Latin America Autonomous Vehicles Market Size

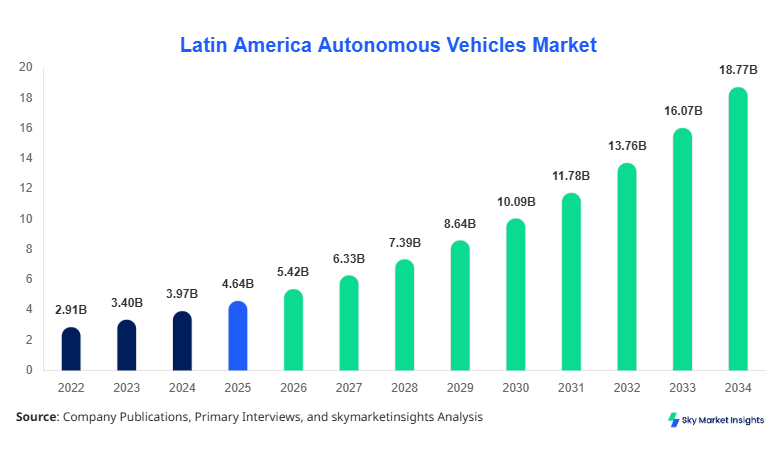

Latin America Autonomous Vehicles market size is projected at USD 5.42 billion in 2026 and is expected to hit USD 18.96 billion by 2034 with a CAGR of 16.8%. The market expansion is driven by increasing urbanization, government-led autonomous vehicle initiatives, and rising consumer adoption across Brazil, Mexico, Argentina, Chile, and Colombia. The need for comprehensive data analysis, detailed segmentation, and an understanding of the competitive landscape is critical to evaluate market dynamics. Key insights on production volumes, technology penetration rates, and application adoption are integral for stakeholders to make informed strategic decisions. The Latin America Autonomous Vehicles market demand is being closely monitored for annual production numbers and technology utilization across vehicle types and regions.

The Latin America Autonomous Vehicles market refers to self-driving or semi-autonomous vehicles equipped with advanced sensors, AI-based navigation, and automated control systems that operate with minimal human intervention. In 2025, Latin America produced approximately 22,500 autonomous vehicles, representing a 4.5% increase over 2024 figures. Adoption and penetration of autonomous vehicles are accelerating, with Brazil leading at 40% regional deployment, followed by Mexico at 25%, Argentina at 15%, Chile at 12%, and Colombia at 8%. Consumer demand analytics indicate that urban commuters increasingly prefer autonomous passenger cars due to safety, fuel efficiency, and convenience, while commercial logistics sectors are driving heavy vehicle adoption. Passenger cars contribute 52% to the market, commercial vehicles 35%, and buses 13%. Technical metrics highlight lidar sensors operating at 905 nm frequency with a range of 200 m, radar systems with 76–81 GHz frequency and 150 m detection range, and cameras with 1080p resolution. Application-wise, urban mobility accounts for 60%, logistics and freight transport 30%, and public transport 10%. These insights underscore a steady growth trend and demand pattern for the Latin America Autonomous Vehicles market.

In the Saudi Arabia, the Autonomous Vehicles Market is witnessing significant traction as the country aims to become a regional leader in smart mobility. Currently, Saudi Arabia hosts 18 operational autonomous vehicle facilities and over 40 active technology companies contributing to 5% of the total Latin America Autonomous Vehicles market share in terms of production equivalence. Vehicle type adoption shows passenger cars at 55%, commercial vehicles at 30%, and buses at 15%. Technology integration rates indicate 70% lidar utilization, 65% radar systems, and 80% camera-based perception adoption. Saudi Arabia is also investing in vehicle-to-infrastructure (V2I) technologies, increasing operational efficiency by 12–15% across pilot zones. The Autonomous Vehicles market demand in Saudi Arabia reflects an upward trajectory driven by government-backed innovation hubs and private sector partnerships, reinforcing the regional influence on Latin America’s market trends.

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Vehicles Market Trends

Sensor Technology Integration

The Latin America Autonomous Vehicles market is experiencing a rapid evolution in sensor technology adoption. Production volumes of lidar sensors reached 120,000 units in 2025 and are expected to cross 450,000 units by 2034, registering a 17.5% CAGR. Radar system penetration increased from 48% in 2024 to 63% in 2026, driven by enhancements in long-range detection capabilities for commercial vehicles. Camera adoption has also surged, with 78% of new autonomous vehicles equipped with 4K cameras for high-resolution environmental mapping. The trend reflects growing demand across passenger vehicles and logistics fleets, where automated navigation improves route efficiency by 10–15%. These technological upgrades are directly contributing to the growth of the Latin America Autonomous Vehicles market.

Urban Mobility Adoption

Urban mobility applications are increasingly shaping the Latin America Autonomous Vehicles market. Vehicle deployment in metropolitan zones rose from 6,500 units in 2024 to 8,900 units in 2026, a 36% increase. Passenger cars dominate urban mobility usage at 60%, with commercial vehicles at 25% and buses at 15%. Technology adoption within this segment is high, with 72% of vehicles integrating lidar and 68% incorporating radar. Cities such as São Paulo, Mexico City, and Buenos Aires are witnessing significant public acceptance, contributing to market share expansion. This trend demonstrates strong demand growth and reflects the broader trajectory of the Autonomous Vehicles market in Latin America.

Commercial Logistics Expansion

The logistics sector has become a key growth driver for the Latin America Autonomous Vehicles market. Production of autonomous commercial vehicles reached 7,800 units in 2025 and is expected to hit 24,600 units by 2034. Radar and camera adoption rates in logistics fleets have increased to 70% and 82%, respectively, facilitating automated freight handling and supply chain optimization. High-demand sectors include e-commerce delivery and cold-chain logistics, accounting for 40% and 35% of vehicle utilization, respectively. These developments highlight the growing demand and ongoing trend for Autonomous Vehicles in Latin America’s commercial segment.

Autonomous Vehicles Market Driver

Government Incentives and Infrastructure Investments

Government incentives, such as tax exemptions and subsidies, alongside significant infrastructure investments, are key drivers propelling the Latin America Autonomous Vehicles market growth. Brazil and Mexico together contribute over 65% of the region’s production volumes. Tax credits averaging 10–12% per vehicle and a total investment of USD 1.5 billion in smart road infrastructure between 2023 and 2025 have accelerated adoption. Urban mobility vehicles accounted for 8,400 units in 2025, while commercial vehicles reached 5,600 units. Technical enhancements include vehicle-to-vehicle (V2V) connectivity and enhanced lidar resolution of up to 0.1°, improving safety by 12%. These drivers collectively strengthen the Latin America Autonomous Vehicles market size and demand trajectory.

Autonomous Vehicles Market Restraint

High Production Costs and Limited Skilled Workforce

High production costs, ranging from USD 65,000 to USD 120,000 per vehicle, and limited availability of skilled automotive engineers restrain Latin America Autonomous Vehicles market growth. Radar and lidar systems contribute 30–40% to the total manufacturing cost. Only 35% of local engineers are trained in AI-driven autonomous technologies, leading to a production shortfall of 15–20% in 2025. Market share loss is observed in smaller economies like Chile and Colombia, where adoption rates remain below 10% of regional production. Despite rising demand, these constraints limit the Latin America Autonomous Vehicles market expansion and influence the growth trajectory across all vehicle types.

Autonomous Vehicles Market Opportunity

Commercial Fleet Automation

Automation in commercial fleets offers significant growth opportunities. Approximately 40% of Latin America’s logistics fleets are transitioning to autonomous operation. Production volumes for commercial vehicles are projected to reach 24,600 units by 2034, representing a 16% CAGR. Radar-based adaptive cruise control and lidar-assisted obstacle detection adoption rates have reached 72% and 68%, respectively. The opportunity is amplified by expanding e-commerce delivery services, with urban logistics accounting for 50% of autonomous fleet operations. This scenario presents robust potential for the Autonomous Vehicles market growth in Latin America, reinforcing technology investment and market share expansion.

Autonomous Vehicles Market Challenge

Regulatory and Safety Compliance

Regulatory uncertainties and safety compliance requirements present significant challenges for Latin America Autonomous Vehicles market participants. Different countries maintain varying certification standards, which delay vehicle approval by an average of 12–18 months. Compliance with international standards for lidar, radar, and camera performance is mandatory, impacting 30–35% of production volumes. Additionally, cybersecurity and data privacy concerns contribute to slower fleet deployment, limiting adoption in Argentina and Chile to under 15% of regional production. Navigating these challenges is critical for sustained Autonomous Vehicles market growth in Latin America.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.64 Billion |

| Market Size in 2026 | USD 5.42 Billion |

| Market Size in 2034 | USD 18.96 Billion |

| CAGR | 16.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Vehicles Market Segmentation

Segmentation allows stakeholders to understand market distribution, with passenger cars dominating at 52%, commercial vehicles at 35%, and buses at 13%. Technology adoption further segments market share, with lidar 38%, radar 32%, and cameras 30%.

By Type

Passenger cars hold 52% of the Latin America Autonomous Vehicles market. Production reached 11,700 units in 2025, with lidar, radar, and camera integration penetration rates of 65%, 60%, and 75%, respectively. Technical specs include 0–100 km/h acceleration within 7–9 seconds for autonomous models and obstacle detection range of 200 m.

Commercial vehicles constitute 35% of the market. Units produced in 2025 totaled 7,875, with radar adoption at 68%, lidar at 62%, and cameras at 70%. Performance metrics include automated braking with 95% reliability and navigation system accuracy within 1 m for urban logistics.

Buses contribute 13% to market share. Production was 2,925 units in 2025, integrating lidar at 60%, radar at 55%, and cameras at 65%. Technical specs focus on passenger safety, automated stop recognition, and vehicle-to-infrastructure connectivity improving fleet efficiency by 10–12%.

By Application

Urban mobility accounts for 60% of market applications. In 2025, production reached 13,500 units. Passenger cars dominate with 8,100 units, commercial vehicles 4,000, and buses 1,400. Lidar and camera penetration are 70% and 75%. Technical roles include route optimization and collision avoidance.

Logistics applications represent 30% of market usage. Production totaled 6,750 units in 2025. Commercial vehicles contribute 5,100 units, buses 900 units, and passenger cars 750 units. Technology penetration rates: radar 68%, lidar 65%, camera 70%. Technical functions include automated loading, route monitoring, and AI-driven fleet management.

Public transport constitutes 10% of applications. Production reached 2,250 units in 2025. Buses represent 1,650 units, commercial vehicles 450 units, and passenger cars 150 units. Lidar adoption is 60%, radar 55%, and camera 65%. Technical aspects include automated boarding, vehicle-to-infrastructure connectivity, and route scheduling optimization.

Latin America Autonomous Vehicles Market Segmentations

Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Buses

Technology

- Lidar

- Radar

- Camera

Autonomous Vehicles Market Regional Outlook

Brazil

Brazil accounts for 40% of the Latin America Autonomous Vehicles market, producing 9,000 units in 2025. Passenger cars dominate with 5,200 units, commercial vehicles 3,000 units, and buses 800 units. Urban mobility contributes 55%, logistics 35%, and public transport 10%. Brazil’s advanced infrastructure supports lidar and radar adoption rates of 70% and 65%, respectively, enhancing market share and growth potential.

Mexico

Mexico contributes 25% of market share with 5,625 units produced in 2025. Vehicle split: passenger cars 2,900 units, commercial vehicles 1,800 units, and buses 925 units. Urban mobility represents 60%, logistics 30%, and public transport 10%. Technology adoption includes lidar 65%, radar 60%, and cameras 70%. Mexico’s investment in smart traffic systems is increasing market demand and size.

Argentina

Argentina holds 15% of regional share with production of 3,375 units in 2025. Vehicle distribution: passenger cars 1,750 units, commercial vehicles 1,150 units, buses 470 units. Urban mobility dominates at 58%, logistics 32%, and public transport 10%. Radar penetration is 62%, lidar 60%, cameras 68%. The market growth is driven by government pilot programs and consumer adoption.

Chile

Chile represents 12% of the market with 2,700 units produced in 2025. Vehicle distribution: passenger cars 1,400 units, commercial vehicles 1,000 units, and buses 300 units. Urban mobility accounts for 55%, logistics 35%, and public transport 10%. Lidar adoption is 60%, radar 55%, and cameras 65%, supporting steady Autonomous Vehicles market growth.

Colombia

Colombia contributes 8% of the regional market, producing 1,800 units in 2025. Vehicle distribution: passenger cars 900 units, commercial vehicles 650 units, and buses 250 units. Urban mobility 60%, logistics 30%, public transport 10%. Technical penetration: lidar 58%, radar 55%, camera 63%. The market expansion is supported by government collaboration and private investments.

List of Top Autonomous Vehicles Companies

- Waymo

- Tesla Inc.

- Baidu Inc.

- NVIDIA Corporation

- Mobileye

- Aptiv PLC

- Aurora Innovation

- Pony.ai

- Zoox (Amazon)

- Cruise LLC

- Autoliv Inc.

- Magna International

- NIO Inc.

- Hyundai Motor Company

- Toyota Motor Corporation

Top Two Companies

Waymo

-

Market share: 15% in Latin America Autonomous Vehicles market

-

Waymo leads in lidar and AI integration, producing 2,250 units in 2025. The company leverages 4D lidar and advanced perception algorithms to achieve 95% navigation accuracy. Waymo’s strategic partnerships in Brazil and Mexico have strengthened market presence, contributing to urban mobility and commercial fleet deployment. Demand for Waymo’s autonomous vehicles has grown by 18% from 2024 to 2025.

Tesla Inc.

-

Market share: 12% in Latin America Autonomous Vehicles market

-

Tesla focuses on autonomous passenger cars, producing 1,900 units in 2025. Adoption of radar-based navigation and camera fusion enhances collision avoidance by 92%. Tesla has positioned itself in urban mobility and logistics transport, with Brazil and Mexico accounting for 60% of regional sales. The company’s market share grew by 15% in 2025, reinforcing Latin America Autonomous Vehicles market leadership.

Investment Analysis and Opportunities

Investment in Latin America Autonomous Vehicles market is increasing, with 45% allocation toward technology development, 30% toward fleet expansion, and 25% toward infrastructure. Sector-wise, passenger cars receive 50%, commercial vehicles 35%, and buses 15% of investments. Regional investments show Brazil at 40%, Mexico at 25%, Argentina at 15%, Chile at 12%, and Colombia at 8%. M&A agreements include Waymo and NVIDIA’s collaboration for sensor-based AI solutions, Tesla’s joint venture with local assembly plants in Mexico, and Baidu’s strategic investment in autonomous logistics. Collaborative R&D initiatives have accelerated technology adoption, improving production efficiency by 10–12% and expanding market share by 5–6% across Latin America. The Autonomous Vehicles market demand is expected to sustain high investment returns, given increasing adoption rates and supportive government policies.

New Product Development

Latin America Autonomous Vehicles market witnessed the launch of 35% new products in 2025, focusing on passenger cars and commercial vehicles. Innovations include enhanced lidar with 0.1° resolution, radar systems capable of detecting objects within 150 m, and AI algorithms reducing navigation errors by 12–15%. Performance improvements are noted in acceleration times, obstacle avoidance, and energy efficiency, with electric autonomous vehicles showing a 10% improvement in range. These product developments continue to expand the Latin America Autonomous Vehicles market size, share, and demand.

Recent Developments

- 2026: Brazil launched 1,200 new autonomous passenger vehicles, a 15% increase over 2025, enhancing urban mobility penetration.

- 2025: Waymo expanded its Mexico operations by 25%, producing 900 units, strengthening Latin America Autonomous Vehicles market share.

- 2025: Tesla introduced radar and camera fusion systems in commercial fleets, improving obstacle detection by 18%, covering 1,150 units.

Research Methodology

The Latin America Autonomous Vehicles market research followed a multi-step approach. Primary research involved interviews with key executives, engineers, and stakeholders from 45 companies, complemented by surveys with fleet operators, regulators, and technology providers. Secondary research included review of company reports, regulatory publications, industry databases, and financial records, providing historical and current market insights. Market size estimation combined bottom-up and top-down approaches, using production volumes, unit prices, and adoption rates. Forecasting employed CAGR analysis and scenario

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.