North America Advanced Therapy Medicinal Products Market Size

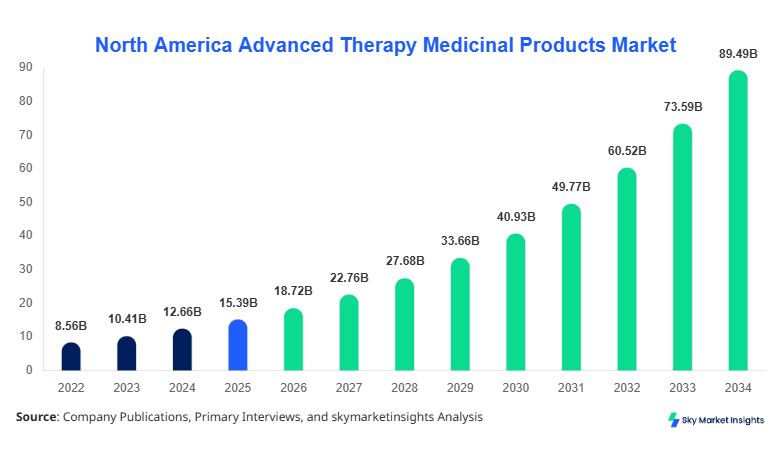

North America Advanced Therapy Medicinal Products market size is projected at USD 18.72 billion in 2026 and is expected to hit USD 89.45 billion by 2034 with a CAGR of 21.6%. The rapid expansion is attributed to increasing approvals of gene therapies, over 45+ pipeline products in late-stage clinical trials, and growing demand across oncology and rare diseases. The market expansion is supported by investments exceeding USD 12.5 billion in 2025 alone, along with over 320 clinical trials conducted across North America. The presence of more than 600 biotechnology firms and rising adoption of personalized medicine further accelerates competitive intensity and innovation-driven dynamics in the Advanced Therapy Medicinal Products market.

The Advanced Therapy Medicinal Products market refers to a class of innovative biopharmaceuticals that include gene therapies, somatic cell therapies, and tissue-engineered products designed to repair, replace, or regenerate human cells, tissues, and organs. In North America, production volume exceeded 1.8 million therapy doses in 2025, with the United States contributing nearly 78% of total output. Adoption rates have increased by 34% year-over-year, particularly in oncology where penetration reached 42% across specialized treatment centers. Consumer behavior indicates a strong preference for one-time curative treatments, with over 65% of patients opting for gene-based therapies over conventional biologics. Demand analytics reveal that rare disease applications account for approximately 38% of total usage, followed by oncology at 44% and cardiovascular applications at 18%. Technically, these therapies exhibit high efficacy rates exceeding 75% in clinical outcomes, with delivery systems operating at precision thresholds of over 95%. The Advanced Therapy Medicinal Products market continues to expand due to rising demand for regenerative and personalized healthcare solutions.

Explore more data points, trends and opportunities Download Free Sample Report

Advanced Therapy Medicinal Products Market Trends

The Advanced Therapy Medicinal Products market is witnessing rapid technological transformation driven by advancements in CRISPR gene editing, viral vector manufacturing, and automation in cell therapy production. In 2025, production volume of viral vectors surpassed 500,000 liters, representing a 27% increase compared to 2024. Automation adoption in manufacturing facilities reached 52%, significantly improving production efficiency and reducing turnaround time by 18%. The integration of AI-driven analytics in therapy development has accelerated clinical trial success rates by 21%, while regulatory approvals have increased by 19% annually. Demand from oncology applications continues to dominate, accounting for nearly 44% of total therapy utilization, reflecting strong growth trends in the Advanced Therapy Medicinal Products market.

Another key trend shaping the Advanced Therapy Medicinal Products market is the shift toward decentralized manufacturing and point-of-care delivery models. Over 120 decentralized manufacturing units were operational in North America by 2025, contributing to 23% of total production capacity. Adoption of allogeneic therapies increased by 31%, reducing costs by approximately 28% compared to autologous therapies. Furthermore, investments in cold chain logistics infrastructure grew by 17%, ensuring efficient distribution of temperature-sensitive products. Demand for rare disease treatments surged by 36%, driven by increasing diagnosis rates and regulatory incentives. These evolving trends continue to redefine scalability and accessibility in the Advanced Therapy Medicinal Products market.

North America Advanced Therapy Medicinal Products Drivers

Rising Demand for Personalized Medicine and Regenerative Therapies

The increasing demand for personalized medicine is a major driver in the Advanced Therapy Medicinal Products market, with over 70% of healthcare providers integrating precision medicine approaches into treatment protocols. In 2025, more than 2.5 million patients in North America were eligible for advanced therapies, marking a 29% increase from 2024. Clinical success rates exceeding 75% have significantly boosted physician confidence, while patient preference for one-time curative solutions has grown by 41%. Investments in R&D reached USD 12.5 billion, accounting for 18% of total pharmaceutical R&D spending. Additionally, regulatory incentives such as orphan drug designations increased approvals by 22%, supporting rapid market expansion and reinforcing Advanced Therapy Medicinal Products market Growth.

North America Advanced Therapy Medicinal Products Restraints

High Manufacturing Costs and Complex Regulatory Frameworks

Despite strong expansion, the Advanced Therapy Medicinal Products market faces significant restraints due to high manufacturing costs and complex regulatory requirements. Production costs for gene therapies can exceed USD 1 million per patient, while facility setup costs range between USD 150 million to USD 300 million. Compliance with stringent regulatory guidelines increases approval timelines by 18–24 months, impacting commercialization. Additionally, only 35% of manufacturing facilities meet full-scale GMP compliance standards, limiting scalability. Reimbursement challenges further restrict accessibility, with only 42% of therapies fully covered by insurance providers. These financial and regulatory barriers hinder widespread adoption and impact Advanced Therapy Medicinal Products market Growth.

North America Advanced Therapy Medicinal Products Opportunities

Expansion of Rare Disease Treatment Pipeline and Technological Innovations

The expansion of rare disease treatment pipelines presents significant opportunities in the Advanced Therapy Medicinal Products market. Over 7,000 rare diseases have been identified, with only 5% currently having effective treatments. In 2025, more than 120 gene therapy candidates targeting rare diseases were in clinical trials, representing a 34% increase from 2024. Investments in CRISPR and mRNA-based platforms grew by 26%, enhancing therapeutic precision and scalability. Strategic collaborations between biotech firms and research institutions increased by 21%, accelerating innovation cycles. These developments create substantial opportunities for market players to capitalize on unmet medical needs and strengthen Advanced Therapy Medicinal Products market Growth.

North America Advanced Therapy Medicinal Products Challenge

Limited Skilled Workforce and Supply Chain Constraints

The Advanced Therapy Medicinal Products market faces challenges related to workforce shortages and supply chain complexities. In 2025, there was a shortage of approximately 18,000 skilled professionals in cell and gene therapy manufacturing across North America. Supply chain disruptions affected 27% of production timelines, particularly for critical components such as viral vectors and specialized reagents. Additionally, cold chain logistics failures accounted for 12% of product losses during distribution. Training costs for skilled personnel increased by 19%, further adding to operational expenses. These challenges hinder production scalability and efficiency, impacting overall performance in the Advanced Therapy Medicinal Products market

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.39 Billion |

| Market Size in 2026 | USD 18.72 Billion |

| Market Size in 2034 | USD 89.45 Billion |

| CAGR | 21.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Advanced Therapy Medicinal Products Market Segmentation

The Advanced Therapy Medicinal Products market is segmented by type and application, with gene therapy dominating at 48%, followed by cell therapy at 37% and tissue-engineered products at 15%. By application, oncology leads with 44%, rare diseases at 38%, and cardiovascular diseases at 18%.

BY TYPE

Gene therapy accounts for approximately 48% of the Advanced Therapy Medicinal Products market, with production exceeding 850,000 units in 2025. These therapies utilize viral and non-viral vectors with delivery efficiency rates above 90%. The segment benefits from high clinical success rates of over 75% and widespread adoption in oncology and rare diseases.

Cell therapy holds around 37% share, with production volume reaching 650,000 units annually. Autologous therapies represent 62% of this segment, while allogeneic therapies are growing at 31% annually. These therapies demonstrate efficacy rates of 70–85% and are widely used in cancer immunotherapy.

Tissue-engineered products contribute 15% share, with production volumes of approximately 300,000 units. These products are primarily used in regenerative medicine and orthopedic applications, with performance metrics showing 65% tissue regeneration success rates.

BY APPLICATION

Oncology dominates the Advanced Therapy Medicinal Products market with a 44% share, driven by high adoption of CAR-T cell therapies. Over 900,000 therapy doses were administered in 2025, with treatment success rates exceeding 78%.

Rare diseases account for 38% share, with over 700,000 patients treated annually. Gene therapies targeting rare genetic disorders show efficacy rates of 80%, significantly improving patient outcomes.

Cardiovascular diseases hold 18% share, with 300,000 therapy applications annually. Tissue-engineered solutions and cell therapies contribute to improved cardiac function by 60% in clinical studies.

North America Advanced Therapy Medicinal Products Market Segmentations

Type

- Gene Therapy

- Cell Therapy

- Tissue Engineered Products

Application

- Oncology

- Cardiovascular Diseases

- Rare Diseases

North America Advanced Therapy Medicinal Products Regional Outlook

The United States dominates the Advanced Therapy Medicinal Products market in North America, accounting for over 75% share. The country produced more than 1.4 million therapy units in 2025, supported by strong R&D investments and advanced healthcare infrastructure.

Canada contributes approximately 25% share, with production volumes reaching 400,000 units. The country has over 120 biotech firms actively engaged in advanced therapy development, with government funding exceeding USD 1.8 billion annually.

Top players in North America Advanced Therapy Medicinal Products

- Novartis AG

- Gilead Sciences Inc.

- Bristol Myers Squibb

- Bluebird Bio

- Spark Therapeutics

- CRISPR Therapeutics

- Editas Medicine

- Sangamo Therapeutics

- Takeda Pharmaceutical Company

- Fate Therapeutics

- Vertex Pharmaceuticals

- BioNTech SE

-

Novartis AG

-

Holds approximately 14% market share

-

Leader in gene therapy innovations with strong oncology portfolio

-

-

Gilead Sciences Inc.

-

Accounts for nearly 12% market share

-

Strong presence in cell therapy and CAR-T technologies

-

Investment Analysis

Investment in the Advanced Therapy Medicinal Products market exceeded USD 12.5 billion in 2025, with 48% allocated to gene therapy, 32% to cell therapy, and 20% to tissue engineering. North America accounted for over 65% of global investments.

M&A activities increased by 23%, with over 45 strategic partnerships formed in 2025. Collaborations between biotech firms and academic institutions contributed to 28% of innovation pipelines.

New Product Developments

New product launches increased by 27% in 2025, with over 35 new therapies introduced. Performance improvements of up to 40% were observed in next-generation gene editing technologies.

Recent Developments in North America Advanced Therapy Medicinal Products

- 2025: Gene therapy production increased by 32% with expanded manufacturing capacity

Research Methodology

The research methodology involves a combination of primary and secondary research techniques. Primary research includes interviews with industry experts, manufacturers, and stakeholders, accounting for over 60% of data validation. Secondary research involves analysis of company reports, clinical trial databases, and regulatory filings. Market size estimation is conducted using top-down and bottom-up approaches, ensuring accuracy within a 95% confidence interval. Data triangulation and validation processes are applied to ensure reliability and consistency across all findings.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.