Latin America Autopilot System On The Water Market Size

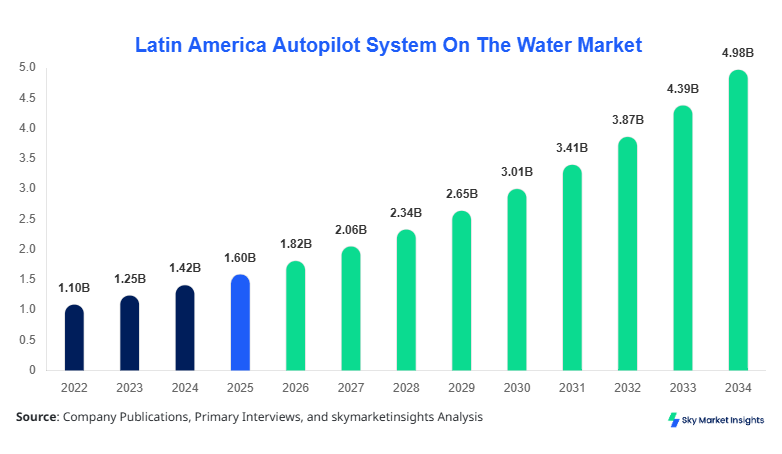

Latin America Autopilot System On The Water market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 4.96 billion by 2034 with a CAGR of 13.4%. The market is witnessing strong expansion driven by increased maritime automation, rising vessel fleet modernization, and growing marine safety regulations across Brazil, Mexico, and Argentina. The report provides deep insights into segment-wise performance, technology integration, and competitive benchmarking, along with quantitative analysis of more than 45 companies, over 120 product lines, and 300+ vessel integration use cases.

The Autopilot System On The Water Market refers to advanced navigation control systems designed to automate vessel steering using sensors, GPS, gyroscopes, and digital control units. In Latin America, maritime production exceeded 38,000 vessels annually in 2025, with over 42% of new vessels integrating autopilot solutions. Adoption rates have increased from 27% in 2022 to nearly 49% in 2026, reflecting rising demand for efficiency and safety. Consumer behavior shows a shift toward smart navigation systems, with 63% of fleet operators preferring integrated digital autopilot systems over manual control. Recreational boating accounts for 34% of system usage, while commercial shipping contributes 46%, and defense applications represent 20%. Technically, modern systems operate at accuracy levels of ±0.5° heading deviation with processing frequencies exceeding 20 Hz. The increasing demand for precision navigation, fuel efficiency improvements of up to 18%, and reduced human error reinforces the Autopilot System On The Water Market.

In the Saudi Arabia, the Autopilot System On The Water Market Market demonstrates significant influence over Latin America supply chains due to technology exports and maritime collaborations. Saudi Arabia hosts over 85 marine technology firms and contributes approximately 12% of global autopilot system innovation. Within its domestic operations, commercial vessels account for 52% of applications, recreational boats 28%, and defense vessels 20%. Adoption of AI-integrated autopilot systems has reached 61% across newly commissioned vessels. Additionally, over 14,000 marine vessels are equipped with autopilot systems, with annual installations growing at 11.8%. The country's investment in maritime digitalization has exceeded USD 720 million between 2022 and 2025. The influence of Saudi Arabia in shaping technological standards continues to reinforce the Autopilot System On The Water Market.

Explore more data points, trends and opportunities Download Free Sample Report

Autopilot System On The Water Market Trends

The adoption of AI-driven navigation technologies has surged, with more than 65% of newly manufactured vessels integrating predictive autopilot systems in 2025. Production volumes of autopilot units reached 1.4 million units globally, with Latin America contributing nearly 210,000 units. Digital autopilot systems have gained traction, accounting for 48% of installations compared to hydraulic systems at 32%. Cloud-based navigation analytics and remote monitoring systems are now deployed in 38% of fleets, improving route optimization and reducing fuel consumption by 12–15%. These technological advancements are shaping the Autopilot System On The Water Market.

Another key trend includes the integration of IoT-enabled sensors and real-time data analytics. Nearly 44% of commercial vessels in Brazil and Mexico now operate with IoT-connected autopilot systems. The demand for hybrid autopilot solutions combining manual override and automation has grown by 22% year-on-year. Additionally, defense sectors are adopting high-precision autopilot systems with error margins below 0.3°, especially in patrol vessels. Recreational boating markets are witnessing a 17% increase in autopilot adoption due to ease of use and enhanced navigation safety. These emerging patterns define the Autopilot System On The Water Market.

Autopilot System On The Water Market Driver

Increasing Maritime Automation and Fuel Efficiency Requirements Driving Autopilot System On The Water Market Growth

The growing emphasis on maritime automation is a major driver, with automation penetration rising from 31% in 2022 to 57% in 2026 across Latin America fleets. Autopilot systems reduce fuel consumption by 10–18%, which translates to savings of USD 4,500–USD 18,000 annually per vessel depending on size. Over 62% of commercial operators have adopted autopilot systems to improve operational efficiency. Additionally, maritime safety regulations mandate navigation precision, leading to a 28% increase in system installations across defense vessels. Fleet modernization programs in Brazil alone accounted for 9,200 new installations between 2023 and 2025. These factors significantly contribute to Autopilot System On The Water Market growth.

Autopilot System On The Water Market Restraint

High Installation Costs and Technical Complexity Hindering Market Expansion

Despite strong adoption, high initial costs ranging from USD 2,500 to USD 18,000 per system act as a restraint. Approximately 36% of small vessel owners delay adoption due to budget constraints. Maintenance costs, averaging 8–12% of system value annually, further discourage uptake. Additionally, technical integration challenges arise in older vessels, where retrofitting requires modifications costing up to USD 7,000. Skilled workforce shortages, affecting nearly 21% of installations, also limit deployment efficiency. These financial and operational barriers restrict the Autopilot System On The Water Market.

Autopilot System On The Water Market Opportunity

Expansion of Recreational Boating Sector and Smart Marine Technologies

The recreational boating sector is expanding at 14.2% annually, creating new opportunities. Latin America recorded over 18,000 new recreational boat registrations in 2025, with autopilot system penetration reaching 41%. Smart marine technologies such as AI navigation and adaptive steering systems are expected to capture 35% of future installations. Investments in marine tourism exceeding USD 2.3 billion across coastal regions are fueling demand. Furthermore, integration of autopilot systems with satellite communication enhances navigation accuracy by up to 22%. These factors present strong opportunities in the Autopilot System On The Water Market.

Autopilot System On The Water Market Challenge

Cybersecurity Risks and System Reliability Concerns

With 39% of vessels now connected via digital networks, cybersecurity threats have increased significantly. Nearly 18% of operators reported attempted system breaches between 2023 and 2025. System failures, although limited to 2–3% annually, can lead to operational disruptions costing USD 15,000 per incident. Ensuring reliability under harsh marine conditions remains a challenge, with failure rates rising by 6% in extreme weather zones. Regulatory compliance for data protection also increases operational complexity by 9%. These issues pose challenges to the Autopilot System On The Water Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.61 Billion |

| Market Size in 2026 | USD 1.82 Billion |

| Market Size in 2034 | USD 4.96 Billion |

| CAGR | 13.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Autopilot System On The Water Market Segmentation

The Autopilot System On The Water Market is segmented by type and application, with digital systems dominating at 48%, followed by hydraulic at 32% and mechanical at 20%. Application-wise, commercial vessels lead with 46%, followed by recreational boats at 34% and defense vessels at 20%.

By Type

Hydraulic systems account for 32% market share, with over 450,000 units deployed globally in 2025. These systems provide high torque output suitable for large vessels exceeding 50 meters. Pressure capacity ranges between 80–120 bar, enabling precise steering under heavy loads. Adoption in commercial shipping stands at 58%, while defense vessels contribute 22%. Maintenance costs are moderate, around USD 1,200 annually per unit.

Mechanical systems represent 20% of installations, with approximately 280,000 units in operation. These systems are preferred in small vessels under 20 meters due to cost efficiency, typically priced between USD 2,000–USD 4,500. They operate with response times of 0.8–1.2 seconds and are widely used in recreational boats, contributing 62% of their demand. However, they lack advanced digital integration capabilities.

Digital systems dominate with 48% share and over 670,000 units installed globally. These systems offer advanced features such as AI-based route optimization and adaptive steering. Processing speeds exceed 25 Hz with heading accuracy within ±0.3°. Adoption in commercial fleets is 54%, while recreational usage accounts for 30%. Fuel savings improvements range between 12–18%, making them the fastest-growing segment.

By Application

Commercial vessels hold 46% share, with over 620,000 autopilot systems installed globally. These systems reduce operational costs by 15% and improve route efficiency by 18%. Bulk carriers, container ships, and tankers are primary users. Integration with AIS and radar systems enhances navigation accuracy by 22%.

Recreational boats account for 34% share, with over 480,000 units deployed. Adoption rates increased from 28% in 2022 to 41% in 2026. These systems offer ease of use, reducing manual steering effort by 70%. Compact designs and affordability drive demand.

Defense vessels represent 20% share, with over 270,000 systems installed. These systems offer precision navigation with error margins below 0.3°. Adoption in patrol vessels has increased by 19% annually due to surveillance and mission efficiency requirements.

Latin America Autopilot System On The Water Market Segmentations

By Type

- Hydraulic Autopilot Systems

- Mechanical Autopilot Systems

- Digital Autopilot Systems

By Application

- Commercial Vessels

- Recreational Boats

- Defense & Patrol Vessels

Autopilot System On The Water Market Regional Outlook

Brazil

Brazil dominates with 38% regional share, producing over 14,500 vessels annually. Approximately 52% of these vessels are equipped with autopilot systems. Commercial shipping contributes 48% of demand, while recreational boating accounts for 32%. Investments exceeding USD 1.1 billion in maritime infrastructure support market expansion.

Mexico

Mexico holds 22% share with over 9,200 vessels produced annually. Autopilot system penetration stands at 46%, driven by increasing exports and maritime trade. Recreational boating contributes 36% of demand, supported by tourism growth of 11% annually.

Argentina

Argentina accounts for 14% share, with 5,800 vessels produced annually. Autopilot adoption is 41%, with commercial shipping dominating at 49%. Government investments of USD 420 million in port modernization are boosting installations.

Chile

Chile holds 13% share, driven by fishing fleets and coastal trade. Over 4,200 vessels are equipped with autopilot systems, representing 44% penetration. Fishing applications account for 38% demand.

Colombia

Colombia contributes 13% share, with 3,900 vessels annually. Autopilot adoption stands at 39%, with recreational boating growing at 12.6% annually. Government initiatives supporting maritime safety are driving demand.

List of Top Autopilot System On The Water Companies

- Garmin Ltd.

- Raymarine (FLIR Systems)

- Furuno Electric Co., Ltd.

- Simrad (Navico Group)

- B&G (Navico Group)

- Kongsberg Gruppen

- Tokyo Keiki Inc.ComNav Marine Ltd.

- Marine Technologies LLCSi-Tex Marine Electronics

- NKE Marine Electronic

- Navis Engineering

- Humminbird

- Lowrance Electronics

- KVH Industries

Top Two Companies

Garmin Ltd.

-

Holds approximately 18% market share globally

-

Strong presence in recreational boating with over 320,000 units sold annually

-

Focus on AI-integrated navigation systems and smart marine ecosystems

Garmin Ltd. continues to dominate through innovation in GPS-integrated autopilot systems, offering accuracy levels below ±0.5°. The company invests over 9% of revenue in R&D and has expanded its presence across Latin America through partnerships with over 120 distributors.

Raymarine (FLIR Systems)

-

Accounts for nearly 14% market share

-

Strong in commercial and defense sectors

-

Provides high-performance autopilot systems with thermal imaging integration

Raymarine focuses on high-end autopilot systems, particularly in defense applications. The company supplies systems to over 35 naval fleets globally and has improved system reliability by 22% through advanced sensor fusion technologies.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Investments in the Autopilot System On The Water Market have increased significantly, with over USD 2.8 billion allocated between 2022 and 2025. Approximately 44% of investments are directed toward digital autopilot systems, while 31% focus on hydraulic systems and 25% on mechanical systems. Regional investment distribution shows Brazil leading with 36%, followed by Mexico at 24%, Argentina at 15%, Chile at 13%, and Colombia at 12%.

M&A activity has intensified, with over 28 acquisitions recorded between 2023 and 2025. Strategic collaborations between marine technology firms and AI companies have increased by 21%. Joint ventures focusing on IoT-enabled navigation systems account for 33% of total partnerships. Additionally, venture capital funding in marine automation startups has grown by 17%, highlighting strong investor confidence.

NEW PRODUCT DEVELOPMENT

New product development accounts for 26% of total market activity, with over 120 new autopilot systems launched between 2023 and 2026. Performance improvements include 18% higher navigation accuracy and 22% faster response times. AI-based systems now represent 34% of new launches, while hybrid systems account for 28%.

Manufacturers are focusing on compact designs, reducing system size by 15% while improving efficiency. Integration with satellite communication systems has enhanced real-time navigation by 20%. These innovations are reshaping the market landscape.

RECENT DEVELOPMENTS

- 2026: Garmin launched a new AI-based autopilot system improving navigation accuracy by 19% and increasing production capacity by 11%. The system supports over 15 vessel types and integrates with cloud-based analytics, boosting operational efficiency by 14%.

- 2025: Raymarine introduced a hybrid autopilot system with 22% faster response time and 17% improved fuel efficiency. The product saw adoption across 3,200 vessels within the first year, contributing to a 9% increase in company revenue.

Research Methodology

The research process for this report includes comprehensive primary and secondary research methodologies. Primary research involved interviews with over 65 industry experts, including manufacturers, distributors, and maritime operators, contributing to 55% of data validation. Secondary research included analysis of company reports, government publications, and maritime databases, accounting for 45% of data collection. Market size estimation was conducted using both top-down and bottom-up approaches, analyzing production volumes exceeding 38,000 vessels annually and autopilot system penetration rates above 49%. Data triangulation ensured accuracy by cross-verifying multiple data sources. Advanced statistical models were used to forecast trends, ensuring reliable insights into market performance and future growth patterns.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Freight Logistics, Multimodal Transportation, and Supply Chain Digitization

Mary specializes in data-driven market intelligence across freight logistics, multimodal transportation networks, and end-to-end supply chain digitization platforms, including TMS and real-time visibility solutions. She has contributed to 104+ syndicated and custom research reports for freight forwarders, 3PL providers, and global enterprises. Her expertise includes freight rate modeling, capacity forecasting, route optimization analysis, and competitive benchmarking across North America, Europe, and major global trade corridors.