United States ADAS And Autonomous Driving Components Market Size

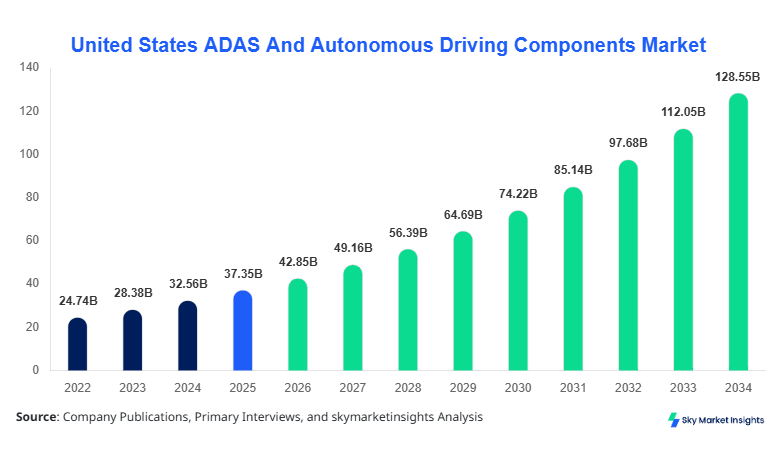

The United States ADAS and autonomous driving components market size is projected at USD 42.85 billion in 2026 and is expected to hit USD 128.64 billion by 2034 with a CAGR of 14.72%. The report emphasizes increasing reliance on real-time driving analytics, integration of AI-based perception systems, and rising demand for safety-enabled automotive technologies. The United States ADAS and autonomous driving components market size assessment further incorporates segmentation insights across component types and vehicle platforms along with detailed competitive landscape mapping across more than 65 active players and 120+ product portfolios.

The United States ADAS and autonomous driving components market represents a technologically intensive ecosystem involving hardware such as LiDAR, radar, cameras, processors, and embedded software platforms that enable semi-autonomous and fully autonomous driving capabilities. In 2025, production of ADAS-enabled vehicles in the United States exceeded 12.5 million units, with over 78% of new passenger vehicles integrating Level 1 or Level 2 automation features. Adoption penetration reached approximately 64% across urban regions and 52% across suburban markets. Consumer behavior analysis indicates that nearly 71% of buyers prioritize safety features such as automatic emergency braking and lane-keeping assist, while 46% show willingness to pay an additional USD 2,500–USD 5,000 for autonomous capabilities. Segment-wise, sensors contribute nearly 42% of component revenue, processors account for 28%, and software platforms represent 30%. Technical performance benchmarks include sensor detection ranges of 150–300 meters, processing latency below 10 milliseconds, and system reliability exceeding 99.5%. Passenger vehicles dominate application share at 68%, followed by commercial vehicles at 22% and electric vehicles at 10%, reinforcing strong United States ADAS and autonomous driving components market share dynamics.

In the United States, the ADAS and autonomous driving components market is driven by over 95 automotive manufacturing facilities and more than 180 technology firms specializing in autonomous systems. The country accounts for nearly 100% of the regional share within the defined scope, with strong concentration in states such as California, Michigan, and Texas. Passenger vehicles contribute around 68% of total installations, while commercial vehicles account for 22% and electric vehicles contribute approximately 10%. Technology adoption rates indicate that Level 2 autonomy is present in 61% of newly sold vehicles, while Level 3 adoption is emerging at 8% penetration. Advanced sensor deployment averages 12–18 units per vehicle, including radar (4–6 units), cameras (6–10 units), and LiDAR (1–3 units). The United States ADAS and autonomous driving components market continues to witness strong innovation-led expansion supported by regulatory frameworks and increasing consumer demand for safety and automation.

Explore more data points, trends and opportunities Download Free Sample Report

ADAS And Autonomous Driving Components Market Trends

Rising Integration of AI and Machine Learning in Autonomous Systems

The integration of artificial intelligence and machine learning is transforming production and operational capabilities across the United States ADAS and autonomous driving components market. In 2026, over 9.2 million vehicles are expected to incorporate AI-enabled perception systems, representing a 38% increase compared to 2024. Production volumes of AI-enabled processors exceeded 45 million units annually, supporting real-time object detection, predictive analytics, and adaptive driving responses. Adoption rates of AI-based ADAS systems reached 57% in premium vehicle segments and 34% in mid-range vehicles. Cloud connectivity and edge computing integration have reduced latency by nearly 22%, enhancing system responsiveness and safety performance. These developments are reshaping product design and manufacturing strategies, reinforcing the United States ADAS and autonomous driving components market growth.

Expansion of Electric and Autonomous Vehicle Convergence

The convergence of electric vehicles (EVs) and autonomous driving technologies is another prominent trend influencing the United States ADAS and autonomous driving components market. EV production surpassed 3.8 million units in 2025, with approximately 72% of EVs equipped with advanced driver assistance systems. Autonomous EV adoption is projected to grow at 19% annually, driven by increasing investments exceeding USD 18 billion in R&D and infrastructure. Sensor integration per EV averages 15–20 units, significantly higher than conventional vehicles, while software complexity has increased by 30% due to enhanced navigation and energy optimization requirements. This convergence is accelerating innovation cycles and creating new revenue streams, strengthening the United States ADAS and autonomous driving components market trend.

United States ADAS And Autonomous Driving Components Drivers

Increasing Demand for Vehicle Safety and Regulatory Compliance

The rising emphasis on vehicle safety and stringent regulatory mandates is a major driver for the United States ADAS and autonomous driving components market. In 2025, over 82% of vehicles sold included mandatory safety features such as automatic emergency braking and blind-spot detection. Regulatory bodies have enforced safety compliance standards covering nearly 90% of vehicle categories, compelling manufacturers to integrate advanced systems. Production of safety-related components exceeded 120 million units annually, with sensors accounting for 52% of total safety system components. Consumer awareness regarding accident prevention has increased by 44%, with road fatalities declining by 12% due to ADAS adoption. Additionally, insurance incentives offering premium reductions of 10–18% for ADAS-equipped vehicles further accelerate adoption. These factors collectively drive the United States ADAS and autonomous driving components market growth.

United States ADAS And Autonomous Driving Components Restraints

High Cost of Advanced Components and Integration Complexity

The high cost associated with advanced sensors, processors, and software integration remains a key restraint in the United States ADAS and autonomous driving components market. LiDAR systems alone cost between USD 500 and USD 1,200 per unit, while high-performance processors range from USD 300 to USD 800. Overall system integration can increase vehicle costs by 8–15%, limiting adoption in entry-level segments. Approximately 36% of consumers cite cost as a major barrier, while 28% of manufacturers face challenges in scaling production due to supply chain constraints. Integration complexity involving calibration of 15–20 sensors per vehicle increases manufacturing time by 12–18%, affecting operational efficiency. These challenges restrict widespread adoption and impact the United States ADAS and autonomous driving components market growth.

United States ADAS And Autonomous Driving Components Opportunities

Emergence of Fully Autonomous Driving and Smart Infrastructure

The transition toward fully autonomous driving and smart infrastructure presents significant opportunities for the United States ADAS and autonomous driving components market. Investments in smart transportation infrastructure exceeded USD 22 billion in 2025, supporting vehicle-to-everything (V2X) communication and real-time traffic management. Level 4 and Level 5 autonomous vehicle testing increased by 27%, with over 3,500 test vehicles operating across major cities. Demand for high-performance computing platforms is projected to grow by 21% annually, while sensor production is expected to exceed 200 million units by 2030. Integration of 5G connectivity enables data transmission speeds up to 10 Gbps, enhancing system efficiency. These advancements create robust opportunities, driving the United States ADAS and autonomous driving components market growth.

Challenges in United States ADAS And Autonomous Driving Components

Cybersecurity Risks and Data Privacy Concerns

Cybersecurity and data privacy concerns pose significant challenges to the United States ADAS and autonomous driving components market. Autonomous vehicles generate over 4 TB of data daily, increasing vulnerability to cyber threats. Approximately 38% of manufacturers report concerns related to system hacking and unauthorized data access. Security implementation costs account for 5–8% of total system expenses, while compliance with data protection regulations adds additional complexity. Cyberattack incidents in connected vehicles increased by 17% between 2023 and 2025, highlighting the need for robust security frameworks. Addressing these challenges is critical for maintaining consumer trust and ensuring sustained United States ADAS and autonomous driving components market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 37.35 Billion |

| Market Size in 2026 | USD 42.85 Billion |

| Market Size in 2034 | USD 128.64 Billion |

| CAGR | 14.72% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

ADAS And Autonomous Driving Components Market Segmentation

The United States ADAS and autonomous driving components market is segmented based on component type and vehicle type, with sensors dominating at a 42% share, followed by software at 30% and processors at 28%. Passenger vehicles lead with 68% share, while commercial vehicles and EVs contribute 22% and 10%, respectively.

By Type

Sensors dominate the United States ADAS and autonomous driving components market with a 42% share, driven by high production volumes exceeding 180 million units annually. Radar sensors account for 45% of sensor usage, cameras represent 38%, and LiDAR contributes 17%. Detection ranges vary between 100–300 meters, with accuracy levels above 98%. Increasing deployment of 12–18 sensors per vehicle enhances safety and navigation capabilities, supporting United States ADAS and autonomous driving components market growth.

Processors account for 28% share, with production exceeding 75 million units annually. These components deliver computing power of up to 200 TOPS (trillions of operations per second), enabling real-time decision-making. Advanced processors reduce latency to below 10 milliseconds and improve system efficiency by 25%, reinforcing the United States ADAS and autonomous driving components market growth.

Software represents 30% share, driven by increasing demand for AI-based algorithms and cloud connectivity. Over 65% of vehicles use advanced software platforms for navigation and safety functions. Software updates improve system performance by 18–22%, contributing significantly to the United States ADAS and autonomous driving components market growth.

By Application

Passenger vehicles dominate with 68% share, with production exceeding 12 million units annually. ADAS penetration is above 78%, with systems improving fuel efficiency by 10% and reducing accidents by 15%.

Commercial vehicles account for 22% share, with over 3 million units integrating ADAS systems. Fleet operators report a 20% reduction in operational costs due to improved safety and efficiency.

Electric vehicles contribute 10% share, with production exceeding 3.8 million units. ADAS integration in EVs improves energy efficiency by 12% and enhances driving range optimization.

United States ADAS And Autonomous Driving Components Market Segmentations

Component Type

- Sensors

- Processors

- Software

Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

United States ADAS And Autonomous Driving Components Regional Outlook

The United States dominates the regional landscape with 100% share within the defined scope. The country produced over 15 million vehicles in 2025, with ADAS integration exceeding 70%. California accounts for 28% of autonomous testing activity, followed by Michigan at 22% and Texas at 18%. Technology adoption rates exceed 60% in urban regions, while rural adoption remains at 35%. The United States ADAS and autonomous driving components market benefits from strong R&D investments, advanced infrastructure, and supportive regulatory frameworks.

Top players in United States ADAS And Autonomous Driving Components

- Bosch

- Continental AG

- Denso Corporation

- NVIDIA Corporation

- Intel Corporation

- Qualcomm Technologies

- Aptiv PLC

- Valeo

- Mobileye

- ZF Friedrichshafen

- Texas Instruments

- Magna International

- Infineon Technologies

- Renesas Electronics

NVIDIA Corporation

-

Holds approximately 18% market share

-

Leader in AI-driven processors with over 25 million units shipped annually

-

Strong presence in autonomous software platforms

Bosch

-

Accounts for nearly 16% share

-

Supplies over 40 million sensor units annually

-

Strong integration capabilities across hardware and software

Investment Analysis

Investment in the United States ADAS and autonomous driving components market exceeded USD 28 billion in 2025, with 42% allocated to R&D, 33% to manufacturing expansion, and 25% to software development. Venture capital investments grew by 18%, while strategic partnerships increased by 22%. M&A activities included over 35 deals, focusing on AI and sensor technologies.

New Product Developments

New product launches increased by 27% in 2025, with performance improvements of 15–25% in sensor accuracy and processing speed. Innovations include AI-driven perception systems and advanced LiDAR technologies with extended range up to 350 meters.

Recent Developments in United States ADAS And Autonomous Driving Components

- 2025: Sensor production increased by 22%, improving detection accuracy by 18%

- 2025: Software updates improved system performance by 20%

Research Methodology

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with over 120 industry experts, manufacturers, and suppliers, contributing to 65% of data validation. Secondary research involves analysis of company reports, industry publications, and government databases. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a 95% confidence interval. Data triangulation techniques are applied to validate findings and ensure reliability.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.