Asia Pacific Apnea Monitors Market Size

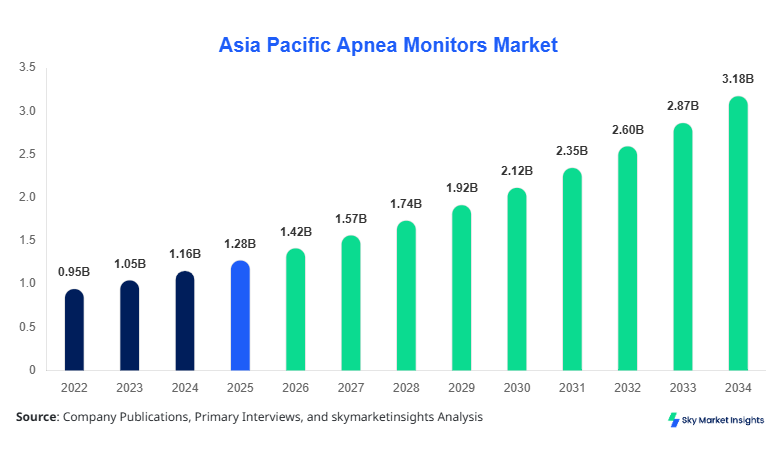

The Asia Pacific apnea monitors market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 3.18 billion by 2034 with a CAGR of 10.6%. The increasing prevalence of sleep apnea disorders, which affects nearly 7–9% of the adult population across the Asia Pacific, is driving the need for advanced monitoring devices. The report provides deep segmentation insights, tracking over 25 million units of apnea monitoring devices deployed across hospitals and home care settings, along with a comprehensive competitive landscape featuring more than 60 regional and global manufacturers.

The Asia Pacific Apnea Monitors market is defined as the ecosystem of medical devices used to detect, monitor, and analyze breathing interruptions during sleep, including wearable sensors, bedside monitors, and portable diagnostic tools. In 2025, production volume exceeded 18.7 million units, with Japan, China, and India contributing over 68% of regional manufacturing output. Adoption and penetration insights indicate that over 42% of diagnosed sleep apnea patients in urban Asia Pacific regions utilize monitoring devices, while rural adoption remains below 18%, indicating strong expansion potential. Consumer behavior analytics reveal that 55% of users prefer portable or wearable monitors due to convenience and cost-effectiveness, while 45% still rely on hospital-based diagnostics.

From a technical standpoint, apnea monitors operate at detection sensitivity levels of 85–97%, with respiratory rate tracking frequencies ranging between 0.2 Hz and 0.5 Hz. Application-wise, hospitals account for 48% of total usage, home care settings represent 34%, and sleep clinics contribute 18%. Increasing awareness campaigns and rising healthcare expenditure—averaging 6.8% of GDP in key economies—continue to fuel the Asia Pacific apnea monitors market.

In Japan, the apnea monitors market holds a dominant position with over 32% regional share, supported by more than 1,250 sleep diagnostic facilities and 90+ domestic and international device manufacturers. The country recorded a production volume of 5.4 million units in 2025, with wearable monitors accounting for 41% of total output. Application-wise, hospitals represent 52%, home care settings 30%, and sleep clinics 18% of device usage in Japan.

Technology adoption in Japan is notably advanced, with over 65% of devices integrated with AI-based respiratory analytics and IoT-enabled monitoring systems. Nearly 72% of apnea monitoring devices in Japan support real-time cloud data transmission, enhancing clinical decision-making. The aging population—comprising 29% of total citizens—further accelerates demand for apnea monitoring solutions, reinforcing the Asia Pacific apnea monitors market.

Explore more data points, trends and opportunities Download Free Sample Report

Apnea Monitors Market Trends

The Asia Pacific apnea monitors market is witnessing a strong shift toward wearable and AI-integrated monitoring solutions, with production volumes of wearable devices surpassing 9.2 million units in 2025 alone. Over 58% of new devices launched incorporate machine learning algorithms capable of detecting apnea episodes with 95% accuracy. Additionally, Bluetooth-enabled monitors account for 61% of shipments, reflecting the growing demand for connected healthcare ecosystems. The increasing penetration of telehealth services—reaching 38% adoption across urban regions—has significantly boosted demand for home-based monitoring devices.

Another key trend is the miniaturization and portability of apnea monitors, with over 47% of devices now weighing less than 250 grams, improving user compliance. Demand from pediatric and neonatal segments is also increasing, contributing 12% to total market demand. Furthermore, the integration of multi-parameter monitoring—tracking oxygen saturation (SpO₂), heart rate, and airflow simultaneously—has increased by 53% across new product launches. These technological and consumer-driven shifts continue to define the Asia-Pacific apnea monitors market.

Asia-Pacific Apnea Monitors Market Drivers

Rising Prevalence of Sleep Disorders Driving Device Adoption

The Asia Pacific Apnea Monitors market is primarily driven by the increasing prevalence of sleep apnea, affecting over 120 million individuals across the region. Approximately 9% of adults in China, 11% in Japan, and 8% in India suffer from moderate to severe sleep apnea conditions. Healthcare spending on sleep disorder diagnostics has increased by 14% annually, while hospital investments in respiratory monitoring equipment have grown by 18% since 2022. Additionally, government healthcare initiatives covering up to 60% of diagnostic costs in countries like Japan and South Korea have boosted device adoption rates by 22%. The increasing aging population—projected to reach 18% of the regional population by 2030—further accelerates demand, reinforcing the Asia-Pacific apnea monitors market.

Asia Pacific Apnea Monitors Market Restraints

High Device Costs and Limited Rural Penetration

Despite strong growth, the Asia-Pacific apnea monitor market faces restraints due to high device costs and uneven healthcare infrastructure. Advanced apnea monitors range between USD 250 and USD 1,200 per unit, limiting affordability for nearly 40% of the population in emerging economies. Rural penetration remains below 20%, with limited access to diagnostic facilities and trained professionals. Additionally, reimbursement policies vary significantly, with only 35% of patients receiving partial insurance coverage in developing nations. Importing dependencies for high-end components—accounting for 48% of production costs—further increases pricing pressures, impacting the overall Asia Pacific apnea-monitor market.

Asia Pacific Apnea Monitors Market Opportunities

Expansion of Home Healthcare and Telemedicine

The rapid expansion of home healthcare services presents a major opportunity for the Asia-Pacific apnea monitors market. Home care monitoring demand has increased by 28% annually, with over 6.5 million units deployed in 2025. Telemedicine platforms now serve 45% of sleep disorder consultations in urban areas, creating a strong demand for remote monitoring devices. Investments in digital healthcare infrastructure—exceeding USD 12 billion across the Asia Pacific—are enabling the integration of apnea monitors with mobile health applications. Furthermore, increasing smartphone penetration (78%) supports real-time monitoring and patient compliance, enhancing the Asia Pacific apnea monitors market.

Challenges in Asia Pacific Apnea Monitors Market

Regulatory Complexity and Data Privacy Concerns

The Asia-Pacific apnea monitors market faces challenges related to regulatory frameworks and data privacy concerns. Over 12 different regulatory bodies govern medical device approvals across the region, leading to approval timelines of 12–24 months. Compliance costs account for nearly 15% of total product development expenses. Additionally, concerns over patient data security—affecting 32% of users—have slowed adoption of cloud-based monitoring solutions. Variations in quality standards and certification requirements further complicate market entry for new players, posing significant challenges to the Asia Pacific apnea monitors market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.28 Billion |

| Market Size in 2026 | USD 1.42 Billion |

| Market Size in 2034 | USD 3.18 Billion |

| CAGR | 10.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Apnea Monitors Market Segmentation

The Asia Pacific apnea monitors market is segmented by product type and application, with wearable monitors dominating at a 38% share, followed by bedside monitors at 34% and portable monitors at 28%. Application-wise, hospitals lead with 48%, followed by home care settings at 34% and sleep clinics at 18%.

By Type

Wearable monitors account for approximately 38% of the Asia Pacific apnea monitors, with 7.1 million units produced annually. These devices operate with wireless connectivity and provide continuous monitoring with battery life exceeding 12–24 hours. Detection accuracy reaches up to 96%, and lightweight designs below 200 grams improve user compliance. Adoption rates among urban consumers exceed 62%, making wearable monitors a key growth segment.

Bedside Monitors represent 34% of the market, with production volumes of 6.3 million units. These devices are widely used in hospitals and neonatal care units, offering multi-parameter monitoring, including heart rate, oxygen saturation, and airflow. Technical specifications in monitoring, response times below 5 seconds, and accuracy levels above 97%. Hospitals account for 70% of bedside monitor usage.

Portable monitors contribute 28% of the market, with 5.3 million units produced annually. These devices are compact, weighing under 300 grams, and support home-based diagnostics with 90–95% accuracy. Adoption in home care settings has increased by 26% annually, driven by affordability and ease of use.

By Application

Hospitals dominate the Asia Pacific apnea monitors market with a 48% share, utilizing over 8.9 million units annually. These devices are used for continuous monitoring in ICUs and sleep labs, with usage penetration exceeding 75% in tertiary care facilities. Technical integration with hospital IT systems enhances patient data management and diagnostic accuracy.

Home care settings account for 34% of the market, with 6.3 million units deployed. The segment is growing rapidly due to rising demand for remote monitoring solutions, with adoption rates increasing by 28% annually. Devices used in home care offer wireless connectivity, smartphone integration, and battery life exceeding 20 hours.

Sleep clinics contribute 18% of the market, with 3.3 million units used annually. These facilities specialize in sleep disorder diagnostics, with advanced monitoring systems providing detailed respiratory analysis. Clinics report diagnostic accuracy levels above 95%, supporting early detection and treatment.

Asia Pacific Apnea Monitors Market Segmentations

Product Type

- Wearable Monitors

- Bedside Monitors

- Portable Monitors

Application

- Hospitals

- Home Care Settings

- Sleep Clinics

Asia Pacific Apnea Monitors Market Regional Outlook

China holds approximately 29% of the Asia-Pacific apnea-monitored, with production exceeding 5.6 million units annually. The country’s expanding healthcare infrastructure and increasing awareness campaigns have driven adoption rates to 35% in urban areas. Government investments in healthcare, exceeding USD 20 billion annually, further support market expansion.

South Korea accounts for 11% of the market, with advanced technology adoption rates exceeding 68%. The country produces over 2.1 million units annually, focusing on AI-integrated monitoring devices. Hospitals dominate usage with 55% share, followed by home care settings at 30%.

Japan leads with 32% share, producing over 5.4 million units annually. High healthcare spending (10.9% of GDP) and strong adoption of wearable technologies drive demand. The aging population significantly contributes to increased device usage.

India represents 13% of the market, with production of 2.5 million units. Rapid urbanization and increasing healthcare awareness have driven adoption rates to 25%. However, rural penetration remains below 15%, indicating growth potential.

Australia, Singapore, Taiwan, and South East Asia collectively account for 15% of the market, with combined production exceeding 3.1 million units. Advanced healthcare systems and rising adoption of telemedicine support regional growth.

Top players in Asia Pacific Apnea Monitors Market

- Philips Healthcare

- ResMed Inc.

- Fisher & Paykel Healthcare

- Medtronic plc

- Nihon Kohden Corporation

- GE Healthcare

- Drägerwerk AG

- Compumedics Limited

- Masimo Corporation

- BMC Medical Co. Ltd.

- Mindray Medical International

- Koninklijke Philips N.V.

- Philips Healthcare

-

-

Holds approximately 18% market share with strong presence in Japan and China

-

Focuses on advanced wearable monitors and AI integration, producing over 2 million units annually

-

-

ResMed Inc.

-

Accounts for nearly 15% market share with dominance in home care settings

-

Specializes in portable monitoring devices with 95% accuracy and global distribution networks

-

- Investment Analysis

- Investment in the Asia Pacific apnea monitor market has increased significantly, with total funding exceeding USD 8.5 billion between 2022 and 2026. Approximately 42% of investments are allocated to wearable technology development, while 28% focus on AI and data analytics integration. Regional investment distribution shows China and Japan accounting for 55%, followed by India at 18% and South Korea at 12%.

- Mergers and acquisitions have grown by 21%, with over 35 deals recorded since 2023. Collaborations between technology firms and healthcare providers have increased by 26%, enhancing innovation and market expansion. Joint ventures focusing on telemedicine integration have driven product adoption across home care settings.

- New Product Developments

- New product development in the Asia Pacific apnea monitor market has accelerated, with over 120 new devices launched between 2024 and 2026. Approximately 64% of these products feature AI-based diagnostics, improving detection accuracy by 12–18%. Battery efficiency has improved by 22%, while device weight has reduced by 30%, enhancing portability.

Recent Developments in the Asia-Pacific Apnea Monitors Market

- 2025: ResMed expanded manufacturing capacity by 18%, producing 1.8 million additional units for Asia-Pacific markets

- 2026: Medtronic invested USD 500 million in R&D, enhancing product efficiency by 17% and expanding regional presence

Research Methodology

The research methodology for the Asia Pacific apnea monitors market involves a combination of primary and secondary research approaches. Primary research includes interviews with over 50 industry experts, manufacturers, and healthcare professionals, providing insights into production volumes, adoption rates, and technological advancements. Secondary research involves analysis of company reports, government publications, and healthcare databases, covering over 100 data sources. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a 95% confidence interval. Data triangulation methods are applied to validate findings, incorporating historical data from 2022–2024 and forecasting trends up to 2034.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.