Europe Aircraft Auxiliary Power Unit (APU) Market Size

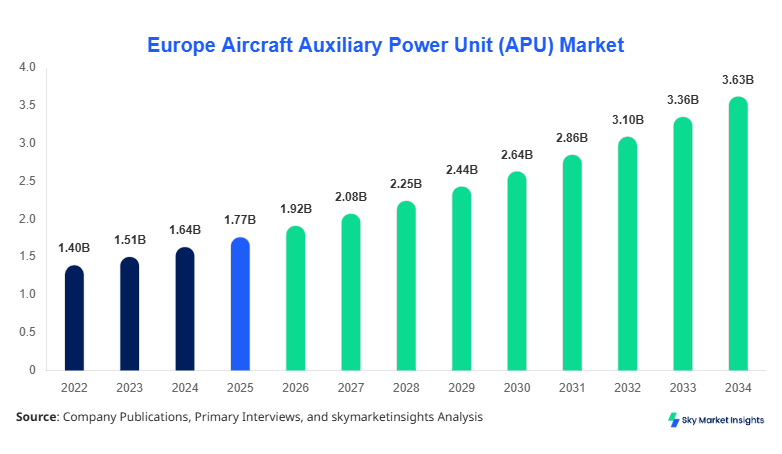

The European Aircraft Auxiliary Power Unit (APU) market size is projected at USD 1.92 billion in 2026 and is expected to hit USD 3.64 billion by 2034 with a CAGR of 8.3%. The market expansion is being driven by increasing aircraft fleet modernization programs, rising aircraft deliveries, and growing adoption of fuel-efficient onboard power systems across European aviation infrastructure. More than 7,200 aircraft operating across Europe currently utilize advanced APU systems for electrical power generation and pneumatic support during ground and in-flight operations. The competitive landscape includes major aerospace component manufacturers, turbine technology developers, and aircraft OEM-integrated suppliers focusing on lightweight systems, low-emission technologies, and digital monitoring platforms to strengthen Europe's Aircraft Auxiliary Power Unit (APU) market size.

The aircraft auxiliary power unit market refers to the manufacturing, integration, maintenance, and deployment of compact onboard power systems installed in aircraft to provide electrical energy and compressed air for engine start-up, cabin conditioning, and emergency backup operations. Europe produced more than 1,850 commercial and defense aircraft components in 2025, while over 68% of narrow-body aircraft in operation integrated upgraded APUs with fuel-saving capabilities. Adoption penetration across next-generation aircraft platforms exceeded 61% in Western Europe, with electric-assisted APUs gaining notable traction in regional jets and business aircraft. Commercial aviation accounted for nearly 56% of total application deployment, while military aviation contributed 28% and business aviation represented approximately 16%. Modern APUs deliver power outputs ranging from 40 kVA to 120 kVA and operate at fuel efficiency levels, improving by nearly 14% compared to legacy systems. Demand analytics indicate that airlines prioritize maintenance cycle extension by 18% and reduction of airport ground fuel consumption by 11%, reinforcing Europe's Aircraft Auxiliary Power Unit (APU) market share.

In the United Kingdom, the Aircraft Auxiliary Power Unit (APU) market accounted for nearly 24% of the European regional revenue in 2025, supported by the presence of more than 140 aerospace manufacturing facilities and over 310 aviation component suppliers. The country manufactured approximately 1,900 APU-related turbine assemblies and electrical control modules during 2025, while commercial aviation applications contributed nearly 58% of total installations. Military aircraft programs represented 27% of demand due to increased defense modernization expenditure exceeding USD 8.5 billion in aviation systems procurement. More than 63% of aircraft maintenance centers in the United Kingdom adopted predictive APU diagnostics platforms integrated with AI-driven monitoring systems. Electric APU deployment increased by 19% year-over-year as airlines sought lower emissions and reduced turnaround times. Heathrow, Manchester, and Gatwick collectively handled over 2.1 million aircraft movements requiring advanced auxiliary power systems, strengthening Europe's Aircraft Auxiliary Power Unit (APU) market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Aircraft Auxiliary Power Unit (APU) Market Trends

Increasing Adoption of Electrified APU Architectures

The European aviation industry is witnessing rapid adoption of electrified and hybrid APU systems to reduce fuel consumption and carbon emissions. More than 34% of newly delivered narrow-body aircraft in 2025 incorporated partially electrified auxiliary power architectures compared to only 18% in 2022. Aircraft operators reduced ground fuel burn by approximately 12% through advanced battery-assisted APUs capable of optimized power management during boarding and maintenance operations. European aerospace manufacturers invested over USD 620 million in electrical subsystem innovation programs between 2023 and 2025. Hybrid APUs delivering power capacities above 90 kVA gained increased adoption in long-haul commercial fleets and military surveillance aircraft. Nearly 48% of European airlines prioritized low-noise auxiliary systems for compliance with airport sustainability mandates. The rising integration of digital thermal management systems and advanced control software continues to accelerate the European Aircraft Auxiliary Power Unit (APU) market trend.

Rising Integration of Predictive Maintenance Technologies

Predictive analytics and digital twin technologies are becoming critical trends in the European aircraft auxiliary power unit ecosystem. More than 71% of tier-1 aviation maintenance providers implemented condition-monitoring platforms capable of tracking APU turbine temperature, vibration frequency, and fuel efficiency metrics in real time. Data generated from connected APUs exceeded 3.2 petabytes annually across Europe during 2025, allowing airlines to reduce unscheduled maintenance events by nearly 22%. Lufthansa Technik, Safran, and Honeywell increased investments in predictive maintenance algorithms capable of extending APU operational life by 17%. Airlines reported cost savings of approximately USD 85,000 per aircraft annually through optimized maintenance scheduling and lower downtime. The transition toward smart aviation ecosystems and digital aviation operations continues supporting Europe's Aircraft Auxiliary Power Unit (APU) market demand.

Growth in Defense Aviation Procurement

European defense aviation modernization programs are significantly influencing demand for advanced APUs. Military aircraft procurement across Europe increased by 14% in 2025, while defense aviation budgets surpassed USD 78 billion. Modern fighter aircraft and surveillance platforms require APUs with enhanced reliability, high-altitude performance, and rapid-start capability. More than 420 military aircraft retrofit programs across Germany, France, and the United Kingdom integrated upgraded gas turbine APUs with improved thermal resilience and 15% greater efficiency. NATO-aligned aviation modernization initiatives are supporting increased demand for ruggedized systems capable of operating under extreme environmental conditions. Long-endurance unmanned aerial systems also increasingly rely on compact APUs for emergency power support, accelerating Europe's Aircraft Auxiliary Power Unit (APU) market growth.

Europe Aircraft Auxiliary Power Unit (APU) Market Drivers

Expansion of Commercial Aircraft Fleet Modernization Programs

Europe’s commercial aviation sector continues to expand its investment in fuel-efficient and technologically advanced aircraft systems, driving strong demand for auxiliary power units. More than 2,850 commercial aircraft operating in Europe underwent cabin modernization and system upgrade programs during 2025, with over 62% integrating next-generation APUs. Airlines are prioritizing systems capable of reducing fuel burn by 10% to 14% during ground operations. Airbus delivered over 735 aircraft globally in 2025, while nearly 31% of those aircraft were allocated to European operators. The increasing need for uninterrupted cabin conditioning, electronic flight systems, and emergency electrical backup functions has accelerated installation rates of APUs across narrow-body and wide-body fleets. In addition, airport operational efficiency programs targeting reduced turnaround times by 18% are encouraging airlines to deploy APUs with faster engine start capabilities and improved thermal management. The integration of lightweight composite materials in turbine housing components has further improved operational efficiency while lowering maintenance frequency by approximately 16%, reinforcing Europe's Aircraft Auxiliary Power Unit (APU) market growth.

Europe Aircraft Auxiliary Power Unit (APU) Market Restraints

High Maintenance and Replacement Costs of Advanced APU Systems

Despite strong demand, high maintenance expenditure associated with advanced APUs remains a significant restraint for aircraft operators and regional airlines. The average overhaul cost for a modern gas turbine APU ranges between USD 280,000 and USD 450,000, depending on aircraft category and operational cycles. More than 39% of regional airlines across Europe reported delays in APU replacement programs due to increasing spare component costs and limited supply chain availability. Frequent inspections involving compressor blades, turbine bearings, and electronic controllers increase maintenance expenditure by nearly 13% annually. In addition, the shortage of skilled aerospace technicians across Europe exceeded 18,000 positions in 2025, resulting in longer repair turnaround times and increased aircraft downtime. Older aircraft fleets operating in Eastern Europe face challenges integrating next-generation APUs due to compatibility issues and retrofitting costs exceeding USD 1.2 million per aircraft. These operational and financial constraints continue to hinder rapid deployment across price-sensitive aviation operators, affecting Europe's Aircraft Auxiliary Power Unit (APU) market share.

Europe Aircraft Auxiliary Power Unit (APU) Market Opportunities

Rising Investments in Sustainable Aviation Infrastructure

The transition toward sustainable aviation presents substantial opportunities for aircraft auxiliary power unit manufacturers across Europe. More than USD 14 billion has been allocated toward green aviation initiatives by European governments and private aerospace organizations between 2025 and 2030. Airlines are increasingly investing in low-emission APUs capable of reducing carbon dioxide output by 20% and nitrogen oxide emissions by 15%. Nearly 44% of new airport infrastructure projects across Europe include electrified ground support compatibility aimed at optimizing APU operations. Hydrogen-compatible and hybrid-electric APU research projects increased by 27% in 2025, particularly in Germany and France. Aerospace OEMs are collaborating with battery technology companies to develop compact energy storage systems enabling quieter and more efficient auxiliary operations. Increased demand for sustainable business aviation and regional connectivity is expected to create significant deployment opportunities for advanced APUs across short-haul fleets and defense aviation applications, strengthening Europe's Aircraft Auxiliary Power Unit (APU) market demand.

Challenges in Europe: Aircraft Auxiliary Power Unit (APU) Market

Supply Chain Disruptions and Semiconductor Dependency

Supply chain volatility and semiconductor shortages continue to challenge APU manufacturers and aerospace suppliers across Europe. More than 46% of aviation component manufacturers reported procurement delays affecting turbine electronics, digital control units, and thermal sensors during 2025. Semiconductor lead times increased from 18 weeks in 2022 to nearly 39 weeks in 2025, disrupting production schedules and aircraft delivery timelines. Rising raw material costs for titanium alloys and nickel-based superalloys increased APU manufacturing expenditure by approximately 11%. In addition, geopolitical trade restrictions and logistics bottlenecks reduced the availability of precision aerospace components sourced from Eastern Europe and Asia-Pacific suppliers. Nearly 21% of OEMs reported contract delays associated with late delivery of integrated control modules. Smaller regional maintenance operators also face difficulties accessing certified replacement components within required timelines, affecting fleet operational efficiency. These structural supply chain issues remain a major challenge for sustainable European Aircraft Auxiliary Power Unit (APU) market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.77 Billion |

| Market Size in 2026 | USD 1.92 Billion |

| Market Size in 2034 | USD 3.64 Billion |

| CAGR | 8.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Aircraft Auxiliary Power Unit (APU) Market Segmentation

The European aircraft auxiliary power unit market is segmented by type and application, with gas turbine APUs dominating nearly 63% of the market due to widespread deployment in commercial and military aircraft fleets. Commercial aviation remained the leading application segment with more than 56% revenue contribution owing to increased aircraft utilization, passenger traffic growth, and fleet modernization programs.

By Type

Electric APUs represented approximately 21% of the European market in 2025 and are gaining strong adoption across regional aircraft and business jets. More than 680 electric-assisted APUs were deployed across Europe during the year, primarily in low-emission aircraft programs. These systems typically deliver power outputs ranging between 35 kVA and 75 kVA while reducing fuel consumption by nearly 14%. Airlines increasingly prefer electric APUs due to lower maintenance intervals and improved operational efficiency. Germany and France collectively contributed nearly 48% of electric APU installations due to substantial investments in sustainable aviation technologies. Lightweight battery systems and advanced thermal control modules have improved operational endurance by approximately 19%. Electric APUs are also enabling quieter airport operations with noise reduction levels exceeding 16 decibels compared to conventional systems.

Gas turbine APUs accounted for nearly 63% of the total market revenue and remain the dominant technology across commercial wide-body and defense aircraft. More than 4,500 aircraft operating in Europe rely on gas turbine APUs for engine start, cabin conditioning, and emergency electrical support. These systems operate at rotational speeds exceeding 45,000 rpm and deliver output capacities up to 120 kVA. Commercial airlines continue investing in upgraded gas turbine systems capable of improving fuel efficiency by 12% and reducing maintenance cycles by 15%. Military aviation programs across the United Kingdom and France expanded procurement of ruggedized turbine APUs with enhanced altitude tolerance and thermal resilience. The segment benefits from established infrastructure, proven reliability, and broad compatibility across legacy aircraft fleets.

Hybrid APUs represented nearly 16% of the European market in 2025 and are rapidly emerging as a preferred solution for sustainable aviation operations. More than 240 hybrid APU prototypes and commercial units entered testing and deployment phases across Europe during the year. These systems combine gas turbine functionality with battery-assisted power management to improve energy efficiency by approximately 20%. Hybrid APUs are increasingly utilized in long-range business jets and next-generation military surveillance aircraft. Airbus and several European aerospace technology firms are investing heavily in hybrid propulsion integration programs exceeding USD 420 million collectively. The technology also supports reduced airport emissions and optimized onboard electrical distribution systems, enhancing operational flexibility.

By Application

Commercial aviation dominated the market with approximately 56% share in 2025 due to rising passenger traffic and expansion of narrow-body aircraft fleets. European airlines operated more than 6,800 commercial aircraft equipped with APUs during the year. Modern commercial APUs provide electrical support for avionics, cabin air conditioning, and auxiliary hydraulic functions while improving aircraft turnaround efficiency by nearly 17%. Major airline operators increasingly prioritize low-noise and low-emission systems to comply with airport sustainability regulations. More than 61% of newly delivered aircraft integrated advanced predictive maintenance systems capable of monitoring turbine performance in real time. Growth in low-cost carrier operations across Spain and Italy has further strengthened demand for fuel-efficient APUs.

Military aviation accounted for approximately 28% of market demand, supported by rising defense budgets and fleet modernization initiatives. Europe deployed over 1,200 military aircraft utilizing advanced APUs for mission-critical onboard power generation and emergency operations. Modern military APUs deliver high-temperature resistance, rapid engine restart capability, and operational stability in extreme conditions. Defense aviation programs across Germany, France, and the United Kingdom increased procurement of upgraded APUs by nearly 18% in 2025. NATO-aligned aircraft modernization projects and surveillance drone expansion programs continue generating demand for compact and reliable auxiliary systems. Military APUs also support advanced communication systems, radar equipment, and onboard weapons management platforms.

Business jets represented nearly 16% of the market due to increasing demand for private aviation and executive travel across Europe. More than 1,450 business aircraft operating in Europe utilized advanced APUs for cabin comfort and electrical backup systems in 2025. Operators increasingly demand lightweight APUs capable of reducing operational costs by 11% while enhancing passenger comfort during extended ground operations. Hybrid and electric APUs are gaining traction in premium business aircraft due to lower noise emissions and reduced fuel burn. France and the United Kingdom accounted for over 46% of total business aviation APU installations. Increasing adoption of luxury aviation services and growth in charter operations continue to support the segment.

Europe Aircraft Auxiliary Power Unit (APU) Market Segmentations

Type

- Electric APU

- Gas Turbine APU

- Hybrid APU

Application

- Commercial Aviation

- Military Aviation

- Business Jets

Europe Aircraft Auxiliary Power Unit (APU) Market: Regional Outlook

United Kingdom

The United Kingdom accounted for approximately 24% of the European market revenue in 2025, supported by advanced aerospace manufacturing infrastructure and strong defense aviation expenditure. More than 140 aerospace facilities and over 310 aviation suppliers contributed to domestic APU production and integration activities. Commercial aviation represented nearly 58% of national demand, while military aviation contributed 27%. The country handled more than 2.1 million annual aircraft movements requiring efficient onboard auxiliary systems. Investments exceeding USD 2.4 billion in sustainable aviation technologies accelerated deployment of hybrid APUs and predictive maintenance systems.

Germany

Germany represented nearly 22% of the European market due to strong aerospace engineering capabilities and industrial automation leadership. More than 95 aerospace production facilities and 180 component suppliers supported aircraft system manufacturing in 2025. Commercial aircraft modernization programs increased by 17%, while over 52% of German airlines deployed digital APU monitoring platforms. The country also invested heavily in hydrogen-compatible aviation technologies and electric propulsion systems. Defense aviation applications accounted for nearly 31% of domestic demand.

France

France contributed approximately 19% of the regional market and remained a key hub for aerospace innovation and aircraft assembly operations. More than 120 aerospace manufacturing plants supported the domestic aviation ecosystem in 2025. Airbus-led procurement programs and advanced research partnerships accelerated development of hybrid APUs and lightweight turbine systems. Commercial aviation accounted for 54% of domestic demand, while business aviation contributed nearly 18%. France also allocated more than USD 1.8 billion toward sustainable aviation research programs.

Spain

Spain held nearly 11% of the European market revenue, driven by growth in low-cost airline operations and airport modernization initiatives. More than 75 aviation maintenance centers and component suppliers supported national APU deployment activities. Commercial aviation dominated domestic demand with nearly a 63% contribution due to strong tourism-driven air traffic. Investments in airport electrification and sustainable aviation fuel infrastructure increased by 14% during 2025. Business jet operations also expanded steadily across Madrid and Barcelona aviation hubs.

Italy

Italy accounted for approximately 10% of regional revenue owing to increasing business aviation activity and defense modernization programs. More than 60 aerospace manufacturing and maintenance facilities operated across the country in 2025. Commercial aircraft utilization increased by 13%, while military aviation procurement programs supported increased deployment of upgraded APUs with improved operational endurance. Italy also experienced rising charter aviation demand, particularly for executive and luxury travel applications. Hybrid APUs gained increasing adoption across premium aviation fleets.

Russia

Russia represented nearly 14% of the European market due to substantial military aviation activity and domestic aircraft manufacturing capacity. More than 190 aerospace facilities supported aviation component production and maintenance activities. Military aircraft accounted for nearly 49% of domestic APU demand owing to extensive defense aviation operations. The country increased investment in indigenous turbine technologies and localized aerospace manufacturing capabilities following international trade restrictions. Advanced APUs designed for harsh climate operations and long-range aviation platforms remained a key focus area

Top players in Europe's Aircraft Auxiliary Power Unit (APU)

- Honeywell International Inc.

- Safran S.A.

- Pratt & Whitney Canada

- RTX Corporation

- PBS Group

- The Marvin Group

- Technodinamika

- AeroControlex Group

- Liebherr-Aerospace

- Rolls-Royce Holdings plc

- MTU Aero Engines AG

- Meggitt PLC

- Elbit Systems Ltd.

- Hamilton Sundstrand

- Aerosila

Honeywell International Inc.

-

Honeywell International Inc. held approximately 18% of the European market revenue in 2025 due to its extensive commercial aviation partnerships and advanced turbine technology portfolio.

-

The company supplied APUs for more than 3,600 aircraft operating across Europe and increased investment in predictive maintenance software platforms by 21%.

-

Honeywell’s systems deliver improved fuel efficiency of nearly 14% and reduced maintenance downtime by 18%.

-

The company strengthened its positioning through collaborations with major airline operators and aircraft OEMs focused on next-generation sustainable aviation systems.

Safran S.A.

-

Safran S.A. accounted for nearly 15% of the regional market and maintained strong positioning through integrated aerospace manufacturing capabilities.

-

The company expanded hybrid-electric APU development programs with investments exceeding USD 350 million between 2023 and 2025.

-

Safran supplied advanced APUs for both commercial and military aircraft platforms and improved thermal efficiency by approximately 16%.

-

The company’s strategic partnerships with European defense aviation agencies and aircraft manufacturers strengthened its competitive positioning across multiple aircraft categories.

Investment Analysis

Investment activity across the European aircraft auxiliary power unit sector increased substantially during 2025, with total aerospace auxiliary systems investment exceeding USD 6.8 billion. Commercial aviation accounted for nearly 52% of total investment allocation, while defense aviation represented 34% and business aviation contributed 14%. Germany, France, and the United Kingdom collectively attracted more than 67% of all regional aerospace technology investments. Airlines increased expenditure on predictive maintenance software and electrified APU systems by approximately 23% compared to 2024. Venture capital funding for sustainable aviation component technologies surpassed USD 920 million during the year.

Mergers, acquisitions, and strategic collaborations continued shaping the competitive landscape. Aerospace OEMs increasingly partnered with semiconductor and battery manufacturers to improve onboard power management systems and thermal efficiency technologies. More than 28 collaboration agreements were announced across Europe between 2024 and 2025 involving digital aviation analytics, hybrid propulsion systems, and lightweight composite materials. Defense aviation modernization programs also generated long-term procurement contracts valued above USD 4.3 billion for advanced APUs and related aerospace systems. Cross-border aerospace partnerships between the United Kingdom, Germany, and France strengthened localized manufacturing capabilities and reduced dependency on external component suppliers.

The growing emphasis on sustainable aviation infrastructure has further accelerated private equity participation in low-emission aerospace technologies. Nearly 31% of total aviation technology investments in Europe targeted carbon reduction initiatives and hybrid-electric propulsion systems. Airport operators and aviation service providers are also increasing capital allocation toward electrified ground support systems compatible with advanced APUs. These long-term investment patterns continue creating strong commercialization opportunities across Europe.

New Product Developments

European aerospace manufacturers introduced several advanced APU technologies during 2025 focused on efficiency, sustainability, and predictive maintenance capabilities. Nearly 26% of newly launched auxiliary systems incorporated hybrid-electric functionality and digital thermal monitoring technologies. Advanced turbine blade materials improved operational durability by approximately 18%, while lightweight composite housings reduced overall system weight by 11%. More than 34 new APU-related aerospace patents were filed across Europe during the year.

Manufacturers also focused on reducing acoustic emissions and improving energy optimization. Next-generation APUs demonstrated fuel consumption reductions ranging from 12% to 17% compared to earlier systems. Several aerospace companies launched AI-integrated control systems capable of real-time performance optimization and predictive maintenance analytics. These technological innovations continue supporting operational efficiency and sustainability objectives across commercial and defense aviation sectors.

Recent Developments in Europe's Aircraft Auxiliary Power Unit (APU)

- 2025: Honeywell International expanded production capacity for hybrid APUs in Europe by 19% to support increasing demand from commercial airlines transitioning toward sustainable aviation systems. The expansion included new predictive maintenance software integration and enhanced thermal efficiency capabilities. The company also increased R&D investment in electric-assisted turbine technologies and secured multiple airline modernization contracts across Germany and the United Kingdom.

- 2025: Safran S.A. introduced a next-generation low-emission gas turbine APU capable of reducing fuel consumption by approximately 15% and lowering nitrogen oxide emissions by 12%. The product launch targeted narrow-body aircraft modernization programs and included advanced digital diagnostics functionality. Safran also strengthened partnerships with European aircraft manufacturers to expand deployment across regional aviation fleets.

Research Methodology

The European aircraft auxiliary power unit market report was developed using a combination of primary and secondary research methodologies to ensure accurate forecasting and comprehensive industry evaluation. The research process included extensive analysis of aerospace manufacturing databases, aviation regulatory publications, airline procurement records, company annual reports, and aircraft fleet deployment statistics across Europe. Primary research involved interviews with aerospace engineers, aviation maintenance providers, aircraft OEM executives, and airline procurement managers to validate market assumptions and operational trends. Secondary research incorporated data from aerospace associations, government aviation authorities, defense procurement agencies, and aircraft maintenance organizations. Market size estimation was conducted using bottom-up and top-down analytical models integrating aircraft fleet numbers, APU installation rates, production volumes, and average component pricing structures. Forecasting models also considered macroeconomic indicators, defense expenditure trends, sustainable aviation investments, and aircraft delivery projections between 2026 and 2034. Data triangulation and validation techniques were applied to ensure statistical consistency and reliable market interpretation across all regional and segmental analyses.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.