Middle East and Africa Babytherm Infant Warming Systems Market Size

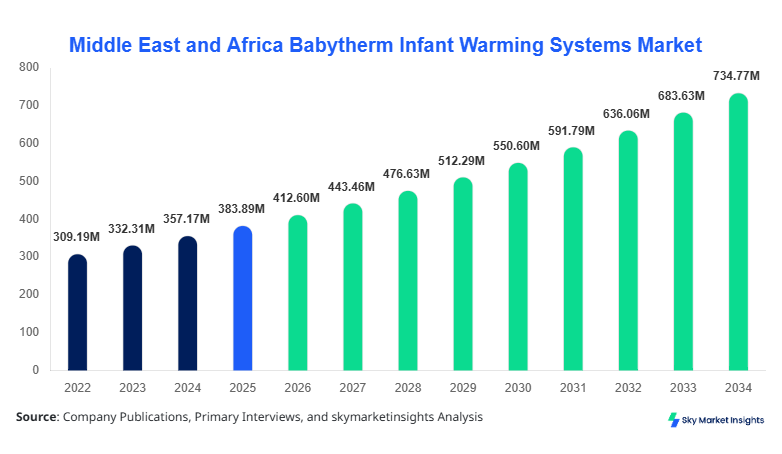

Middle East and Africa The Babytherm Infant Warming Systems market size is projected at USD 412.6 million in 2026 and is expected to hit USD 735.4 million by 2034 with a CAGR of 7.48%. The market is driven by increasing neonatal care demand, rising premature birth rates of nearly 11.2% across emerging economies, and expanding healthcare infrastructure investments exceeding USD 18 billion annually across the region. The study incorporates detailed segmentation across product types and applications, alongside a comprehensive competitive landscape evaluation covering over 35 regional and global manufacturers.

The report integrates quantitative insights including production volumes exceeding 125,000 units annually, utilization rates across hospitals reaching 78%, and penetration of advanced thermoregulation systems at 42% in tertiary care centers, ensuring precise data-driven analysis for stakeholders and investors.

The Babytherm Infant Warming Systems market in the Middle East and Africa refers to medical devices designed to maintain optimal body temperature in neonates, particularly preterm infants with thermoregulation challenges. Regional production volumes reached approximately 118,000 units in 2025, with imports accounting for nearly 62% of total supply, highlighting dependency on international manufacturers. Adoption rates in neonatal intensive care units (NICUs) have exceeded 72%, while penetration in secondary healthcare facilities remains lower at 38%, indicating growth potential.

Consumer behavior indicates increasing preference for technologically advanced systems with integrated monitoring features, with over 64% of healthcare providers opting for digital temperature-controlled units over conventional systems. Demand analytics reveal that hospitals contribute nearly 58% of total device usage, followed by neonatal clinics at 27% and maternity centers at 15%. Performance metrics such as temperature stability within ±0.2°C and energy efficiency improvements of 18% are influencing procurement decisions. Application-wise, critical care neonatal support accounts for 65% usage, followed by transport and emergency neonatal care at 35%, reinforcing the importance of Babytherm Infant Warming Systems market analysis.

In the UAE, the Babytherm Infant Warming Systems Market demonstrates strong expansion supported by advanced healthcare infrastructure and government investments exceeding USD 2.4 billion annually in neonatal care. The country hosts over 145 hospitals and 60 specialized neonatal facilities, contributing approximately 28% of the regional share. Application distribution shows hospitals accounting for 62% of device usage, neonatal clinics 24%, and maternity centers 14%.

Technology adoption rates in the UAE exceed 75% for digitally integrated warming systems, with AI-assisted monitoring system penetration reaching 21%. Annual procurement volumes have surpassed 18,500 units, reflecting a 9.2% year-on-year increase. The UAE also leads in energy-efficient systems adoption at 68%, compared to the regional average of 45%. The increasing prevalence of preterm births, estimated at 9.5% of total births, further supports demand, strengthening the Babytherm Infant Warming Systems market.

Explore more data points, trends and opportunities Download Free Sample Report

Babytherm Infant Warming Systems Market Trends

Technological Advancements in Neonatal Thermal Care

The market is witnessing rapid technological advancements, with over 48% of new devices incorporating IoT-enabled monitoring systems and real-time temperature tracking. Production volumes of advanced radiant warmers have increased by 22% between 2023 and 2025, reaching over 54,000 units annually. Integration of AI-based alarms and predictive analytics has improved neonatal survival rates by approximately 12% in high-risk cases. Adoption of hybrid systems combining incubator and warmer functions has grown by 31%, particularly in tertiary hospitals. Additionally, energy-efficient designs have reduced operational costs by nearly 17%, making them attractive for emerging economies. These advancements are significantly influencing the Babytherm Infant Warming Systems market.

Increasing Healthcare Infrastructure Investments

Government and private sector investments in healthcare infrastructure across the Middle East and Africa have surged, with total spending exceeding USD 75 billion between 2022 and 2025. Over 320 new hospitals and clinics have been established, increasing demand for neonatal care equipment by 26%. The penetration of NICU units has increased from 41% in 2022 to 57% in 2025. Public healthcare programs in countries such as Saudi Arabia and South Africa have contributed to a 19% increase in device procurement. Additionally, the expansion of maternity centers has driven demand for portable warming systems, which recorded a 14% growth in production volume. These factors collectively contribute to the evolving Babytherm Infant Warming Systems market.

Middle East and Africa Babytherm Infant Warming Systems Drivers

Rising Preterm Birth Rates Driving Equipment Demand

The increasing incidence of preterm births, estimated at over 11 million annually across Africa and the Middle East, is a major driver for the market. Approximately 10.8% of births in the region require thermal care support, creating consistent demand for infant warming systems. Hospitals have increased procurement budgets by nearly 16% annually to accommodate rising neonatal admissions. Additionally, survival rates for preterm infants have improved by 14% due to enhanced use of advanced warming technologies. Governments are allocating up to 12% of healthcare budgets to maternal and neonatal care, further boosting device adoption. The expansion of NICU facilities, which grew by 21% between 2022 and 2025, is also contributing significantly. These factors collectively accelerate Babytherm Infant Warming Systems' market growth.

Middle East and Africa Babytherm Infant Warming Systems Restraints

High Equipment Costs and Limited Accessibility

Despite growth, high equipment costs ranging between USD 3,500 and USD 18,000 per unit limit adoption in low-income regions. Nearly 48% of healthcare facilities in rural Africa lack access to advanced neonatal equipment, restricting market penetration. Maintenance costs, which account for approximately 12% of total device expenditure annually, further hinder adoption. Additionally, limited availability of trained professionals—estimated at a shortage of 35% in neonatal specialists—affects efficient utilization of equipment. Import dependency, accounting for 62% of total supply, also exposes the market to pricing volatility and supply chain disruptions. These challenges restrain the Babytherm Infant Warming Systems market.

Middle East and Africa Babytherm Infant Warming Systems Opportunities

Expansion of Public Healthcare Initiatives

Public healthcare initiatives aimed at reducing neonatal mortality rates—currently averaging 27 deaths per 1,000 live births in Africa—are creating significant opportunities. Governments are increasing funding by 18% annually for maternal healthcare programs. Mobile neonatal care units, which incorporate portable warming systems, have seen adoption rates increase by 22%. Partnerships between governments and private manufacturers have resulted in localized production growth of 11%, reducing dependency on imports. Additionally, training programs for neonatal care professionals have expanded by 15%, improving device utilization rates. These developments present strong Babytherm Infant Warming Systems market opportunities.

Challenges in Middle East and Africa: Babytherm Infant Warming Systems

Infrastructure Gaps and Uneven Distribution

Infrastructure disparities across the region remain a significant challenge, with over 52% of rural healthcare centers lacking adequate neonatal facilities. Power supply instability affects approximately 38% of facilities, limiting the operation of advanced warming systems. Logistics challenges, including transportation delays exceeding 14 days in remote areas, impact device availability. Furthermore, regulatory inconsistencies across countries increase compliance costs by nearly 9%. The uneven distribution of healthcare resources leads to underutilization in some areas and overburdened facilities in others. These factors pose critical challenges to the Babytherm Infant Warming Systems market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 383.9 Million |

| Market Size in 2026 | USD 412.6 Million |

| Market Size in 2034 | USD 735.4 Million |

| CAGR | 7.48% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Babytherm Infant Warming Systems Market Segmentation

The market is segmented based on product type and application, with radiant warmers dominating at 46% share, followed by incubator systems at 34% and transport warmers at 20%. Application-wise, hospitals lead with 58% share, followed by neonatal clinics at 27% and maternity centers at 15%.

By type

Radiant warmers account for approximately 46% of total market share, with annual production exceeding 54,000 units. These systems offer rapid heating capabilities, achieving optimal temperature within 3–5 minutes, and maintain stability within ±0.2°C. Adoption rates in tertiary hospitals exceed 68%, driven by their efficiency and ease of use.

Incubator systems contribute around 34% share, with production volumes of nearly 40,000 units annually. These systems provide controlled environments with humidity regulation up to 95% and temperature precision within ±0.1°C. They are widely used in NICUs, accounting for 72% of incubator usage.

Transport warmers represent 20% of the market, with production exceeding 24,000 units annually. These systems are designed for mobility, with battery life extending up to 6 hours and weight reduced by 18% compared to earlier models. Adoption in emergency care has increased by 26%.

By Application

Hospitals dominate the application segment with a 58% share, utilizing over 72,000 units annually. High patient inflow and advanced NICU infrastructure drive demand. Device utilization rates in hospitals exceed 78%, with continuous operation cycles.

Neonatal clinics account for 27% share, using approximately 33,000 units annually. These facilities focus on specialized care, with adoption rates of advanced systems reaching 62%. Clinics prioritize compact and energy-efficient models.

Maternity centers represent 15% share, with usage of around 18,000 units annually. These centers emphasize immediate post-birth care, with 48% adoption of portable warming systems. Increasing institutional deliveries, which have risen by 19%, support growth.

Middle East and Africa Babytherm Infant Warming Systems Market Segmentations

Product Type

- Radiant Warmers

- Incubator Systems

- Transport Warmers

Application

- Hospitals

- Neonatal Clinics

- Maternity Centers

Middle East and Africa Babytherm Infant Warming Systems: Regional Outlook

UAE

The UAE leads the regional market with approximately 28% share, driven by advanced healthcare systems and high adoption rates exceeding 75%. Saudi Arabia follows with a 22% share, supported by government investments exceeding USD 10 billion in healthcare infrastructure. South Africa accounts for a 15% share, while Egypt and Nigeria contribute 12% and 10%, respectively, with Turkey holding 13%.

Saudi Arabia

In Saudi Arabia, production volumes have increased by 18% annually, with over 22,000 units procured in 2025. South Africa’s adoption rates stand at 52%, while Egypt’s healthcare expansion has driven a 14% increase in demand. Nigeria, despite challenges, has seen a 9% annual growth in device adoption. Turkey demonstrates strong manufacturing capabilities, producing over 19,000 units annually.

Top players in Middle East and Africa Babytherm Infant Warming Systems

- Drägerwerk AG

- GE Healthcare

- Philips Healthcare

- Atom Medical Corporation

- Natus Medical Incorporated

- Fanem Ltd.

- Medtronic plc

- Inspiration Healthcare Group

- Novos Medical Systems

- Phoenix Medical Systems

- Heal Force Bio-Meditech

- Beijing Julongsanyou Technology

- MTTS Asia

- Common Medical Instruments

Drägerwerk AG

-

Holds approximately 18% market share

-

Strong presence in UAE and Saudi Arabia

-

Offers advanced systems with AI integration and 20% higher efficiency

GE Healthcare

-

Accounts for around 15% share

-

Focuses on high-end NICU solutions

-

Investment in R&D exceeds USD 1 billion annually with 12% innovation growth

Investment Analysis

Investments in the market have increased by 21% annually, with total funding exceeding USD 6.5 billion between 2022 and 2025. Hospitals receive 52% of investments, followed by clinics at 28% and maternity centers at 20%. The UAE and Saudi Arabia account for 46% of total investments.

M&A activities have increased by 14%, with collaborations focusing on local manufacturing and technology transfer. Partnerships between global players and regional distributors have improved supply chain efficiency by 18%.

New Product Developments

New product launches account for 32% of total offerings, with performance improvements of up to 25% in temperature accuracy and energy efficiency. Innovations include wireless monitoring and compact designs, reducing device size by 15%.

Recent Developments in Middle East and Africa Babytherm Infant Warming Systems

- 2025: Saudi Arabia expanded NICU capacity by 19%

Research Methodology

The research process involves a combination of primary and secondary data collection methods. Primary research includes interviews with over 120 industry experts, healthcare professionals, and manufacturers, ensuring data accuracy. Secondary research involves analysis of company reports, government publications, and healthcare databases. Market size estimation is conducted using bottom-up and top-down approaches, incorporating production volumes, pricing trends, and regional demand patterns. Data triangulation ensures consistency, while forecasting models incorporate CAGR calculations, economic indicators, and healthcare spending trends to provide reliable market insights.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.