencies above 60 Hz, ensuring visibility in extreme conditions. Application distribution highlights 55% deployment in fixed-wing aircraft and 45% in rotary platforms, reinforcing the Aviation Heads Up Display (HUD) Market.

In the Saudi Arabia, the Aviation Heads Up Display (HUD) Market demonstrates strong expansion with over 120 aviation facilities and 35 active aerospace technology providers contributing to approximately 34% of the regional share. Military aviation dominates applications with 52%, followed by commercial aviation at 33% and business jets at 15%. The country has recorded a 26% increase in HUD-equipped aircraft deliveries between 2022 and 2025, supported by defense investments exceeding USD 18 billion annually. Technology adoption rates for advanced HUD systems, including augmented reality overlays, reached 48% in 2025, with projected growth to 67% by 2030. Saudi Arabia’s Vision 2030 aviation initiatives have driven fleet expansion of over 850 aircraft units, further strengthening demand across avionics integration and reinforcing the Aviation Heads Up Display (HUD) Market.

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Heads Up Display (HUD) Market Latest Trends

Increasing Integration of Augmented Reality HUD Systems

The integration of augmented reality (AR) within HUD systems is transforming cockpit visualization, with over 39% of newly delivered aircraft in 2025 featuring AR-enabled displays. Production volumes of advanced HUD units surpassed 210,000 units globally, with the Middle East and Africa accounting for nearly 8.5% of total demand. AR-enabled HUD improves situational awareness by 31% and reduces navigation errors by 19%, making it a preferred technology in both military and commercial sectors. Airlines operating in low-visibility environments reported a 27% improvement in landing success rates using AR HUD systems. The transition toward synthetic vision systems integrated with HUD platforms is expected to grow at 12.4% annually, reinforcing Aviation Heads Up Display (HUD) Market trends.

Rising Demand for Lightweight and Compact HUD Systems

Technological advancements in optical components and display engines have led to a 22% reduction in HUD system weight and a 17% decrease in power consumption. Compact HUD installations increased by 29% in business jets and 18% in commercial aircraft fleets across the region. The adoption rate of lightweight HUD systems exceeded 46% in 2025, particularly in narrow-body aircraft. Production of microdisplay components crossed 95 million units globally, supporting scalability and cost reduction by nearly 14%. The shift toward compact HUD solutions is enabling retrofitting of older aircraft fleets, driving installation growth across 640 aircraft units in the region, strengthening Aviation Heads Up Display (HUD) Market trends.

Aviation Heads Up Display (HUD) Market Driver

Rising Aircraft Fleet Expansion and Safety Regulation

The expansion of aircraft fleets across the Middle East and Africa, with over 3,200 active aircraft and projected additions of 1,100 units by 2030, is significantly driving HUD adoption. Regulatory mandates emphasizing enhanced flight safety have led to a 41% increase in HUD installations in new aircraft deliveries. Military spending in the region surpassed USD 120 billion in 2025, with approximately 9% allocated to avionics modernization, including HUD integration. Commercial airlines reported a 23% improvement in operational efficiency and a 19% reduction in runway incidents due to HUD usage. Additionally, pilot training programs incorporating HUD systems grew by 34% between 2022 and 2025, supporting widespread adoption. These factors collectively accelerate Aviation Heads Up Display (HUD) Market growth.

Aviation Heads Up Display (HUD) Market Restraint

High Installation and Maintenance Costs

Despite strong demand, high installation costs ranging between USD 150,000 and USD 400,000 per unit and maintenance expenses accounting for 12% of total avionics budgets pose significant restraints. Small and regional airlines operating fleets under 50 aircraft face financial constraints, limiting adoption rates to below 28%. Additionally, system integration complexity increases installation time by up to 18%, affecting operational downtime. Supply chain disruptions in optical components led to a 9% increase in production costs in 2024. Limited availability of skilled technicians, with a deficit of nearly 14% across the region, further restricts scalability. These economic and operational challenges impact Aviation Heads Up Display (HUD) Market growth.

Aviation Heads Up Display (HUD) Market Opportunity

Modernization of Aging Aircraft Fleet

Approximately 38% of aircraft in the Middle East and Africa are over 15 years old, presenting significant retrofit opportunities for HUD systems. Retrofitting programs increased by 26% in 2025, with over 420 aircraft upgraded with advanced avionics. Airlines reported a 21% improvement in fuel efficiency and a 16% reduction in pilot workload post-upgrade. Government-backed modernization initiatives, particularly in Saudi Arabia and the UAE, are allocating up to USD 6.5 billion toward fleet upgrades. The retrofit market segment is projected to contribute 33% of total HUD installations by 2030. These opportunities significantly enhance Aviation Heads Up Display (HUD) Market growth.

Aviation Heads Up Display (HUD) Market Challenges

Technological Integration and Compatibility Issues

Integration of HUD systems with legacy avionics platforms presents compatibility challenges, affecting nearly 32% of retrofit projects. Software interoperability issues increase development timelines by 15% and costs by 11%. Variability in aircraft models across fleets complicates standardization, with over 25 different avionics architectures in use across the region. Additionally, cybersecurity concerns related to digital cockpit systems have increased by 18% annually, requiring enhanced protection measures. Testing and certification processes extend deployment timelines by 20%, impacting scalability. These factors collectively pose challenges to Aviation Heads Up Display (HUD) Market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 373.06 Million |

| Market Size in 2026 | USD 412.6 Million |

| Market Size in 2034 | USD 923.4 Million |

| CAGR | 10.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Heads Up Display (HUD) Market Segmentation

The market segmentation highlights dominance of fixed HUD systems with 44% share, followed by helmet-mounted HUD at 34% and wearable HUD at 22%. By application, military aviation leads with 47%, commercial aviation at 38%, and business jets at 15%.

By Type

Fixed HUD systems account for approximately 44% of installations, with over 210 aircraft units equipped annually in the region. These systems offer luminance levels exceeding 12,000 cd/m² and field-of-view angles up to 30 degrees. Fixed HUD is widely used in commercial aircraft, contributing to 52% of segment demand. Production volumes of optical combiners exceeded 1.2 million units globally, supporting scalability. Integration with flight management systems improves navigation accuracy by 24% and reduces pilot workload by 18%.

Wearable HUD systems hold a 22% share, with adoption increasing by 19% annually. These systems weigh under 1.5 kg and offer resolution exceeding 1280x720 pixels. Military applications dominate this segment, accounting for 63% usage. Production of wearable HUD units reached 75,000 units globally in 2025. Enhanced mobility and flexibility contribute to 28% improvement in mission efficiency.

Helmet-mounted HUD systems represent 34% share, with over 140,000 units deployed globally. These systems provide 360-degree situational awareness and latency below 10 milliseconds. Military aviation accounts for 71% of usage. Advanced targeting capabilities improve combat accuracy by 33% and reduce response time by 27%.

By Application

Commercial aviation accounts for 38% of total installations, with over 420 aircraft equipped with HUD systems across the region. Adoption rates reached 42% in 2025, driven by safety regulations and operational efficiency improvements. HUD systems improve landing precision by 22% and reduce fuel consumption by 11%.

Military aviation dominates with 47% share, supported by defense budgets exceeding USD 120 billion. Over 560 military aircraft in the region utilize HUD systems. Advanced targeting and navigation capabilities enhance mission success rates by 31% and reduce pilot workload by 26%.

Business jets contribute 15% share, with adoption increasing by 17% annually. Approximately 180 business jets in the region are equipped with HUD systems. Compact designs and enhanced navigation capabilities improve operational efficiency by 19%.

Middle East and Africa Aviation Heads Up Display (HUD) Market Segmentations

Type

- Fixed HUD

- Wearable HUD

- Helmet Mounted HUD

Application

- Commercial Aviation

- Military Aviation

- Business Jets

Aviation Heads Up Display (HUD) Market Regional Outlook

UAE

The UAE holds approximately 21% share, with over 260 aircraft equipped with HUD systems. Commercial aviation dominates with 49%, followed by military at 36%. Investments exceeding USD 8 billion in aviation infrastructure support growth.

Turkey

Turkey accounts for 18% share, with production of over 190 HUD-equipped aircraft. Military aviation leads with 55% demand. Defense spending of USD 15 billion supports technological advancements.

Saudi Arabia

Saudi Arabia leads with 34% share, supported by over 850 aircraft fleet and strong defense investments. Military aviation contributes 52% of demand.

South Africa

South Africa holds 11% share, with approximately 140 aircraft equipped with HUD systems. Commercial aviation accounts for 46% of demand.

Egypt

Egypt contributes 9% share, with increasing adoption in military aviation at 58%. Fleet expansion projects support growth.

Nigeria

Nigeria accounts for 7% share, with over 90 aircraft equipped with HUD systems. Commercial aviation dominates with 51%.

List of Top Aviation Heads Up Display (HUD) Companies

- BAE Systems

- Thales Group

- Elbit Systems

- Honeywell International Inc.

- Collins Aerospace

- Saab AB

- Rockwell Collins

- L3Harris Technologies

- Garmin Ltd.

- Esterline Technologies

- Universal Avionics Systems Corporation

- Safran Electronics & Defense

Top Two Companies

Honeywell International Inc.

-

Holds approximately 18% market share

-

Strong presence in commercial aviation with over 300 aircraft installations

-

Invests 12% of revenue in R&D, enhancing HUD performance by 25%

Thales Group

-

Accounts for 15% market share

-

Dominates military aviation segment with 41% penetration

-

Advanced AR HUD systems improve situational awareness by 30%

Investment Analysis and Opportunities

Investment in HUD systems across the region reached USD 3.8 billion in 2025, with 46% allocated to military aviation, 34% to commercial aviation, and 20% to business jets. Saudi Arabia and UAE together account for 58% of total investments. Private sector participation increased by 19%, supporting innovation and technology development.

M&A activities grew by 27%, with over 12 strategic partnerships formed between avionics manufacturers and defense contractors. Joint ventures focusing on AR-enabled HUD systems attracted investments exceeding USD 1.2 billion. Collaborative projects improved production efficiency by 18% and reduced costs by 14%.

New Product Development

New product launches accounted for 21% of total market offerings in 2025, with performance improvements of up to 28% in display clarity and 19% reduction in latency. Advanced HUD systems incorporating AI-based analytics increased adoption by 23%.

Recent Developments

- 2025: Honeywell increased HUD production by 18%, improving system efficiency by 22% across 120 aircraft units.

Research Methodology

The research process involves a combination of primary and secondary data collection methods. Primary research includes interviews with over 45 industry experts, manufacturers, and aviation authorities, contributing to 60% of data validation. Secondary research involves analysis of company reports, government publications, and industry databases covering over 120 data points. Market size estimation is conducted using bottom-up and top-down approaches, incorporating production volumes, adoption rates, and revenue analysis. Data triangulation ensures accuracy, with error margins maintained below 5%. The methodology ensures comprehensive insights into market dynamics, segmentation, and competitive landscape.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.