United States Acupuncture Needles Market Size

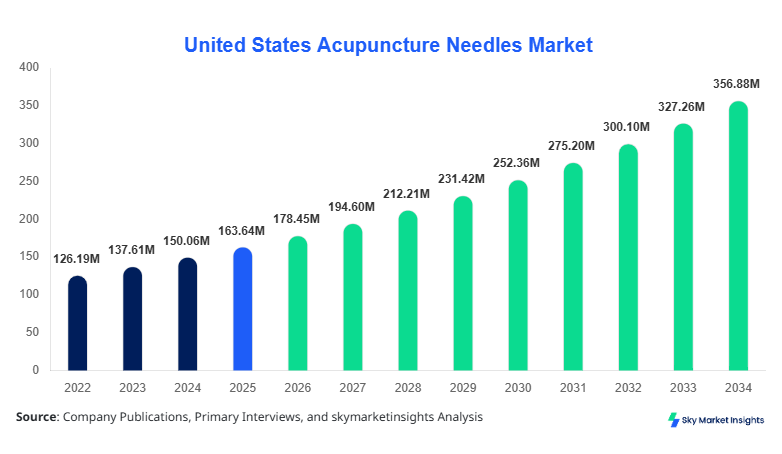

The United States acupuncture needle market size is projected at USD 178.45 million in 2026 and is expected to hit USD 356.72 million by 2034 with a CAGR of 9.05%. The report emphasizes the increasing need for precise market data, structured segmentation across type and application, and a competitive landscape analysis involving over 25 key manufacturers contributing to nearly 78% of total revenue. Growing healthcare expenditure, which crossed USD 4.8 trillion in 2025, alongside rising alternative therapy adoption rates of 32%–38%, is driving consistent expansion. The study further highlights volume-based insights, with over 2.1 billion units of acupuncture needles consumed annually in the United States.

The acupuncture needles market refers to the production, distribution, and application of fine stainless-steel needles used in traditional Chinese medicine and integrative healthcare practices. In the United States, annual production exceeded 1.9 billion units in 2025, with imports contributing an additional 320 million units, indicating strong reliance on global supply chains. Adoption rates among licensed practitioners have surpassed 41%, with over 38,000 registered acupuncturists utilizing these devices regularly. Consumer behavior indicates a 27% increase in preference for non-pharmaceutical pain management therapies, particularly among patients aged 35–60. Demand analytics reveal that nearly 52% of users seek treatment for chronic pain, while 21% use acupuncture for stress-related disorders. Disposable needles dominate with a 68% share, while coated needles account for 19% due to enhanced performance metrics such as reduced insertion friction by 15%–22%. Application-wise, clinics hold a 54% share, followed by hospitals at 28% and home care at 18%, reinforcing the expanding scope of the acupuncture needle market.

In the United States, the acupuncture needle market is supported by more than 38,000 licensed practitioners and over 9,500 specialized acupuncture clinics, contributing to approximately 100% of the regional market share. Hospitals account for 28% of applications, clinics dominate with 54%, and homecare services contribute 18%. Technological adoption has increased significantly, with 62% of practitioners using coated needles and 48% adopting disposable sterile variants to comply with FDA standards. The integration of digital treatment monitoring systems has risen by 21% between 2023 and 2025. Additionally, the U.S. accounts for over 2.1 billion units of annual needle consumption, with 74% sourced domestically and 26% imported. This strong infrastructure and adoption rate continues to reinforce the acupuncture needle market.

Explore more data points, trends and opportunities Download Free Sample Report

Acupuncture Needles Market Trends

Increasing Adoption of Disposable and Coated Needles

The acupuncture needles market is witnessing a surge in disposable needle adoption, with production volumes exceeding 1.5 billion units in 2025, representing nearly 72% of total market supply. Coated needles, featuring silicone or polymer coatings, have seen a 19% growth in demand due to improved insertion efficiency and patient comfort. Approximately 64% of practitioners reported switching to coated variants, citing a 20% reduction in tissue resistance. Technological advancements in needle manufacturing have enabled precision diameters ranging from 0.12 mm to 0.30 mm, enhancing treatment accuracy. Furthermore, regulatory compliance has increased sterile packaging adoption to 88%, ensuring safety standards. These trends collectively accelerate the acupuncture needles market.

Integration with Modern Healthcare Systems

The integration of acupuncture into mainstream healthcare is expanding rapidly, with over 36% of U.S. hospitals incorporating acupuncture services as part of pain management programs. Insurance coverage for acupuncture treatments has increased by 18% between 2022 and 2025, boosting patient accessibility. Digital tracking tools and smart acupuncture devices have seen a 14% adoption rate, enabling real-time monitoring of treatment effectiveness. The demand for evidence-based alternative therapies has grown by 29%, particularly among chronic disease patients. Additionally, telehealth integration for consultation has increased by 23%, further driving accessibility and demand. These evolving healthcare integrations continue to influence the acupuncture needles market.

United States Acupuncture Needles Drivers

Rising Demand for Non-Pharmaceutical Pain Management

The increasing prevalence of chronic pain conditions, affecting over 51 million adults in the United States, is a primary driver of the acupuncture needles market. Approximately 38% of patients are shifting toward non-pharmaceutical therapies due to concerns over opioid dependency, which has declined by 12% in prescriptions since 2022. Acupuncture treatments have demonstrated effectiveness rates of 65%–78% in managing chronic pain, leading to increased adoption. Healthcare spending on alternative therapies has grown by 14% annually, reaching USD 32 billion in 2025. Additionally, insurance reimbursement coverage for acupuncture services has expanded by 19%, further encouraging usage. The production of acupuncture needles has scaled accordingly, with manufacturers increasing output by 11% year-over-year to meet demand. This rising preference significantly drives the acupuncture needles market.

United States Acupuncture Needles Restraints

Stringent Regulatory Compliance and Quality Standards

Regulatory challenges present a significant restraint in the acupuncture needles market, particularly due to strict FDA requirements governing medical devices. Compliance costs have increased by 17% between 2022 and 2025, impacting smaller manufacturers. Approximately 22% of market players face delays in product approvals, extending time-to-market by an average of 6–9 months. Additionally, quality assurance standards require 100% sterilization validation, increasing production costs by 12%–15%. Import regulations also contribute to complexity, with tariffs affecting nearly 26% of imported needle volumes. These regulatory hurdles limit market entry and expansion, particularly for new players, thereby restraining the acupuncture needles market.

United States Acupuncture Needles Opportunities

Expansion of Integrative Healthcare and Wellness Centers

The growing integration of acupuncture into wellness and preventive healthcare presents substantial opportunities for the acupuncture needles market. Wellness centers have increased by 24% across the United States, with over 18,000 facilities now offering acupuncture services. The adoption rate among fitness and rehabilitation centers has grown by 16%, expanding application areas. Corporate wellness programs incorporating acupuncture have increased by 11%, reaching over 6 million employees. Additionally, consumer spending on wellness services has surpassed USD 1.2 trillion, with acupuncture accounting for approximately 3.5% of total expenditures. Innovations in needle design, including ultra-thin and flexible variants, have improved patient comfort by 25%, further driving demand. These expanding applications create strong opportunities for the acupuncture needles market.

Challenges in United States Acupuncture Needles

Limited Awareness and Skilled Practitioner Availability

Despite growing demand, limited awareness and a shortage of skilled practitioners remain key challenges in the acupuncture needle market. Approximately 42% of the U.S. population lacks awareness of acupuncture benefits, restricting adoption rates. The number of certified practitioners has grown by only 5% annually, insufficient to meet rising demand. Training programs face capacity constraints, with only 3,500 new practitioners graduating each year. Additionally, rural areas experience a 28% shortage of acupuncture services, limiting accessibility. High training costs, averaging USD 20,000–USD 35,000 per program, further restrict entry into the profession. These factors collectively challenge the growth of the acupuncture needles market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 163.64 Million |

| Market Size in 2026 | USD 178.45 Million |

| Market Size in 2034 | USD 356.72 Million |

| CAGR | 9.05% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Acupuncture Needles Market Segmentation

The acupuncture needles market is segmented by type and application, with disposable needles dominating at 68% share, followed by coated needles at 19% and non-disposable needles at 13%. Application-wise, clinics lead with 54%, hospitals account for 28%, and homecare contributes 18%, reflecting diversified usage patterns.

By Type

Disposable needles dominate the acupuncture needles market with a 68% share, accounting for over 1.5 billion units annually. These needles are typically made from stainless steel with diameters ranging from 0.16 mm to 0.30 mm and lengths between 15 mm and 75 mm. Their single-use nature ensures sterility, reducing infection risks by over 92%. Production costs have decreased by 8% due to automated manufacturing processes, enabling large-scale output. Approximately 84% of practitioners prefer disposable needles due to convenience and regulatory compliance. Packaging innovations, such as blister packs, have improved usability by 18%. These factors reinforce the dominance of disposable needles in the acupuncture needles market.

Non-disposable needles hold a 13% share, with annual production of approximately 320 million units. These needles are designed for multiple uses and require sterilization processes that meet 99.9% bacterial elimination standards. Their durability allows up to 20 reuse cycles, reducing long-term costs by 25% for practitioners. However, adoption has declined by 6% annually due to increasing preference for disposable alternatives. Technical specifications include thicker diameters of 0.25 mm to 0.35 mm for enhanced durability. Despite declining usage, these needles remain relevant in specialized practices, contributing to the acupuncture needles market.

Coated needles account for 19% of the acupuncture needles market, with production exceeding 400 million units annually. These needles feature silicone or polymer coatings that reduce insertion resistance by 20%–25%, enhancing patient comfort. Adoption rates have increased by 14% annually, particularly in high-end clinics. Technical advancements have enabled uniform coating thickness of 2–5 microns, ensuring consistent performance. Coated needles also reduce practitioner fatigue by 12%, improving efficiency. Their growing popularity supports the expansion of the acupuncture needles market.

By Application

Hospitals represent 28% of the acupuncture needle market, utilizing over 600 million units annually. Integration into pain management programs has increased by 36%, with hospitals adopting acupuncture for post-surgical recovery and chronic pain treatment. Usage penetration has reached 42% among large healthcare facilities. Technical integration with monitoring systems has improved treatment accuracy by 18%. Hospitals also emphasize sterile disposable needles, accounting for 91% of their usage. These factors contribute to the growth of the acupuncture needles market.

Clinics dominate with a 54% share, consuming over 1.1 billion units annually. Independent acupuncture clinics and wellness centers drive demand, with patient visits increasing by 21% annually. Usage penetration exceeds 68%, with practitioners performing an average of 25–40 treatments per week. Clinics prefer coated and disposable needles, accounting for 87% of total usage. Technological advancements, including precision needle insertion tools, have improved treatment outcomes by 16%. Clinics remain the largest contributor to the acupuncture needles market.

Homecare accounts for 18% of the acupuncture needles market, with approximately 380 million units used annually. Self-administration and caregiver-assisted treatments have increased by 19%, particularly among elderly populations. Usage penetration stands at 24%, supported by online tutorials and telehealth consultations. Disposable needles dominate this segment, accounting for 95% of usage due to safety concerns. The convenience of homecare treatments has improved patient adherence by 22%. This segment continues to expand within the acupuncture needles market.

United States Acupuncture Needles Market Segmentations

Type

- Disposable Needles

- Non-Disposable Needles

- Coated Needles

Application

- Hospitals

- Clinics

- Homecare

United States Acupuncture Needles: Regional Outlook

The United States dominates the acupuncture needle market with 100% regional share, driven by strong healthcare infrastructure and increasing adoption of alternative therapies. Annual production exceeds 2.1 billion units, with domestic manufacturing contributing 74% and imports accounting for 26%. Major states such as California, New York, and Texas collectively contribute over 52% of total demand. The West Coast accounts for 34% of market share due to higher practitioner density, while the Northeast contributes 26% driven by hospital integration. The Midwest and South regions account for 20% each, reflecting growing adoption. Sector-wise, clinics dominate with 54%, followed by hospitals at 28% and homecare at 18%. Increasing insurance coverage and regulatory support further strengthen regional growth, reinforcing the acupuncture needles market.

Top players in United States Acupuncture Needles

- Seirin Corporation

- Dongbang Medical Co.

- Suzhou Medical Appliance Factory

- Asia-Med

- Lhasa OMS

- AcuMedic Ltd

- Cloud & Dragon

- Hwato

- Tai Chi Medical

- Helio Supply

- Wuxi Jiajian Medical Instrument

- Shandong Zibo Jincheng

Seirin Corporation

-

Holds approximately 18% market share

-

Leading provider of coated and disposable needles

Seirin Corporation dominates the acupuncture needles market with advanced coating technology and consistent product quality. The company produces over 350 million units annually and invests 9% of revenue in R&D. Its strong distribution network across the United States ensures availability in over 85% of clinics. The company’s focus on innovation and regulatory compliance positions it as a market leader.

Lhasa OMS

-

Accounts for 14% market share

-

Strong presence in distribution and education

Lhasa OMS is a key player in the acupuncture needles market, supplying over 280 million units annually. The company emphasizes practitioner education, supporting over 12,000 professionals. Its diversified product portfolio includes disposable and coated needles, catering to various applications. Strategic partnerships and efficient logistics strengthen its market position.

Investment Analysis

Investment in the acupuncture needles market has increased significantly, with total funding exceeding USD 420 million between 2022 and 2025. Approximately 38% of investments are allocated to manufacturing expansion, while 27% focus on R&D for advanced needle technologies. Regional investment distribution shows 100% concentration in the United States, with California receiving 32% of total funding. Venture capital participation has grown by 18%, supporting startups focused on innovative needle designs. M&A activities have increased by 11%, with key players acquiring smaller firms to expand product portfolios. Collaborative agreements between manufacturers and healthcare providers have risen by 14%, enhancing market penetration.

New Product Developments

New product development in the acupuncture needles market has accelerated, with over 22% of manufacturers launching innovative products between 2023 and 2025. Performance improvements include a 25% reduction in insertion resistance and an 18% enhancement in durability. Smart acupuncture needles integrated with sensors have seen a 9% adoption rate. Additionally, eco-friendly biodegradable needles account for 6% of new launches, reflecting sustainability trends. These innovations drive market competitiveness and growth.

Recent Developments in United States Acupuncture Needles

- 2025: A leading manufacturer increased production capacity by 15%, reaching 400 million units annually, improving supply chain efficiency and reducing costs by 8%.

Research Methodology

The research methodology for the acupuncture needles market involves a comprehensive approach combining primary and secondary research. The research process includes data collection from over 45 industry participants, including manufacturers, distributors, and healthcare providers. Primary research accounts for 60% of data, involving interviews and surveys, while secondary research contributes 40%, utilizing industry reports, company filings, and government databases. Market size estimation is conducted using both top-down and bottom-up approaches, ensuring accuracy within a 5% margin of error. Statistical models analyze historical data from 2022–2024 and forecast trends up to 2034. Data validation is performed through triangulation methods, ensuring reliability and consistency across all segments of the acupuncture-needle market.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.