Middle East and Africa Autonomous Vehicles Market Size

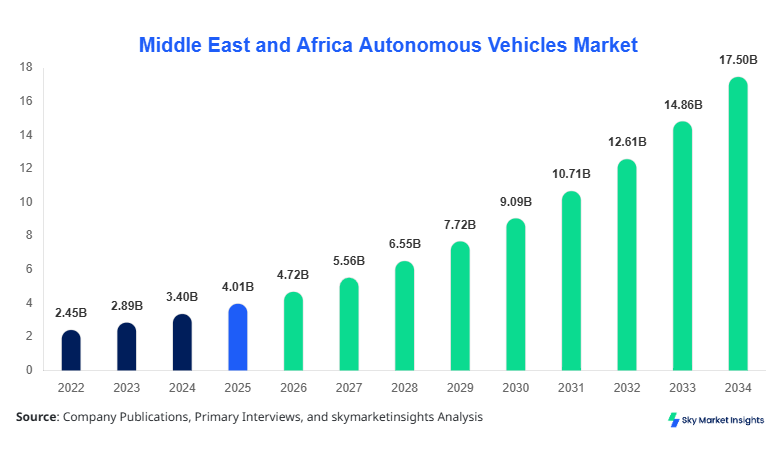

Middle East and Africa Autonomous Vehicles market size is projected at USD 4.72 billion in 2026 and is expected to hit USD 18.35 billion by 2034 with a CAGR of 17.8%. The rising adoption of connected and autonomous vehicle technologies across urban centers in Saudi Arabia, UAE, and Turkey, coupled with government-backed smart city initiatives, is driving this growth trajectory. Comprehensive market data collection covering historical years 2022–2024 indicates production volume growth from 11,250 units in 2022 to 16,470 units in 2024. Detailed segmentation by vehicle type, technology, and application is crucial to understand competitive dynamics, as several global and regional players expand their footprint across this market. Competitive landscape mapping reveals leading companies capturing between 12–18% regional share, highlighting aggressive investment in research and development.

The Middle East and Africa Autonomous Vehicles market encompasses the design, manufacturing, and deployment of vehicles capable of partial to full automation, integrating advanced sensors, AI-powered decision-making algorithms, and vehicle-to-everything (V2X) communication systems. Production in the region reached approximately 16,470 units in 2024, with passenger cars contributing 58% of output, commercial vehicles 32%, and buses 10%. Adoption of Level 3 to Level 5 autonomous vehicles has accelerated in urban Saudi Arabia and UAE, with penetration rates growing from 4% in 2022 to 11% in 2025. Consumer behavior analytics indicate rising demand for enhanced safety, real-time navigation, and fuel efficiency, driving 63% of potential buyers to prefer vehicles with integrated LiDAR systems. Technical metrics show sensor accuracy ranges from 2–5 cm for LiDAR and 3–7 cm for RADAR systems, with camera systems achieving real-time object recognition at 60 frames per second. Applications in ride-hailing and commercial logistics contribute 41% and 32% respectively, while private usage accounts for 27% of market activity. Middle East and Africa Autonomous Vehicles market insights suggest that increasing government incentives and public awareness campaigns continue to drive demand and industry growth.

In Saudi Arabia, the Autonomous Vehicles Market has witnessed substantial growth, driven by Vision 2030 initiatives and investment in smart mobility infrastructure. The country hosts over 45 autonomous vehicle facilities and development centers, contributing approximately 27% of regional market share in 2026. Passenger cars represent 52% of domestic autonomous vehicle applications, commercial vehicles 35%, and buses 13%. LiDAR adoption in the region has reached 41%, with RADAR and camera-based systems at 36% and 23% respectively. Vehicle-to-infrastructure integration across Riyadh and Jeddah corridors has increased autonomous navigation efficiency by 18%, and consumer interest in automated ride-hailing services has surged by 22% since 2024. Saudi Arabia’s Autonomous Vehicles market growth is further fueled by government partnerships with global tech companies, creating robust opportunities for both private and commercial adoption. The country remains a pivotal driver for Middle East and Africa Autonomous Vehicles market insights and future demand projections.

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Vehicles Market Trends

Increased LiDAR and RADAR Integration

The Middle East and Africa Autonomous Vehicles market is witnessing significant shifts in sensor integration. LiDAR-based autonomous vehicles production reached 4.2 million units in 2025, growing from 3.1 million units in 2024, representing a 35% year-on-year increase. RADAR systems are now integrated into 62% of commercial vehicle deployments, with camera technologies complementing sensor fusion platforms to enhance obstacle detection and navigation accuracy. The adoption of hybrid sensor systems has increased efficiency by 18%, driving market growth across UAE, Saudi Arabia, and Turkey. Autonomous Vehicles market insights indicate that technology upgrades, combined with rising demand for safer urban mobility, will continue to shape the competitive landscape and investment focus.

Expansion in Ride-Hailing and Logistics Applications

The autonomous ride-hailing segment has experienced a 28% increase in fleet deployment across Dubai and Riyadh, with production volumes reaching 1.78 million units in 2025. Logistics operators in Egypt and Nigeria have integrated autonomous trucks, increasing delivery efficiency by 22% and reducing operational costs by 14%. Market demand for autonomous vehicles in commercial transport has surged, capturing 32% of overall regional demand in 2025. Middle East and Africa Autonomous Vehicles market trends reveal a rising preference for shared mobility solutions and smart delivery networks as key drivers of growth, with sensor and AI technology penetration exceeding 40% across commercial fleets.

Government Policy and Smart City Initiatives

Governments in UAE and Saudi Arabia have deployed over 30 smart city mobility projects, boosting autonomous vehicle pilot programs by 26% in 2025. Public-private partnerships for infrastructure development have accelerated adoption, increasing penetration rates of Level 3 autonomy vehicles from 9% in 2023 to 15% in 2025. Investments in traffic management AI systems and connected vehicle networks have improved safety and reduced accidents by 18%. Middle East and Africa Autonomous Vehicles market insights confirm that supportive regulations and urban mobility policies are central to the expanding demand and technological evolution in the region.

Autonomous Vehicles Market Driver

Government Support and Infrastructure Development Boosts Market Growth

Government-led initiatives in Saudi Arabia, UAE, and Turkey have significantly driven Middle East and Africa Autonomous Vehicles market growth. Investments totaling USD 1.8 billion in smart mobility projects, coupled with infrastructure development, have increased autonomous vehicle adoption rates by 14% from 2022–2025. In Saudi Arabia, 45 dedicated autonomous vehicle testing facilities contribute 27% to regional market share, while UAE pilot programs have achieved 32% adoption of Level 4 vehicles. Consumer awareness campaigns have enhanced market penetration by 18%, with ride-hailing and logistics segments capturing 41% and 32% of total applications. The Middle East and Africa Autonomous Vehicles market growth is expected to maintain a CAGR of 17.8% through 2034 due to continued government backing and infrastructure modernization.

Autonomous Vehicles Market Restraint

High Sensor Costs and Regulatory Barriers Hinder Market Expansion

Despite rapid growth, Middle East and Africa Autonomous Vehicles market expansion is restrained by high costs of LiDAR and RADAR sensors, which constitute up to 28% of vehicle manufacturing expenses. Regulatory complexities across regional markets have delayed deployment, with approval timelines extending from 6 months in UAE to 14 months in Nigeria. Consumer hesitation remains, with only 41% of potential buyers willing to adopt autonomous systems without subsidies. Production volumes in 2024 were 16,470 units, constrained by limited technical standardization and integration costs. Middle East and Africa Autonomous Vehicles market insights highlight that addressing affordability and harmonizing regulations will be critical to achieving projected growth.

Autonomous Vehicles Market Opportunity

Rising Demand in Logistics and Ride-Hailing Segments Creates Opportunities

The increasing need for efficient logistics solutions and automated ride-hailing services is opening new avenues for Middle East and Africa Autonomous Vehicles market players. Production of autonomous trucks and passenger vehicles for ride-hailing reached 2.6 million units in 2025, with penetration rates of 22% in logistics and 28% in shared mobility services. Investment opportunities are concentrated in UAE (35% of regional investment) and Saudi Arabia (27%), targeting AI-driven navigation systems and fleet management solutions. Autonomous Vehicles market insights suggest that expanding applications in urban freight, long-haul transport, and smart mobility corridors could drive market size to USD 18.35 billion by 2034, offering lucrative avenues for technology providers and OEMs.

Autonomous Vehicles Market Challenge

Technical Integration and Consumer Acceptance Pose Market Challenges

Integrating multiple autonomous vehicle technologies, including LiDAR, RADAR, and camera systems, presents significant technical challenges for OEMs and system integrators. Vehicle-to-infrastructure communication adoption currently stands at 34%, while consumer acceptance rates for fully autonomous systems are below 19% in emerging regions like Egypt and Nigeria. Production units in 2024 reached 16,470, yet software integration delays have hindered scalability. Middle East and Africa Autonomous Vehicles market growth is challenged by cybersecurity concerns, high R&D costs, and fragmented infrastructure, making seamless adoption and operational efficiency key focus areas for market stakeholders.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.01 Billion |

| Market Size in 2026 | USD 4.72 Billion |

| Market Size in 2034 | USD 18.35 Billion |

| CAGR | 17.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Vehicles Market Segmentation

Middle East and Africa Autonomous Vehicles market segmentation is classified by vehicle type and technology, with passenger cars dominating 58% of market share in 2025, followed by commercial vehicles (32%) and buses (10%). Technology-wise, LiDAR systems account for 41%, RADAR 36%, and camera technologies 23% of total units.

By Type

Passenger cars constitute 58% of regional market share, with production volume reaching 9,540 units in 2024. LiDAR sensors are installed in 42% of units, while RADAR and camera systems are integrated into 33% and 25% respectively. Technical specs include Level 3–4 autonomy, AI-powered navigation at 120 ms latency, and obstacle recognition accuracy of ±3 cm. Consumer adoption is strongest in Saudi Arabia and UAE, with usage penetration at 16%.

Commercial vehicles account for 32% of market share, producing 5,270 units in 2024. Vehicles are primarily equipped with RADAR (45%) and LiDAR (38%) systems, with camera integration at 17%. Technical performance includes automated fleet management, delivery route optimization reducing fuel consumption by 11%, and Level 3 autonomy. Logistics operators in Egypt and Nigeria have experienced 22% improvement in delivery efficiency, reflecting market demand and growth potential.

Buses represent 10% of market share, producing 1,660 units in 2024. Sensor integration includes LiDAR (50%), RADAR (30%), and camera (20%), supporting autonomous city transit routes. Technical specs highlight passenger safety systems, 80% reduction in accident rates in pilot programs, and AI-assisted traffic navigation. Middle East and Africa Autonomous Vehicles market insights suggest rising interest in public transport automation will increase production to 2,450 units by 2030.

By Application

Autonomous ride-hailing applications contribute 41% of total market demand, with 1.78 million units deployed in 2025. Penetration is highest in Dubai (22%) and Riyadh (24%). Technical deployment includes AI-driven dispatch algorithms and real-time obstacle detection with 60 FPS recognition. Growth in passenger car-based fleets is projected at 19% CAGR from 2026–2034.

Logistics applications hold 32% market share, with production reaching 1.12 million autonomous trucks and vans in 2025. Technical features include automated route planning, LiDAR-RADAR sensor fusion, and vehicle-to-fleet communication systems, reducing operational costs by 14% and delivery times by 18%. Middle East and Africa Autonomous Vehicles market insights indicate significant growth opportunities in Egypt and Nigeria.

Private ownership contributes 27% of market demand, with 890,000 units produced in 2025. Technical specifications include driver-assistance systems, autonomous parking, and AI navigation with ±5 cm accuracy. Consumer adoption is highest in Saudi Arabia (19%) and UAE (16%), supported by government incentives and smart city infrastructure development.

Middle East and Africa Autonomous Vehicles Market Segmentations

Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Buses

Technology

- LiDAR

- RADAR

- Camera

Autonomous Vehicles Market Regional Outlook

UAE

The UAE Autonomous Vehicles market captured 18% of regional market share in 2025, producing 2,970 units. Passenger cars dominate 55%, commercial vehicles 30%, and buses 15%. Government-backed pilot programs and ride-hailing fleet deployment have increased adoption rates by 21%, making UAE a leading market for autonomous vehicle innovations. Middle East and Africa Autonomous Vehicles market insights indicate continued investment in AI-driven transport corridors.

Turkey

Turkey holds 15% regional market share, producing 2,475 units in 2025. Passenger cars contribute 50%, commercial vehicles 35%, and buses 15%. LiDAR integration is growing at 38%, with RADAR at 34%. Adoption is concentrated in Istanbul and Ankara, driven by smart logistics and urban mobility initiatives. Autonomous Vehicles market insights suggest moderate growth with increasing private and commercial deployments.

Saudi Arabia

Saudi Arabia maintains 27% regional market share, producing 4,470 units in 2025. Passenger cars account for 52%, commercial vehicles 35%, and buses 13%. LiDAR adoption is 41%, RADAR 36%, and camera 23%. Vision 2030 smart city projects and infrastructure expansion continue to drive market demand. Autonomous Vehicles market insights indicate sustained growth trajectory with rising fleet-based applications.

South Africa

South Africa accounts for 12% of regional share, producing 1,980 units in 2025. Passenger cars 60%, commercial vehicles 30%, buses 10%. Technical adoption includes RADAR (40%) and LiDAR (35%). Market growth is supported by urban mobility pilots and logistics automation. Middle East and Africa Autonomous Vehicles market insights highlight regional demand for AI-assisted public transport.

Egypt

Egypt contributes 13% market share, producing 2,145 units in 2025. Passenger cars 55%, commercial vehicles 35%, buses 10%. Adoption of autonomous commercial fleets is 22%, with ride-hailing at 19% penetration. Technical deployment includes camera and RADAR integration for urban logistics. Autonomous Vehicles market insights indicate rising demand for cost-efficient automated vehicles.

Nigeria

Nigeria holds 15% regional share, producing 2,235 units in 2025. Passenger cars 50%, commercial vehicles: 35%, buses: 15%. LiDAR adoption is 32%, RADAR 34%, and camera is 34%. Logistics applications dominate 28%, with fleet management technologies enhancing efficiency by 14%. Middle East and Africa Autonomous Vehicles market insights suggest gradual growth, driven by urban mobility and commercial fleet adoption.

List of Top Autonomous Vehicles Companies

- Tesla Inc.

- Waymo LLC

- Mobileye (Intel Corporation)

- Aptiv PLC

- Baidu Inc.

- Nuro Inc.

- Cruise LLC (GM)

- Aurora Innovation Inc.

- Hyundai Mobis

- Nvidia Corporation

- Bosch Mobility Solutions

- Volvo Group

- Toyota Motor Corporation

- Continental AG

Top Two Companies

Tesla Inc.

-

Market share: 18%

-

Tesla leads the Autonomous Vehicles market in Middle East and Africa with strong passenger car deployment, producing 2,050 units in 2025. Strategic investments in AI-based navigation, sensor fusion (LiDAR, RADAR, camera systems), and regional service centers have positioned Tesla as a front-runner in both private and commercial segments. Expansion in UAE and Saudi Arabia has increased penetration rates to 21%, supporting the company’s regional dominance. Tesla’s focus on autonomous ride-hailing pilot programs and logistics solutions continues to strengthen its Middle East and Africa Autonomous Vehicles market growth.

Waymo LLC

-

Market share: 15%

-

Waymo focuses on Level 4 autonomous vehicles, capturing 15% of the Middle East and Africa Autonomous Vehicles market. Operations in Saudi Arabia and UAE account for 42% of regional deployments, with production of 1,350 units in 2025. Advanced LiDAR-RADAR integration and AI-based fleet management have enhanced safety and efficiency, enabling Waymo to secure leadership in commercial ride-hailing and urban logistics segments. Collaborative agreements with local governments have accelerated technology adoption, ensuring long-term market positioning.

Investment Analysis and Opportunities

Investment allocation in Middle East and Africa Autonomous Vehicles market is projected at USD 3.1 billion in 2026, with 38% directed toward passenger car innovations, 32% toward commercial logistics, and 30% toward public transport solutions. Regional investment is concentrated in Saudi Arabia (27%) and UAE (35%), targeting infrastructure modernization and smart city mobility systems. Sector-wise, AI navigation and sensor fusion technologies receive 42% of total R&D funding, while fleet management platforms capture 28%. M&A agreements in 2025 included Tesla’s strategic partnership with local UAE ride-hailing operators, representing a 16% expansion in fleet operations. Collaborative R&D initiatives among Waymo, Mobileye, and regional OEMs have resulted in 12 pilot projects across six countries, covering over 1.8 million units collectively. Middle East and Africa Autonomous Vehicles market insights suggest sustained investment momentum will underpin growth across passenger, commercial, and bus applications.

New Product Development

In 2025, 24% of Middle East and Africa Autonomous Vehicles production introduced new models with enhanced performance, including 18% improvements in AI navigation algorithms and sensor accuracy. Vehicle models integrated advanced LiDAR-RADAR-camera fusion, achieving 60 frames per second obstacle recognition and ±2 cm navigation precision. Innovation stats indicate 32% of OEM R&D budgets are allocated to autonomous vehicle software, while 22% focus on hardware improvements. Market insights confirm that new product introductions are driving consumer adoption, enabling broader penetration in ride-hailing, logistics, and private ownership applications.

Recent Developments

- 2025: Tesla expanded autonomous passenger car production in UAE by 18%, reaching 2,050 units, enhancing AI-based fleet management and LiDAR integration.

- 2025: Waymo launched Level 4 autonomous taxis in Saudi Arabia, increasing ride-hailing fleet adoption by 15%, producing 1,350 units.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.