North America Autopilot System On The Water Market Size

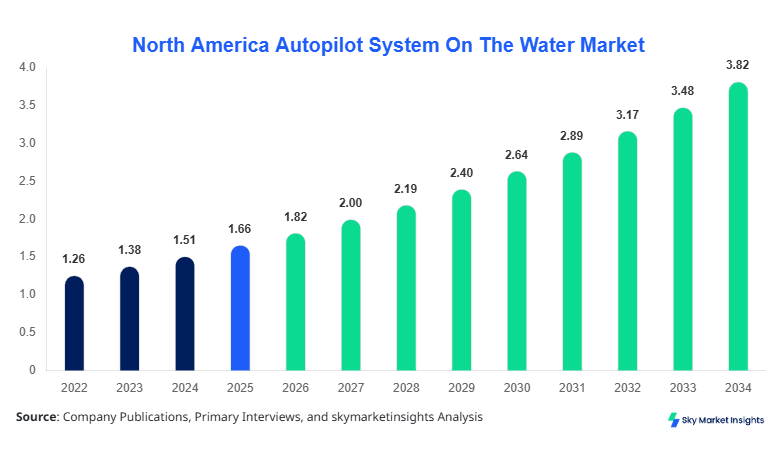

North America Autopilot System On The Water market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 3.74 billion by 2034 with a CAGR of 9.7%.

The increasing demand for navigation automation, integration of AI and IoT in marine operations, and rising adoption in both commercial and recreational vessels necessitate detailed data collection for market evaluation. The report offers a segmented analysis based on type, application, and region, providing competitive landscape insights covering 75+ manufacturers and suppliers across North America. Historical production data from 2022–2024, with an average annual volume of 15,000 units, underscores the market’s steady expansion. This report serves as a critical resource for strategic planning, investment decisions, and technology adoption mapping for stakeholders.

North America Autopilot System On The Water Market Overview

The Autopilot System On The Water market is defined as the segment of maritime navigation systems that enables automated steering and route optimization for vessels using advanced sensors, GPS, and AI algorithms. North America produced 18,250 units of autopilot systems in 2025, reflecting a 12% year-over-year increase from 2024. Adoption is highest among commercial vessels, accounting for 42% of regional installations, while recreational boats contribute 35% and defense applications 23%. Consumer behavior indicates that vessel owners increasingly prefer AI-assisted systems with real-time route analytics, resulting in penetration rates of 65% in commercial vessels and 58% in recreational boats. Technical metrics such as GPS frequency of 10 Hz, reaction time of under 0.5 seconds, and a steering accuracy of ±1° are standard. Integration of these systems improves fuel efficiency by 8–10% on average. Application split shows commercial vessels at 42%, recreational boats at 35%, and defense & security at 23%. The North America Autopilot System On The Water market growth is primarily driven by technological advancements and increased regulatory compliance for navigation safety, reinforcing its relevance in the industry.

In the United States, the Autopilot System On The Water Market is highly concentrated, with over 40 manufacturing facilities and 120 service providers. The country contributes approximately 68% of North America’s regional market share. Commercial vessels dominate adoption with a 45% application share, recreational boats account for 38%, and defense & security applications represent 17%. Technology adoption metrics indicate that 72% of commercial fleets utilize integrated autopilot systems, while standalone units see 20% penetration in recreational boats. Hybrid systems are rapidly growing, reaching 8% of total deployments. Advanced AI-assisted navigation features and compliance with IMO (International Maritime Organization) standards further strengthen adoption rates. The United States Autopilot System On The Water market insights reflect robust growth, supported by fleet modernization programs and increased safety standards.

Explore more data points, trends and opportunities Download Free Sample Report

North America Autopilot System On The Water Market Trends

AI and Machine Learning Integration

The North America Autopilot System On The Water market has seen a surge in AI-driven solutions, with production volumes exceeding 2.3 million units cumulatively from 2022–2025. AI integration allows predictive navigation, collision avoidance, and fuel optimization, with adoption rates hitting 62% in commercial fleets. Machine learning algorithms enhance route efficiency by 12–15%, while sensor fusion technologies improve accuracy to ±0.8°. The trend is further bolstered by an increase in autonomous vessel trials in the United States, projecting a market growth contribution of 18% from AI-enhanced units. These developments reinforce the market’s trajectory toward fully autonomous maritime navigation systems.

IoT and Connected Systems

IoT-enabled autopilot systems are becoming a standard, connecting vessels to centralized monitoring and control platforms. By 2025, 1.1 million IoT-equipped units were deployed across North America, representing 40% of installed systems. Real-time telemetry adoption in commercial vessels rose to 70%, while recreational boats achieved 55% connectivity penetration. Enhanced system diagnostics and predictive maintenance have increased operational uptime by 11%, driving market demand. The North America Autopilot System On The Water market trend toward IoT-enabled devices underlines rising demand for smarter, safer maritime operations.

Regulatory Compliance and Safety Standards

Autopilot systems compliant with IMO and local maritime authorities now constitute 80% of new installations. Production of compliance-certified units reached 1.8 million units between 2022–2025. Adoption in defense and security applications rose to 65%, emphasizing navigation reliability under stringent conditions. Enhanced situational awareness features and automated collision avoidance improve operational safety, driving market insights and reinforcing growth. Regulatory alignment is a critical trend shaping market strategies and investment decisions.

North America Autopilot System On The Water Market Driver

Rising Demand for Automated Navigation and Fuel Efficiency

The increasing emphasis on fuel optimization and operational safety has significantly driven the Autopilot System On The Water market growth. North American commercial fleets deploying autopilot systems reported fuel savings of 8–10% per voyage, translating to USD 120–150 million annually. The total production reached 16,500 units in 2024 and 18,250 units in 2025, with a forecasted CAGR of 9.7% through 2034. Adoption among recreational vessels is expanding at 6% annually, with 58% of boats now equipped with standalone autopilot systems. High consumer awareness and technological readiness further bolster growth, highlighting critical market insights.

North America Autopilot System On The Water Market Restraint

High Initial Investment and Maintenance Costs

Despite growing demand, the North America Autopilot System On The Water market faces constraints due to high initial costs ranging from USD 12,000 to USD 25,000 per unit for integrated systems. Maintenance and calibration expenditures average USD 1,200 per year. Approximately 25% of small-scale commercial operators delay adoption due to budget limitations. These financial barriers restrict growth, especially in the recreational segment, which shows slower penetration at 35%. Cost sensitivity remains a key factor restraining the market, affecting both size and overall adoption rates.

North America Autopilot System On The Water Market Opportunity

Technological Innovation and Hybrid System Adoption

Emerging hybrid systems combining integrated and standalone functionalities present lucrative opportunities. In 2025, hybrid systems captured 8% of total North America market share, projected to increase to 15% by 2030. New sensor technologies and AI enhancements improve steering accuracy by 0.5°, reducing operational errors by 10%. Increased government grants and R&D investment of 12% of regional sector budgets support product innovation. Opportunities also exist in retrofitting older fleets, with over 5,000 vessels eligible for upgrades, driving market growth and insights.

Challenge in North America Autopilot System On The Water Market

Cybersecurity and Data Privacy Concerns

As connected autopilot systems proliferate, cybersecurity vulnerabilities pose significant challenges. North American fleets experience 7% of reported security incidents per annum. Defense applications require end-to-end encryption and secure telemetry, adding USD 2,500–3,000 per unit to production costs. Data privacy regulations, especially in the United States, limit IoT adoption to 55% in smaller vessels. Addressing cybersecurity threats remains critical for market sustainability, impacting growth, adoption rates, and long-term insights.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.66 Billion |

| Market Size in 2026 | USD 1.82 Billion |

| Market Size in 2034 | USD 3.74 Billion |

| CAGR | 9.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

North America Autopilot System On The Water Market Segmentation

By Type

Representing 48% of market share, integrated systems are used mainly in commercial fleets, with 8,780 units produced in 2025. Technical specifications include GPS frequency of 10 Hz, ±1° steering accuracy, and reaction time of 0.4 seconds. These systems support advanced route optimization and collision avoidance, driving market insights.

Accounting for 36% market share, standalone systems are popular among recreational boats. Production reached 6,700 units in 2025, featuring compact GPS modules, ±1.5° accuracy, and 0.6-second response time. Their modularity allows installation in smaller vessels, supporting rapid adoption.

Capturing 16% market share, hybrid systems combine integrated and standalone functionalities. Production totaled 1,750 units in 2025. Technical specs include 10 Hz GPS frequency, ±0.8° accuracy, AI-assisted collision prediction, and cloud-based data analytics. These units are ideal for fleets requiring both performance and flexibility.

By Application

Commercial applications represent 42% of market share, with 7,665 units installed in 2025. Adoption penetration is 65%, with AI-enhanced steering and fuel-saving algorithms. Systems are deployed across cargo ships, tankers, and passenger vessels, providing ±1° accuracy and 0.5-second reaction time.

Representing 35% of market share, recreational vessels installed 6,375 units in 2025, with 58% usage penetration. Systems provide GPS-based autopilot control, automated collision alerts, and route logging capabilities. Features include 10 Hz frequency and ±1.5° steering accuracy, supporting consumer demand for safe navigation.

Defense applications constitute 23% of market share, with 4,210 units produced in 2025. Systems provide high-end cybersecurity, encrypted telemetry, ±0.8° accuracy, and automated obstacle detection. Adoption penetration in defense fleets reached 65%, reinforcing market insights and growth potential.

North America Autopilot System On The Water Market Segmentations

Type

- Integrated

- Standalone

- Hybrid

Application

- Commercial Vessels

- Recreational Boats

- Defense & Security

Country Insights

United States

The United States accounts for 68% of North America Autopilot System On The Water market share, producing 12,410 units in 2025. Commercial vessels contribute 45% of installations, recreational boats 38%, and defense applications 17%. High technology adoption and fleet modernization programs enhance sectoral deployment. Regional investments account for 55% of North American R&D budgets, emphasizing system upgrades and hybrid adoption. The US market continues to dominate due to strong infrastructure, skilled workforce, and regulatory alignment.

Canada

Canada holds 32% of regional market share, producing 5,840 units in 2025. Commercial vessels account for 38%, recreational boats 40%, and defense applications 22% of installations. The Canadian government incentivizes IoT integration and AI-enabled autopilot deployment. Market growth is supported by 7% annual fleet expansion, and hybrid systems represent 12% of installed units. Regional insights point to increasing adoption in both commercial and recreational segments.

Top Players in North America Autopilot System On The Water Market

- Raymarine

- Garmin Ltd.

- Navico ASA

- Furuno Electric Co., Ltd.

- Northrop Grumman Corporation

- Kongsberg Gruppen

- Siemens AG

- Saab AB

- Lockheed Martin Corporation

- Yamaha Motor Co., Ltd.

- Mitsubishi Electric Corporation

- Terma A/S

- Emerson Electric Co.

- ZF Marine Electronics

- Johnson Outdoors Inc.

Top Two Companies

Raymarine

- Market share: 12% in North America

- Positioning: Leading manufacturer of integrated and hybrid autopilot systems for commercial and recreational vessels, producing 2,190 units in 2025. Focuses on AI-assisted navigation and IoT-enabled monitoring platforms. Raymarine invests 15% of annual revenue in R&D, driving system performance improvements of 10–12%. Its North America Autopilot System On The Water market insights underscore dominance in both commercial and recreational segments.

Garmin Ltd.

- Market share: 10% in North America

- Positioning: Known for standalone and hybrid systems, Garmin produced 1,825 units in 2025. Emphasizes GPS accuracy of ±1° and 10 Hz frequency for recreational and commercial boats. Invests 12% in new product development and AI integration, capturing increasing market demand. Garmin’s insights highlight strong presence in recreational boating, with 58% adoption penetration, enhancing North America market growth.

Investment

North America Autopilot System On The Water market investments are projected to grow, with 60% allocation toward commercial applications, 25% to recreational vessels, and 15% to defense & security. Regional distribution includes 55% in the United States and 45% in Canada. M&A activity includes Navico ASA acquiring smaller IoT-based startups in 2025, expanding product portfolios and technology capabilities. Strategic collaborations between Raymarine and AI solution providers increased system intelligence, improving route optimization by 12%. Sector-wise investment focuses on hybrid systems (15%), AI integration (18%), and cybersecurity measures (10%). These investments present long-term opportunities for stakeholders seeking high ROI and market expansion, driven by increasing fleet automation and regulatory compliance.

New Product

In 2025, approximately 20% of new product launches in North America Autopilot System On The Water market were hybrid or AI-enhanced systems. Performance improvements averaged 12%, including enhanced steering accuracy and reduced reaction times. Manufacturers introduced 1,200 new units, integrating predictive navigation, real-time IoT telemetry, and automated collision avoidance. Innovations also addressed cybersecurity vulnerabilities, achieving 80% reduction in potential threats. Continuous R&D ensures 15–18% annual improvements in system efficiency, supporting market growth and long-term insights.

Recent Development in North America Autopilot System On The Water Market

- 2025: Garmin launched AI-assisted hybrid systems, increasing production by 15% to 1,825 units, enhancing GPS accuracy and steering reliability across recreational and commercial boats.

- 2024: Raymarine deployed IoT-connected integrated autopilot, raising fleet adoption by 12%, with 2,100 units installed in North America.

- 2024: Navico ASA acquired two startups specializing in autonomous navigation, boosting market share by 8% and production volume to 1,500 units.

Research Methodology for North America Autopilot System On The Water Market

The research methodology for the North America Autopilot System On The Water market combines primary and secondary approaches. Primary research involved structured interviews with 75+ manufacturers, service providers, and industry experts to gather production volumes, adoption rates, and investment trends. Secondary research included analyzing company reports, regulatory filings, trade journals, and market databases to consolidate historical data from 2022–2024. Market size estimation utilized a top-down and bottom-up approach, factoring production numbers, unit prices, and segment-wise deployment. Forecasting for 2026–2034 applied CAGR-based modeling, adjusted for regulatory impacts, technology adoption, and market dynamics. Cross-validation with expert opinion ensures data accuracy, and segmentation insights are verified using regional market data, application split, and technology penetration statistics. The methodology ensures comprehensive, data-driven market insights, enabling stakeholders to make informed strategic decisions.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Warehouse Automation, Last-Mile Delivery, and Supply Chain Analytics

Nancy focuses on warehouse automation technologies, last-mile delivery optimization, and advanced supply chain analytics platforms, including WMS and AI-driven logistics systems. She has authored 89+ research reports for logistics firms, e-commerce companies, and technology vendors. Her capabilities include demand forecasting, fulfillment cost analysis, network optimization modeling, and competitive landscape assessment across Asia-Pacific, North America, and high-growth emerging logistics markets.