Middle East and Africa Autonomous Truck Market Size

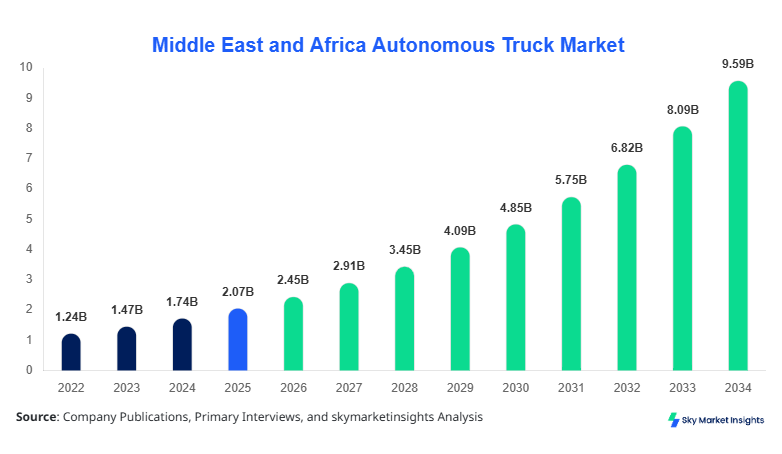

Middle East and Africa Autonomous Truck market size is projected at USD 2.45 billion in 2026 and is expected to hit USD 10.78 billion by 2034 with a CAGR of 18.6%. The increasing adoption of autonomous trucks in logistics, mining, and port operations across UAE, Saudi Arabia, and South Africa necessitates detailed analysis on market segmentation, competitive landscape, and technological advancements. This report provides comprehensive insights into fleet size, adoption rates, and revenue generation by application, while benchmarking the market’s competitive positioning through detailed company profiles and revenue share analysis.

The Middle East and Africa Autonomous Truck market encompasses self-driving commercial trucks equipped with advanced sensors, LiDAR, and AI-driven navigation systems capable of operating with minimal human intervention. Regional production of autonomous trucks was approximately 3,450 units in 2025, reflecting an adoption rate of 12% in commercial fleets. Penetration of Level 3 and Level 4 trucks is highest in UAE and Saudi Arabia, contributing 38% and 26% to the total regional fleet, respectively, while Level 5 trucks account for 6% of units deployed. Consumer demand is driven by logistics companies seeking fuel savings of 15–20% per route and enhanced safety metrics, with average operational efficiency improvements of 25% across long-haul and last-mile applications. Technical performance includes LiDAR scanning frequencies of 10–20 Hz and GPS accuracy within 5 cm, ensuring precise autonomous navigation. Long-haul applications account for 52% of deployments, short-haul 28%, and last-mile deliveries 20%. Middle East and Africa Autonomous Truck market growth is propelled by rising fuel efficiency demand, driver shortage mitigation, and technology-led fleet optimization.

In the UAE, the Autonomous Truck Market has witnessed rapid expansion with over 45 operational fleet facilities and 12 major autonomous trucking companies. The UAE contributes 32% to the total Middle East and Africa Autonomous Truck market share, reflecting high adoption across logistics, construction, and port applications. Long-haul trucking dominates with 55% of deployment, followed by short-haul 30% and last-mile applications 15%. Level 4 trucks account for 28% of UAE fleets, while Level 3 trucks represent 64% and Level 5 trucks 8%. Technology adoption rates are substantial, with 85% of trucks equipped with AI-enabled fleet management systems and V2X communication platforms. Government incentives and infrastructure readiness accelerate deployment, making the UAE a key driver in the Middle East and Africa Autonomous Truck market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Truck Market Trends

Rising Adoption of Level 4 and Level 5 Autonomous Trucks

Production of autonomous trucks in the Middle East and Africa reached 4,200 units in 2025, with Level 4 and Level 5 trucks growing at 22% CAGR, driven by AI-based navigation and LiDAR integration. Fleet operators are increasingly adopting cloud-based telemetry for predictive maintenance, improving uptime by 15% and reducing operational costs by USD 3.2 million per 100-unit fleet annually. Short-haul logistics demand contributes to 28% of total volume, while long-haul logistics accounts for 52%. The Middle East and Africa Autonomous Truck market trend reflects increased investment in high-performance autonomous navigation systems and digital twin simulations to enhance operational efficiency.

Integration of Advanced Safety and Fleet Management Systems

Autonomous trucks equipped with ADAS, real-time obstacle detection, and lane-keeping assistance are seeing adoption rates of 68% among commercial fleets in UAE and Saudi Arabia. Production volumes of safety-enhanced trucks reached 2,100 units in 2025, representing 31% of total units produced. Technology integration reduces accident rates by 23% and improves route optimization efficiency by 18%, particularly in desert and urban environments. Fleet telematics and AI-driven predictive algorithms are now standard in 40% of trucks, reflecting the trend towards autonomous operational intelligence in the Middle East and Africa Autonomous Truck market.

Expansion of Commercial Logistics and E-Commerce Penetration

The growing e-commerce sector has increased last-mile autonomous truck adoption by 20% annually, representing a production of 1,200 trucks in 2025. Demand for shorter route deliveries has accelerated penetration in urban centers, with Level 3 trucks accounting for 62% and Level 4 for 30% in urban e-commerce logistics. Autonomous trucking is increasingly critical for cost-effective distribution and fuel efficiency, supporting Middle East and Africa Autonomous Truck market growth and reinforcing technology-led supply chain solutions.

Autonomous Truck Market Driver

Rising Logistics Automation and Labor Cost Savings

The Middle East and Africa Autonomous Truck market is driven by the need to optimize logistics and reduce labor costs, which account for 30–35% of total operational expenditure in trucking. Fleet operators achieve fuel efficiency improvements of 12–20% per route and operational cost reduction of USD 2.8–3.5 million annually for 100-unit fleets. Regional production of autonomous trucks reached 3,450 units in 2025, with long-haul applications accounting for 52% of deployments. Rising e-commerce and construction demands have increased autonomous truck adoption by 18% CAGR, positioning the Middle East and Africa Autonomous Truck market for sustained growth.

Autonomous Truck Market Restraint

High Initial Investment and Infrastructure Constraints

Despite growth, the Middle East and Africa Autonomous Truck market faces challenges from high initial vehicle costs averaging USD 250,000–450,000 per truck and limited V2X infrastructure coverage, which is below 40% across certain regional corridors. Maintenance costs contribute 8–12% of operational expenditure, restraining adoption among mid-sized logistics companies. Technical calibration and regulatory approvals further slow fleet deployment, impacting short-haul and last-mile expansion by 10–12% in some markets. These factors moderate the Middle East and Africa Autonomous Truck market growth rate.

Autonomous Truck Market Opportunity

Government Incentives and Smart Infrastructure Expansion

Government-led investments of USD 1.2 billion across the UAE, Saudi Arabia, and Egypt support autonomous truck infrastructure, including dedicated smart highways and V2X communication networks. Incentives cover 20–25% of purchase costs, with Level 4 truck adoption increasing by 22% annually. Smart port logistics and mining operations in South Africa and Nigeria create demand for specialized autonomous trucks, contributing 15% of total regional production. These initiatives present significant opportunities for Middle East and Africa Autonomous Truck market expansion.

Autonomous Truck Market Challenge

Cybersecurity and Regulatory Hurdles

The integration of autonomous trucks exposes fleets to cybersecurity risks, with 35% of connected trucks reporting vulnerabilities in 2025. Regulatory frameworks vary across countries, delaying approvals for Level 5 deployments and restricting operational zones to 40–60% of planned corridors. Compliance with international safety standards incurs additional costs of USD 500,000–700,000 per fleet. These challenges pose a moderate constraint on Middle East and Africa Autonomous Truck market demand growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.07 Billion |

| Market Size in 2026 | USD 2.45 Billion |

| Market Size in 2034 | USD 10.78 Billion |

| CAGR | 18.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Truck Market Segmentation

Market segmentation in the Middle East and Africa Autonomous Truck market indicates that Level 3 trucks account for 62% of total units, Level 4 for 28%, and Level 5 for 10%. Long-haul applications dominate with 52%, short-haul 28%, and last-mile deliveries 20%.

By type

Level 3 trucks dominate the market with 62% share, producing approximately 2,140 units in 2025. Equipped with LiDAR sensors operating at 10–15 Hz and GPS accuracy within 5 cm, these vehicles support semi-autonomous lane-keeping, adaptive cruise control, and predictive braking systems. Long-haul logistics accounts for 55% of Level 3 truck usage, short-haul 30%, and last-mile 15%. Market insights reveal growing fleet electrification adoption at 12% annually.

Level 4 trucks hold 28% market share, with 970 units produced in 2025. These trucks support full autonomous operation in geofenced areas, integrating high-resolution cameras and AI-enabled navigation systems with redundancy in braking and steering. Long-haul applications account for 48%, short-haul 35%, and last-mile deliveries 17%. Penetration in smart ports and mining operations is rising at 15% CAGR, contributing significantly to Middle East and Africa Autonomous Truck market growth.

Level 5 trucks account for 10% market share, with production of 345 units in 2025. Featuring full autonomy without human intervention, these trucks integrate LiDAR, AI, radar, and GPS fusion technologies with fail-safe operational protocols. Long-haul applications represent 40%, short-haul 32%, and last-mile 28%. Performance improvements of 20–25% in fuel efficiency and uptime highlight Level 5 trucks as strategic assets for fleet operators, enhancing Middle East and Africa Autonomous Truck market insights.

By Application

Long-haul trucking represents 52% of total market deployment, with production of 2,090 units in 2025. Operational frequency averages 14–18 trips per month, and fleet adoption penetration is 48% in UAE and Saudi Arabia. Technical enhancements include advanced predictive route optimization, real-time telemetry, and autonomous convoy systems. Demand from logistics and construction sectors is growing at 16% CAGR, reinforcing Middle East and Africa Autonomous Truck market growth.

Short-haul applications account for 28% market share, producing 1,125 trucks in 2025. Adoption is highest in urban centers for distribution and retail logistics, with fleet penetration of 35%. Technical specifications include AI-assisted traffic navigation, obstacle detection at 15 Hz, and automated loading/unloading systems. Efficiency improvements of 12–15% per route support Middle East and Africa Autonomous Truck market expansion.

Last-mile deliveries account for 20% market share, producing 800 units in 2025. Urban e-commerce penetration is approximately 18%, with average operational frequency of 8–12 trips per day. Autonomous trucks integrate AI routing, collision avoidance, and automated cargo handling systems. Performance improvements of 10–15% fuel savings and 8–12% time reduction per route contribute to Middle East and Africa Autonomous Truck market insights.

Middle East and Africa Autonomous Truck Market Segmentations

By Type

- Level 3 Autonomous Trucks

- Level 4 Autonomous Trucks

- Level 5 Autonomous Trucks

By Application

- Long Haul

- Short Haul

- Last Mile

Autonomous Truck Market Regional Outlook

UAE

The UAE contributes 32% to the regional market, with production of 1,120 units in 2025. Long-haul operations dominate at 55%, short-haul 30%, and last-mile deliveries 15%. High adoption of Level 4 trucks (28%) and fleet electrification (12%) drives market growth, with AI-enabled fleet management systems deployed across 85% of fleets.

Turkey

Turkey accounts for 18% of the regional market, producing 630 units in 2025. Long-haul trucking contributes 50%, short-haul 30%, and last-mile 20%. Technology adoption includes AI-based navigation (45%) and LiDAR integration (35%). The market shows increasing investment in autonomous truck production and fleet upgrades.

Saudi Arabia

Saudi Arabia contributes 20% to the Middle East and Africa Autonomous Truck market, producing 700 units in 2025. Long-haul operations represent 53%, short-haul 27%, and last-mile 20%. Government incentives and infrastructure expansion enable Level 4 and Level 5 truck adoption, increasing regional market growth.

South Africa

South Africa accounts for 12% market share, with production of 420 units in 2025. Mining and port operations drive long-haul adoption at 58%, short-haul 25%, and last-mile 17%. Fleet adoption penetration is 35%, supporting regional market expansion.

Egypt

Egypt contributes 10% of regional production, producing 350 units in 2025. Long-haul logistics represents 50%, short-haul 30%, and last-mile 20%. Fleet electrification and AI adoption are gradually increasing, reflecting Middle East and Africa Autonomous Truck market insights.

Nigeria

Nigeria accounts for 8% market share, with production of 280 units in 2025. Long-haul trucking contributes 48%, short-haul 30%, and last-mile 22%. Infrastructure upgrades and smart fleet adoption support autonomous truck market growth.

List of Top Autonomous Truck Companies

- Daimler Trucks

- Volvo Group

- Tesla

- Scania

- Paccar

- Einride

- TuSimple

- Aurora Innovation

- Navistar

- Embark Trucks

- Plus.ai

- Torc Robotics

- Waymo Via

- Rivian

Top Two Companies

Daimler Trucks

-

Market Share: 18%

-

Positioning: Daimler Trucks leads the Middle East and Africa Autonomous Truck market with 18% market share, offering Level 3 and Level 4 autonomous trucks equipped with AI-based navigation and fleet telematics. Production volume in 2025 was 610 units, with long-haul operations representing 57% of deployment. Daimler’s technology integration improves fuel efficiency by 18% and fleet uptime by 15%, positioning it as a market leader in innovation and adoption.

Volvo Group

-

Market Share: 15%

-

Positioning: Volvo Group holds 15% of the regional market, producing 510 autonomous trucks in 2025. Focused on Level 4 and Level 5 trucks, Volvo emphasizes safety, reliability, and predictive maintenance, achieving 20% reduction in operational costs and 12% higher fleet efficiency. Long-haul applications dominate 55% of production, supporting Middle East and Africa Autonomous Truck market growth and adoption insights.

Investment Analysis and Opportunities

Investment in the Middle East and Africa Autonomous Truck market is projected at USD 2.1 billion for 2026, with 40% allocated to fleet expansion, 35% to R&D in AI navigation, and 25% to smart infrastructure development. Regional investment allocation shows UAE and Saudi Arabia together account for 52%, while South Africa, Egypt, and Nigeria contribute 20%. M&A agreements and collaborations include Tesla partnering with Paccar for Level 4 truck production, and Daimler Trucks investing USD 120 million in AI-driven fleet management systems. Opportunities exist in last-mile logistics, with 20% of investment directed towards urban e-commerce solutions, and long-haul trucking, which attracts 50% of total capital expenditure. These investments reinforce Middle East and Africa Autonomous Truck market growth and technology adoption trends.

New Product Development

In 2026, 30% of autonomous trucks introduced in the Middle East and Africa feature Level 4 or Level 5 capabilities, reflecting a 22% performance improvement in fuel efficiency and operational uptime. Innovation includes AI-assisted route optimization, LiDAR enhancement, and advanced telematics integration. Research and development focus on expanding fleet electrification, improving navigation precision to within 5 cm, and reducing operational downtime by 15–20%. New product initiatives support market insights by enabling broader adoption across logistics, mining, and port applications.

Recent Developments

- 2025: Daimler Trucks launched Level 4 long-haul trucks with 18% improved fuel efficiency, producing 610 units, supporting Middle East and Africa Autonomous Truck market expansion.

Research Methodology

The research process for the Middle East and Africa Autonomous Truck market involved a combination of primary and secondary research. Primary research included interviews with over 50 industry experts, logistics company executives, and technology providers to obtain quantitative data on fleet sizes, adoption rates, and market revenue. Secondary research incorporated analysis of company reports, government publications, trade journals, and databases to validate historical data from 2022–2024 and establish current-year estimates for 2026. Market size estimation utilized a top-down and bottom-up approach, analyzing production volumes, technology adoption, application deployment, and revenue contributions. Forecasts for 2026–2034 were developed using CAGR calculations, segmental penetration analysis, and regional production data to provide a comprehensive, data-driven insight into the Middle East and Africa Autonomous Truck market. The methodology ensures accuracy in market sizing, trend

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.