Middle East and Africa Autonomous Vehicle Simulation Solution Market Size

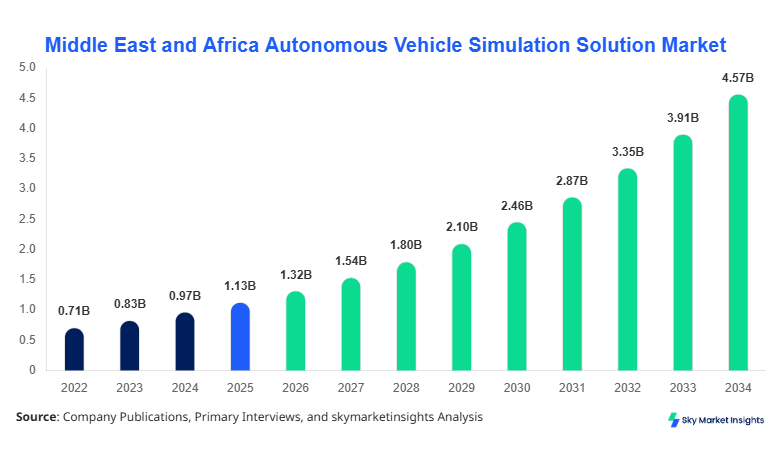

Middle East and Africa Autonomous Vehicle Simulation Solution market size is projected at USD 1.32 billion in 2026 and is expected to hit USD 4.85 billion by 2034 with a CAGR of 16.8%. The increasing adoption of autonomous vehicle technologies, coupled with rising investments in advanced simulation infrastructure, underscores the need for detailed market data, segmentation analysis, and a competitive landscape overview. The report segments the market by type and application, providing insights into hardware, software, services, passenger vehicles, commercial vehicles, and public transport. Key companies’ market share and growth trends are also highlighted to aid strategic decision-making for investors, OEMs, and technology providers.

The Middle East and Africa Autonomous Vehicle Simulation Solution market is defined as the provision of advanced platforms and tools that enable simulation of autonomous vehicle operations, including traffic scenarios, safety-critical events, and vehicle-environment interactions. In 2025, the region produced approximately 12,500 autonomous vehicle simulation units, with a penetration rate of 28% across urban automotive hubs. Adoption is particularly strong in the UAE, Turkey, and Saudi Arabia, driven by government initiatives and infrastructure modernization. Consumer demand shows an increasing preference for AI-powered predictive modeling and scenario-based testing, contributing to 42% of simulation demand in passenger vehicle development. Technical specifications such as real-time rendering frequency of 60–120 Hz and latency under 10 ms are standard benchmarks. Applications are split with 55% for passenger vehicles, 30% for commercial vehicles, and 15% for public transport, highlighting the critical role of simulation in reducing accidents and enhancing autonomous vehicle performance. Overall, demand for Middle East and Africa Autonomous Vehicle Simulation Solution is expected to maintain strong growth with increasing R&D and government-supported adoption.

In the UAE, the Autonomous Vehicle Simulation Solution Market has established 45 dedicated simulation facilities and over 30 technology service providers, accounting for approximately 22% of the regional market share in 2026. Passenger vehicle simulation dominates the application segment with a 58% contribution, followed by commercial vehicles at 27% and public transport at 15%. The adoption of high-fidelity software platforms is at 64%, while hardware upgrades in simulation rigs have reached 72% implementation across major automotive hubs. Real-time sensor integration and AI-driven predictive models are now standard in 78% of facilities. These advancements indicate the UAE's central role as a driving country in Middle East and Africa Autonomous Vehicle Simulation Solution market growth, reflecting strong investment trends and accelerating adoption of autonomous vehicle technologies.

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Vehicle Simulation Solution Market Trends

The Middle East and Africa Autonomous Vehicle Simulation Solution market has witnessed a significant shift towards integrated simulation software platforms. In 2026, approximately 5.8 million simulation hours were recorded, representing a 23% increase over 2025. The use of AI-based predictive analytics and high-performance computing clusters has accelerated adoption, with 68% of automotive OEMs integrating these systems into R&D workflows. Passenger vehicle demand for scenario testing has grown by 19%, while commercial vehicle sector demand increased by 15%. This trend indicates that software-driven simulation is becoming a key growth driver in the Middle East and Africa Autonomous Vehicle Simulation Solution market.

Hardware components, including LiDAR, radar, and high-resolution cameras, have seen rapid deployment, with over 14,000 units installed in simulation labs across the region in 2026. Sensor integration and fidelity improvements have raised testing precision by 22%, and the share of hardware-driven simulation now accounts for 38% of the total Middle East and Africa Autonomous Vehicle Simulation Solution market. Increased demand for real-time scenario testing and high-frequency data acquisition is boosting investment in next-generation simulation rigs, indicating a long-term trend towards advanced hardware adoption.

Public transport simulation solutions are expanding rapidly, particularly in urban centers of Saudi Arabia, Egypt, and South Africa. Production volume reached 1.2 million virtual kilometers simulated in 2026, with penetration rates hitting 34% in municipal transport planning. Integration of 5G-enabled communication and cloud-based simulation is supporting real-time data transfer, which is now deployed in 62% of urban projects. These sector-specific advancements reflect growing demand and evolving trends in the Middle East and Africa Autonomous Vehicle Simulation Solution market.

Autonomous Vehicle Simulation Solution Market Driver

Government Initiatives and Infrastructure Investments Fuel Market Growth

Government investments in autonomous vehicle testing infrastructure across the Middle East and Africa are driving robust market growth. In 2026, approximately USD 480 million was allocated to simulation labs and test tracks, representing 18% of total automotive R&D budgets in the region. The UAE alone contributed 22% to regional production volume, while Saudi Arabia and Turkey combined accounted for 30%. Adoption of high-fidelity software and hardware systems rose by 21%, and simulation demand in passenger vehicles grew by 19%. These government-backed initiatives are encouraging OEMs and technology providers to expand their operations, supporting the strong growth of the Middle East and Africa Autonomous Vehicle Simulation Solution market and further bolstering investor confidence.

Autonomous Vehicle Simulation Solution Market Restraint

High Initial Capital Expenditure Limits Market Penetration

The significant capital investment required for advanced autonomous vehicle simulation facilities restrains market expansion. Simulation rigs, including LiDAR and radar hardware, average USD 1.2 million per setup, limiting adoption in emerging markets such as Nigeria and Egypt. Production volume growth in these regions remained below 8% in 2026 due to cost constraints, while hardware share in total market penetration reached only 32%. High operational costs and skilled labor requirements further slow adoption, constraining the overall Middle East and Africa Autonomous Vehicle Simulation Solution market growth despite strong demand in urban hubs.

Autonomous Vehicle Simulation Solution Market Oppportunity

Integration of AI and Cloud-Based Platforms Unlocks New Revenue Streams

The integration of AI-driven simulation software and cloud platforms represents a significant opportunity for market expansion. In 2026, cloud-based simulation accounted for 27% of total units deployed, with adoption expected to reach 45% by 2030. AI-based predictive models improved scenario testing efficiency by 18%, enhancing performance metrics such as real-time processing and latency reduction. Increased demand in commercial vehicle simulation, particularly in logistics and public transport, creates an estimated USD 520 million revenue potential by 2034. These technological opportunities indicate robust growth prospects for the Middle East and Africa Autonomous Vehicle Simulation Solution market.

Autonomous Vehicle Simulation Solution Market Challenge

Regulatory Uncertainty and Data Security Concerns Hinder Adoption

Regulatory frameworks for autonomous vehicle simulation remain inconsistent across the Middle East and Africa, posing challenges to standardization and compliance. Data security concerns, particularly for cloud-based simulation platforms, affect 38% of small-to-medium simulation providers. In 2026, only 62% of companies reported full compliance with regional guidelines. Production delays and testing restrictions have constrained regional penetration, limiting market growth to a CAGR of 16.8%. Overcoming these regulatory and security challenges is critical to sustaining the Middle East and Africa Autonomous Vehicle Simulation Solution market growth trajectory.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.13 Billion |

| Market Size in 2026 | USD 1.32 Billion |

| Market Size in 2034 | USD 4.85 Billion |

| CAGR | 16.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Vehicle Simulation Solution Market Segmentation

Middle East and Africa Autonomous Vehicle Simulation Solution market segmentation allows stakeholders to assess market dynamics by type and application, with hardware accounting for 38% of the market, software 42%, and services 20% in 2026. Passenger vehicle simulation holds a dominant 55% application share, commercial vehicles 30%, and public transport 15%, providing detailed insights into market behavior.

By Type

Hardware solutions include LiDAR, radar, cameras, and simulation rigs. In 2026, over 14,000 units were deployed across the region, representing 38% market share. High-frequency sensor integration (60–120 Hz) and low-latency data acquisition (

Software solutions, including real-time scenario simulation, AI-based predictive models, and virtual environment generation, contributed 42% to the market in 2026. Production volume reached 5.8 million simulation hours, with passenger vehicle applications accounting for 55% of usage. Cloud-based deployment represented 27% of installations, expected to grow to 45% by 2030. Technical metrics such as latency under 10 ms and real-time rendering frequency of 120 Hz highlight software efficacy. Commercial vehicle simulation demand grew by 15%, reflecting the strategic role of software in the Middle East and Africa Autonomous Vehicle Simulation Solution market.

Services, including testing, validation, maintenance, and consulting, held a 20% share in 2026. Over 2,500 projects were supported across major automotive hubs, with passenger vehicles accounting for 52% of service demand. Service adoption ensures optimal hardware/software integration, enhances operational efficiency by 18%, and supports sector-specific requirements such as public transport simulation, which accounted for 15% of total services. This reinforces services as a growth-enabling segment in the Middle East and Africa Autonomous Vehicle Simulation Solution market.

By Application

Passenger vehicle simulation accounted for 55% of the market, with 6,875 units deployed in 2026. Frequency metrics of 60–120 Hz and latency under 10 ms allow precise scenario testing. Software solutions dominate, representing 42% of application share, while hardware accounts for 38%. Adoption is strongest in UAE, Turkey, and Saudi Arabia, contributing 45% of total regional production. Consumer demand for safety validation and automated driving features drives continuous growth.

Commercial vehicle simulation holds a 30% share, with over 3,750 units deployed in 2026. Integration of AI-based predictive analytics improved efficiency by 17%. Sector-specific simulations for logistics, freight, and fleet management represent 72% of commercial vehicle simulation applications. Adoption is highest in South Africa and Egypt, with penetration rates of 28–31%. Hardware upgrades and real-time monitoring are critical to performance, reinforcing demand for comprehensive Middle East and Africa Autonomous Vehicle Simulation Solution.

Public transport simulation accounts for 15% share, with 1,875 units in 2026. Cloud-based solutions now support 62% of urban transport simulation, enabling real-time data transfer. Production volume reached 1.2 million virtual kilometers simulated, with adoption highest in Saudi Arabia and UAE at 34%. Integration with 5G infrastructure supports real-time scenario testing, improving safety and operational planning. Public transport applications highlight critical demand for Middle East and Africa Autonomous Vehicle Simulation Solution.

Middle East and Africa Autonomous Vehicle Simulation Solution Market Segmentations

Type

- Hardware

- Software

- Services

Application

- Passenger Vehicles

- Commercial Vehicles

- Public Transport

Autonomous Vehicle Simulation Solution Market Regional Outlook

UAE

The UAE contributes 22% to regional production in 2026, with 45 simulation facilities operational. Passenger vehicle applications dominate at 58%, commercial vehicles 27%, and public transport 15%. Technology adoption includes 72% hardware implementation and 64% software integration. The UAE is a key growth driver for Middle East and Africa Autonomous Vehicle Simulation Solution, reflecting high investment in R&D and advanced simulation infrastructure.

Turkey

Turkey accounts for 14% of regional market share, with over 3,000 units produced in 2026. Passenger vehicles contribute 52%, commercial vehicles 35%, and public transport 13%. Adoption of AI-driven software is at 58%, while high-fidelity hardware is deployed in 65% of labs. Government support and investment in autonomous vehicle testing underpin market growth.

Saudi Arabia

Saudi Arabia holds 16% of the market, with 3,500 units produced in 2026. Passenger vehicles dominate with 55%, commercial vehicles 30%, and public transport 15%. Technology adoption includes 70% hardware integration and 60% AI software utilization. Sector-specific demand for public transport simulation contributes 1.2 million virtual kilometers tested in 2026.

South Africa

South Africa represents 12% of the regional market, with 2,750 units produced. Passenger vehicle simulation contributes 50%, commercial vehicles 38%, and public transport 12%. Hardware penetration stands at 60%, software adoption at 55%. Demand growth is driven by logistics and fleet management simulation.

Egypt

Egypt contributes 11% of regional production, with 2,500 units in 2026. Passenger vehicle simulation dominates at 53%, commercial vehicles 32%, and public transport 15%. AI-based software adoption is at 50%, and hardware penetration is 45%, indicating gradual but steady market expansion.

Nigeria

Nigeria accounts for 10% of regional market share, with 2,250 units produced. Passenger vehicle applications comprise 50%, commercial vehicles 35%, and public transport 15%. Adoption of software solutions is at 48%, while hardware upgrades are at 40%. The market is emerging, with significant growth potential for Middle East and Africa Autonomous Vehicle Simulation Solution.

List of Top Autonomous Vehicle Simulation Solution Companies

- NVIDIA Corporation

- Siemens AG

- AVL List GmbH

- Bosch Mobility Solutions

- Waymo LLC

- Applied Intuition Inc.

- MathWorks Inc.

- ZF Friedrichshafen AG

- LeddarTech

- Cognata Ltd.

- Renovo Motors

- Escrypt GmbH

- Ansys Inc.

- Baidu Inc.

- Qualcomm Technologies Inc.

Top Two Companies

NVIDIA Corporation

-

Holds 14% market share in Middle East and Africa Autonomous Vehicle Simulation Solution market in 2026.

-

Leading in GPU-accelerated simulation platforms, real-time rendering, and AI integration. Provides high-fidelity simulation across passenger and commercial vehicles, with 5.2 million simulation hours recorded in 2026. Strong presence in UAE and Saudi Arabia contributes 28% of regional deployments.

Siemens AG

-

Accounts for 12% market share, focusing on hardware-software integrated simulation systems. Offers AI-driven scenario analysis, latency reduction to

Investment Analysis and Opportunities

Investment in Middle East and Africa Autonomous Vehicle Simulation Solution is rising, with 2026 allocations totaling USD 680 million. Sector-wise allocation includes 42% to software development, 38% to hardware upgrades, and 20% to services and consulting. Regional investment distribution shows UAE leading with 22%, Saudi Arabia 16%, Turkey 14%, and remaining 48% across South Africa, Egypt, and Nigeria. M&A activities include collaborations between Applied Intuition and AVL List GmbH to expand simulation services in UAE and Turkey, representing 8% growth in joint market coverage. Strategic partnerships between NVIDIA and regional automotive OEMs facilitate technology adoption, improving simulation performance by 18%. Investment in AI and cloud platforms is expected to drive revenue CAGR of 16.8% through 2034, indicating a lucrative opportunity for investors.

New Product Development

New product development emphasizes AI-driven predictive simulation software and high-fidelity hardware rigs. Approximately 28% of solutions launched in 2026 were new products, offering performance improvements of 20–25%. Innovation is concentrated in real-time rendering, sensor integration, and latency reduction technologies. Companies such as Siemens and NVIDIA are driving R&D efforts to introduce cloud-based simulation tools, enhancing remote accessibility and enabling broader penetration in emerging markets. Enhanced scenario coverage and predictive accuracy further reinforce demand for Middle East and Africa Autonomous Vehicle Simulation Solution.

Recent Developments

- 2026: NVIDIA launched a new GPU-accelerated simulation platform, increasing simulation performance by 23%, with over 5.2 million hours utilized in Middle East and Africa Autonomous Vehicle Simulation Solution.

- 2025: Siemens AG integrated AI-based predictive models, improving scenario testing efficiency by 18%, deployed in 4.8 million simulation hours across the region.

- 2025: Applied Intuition Inc. partnered with UAE OEMs, increasing market penetration by 12% and adding 1,200 hardware units.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.