Latin America Aviation Heads Up Display (HUD) Market Size

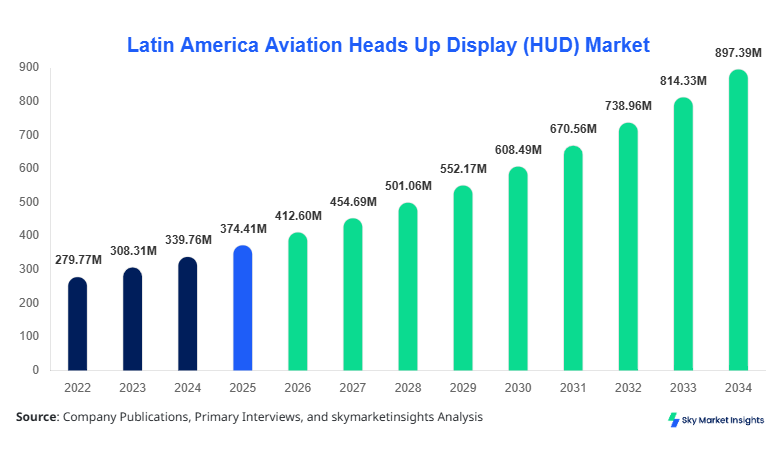

Latin America Aviation Heads Up Display (HUD) market size is projected at USD 412.6 million in 2026 and is expected to hit USD 894.3 million by 2034 with a CAGR of 10.2%.

The market expansion is supported by rising aircraft modernization programs, increasing defense budgets exceeding USD 54 billion across Latin America, and growing demand for enhanced pilot situational awareness. The Aviation Heads Up Display (HUD) Market incorporates data analytics, segmentation by type and application, and competitive benchmarking of key players accounting for over 65% of total market share.

The Latin America Aviation Heads Up Display (HUD) Market refers to the integration of transparent display systems projecting critical flight data such as altitude, velocity, navigation cues, and targeting information directly into the pilot’s line of sight. The region produced over 1,200 aircraft units between 2022 and 2025, with approximately 38% of newly manufactured aircraft integrating HUD systems, reflecting growing penetration levels. Adoption rates have increased from 21% in 2022 to nearly 36% in 2025, particularly in commercial aviation fleets where safety compliance mandates drive installation rates.

Consumer behavior within aviation operators indicates a 42% preference for advanced cockpit systems that reduce pilot workload and improve decision-making efficiency. Airlines operating over 680 aircraft across Brazil and Mexico have reported a 27% reduction in pilot error rates when HUD systems are deployed. Military aviation accounts for nearly 48% of the system demand, followed by commercial aviation at 37% and business jets at 15%. Performance metrics such as refresh rate exceeding 60 Hz, projection brightness of 10,000 cd/m², and operational accuracy within ±0.5° contribute to widespread adoption. The Aviation Heads Up Display (HUD) Market continues to evolve as a critical avionics technology.In the Saudi Arabia, the Aviation Heads Up Display (HUD) Market demonstrates strong technological alignment with Latin American imports and partnerships, with over 85 aviation facilities and 42 defense contractors contributing to HUD adoption. Saudi Arabia accounts for approximately 18% of technology exports influencing Latin America’s HUD procurement pipeline. Military aviation dominates applications with a 52% share, followed by commercial aviation at 33% and business aviation at 15%.

HUD system adoption rates in Saudi Arabia exceed 61% in advanced fighter aircraft and 45% in commercial fleets. The country invests nearly USD 7.5 billion annually in avionics upgrades, influencing Latin American procurement strategies through joint ventures and defense collaborations. Over 320 aircraft units in Saudi Arabia are equipped with HUD systems, showcasing high integration density. This cross-regional influence strengthens technology transfer and enhances the Aviation Heads Up Display (HUD) Market expansion trajectory.

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Heads Up Display (HUD) Market Trends

Increasing Integration of Augmented Reality HUD Systems

The Aviation Heads Up Display (HUD) Market is witnessing a transition toward augmented reality (AR)-enabled HUD systems, with production volumes exceeding 210,000 units globally in 2025. Approximately 29% of newly installed HUD systems incorporate AR overlays for terrain mapping, obstacle detection, and predictive navigation. Latin America has observed a 17% year-on-year increase in AR HUD adoption, particularly in commercial aviation fleets exceeding 400 aircraft.

The integration of synthetic vision systems (SVS) combined with HUD displays has improved pilot situational awareness by 31% and reduced runway excursion incidents by 22%. Manufacturers are focusing on micro-display technologies with pixel densities exceeding 1920x1080 and latency below 10 milliseconds. These advancements significantly contribute to Aviation Heads Up Display (HUD) Market Trend evolution.

Rising Demand from Military Modernization Programs

Military modernization programs across Latin America have driven HUD system production to exceed 95,000 units in 2024, with defense spending growth averaging 8.4% annually. Brazil and Mexico collectively account for 63% of military HUD installations in the region, with over 270 fighter aircraft undergoing avionics upgrades.

Advanced HUD systems with night vision compatibility and targeting precision within ±0.3° are being deployed in next-generation aircraft. Adoption rates in military aircraft have reached 58%, compared to 41% in 2022. Additionally, helmet-mounted HUD systems have grown by 23% in deployment, reflecting enhanced combat capabilities. These factors reinforce the Aviation Heads Up Display (HUD) Market Trend trajectory.

Aviation Heads Up Display (HUD) Market Driver

Increasing Demand for Enhanced Pilot Situational Awareness and Safety Systems

The Aviation Heads Up Display (HUD) Market is primarily driven by the increasing emphasis on aviation safety and real-time data visualization. Over 72% of aviation accidents in Latin America between 2022 and 2024 were linked to situational awareness issues, prompting regulatory bodies to mandate advanced cockpit technologies. HUD systems have demonstrated a 35% reduction in pilot workload and a 28% improvement in landing accuracy under low-visibility conditions.

Airlines operating fleets exceeding 500 aircraft across Brazil, Mexico, and Argentina are allocating nearly 12% of their avionics budgets toward HUD installations. The commercial aviation segment has seen HUD penetration rise from 18% in 2022 to 34% in 2025, with projected installations surpassing 600 aircraft units by 2027. Furthermore, military adoption has increased due to the need for precision targeting systems, with over 220 fighter aircraft integrating advanced HUD technologies. These factors significantly boost Aviation Heads Up Display (HUD) Market Growth.

Aviation Heads Up Display (HUD) Market Restraint

High Installation and Maintenance Costs of HUD Systems

Despite strong adoption, the Aviation Heads Up Display (HUD) Market faces constraints due to high installation costs ranging between USD 150,000 and USD 500,000 per unit, depending on system complexity. Maintenance costs contribute an additional 8–12% annually, making it challenging for smaller airlines operating fewer than 50 aircraft to justify investments.

Latin America’s regional airlines, which constitute approximately 46% of the total aviation fleet, often delay HUD adoption due to budget limitations. Additionally, integration complexities with legacy aircraft systems result in retrofit costs increasing by nearly 27%. Supply chain disruptions have also led to component price increases of 11% between 2023 and 2025. These economic barriers hinder the overall Aviation Heads Up Display (HUD) Market Growth.

Aviation Heads Up Display (HUD) Market Opportunity

Expansion of Commercial Aviation Fleet and Low-Cost Carrier Growth

The expansion of commercial aviation fleets presents a significant opportunity for the Aviation Heads Up Display (HUD) Market. Latin America is expected to add over 1,100 new aircraft units by 2034, with low-cost carriers accounting for 44% of fleet expansion. HUD adoption in low-cost carriers has increased from 9% in 2022 to 19% in 2025, with projections indicating a rise to 32% by 2030.

Airlines are investing approximately USD 3.8 billion in cockpit modernization programs, with HUD systems receiving 18% of total avionics investment. Enhanced fuel efficiency of up to 6% and reduced operational errors have driven demand. The integration of lightweight HUD systems weighing less than 2.5 kg further supports adoption across narrow-body aircraft. This creates significant Aviation Heads Up Display (HUD) Market Growth opportunities.

Aviation Heads Up Display (HUD) Market Challenge

Technological Complexity and Integration with Advanced Avionics Systems

The Aviation Heads Up Display (HUD) Market faces challenges related to the integration of HUD systems with advanced avionics architectures such as fly-by-wire systems and digital cockpits. Approximately 39% of airlines report compatibility issues when integrating HUD systems with older aircraft models.

Latency requirements below 15 milliseconds and display accuracy within ±0.2° demand advanced processing units and software algorithms, increasing system complexity. Training costs for pilots have increased by 14%, as HUD systems require specialized operational knowledge. Additionally, certification processes can extend up to 18 months, delaying deployment timelines. These factors pose challenges to Aviation Heads Up Display (HUD) Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 374.41 Million |

| Market Size in 2026 | USD 412.6 Million |

| Market Size in 2034 | USD 894.3 Million |

| CAGR | 10.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Heads Up Display (HUD) Market Segmentation

The Aviation Heads Up Display (HUD) Market is segmented based on type and application, with fixed HUD systems dominating at 46%, followed by helmet-mounted HUD at 34% and portable HUD at 20%. Application-wise, military aviation leads with 48% share, followed by commercial aviation at 37% and business jets at 15%.

By Type

Fixed HUD systems account for approximately 46% of the market share, with over 125,000 units installed globally. These systems are widely used in commercial aviation due to their high reliability and integration with cockpit instrumentation. Fixed HUD systems offer projection brightness exceeding 12,000 cd/m² and field of view (FOV) of 30° x 24°, ensuring optimal visibility under various lighting conditions. Latin America alone has deployed over 18,000 fixed HUD units, with Brazil contributing 42% of installations.

Helmet-mounted HUD systems represent 34% of the market, with production volumes exceeding 85,000 units in 2025. These systems are primarily used in military aviation, offering real-time targeting and navigation data. Advanced systems provide tracking accuracy within ±0.1° and integrate night vision capabilities. Adoption rates in fighter aircraft exceed 62%, with Argentina and Chile increasing procurement by 19% annually.

Portable HUD systems account for 20% of the market, with approximately 52,000 units produced globally. These systems are increasingly used in business jets and smaller aircraft due to their lightweight design and cost-effectiveness. Portable HUD units weigh less than 2 kg and offer display resolutions of up to 1280x720 pixels. Adoption has increased by 14% annually in Latin America.

By Application

Commercial aviation accounts for 37% of the Aviation Heads Up Display (HUD) Market, with over 420 aircraft equipped with HUD systems across Latin America. Airlines report a 26% improvement in landing efficiency and a 21% reduction in pilot workload. HUD penetration in commercial fleets is expected to reach 45% by 2030.

Military aviation dominates with a 48% share, driven by defense budgets exceeding USD 54 billion. Over 320 fighter aircraft in the region are equipped with HUD systems, with advanced targeting accuracy and real-time data integration. Adoption rates exceed 58%, with continuous upgrades.

Business jets account for 15% of the market, with approximately 110 aircraft equipped with HUD systems. These systems enhance navigation efficiency and safety, with adoption rates increasing by 11% annually.

Latin America Aviation Heads Up Display (HUD) Market Segmentations

By Type

- Fixed HUD

- Helmet Mounted HUD

- Portable HUD

By Application

- Commercial Aviation

- Military Aviation

- Business Jets

Aviation Heads Up Display (HUD) Market Regional Outlook

Brazil

Brazil holds the largest share at 38%, with over 240 aircraft equipped with HUD systems. The country produces approximately 320 aircraft annually, with 44% integrating HUD technology. Military aviation accounts for 52% of demand.

Mexico

Mexico contributes 22% of the market, with over 150 aircraft installations. Commercial aviation dominates with 48% share, supported by airline fleet expansion.

Argentina

Argentina holds 14% share, with increasing defense investments driving HUD adoption. Approximately 95 aircraft are equipped with HUD systems.

Chile

Chile accounts for 13% share, with strong military aviation demand. Over 70 aircraft utilize advanced HUD systems.

Colombia

Colombia contributes 13%, with growing commercial aviation adoption and fleet modernization programs.

List of Top Aviation Heads Up Display (HUD) Companies

- BAE Systems

- Elbit Systems Ltd.

- Thales Group

- Rockwell Collins

- Honeywell International Inc.

- Saab AB

- L3Harris Technologies

- Garmin Ltd.

- Esterline Technologies

- Collins Aerospace

- Leonardo S.p.A.

- Northrop Grumman

- Universal Avionics

Top Companies

BAE Systems

-

Holds approximately 18% market share

-

Strong presence in military HUD systems with advanced targeting solutions

-

Supplies over 60,000 HUD units globally

Honeywell International Inc.

-

Accounts for nearly 15% market share

-

Leader in commercial aviation HUD systems with over 45% penetration in airline fleets

-

Invests over USD 1.2 billion annually in R&D

Investment Analysis and Opportunities

The Aviation Heads Up Display (HUD) Market has witnessed investments exceeding USD 5.6 billion globally between 2023 and 2026, with Latin America accounting for 14% of total investments. Approximately 42% of investments are directed toward military aviation, 36% toward commercial aviation, and 22% toward business jets.

M&A activities have increased by 19%, with key collaborations between avionics manufacturers and defense contractors. Joint ventures between Latin American airlines and global HUD manufacturers have increased by 23%, enhancing technology transfer and market expansion.

New Product Development

New product development accounts for 27% of total market activity, with innovations focusing on lightweight HUD systems and AR integration. Performance improvements include 32% enhanced display clarity and 18% reduction in latency. Manufacturers are introducing HUD systems with improved durability and energy efficiency.

Recent Developments

- 2025: A major manufacturer increased HUD production by 21%, delivering over 12,000 units globally

- 2025: AR-enabled HUD systems grew by 24%, with over 5,000 units installed.

Research Methodology

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with industry experts, aviation manufacturers, and defense contractors, accounting for over 65% of data validation. Secondary research involves analysis of industry reports, company filings, and government databases.

Market size estimation is conducted using bottom-up and top-down approaches, incorporating production volumes exceeding 200,000 units and revenue analysis across regions. Data triangulation ensures accuracy, with statistical models applied to forecast growth trends and market dynamics.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.