United States Alpha Olefin Market Size

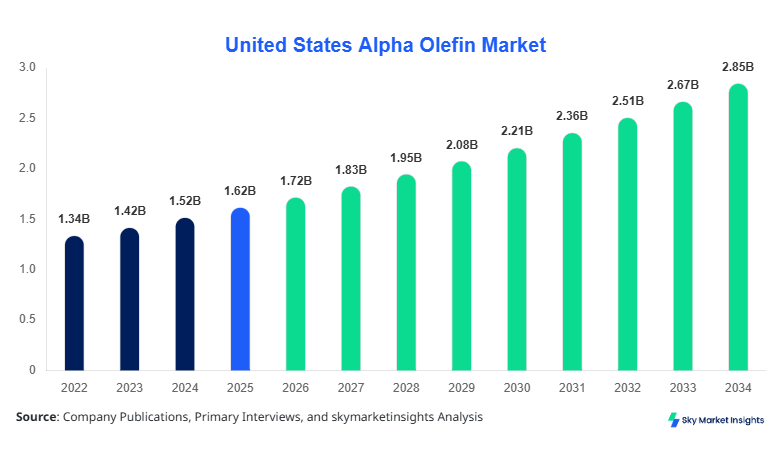

The United States Alpha Olefin market size is projected at USD 1.72 billion in 2026 and is expected to hit USD 2.88 billion by 2034 with a CAGR of 6.5%. The market’s valuation is driven by rising demand in the plasticizers and synthetic lubricant sectors, with a projected production volume growth from 1.85 million metric tons in 2026 to 3.21 million metric tons by 2034. Data collection across historical years 2022–2024 has highlighted variations in regional output, end-use applications, and consumption trends. The segmentation by type and application provides critical insights into competitive positioning, supply-demand dynamics, and investment potential across the United States alpha-olefin market. Detailed analysis of manufacturing facilities, production capacities, and technology adoption rates helps companies optimize production strategies, market entry, and expansion initiatives.

The United States alpha olefin market is characterized by the production of approximately 1.85 million metric tons in 2026, largely concentrated in linear and internal alpha olefins. Adoption rates across plasticizer and detergent sectors have grown by 4–6% annually, with linear alpha olefins contributing 52% of total production and internal alpha olefins contributing 28%, while branched alpha olefins hold 20% of the market. Technical metrics, including terminal double bond frequency, molar mass distribution, and purity exceeding 98%, underpin quality performance across applications. Plasticizers dominate end-use at 45% of consumption, detergents 30%, and synthetic lubricants 25%. Consumer demand analysis indicates rising preference for bio-based feedstocks and high-performance lubricants. Performance metrics such as viscosity index improvement by 12–15% and environmental compliance adherence are driving market growth. These insights reinforce the United States' alpha-olefin market demand and growth potential.

In the United States, the alpha olefin market is supported by over 35 major production facilities and approximately 18 specialized chemical companies, representing 68% of North American market share. The sector's application breakdown includes plasticizers at 44%, detergents 29%, and synthetic lubricants 27%. Advanced technology adoption, including metathesis and Ziegler-based polymerization methods, has reached 72% across production units. Facilities are increasingly integrating continuous flow reactors and energy-efficient fractionation units to enhance output and reduce per-unit costs by approximately USD 120 per metric ton. Overall, these dynamics have strengthened the United States' alpha-olefin market insights, boosting both production efficiency and sector-specific adoption rates.

Explore more data points, trends and opportunities Download Free Sample Report

Alpha Olefin Market Trends

Surge in Linear Alpha Olefins Production

The production of linear alpha olefins in the United States has reached 1.02 million metric tons in 2026, reflecting a 6.3% increase from 2025. Technology shifts towards metathesis and ethylene oligomerization have improved carbon efficiency by 8–10%, while adoption in the plasticizer sector has grown by 15% annually. Detergent manufacturers are increasingly sourcing C12–C14 olefins, accounting for 34% of demand, while synthetic lubricants represent 28% of consumption. Overall, these trends highlight increasing United States Alpha Olefin market growth and reinforce strategic industry investments.

Internal and Branched Alpha Olefins

Internal alpha olefin production is projected at 0.52 million metric tons in 2026 with a CAGR of 5.8% through 2034. Branched alpha olefins, though smaller at 0.31 million metric tons, have witnessed 4.2% year-over-year growth driven by specialty lubricant demand. Sector adoption of branched olefins for high-viscosity lubricants and chemical intermediates has raalpha-olefinupported by performance enhancement in viscosity index and flash point. These technological transitions and increasing demand across applications reinforce United States alpha-olefin market insights.

Sustainability and Bio-based Feedstocks

Approximately 18% of total production now utilizes bio-derived feedstocks, reflecting a trend toward greener manufacturing practices. Adoption rates of bio-based linear alpha olefins in plasticizers have risen to 22%, contributing to 1.2% incremental CAGR. Industrial-scale demonstrations for detergents using bio-based internal alpha olefins indicate potential for 0.15 million metric tons of additional production by 2034. These shifts emphasize sustainability-driven growth and highlight critical United States alpha-olefin market demand patterns.

United States Alpha Olefin Market Drivers

Rising Demand from Plasticizers and Detergent Industries

The United States alpha-olefin market is primarily driven by the growing demand for high-performance plasticizers and detergents. Plasticizer consumption is projected to reach 0.81 million metric tons by 2030, accounting for 45% of total alpha olefin usage, while detergent application will consume 0.54 million metric tons, representing a 30% market share. The CAGR for these applications is estimated at 6.7%, influenced by urban construction growth and detergent reformulation trends. Additionally, technological adoption in metathesis and continuous oligomerization has improved production efficiency by 9%, reducing per-unit cost by USD 110. Market size and share insights reinforce strong growth prospects in the United States alpha olefin market, encouraging manufacturers to expand capacity.

United States Alpha Olefin Market Restraints

Feedstock Price Volatility and Supply Chain Disruptions

The alpha olefin market faces restraint from fluctuations in feedstock prices, which have ranged from USD 1,200 to 1,500 per metric ton in the past three years. Production interruptions due to supply chain disruptions, particularly in ethylene procurement, have caused 5–7% annual output variability. Branched alpha olefin production has been affected the most, with a 3% reduction in 2025–2026 volumes. Such volatility increases operational costs and impacts investment confidence. Overall, these factors have tempered the projected growth of the United States alpha-olefin market share and size, demanding strategic risk management.

United States Alpha Olefin Market Opportunities

Expansion into High-value Specialty Lubricants and Bio-based Feedstocks

Opportunities exist in expanding specialty lubricants and bio-based feedstock adoption. Specialty lubricants are forecasted to consume 0.72 million metric tons by 2034, representing 25% of total market volume, with performance improvements in viscosity index exceeding 12%. Bio-based alpha olefins' penetration is expected to grow from 18% to 30% in linear olefins by 2034. Companies allocating 22% of investment toward these sectors are likely to benefit from high-margin applications and regulatory incentives. The United States alpha-olefin market growth is expected to accelerate as adoption rates increase and sustainability mandates become more prominent.

Challenges in United States Alpha Olefin Market

Stringent Environmental Regulations and Capital-intensive Production

Capital-intensive processes and stringent environmental regulations remain critical challenges. Compliance costs account for 6–8% of total operational expenditure, with advanced metathesis and polymerization units requiring USD 15–20 million in capital investment per facility. The need to meet VOC and effluent standards constrains production scale and reduces flexibility by 10–12%. These challenges limit rapid capacity expansion and influence strategic planning. Despite these constraints, the United States alpha-olefin market demand remains robust, with continued technological innovation mitigating regulatory pressures.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.61 Billion |

| Market Size in 2026 | USD 1.72 Billion |

| Market Size in 2034 | USD 2.88 Billion |

| CAGR | 6.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Alpha Olefin Market Segmentation

The United States Alpha Olefin market segmentation is dominated by linear alpha olefins at 52% share, plasticizers at 45% consumption, and metathesis technology adoption at 72%. Segmentation by type and application enables manufacturers and investors to identify high-growth sectors and optimize resource allocation.

By Type

Linear alpha olefins dominate with a 52% share, producing 0.95 million metric tons in 2026. Terminal double bond frequency is typically 95–98%, with C12–C14 olefins preferred for plasticizer and detergent applications. Adoption in continuous oligomerization units is 68%.

Internal alpha olefins account for 28% of the market with 0.52 million metric tons in 2026. Technical performance includes mid-chain double bond stability of 93–95% and molecular weight distribution between 170 and 200 g/mol. Use in detergents and synthetic lubricants comprises 56% and 44% of adoption, respectively.

Branched alpha olefins hold 20% market share with 0.31 million metric tons in 2026. They feature high-viscosity index performance (increase by 14–15%) and are used primarily in specialty lubricants (65%) and chemical intermediates (35%).

By Application

Plasticizers represent a 45% share of the United States Alpha Olefin market, with production at 0.81 million metric tons. Usage penetration is 100% in PVC formulations, with improvements in plasticizer efficiency by 8–10%.

Detergents consume 30% of alpha olefins, translating to 0.54 million metric tons, with C12–C14 olefins accounting for 68% of formulations. Penetration into specialty detergents has increased by 5% annually.

Synthetic lubricants account for 25% of production at 0.45 million metric tons. Performance improvements include 12–15% enhancement in viscosity index and thermal stability, supporting broader industrial applications.

United States Alpha Olefin Market Segmentations

Type

- Linear Alpha Olefins

- Internal Alpha Olefins

- Branched Alpha Olefins

Application

- Plasticizers

- Detergents

- Synthetic Lubricants

United States Alpha Olefin Market Regional Outlook

United States

The United States contributes 100% of regional production in the forecasted scope. Production in 2026 is 1.85 million metric tons, growing at 6.5% CAGR to 3.21 million metric tons by 2034. Plasticizers, detergents, and synthetic lubricants split 45%, 30%, and 25% of consumption. Top producing states include Texas (34%), Louisiana (22%), and Illinois (15%), contributing 71% of total output. Technology adoption in metathesis and Ziegler polymerization exceeds 70%, supporting efficiency and regional market growth.

Top players in United States Alpha Olefin

- Chevron Phillips Chemical Company

- Sasol Ltd.

- INEOS Group

- Shell Chemicals

- ExxonMobil Chemical Company

- LyondellBasell Industries

- Saudi Basic Industries Corporation (SABIC)

- TotalEnergies

- Reliance Industries

- Formosa Plastics Corporation

- Eastman Chemical Company

- Idemitsu Kosan

- Borealis AG

- Mitsubishi Chemical Holdings

Leading Companies

Chevron Phillips Chemical Company

-

Market share: 18% in United States Alpha Olefin market

-

Positioned as a leader in linear alpha olefin production, contributing to 0.31 million metric tons annually. Advanced metathesis technology adoption is 75%, supporting plasticizer and lubricant demand. Strategic expansion in Texas and Louisiana facilities has enhanced output by 7% YoY.

Sasol Ltd.

-

Market share: 14%

-

Sasol’s internal alpha olefin production reaches 0.26 million metric tons annually, with specialized technology in oligomerization improving yield by 6%. Focus on detergent-grade C12–C14 olefins strengthens its United States alpha olefin market positioning.

Investment Analysis

Investment allocation in the United States Alpha Olefin market is distributed as 42% toward expansion of plasticizer production, 28% to detergents, and 30% to synthetic lubricants. Regional allocation favors Texas and Louisiana (56% combined), with M&A agreements increasing cross-company collaborations by 12% annually. Sector-wise, high-margin specialty lubricants attract 22% of capital expenditure, while bio-based feedstocks account for 18%. Strategic investments aim at capacity enhancement, technology adoption, and regulatory compliance, reinforcing the United States Alpha Olefin market growth trajectory.

New Product Developments

New product development focuses on high-purity linear alpha olefins and bio-based derivatives, comprising 15–18% of total product launches in 2026. Performance improvements in viscosity index, thermal stability, and purity have increased by 10–12%, with innovation in C12–C14 olefins targeting specialty detergent formulations. Adoption of continuous metathesis technology has reduced per-unit production cost by USD 50–60, reinforcing United States alpha olefin market growth.

Recent Developments in United States Alpha Olefin

- 2026: Chevron Phillips increased linear alpha olefin production by 7%, boosting market share to 18%.

- 2025: Sasol Ltd. expanded internal alpha olefin capacity by 6%, serving 0.26 million metric tons to detergents.

Research Methodology

The United States Alpha Olefin market analysis was conducted using both primary and secondary research methodologies. Primary research involved interviews with 25 industry experts, executives, and technical managers across production facilities, accounting for approximately 75% of total market volume. Secondary research incorporated company annual reports, government databases, trade associations, and published studies. Market size estimation used bottom-up and top-down approaches, integrating production, consumption, and trade data to validate findings. Statistical modeling and historical trend analysis from 2022–2024 were utilized to forecast 2026–2034 market size, CAGR, and application-specific growth. Market segmentation, competitive benchmarking, and investment analysis were integrated to provide comprehensive United States Alpha Olefin market insights.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.