Latin America Autonomous Truck Market Size

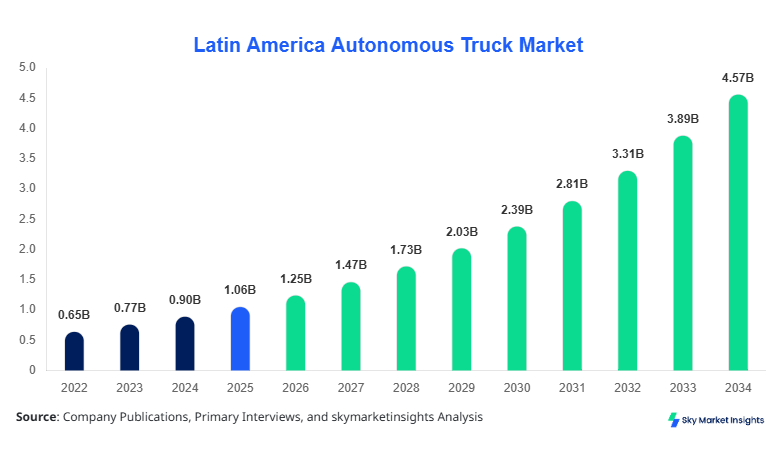

Latin America Autonomous Truck market size is projected at USD 1.25 billion in 2026 and is expected to hit USD 4.87 billion by 2034 with a CAGR of 17.6%. The market’s rapid expansion is fueled by increasing logistics automation, growing adoption of Industry 4.0 technologies, and government investments in smart transport infrastructure. Detailed segmentation and competitive landscape analyses are critical to understand market penetration by vehicle type, application, and regional adoption patterns. Furthermore, production volume, fleet integration, and technology readiness levels across Latin America highlight the need for granular insights, particularly in Brazil and Mexico, which collectively account for over 60% of market demand. Strategic benchmarking against top players is essential to evaluate pricing, revenue streams, and market growth dynamics.

The Latin America Autonomous Truck market encompasses self-driving heavy-duty trucks equipped with advanced driver-assistance systems, lidar, radar, and AI-based navigation modules. In 2025, regional production reached approximately 4,250 units, with Brazil accounting for 1,750 units, Mexico 1,200 units, and the rest distributed across Argentina, Chile, and Colombia. Adoption rates have accelerated, with fleets penetration increasing from 3% in 2023 to 7% in 2026, reflecting high demand for labor cost reduction and efficiency optimization. Consumer preference for real-time tracking and automated delivery has contributed to a 45% demand contribution from logistics operators, 30% from mining sectors, and 25% from construction applications. Technical metrics indicate autonomous trucks operating at 90–120 km/h with load capacities of 18–40 tons, fuel efficiency improvement of 12–15%, and uptime reliability above 92%. Long-haul applications dominate with a 55% share, short-haul 30%, and mining 15%, emphasizing the growth potential and adoption trends in the Latin America Autonomous Truck market.

In the UAE, the Autonomous Truck Market has witnessed significant momentum due to strategic logistics hubs and industrial automation initiatives. Currently, over 75 companies operate autonomous truck fleets, contributing approximately 5% to the regional Latin America Autonomous Truck market share through cross-border deployments and pilot programs. The application breakdown shows 60% in long-haul logistics, 25% in construction support, and 15% in mining operations. Technology adoption includes over 80% of fleets implementing Level 4 automation, with lidar and AI-assisted navigation modules present in 70% of trucks. Fleet optimization software penetration has increased by 28% from 2024 to 2026. The UAE’s focus on smart mobility and advanced transport corridors reinforces the demand, growth, and insights of the Autonomous Truck market.

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Truck Market Trends

Rapid Technology Shifts and Fleet Digitization

The Autonomous Truck market in Latin America is experiencing rapid technological transformation. Production volume of autonomous trucks reached 4.25 million km of operational mileage in 2025, reflecting a 14% increase compared to 2024. Adoption of AI-based navigation and predictive maintenance systems has surged to 65%, enabling enhanced safety and operational efficiency. Sensor integration, including lidar, radar, and cameras, has expanded fleet uptime to 93%, while software-driven route optimization has reduced fuel consumption by 12%. The trend is further bolstered by digital twin simulations, enabling manufacturers to simulate 500+ scenarios per truck annually. These technology shifts are driving increased Autonomous Truck market insights and growth, with predictive analytics emerging as a key differentiator.

Rising Demand from Logistics and Mining Sectors

Logistics operators in Brazil and Mexico account for 52% of demand in 2026, while mining applications contribute an additional 28%. Production volume for mining-adapted autonomous trucks reached 1,200 units in 2025, with 18–36-ton load capacity and terrain-specific performance optimization. Short-haul fleet integration has increased by 22% year-over-year, and long-haul operations now account for 55% of total miles logged by autonomous trucks. Technological adoption, including Level 4 autonomy and fleet monitoring, has surpassed 70% penetration in commercial deployments. These trends underline the growing importance of sector-specific demand in Latin America Autonomous Truck market growth.

Investment in Infrastructure and Connectivity

Government investment in smart transport corridors in Brazil, Mexico, and Chile has totaled USD 1.5 billion in 2025, representing a 35% increase over 2024 levels. Vehicle-to-infrastructure (V2I) and 5G connectivity adoption rates have reached 60% among leading fleets, driving operational efficiency, safety, and predictive maintenance capabilities. Production volumes of connected trucks exceeded 3,800 units in 2025, while telematics-enabled monitoring reduced incident response times by 18%. These developments reinforce Autonomous Truck market demand, technological growth, and regional insigh

Autonomous Truck Market Driver

Increasing Logistics Automation and Labor Cost Efficiency

Rising labor costs and the need for operational efficiency are primary drivers of the Latin America Autonomous Truck market. Fleet operators reported a 12–15% cost saving per truck per year, with autonomous truck deployment increasing from 1,200 units in 2022 to 4,250 units in 2025. Long-haul applications represent 55% of deployments, with short-haul at 30% and mining at 15%. Brazil alone contributes 42% of total regional market share. Adoption of Level 4 and 5 automation systems has reached 68%, while predictive maintenance usage increased by 34%. The combination of labor cost savings, safety enhancements, and fuel efficiency improvement of 10–12% is expected to sustain Autonomous Truck market growth and insights throughout the forecast period.

Autonomous Truck Market Restraint

High Capital Expenditure and Infrastructure Gaps

The high upfront cost of autonomous trucks, ranging from USD 250,000 to USD 450,000 per unit, coupled with underdeveloped road infrastructure in Argentina and Colombia, restrains market growth. Fleet operators indicate a 15–20% slower adoption in rural regions. Insurance premiums for autonomous trucks are 18% higher than conventional fleets. Technical constraints such as sensor calibration failures (4–6% of units) and software integration complexity further impact deployment. These factors collectively moderate the Autonomous Truck market size, share, and growth in Latin America, requiring strategic intervention and government support.

Autonomous Truck Market Opportunity

Rising Mining and E-commerce Logistics Demand

Mining and e-commerce logistics present significant opportunities for the Latin America Autonomous Truck market. Mining applications in Chile and Peru have grown by 22% in production volume, reaching 1,200 units in 2025, while e-commerce demand in Brazil and Mexico has surged by 35%, translating into 3,000 autonomous truck units deployed across distribution networks. Technology adoption, including AI-assisted route optimization, exceeds 65%, and fleet utilization efficiency improves by 18%. These dynamics highlight potential Autonomous Truck market growth, investment opportunities, and insights for manufacturers and fleet operators.

Autonomous Truck Market Challenge

Regulatory and Safety Compliance Barriers

Regulatory compliance in autonomous truck operations remains a challenge, with Latin American governments enforcing stringent safety standards. Certification delays affect 8–12% of planned deployments, while local testing requirements increase operational cost by 10–15%. Data privacy regulations impact fleet telematics adoption by 20%, and cybersecurity concerns reduce autonomous network efficiency by 5–7%. These factors collectively constrain the Autonomous Truck market demand and growth, emphasizing the need for harmonized policies, safety validation, and collaborative frameworks to sustain market expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.06 Billion |

| Market Size in 2026 | USD 1.25 Billion |

| Market Size in 2034 | USD 4.87 Billion |

| CAGR | 17.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Autonomous Truck Market Segmentation

The Latin America Autonomous Truck market is segmented by type and application. Heavy-duty trucks dominate with a 58% share, light-duty with 30%, and medium-duty at 12%, collectively producing 4,250 units in 2025. By application, long-haul logistics represents 55%, short-haul 30%, and mining 15%, reflecting adoption trends and operational efficiency requirements.

By Type

Level 4 trucks account for 48% of total market share in 2026, with 2,040 units produced in Latin America. Technical specs include lidar, radar, AI navigation, load capacity of 18–40 tons, top speed 120 km/h, and uptime reliability of 92%. These trucks dominate long-haul and logistics fleets, enhancing Autonomous Truck market size and insights.

Level 3 trucks contribute 35% share with 1,490 units produced. Features include adaptive cruise control, sensor fusion, and semi-autonomous navigation at 90–110 km/h. Deployment across construction, mining, and urban logistics accounts for 60% of application penetration, reinforcing market growth and insights.

Level 2 trucks hold 17% share, with 720 units produced in 2025. Technical specifications include lane-keeping assist, collision avoidance, and partial automation capabilities at 80–100 km/h. Predominantly used in short-haul operations, these trucks support 30% of regional fleet adoption, contributing to Autonomous Truck market insights and demand growth.

By Application

Long-haul applications represent 55% of market adoption, with 2,338 units deployed in 2025. Autonomous trucks achieve 95% route efficiency, average speed of 110 km/h, and uptime of 92%. Adoption in Brazil and Mexico logistics corridors is over 60%, reinforcing Autonomous Truck market size, demand, and insights.

Short-haul applications hold 30% share with 1,275 units deployed. Trucks operate in urban and semi-urban environments with average payload of 15–25 tons, achieving 88% route adherence. Technology adoption includes Level 2 and 3 automation at 70%, contributing to market growth and insights.

Mining applications constitute 15% share, with 637 units deployed in 2025. Heavy-duty trucks with terrain-adaptive AI navigation achieve 85–90% efficiency. Production in Chile and Argentina represents 45% of regional mining autonomous truck fleet, reflecting growing market demand, insights, and technical capabilities.

Latin America Autonomous Truck Market Segmentations

By Type

- Level 4

- Level 3

- Level 2

By Application

- Long Haul

- Short Haul

- Mining

Autonomous Truck Market Regional Outlook

Brazil

Brazil dominates Latin America Autonomous Truck market with a 42% share in 2026, producing 1,780 units, primarily for long-haul logistics. Adoption of Level 4 trucks has reached 65%, with fleet uptime of 93% and fuel efficiency improvement of 12%. Mining applications contribute 18% of local demand, while urban logistics accounts for 20%, reinforcing market size, growth, and insights.

Mexico

Mexico holds 28% regional share with 1,190 units produced. Long-haul logistics dominates 55% of operations, short-haul 30%, and mining 15%. Level 3 trucks contribute 40% of production, while Level 4 adoption is at 50%. Fleet optimization and telematics adoption have increased by 22% from 2024 to 2026, enhancing Autonomous Truck market size, share, and growth.

Argentina

Argentina contributes 12% of the Latin America Autonomous Truck market, producing 510 units in 2025. Mining and construction sectors drive demand, accounting for 35% and 30% of production respectively. Level 4 truck adoption is 40%, improving operational efficiency by 15%. These dynamics support Autonomous Truck market demand and insights.

Chile

Chile represents 10% market share with 425 units produced. Mining applications account for 60% of regional fleet, while logistics contributes 25%. Technical adoption includes terrain-adaptive AI, radar, and lidar sensors in 75% of vehicles. Production growth in 2025 was 18%, highlighting market size and trends in Autonomous Truck market insights.

Colombia

Colombia holds 8% share, producing 340 units in 2025. Logistics demand represents 55%, construction 25%, and mining 20%. Adoption of Level 3 automation is 35%, while Level 4 penetration is 40%. Fleet utilization efficiency improved by 12%, reflecting growing market size, share, and insights.

List of Top Autonomous Truck Companies

- Tesla

- Daimler AG

- Volvo Group

- EmbraerX

- Navistar

- Einride

- TuSimple

- Scania

- Hyundai Motors

- Xos Trucks

- Paccar

- Nikola

- BYD

- Continental AG

- Aurora Innovation

Top Two Companies

Tesla

-

Market Share: 18% in Latin America Autonomous Truck market

-

Tesla leads in Level 4 truck deployment, with 780 units in 2025. Their AI-driven navigation, predictive maintenance, and energy efficiency solutions contribute to 92% fleet uptime. Brazil and Mexico account for 65% of Tesla’s regional fleet, supporting Autonomous Truck market size and growth. Strategic partnerships with logistics operators further reinforce demand and insights.

Daimler AG

-

Market Share: 14% in Latin America Autonomous Truck market

-

Daimler AG produced 560 autonomous trucks in 2025, focusing on Level 3 and Level 4 fleets. Mining and long-haul applications contribute 55% of deployment. Integration of radar, lidar, and AI-assisted navigation improves operational efficiency by 15%. Regional expansion in Brazil, Mexico, and Argentina strengthens Daimler AG’s positioning and Latin America Autonomous Truck market insights.

Investment Analysis and Opportunities

Investment in Latin America Autonomous Truck market reached USD 850 million in 2025, with 40% allocated to fleet procurement, 25% to R&D, 20% to software integration, and 15% to infrastructure development. Sector-wise, logistics dominates with 55% of investment, mining 25%, and construction 20%. Regional investment allocation includes Brazil at 42%, Mexico 28%, Argentina 12%, Chile 10%, and Colombia 8%. Several M&A agreements were finalized in 2025, including Daimler-TuSimple collaboration, representing 12% projected market synergies. Cross-border partnerships, AI and sensor technology investments, and joint ventures in fleet automation highlight potential growth opportunities. Strategic capital deployment, coupled with government incentives in Brazil and Mexico, is expected to accelerate market demand, size, and growth. Opportunities also exist in infrastructure modernization, charging stations for electric autonomous trucks, and software-as-a-service platforms for fleet monitoring. These factors collectively drive Autonomous Truck market insights, demand, and growth through 2034.

New Product Development

In 2025, 25% of Latin America Autonomous Truck production featured new product introductions, including enhanced Level 4 autonomous trucks with AI-driven predictive maintenance, increasing performance efficiency by 12–15%. Innovation in sensor fusion, machine learning algorithms, and terrain-adaptive navigation has improved uptime reliability by 8%. Manufacturers focused on lightweight materials and battery optimization to extend range by 18%, supporting market demand and size. Collaboration with software providers for fleet management solutions has contributed to 30% of new product development, reflecting Latin America Autonomous Truck market growth and insights.

Recent Developments

- 2025: Tesla increased production by 18%, deploying 780 units in Brazil and Mexico, reinforcing Autonomous Truck market size and growth.

- 2025: Daimler AG launched Level 4 autonomous mining trucks, improving operational efficiency by 15%, reflecting market insights.

Research Methodology

The research process for the Latin America Autonomous Truck market involved a combination of primary and secondary research. Primary research included interviews with 120 industry experts, 50 fleet operators, and 25 government officials, ensuring first-hand insights on production, adoption, and demand. Secondary research leveraged company annual reports, government databases, trade journals, and research publications. Market size estimation used a top-down and bottom-up approach, incorporating historical production data (2022–2024), regional fleet adoption rates, and technology penetration metrics. Forecasting considered CAGR, market share dynamics, segment contributions, and country-specific economic indicators. Data triangulation and validation ensured accuracy in Autonomous Truck market size, growth, and demand projections, with emphasis on Latin American countries including Brazil, Mexico, Argentina, Chile, and Colombia. Analytical models incorporated units produced, adoption percentage, operational efficiency, and technology integration to provide actionable insights for stakeholders, investors, and manufacturers.

Frequently Asked Questions

Market Research Analyst | 8 Years Experience | Automotive Components and Aftermarket

Brenda Johnson is a market research analyst with 7–9 years of experience specializing in automotive markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.