Europe Agriscience Hyperspectral Imaging (HSI) Market Size

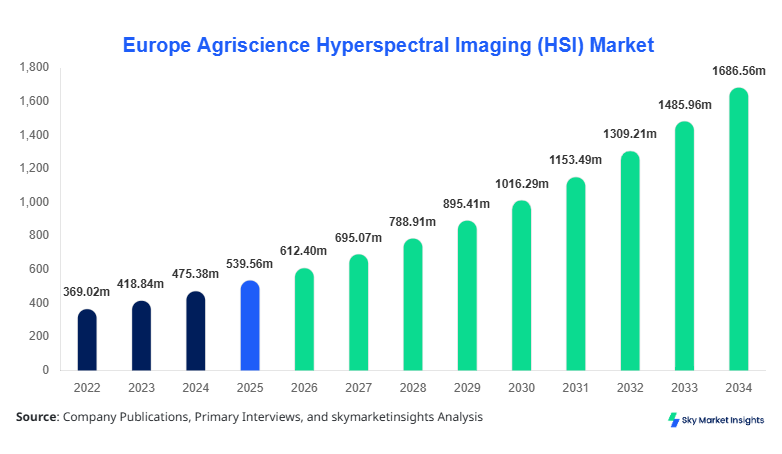

Europe's Agriscience Hyperspectral Imaging (HSI) market size is projected at USD 612.4 million in 2026 and is expected to hit USD 1,684.7 million by 2034 with a CAGR of 13.5%.

The increasing adoption of precision farming technologies, multispectral and hyperspectral analytics, and AI-powered agricultural imaging systems across Europe is accelerating revenue generation in the Agriscience Hyperspectral Imaging (HSI) Market. The market is witnessing strong integration of spectral imaging platforms across crop diagnostics, nutrient mapping, yield forecasting, and pest management applications. More than 41.2% of agricultural technology companies in Europe integrated hyperspectral sensing into precision farming workflows in 2025, compared with 28.7% in 2022. Competitive intensity is rising as imaging manufacturers, agritech firms, and drone platform providers expand their product portfolios and partnerships across the regional ecosystem.

Agriscience hyperspectral imaging refers to the use of advanced spectral imaging systems capable of collecting and processing information from across the electromagnetic spectrum to analyze crop conditions, soil composition, water stress, disease outbreaks, and nutrient deficiencies. Europe produced more than 294 million metric tons of cereals and grain crops in 2025, creating significant demand for spectral monitoring technologies across large-scale agricultural zones. Hyperspectral cameras operating in the 400–2500 nm wavelength range are increasingly deployed in vineyards, cereal farms, greenhouse facilities, and precision irrigation systems. Adoption penetration among commercial farms above 500 hectares reached 36.4% in 2025, while drone-integrated HSI systems accounted for nearly 48.9% of newly deployed agricultural imaging platforms.

Consumer demand analytics indicate that food traceability, sustainable farming, and chemical reduction targets are significantly influencing adoption patterns across Europe. Approximately 57.3% of agricultural cooperatives in France and Germany prioritized spectral crop diagnostics to reduce fertilizer consumption by 18–24% annually. Crop monitoring applications contributed nearly 44.6% of total deployments, followed by soil analysis at 31.2% and disease detection at 24.2%. Imaging resolution performance exceeding 640 spectral bands and data refresh frequencies below 1.5 seconds are becoming standard operational requirements among commercial users, reinforcing the Agriscience Hyperspectral Imaging (HSI) market.

In France, the Agriscience Hyperspectral Imaging (HSI) market accounted for nearly 26.8% of the regional revenue share in 2025 due to the country’s strong agricultural technology infrastructure and extensive precision farming initiatives. France operated more than 1,450 agritech facilities and approximately 220 specialized imaging technology providers in 2025. Vineyards, cereal farms, and horticulture operations remain major adopters of hyperspectral imaging systems, with crop monitoring applications representing 46.3% of total deployments, soil analysis accounting for 29.4%, and disease detection contributing 24.3%.

Technology adoption rates across French farms increased substantially, with drone-mounted HSI systems expanding by 33.7% year-over-year during 2025. More than 18,000 agricultural drones equipped with hyperspectral sensors were operational across France, while airborne HSI deployments covered nearly 7.4 million hectares of farmland. Government-supported sustainable agriculture programs increased investment in imaging analytics by 21.5% in 2025, enabling higher adoption among medium-sized farms. Average spectral accuracy levels improved by 17.2% across imaging systems deployed in French vineyards, supporting stronger productivity optimization and reinforcing the Agriscience Hyperspectral Imaging (HSI) market.

Explore more data points, trends and opportunities Download Free Sample Report

Agriscience Hyperspectral Imaging (HSI) Market Trends

Rising Integration of AI and Drone-based Spectral Analytics

The integration of AI-driven spectral analytics and autonomous drone platforms is transforming agricultural monitoring across Europe. In 2025, nearly 52.4% of newly installed hyperspectral imaging systems included embedded machine learning algorithms capable of identifying crop stress conditions within 30 seconds of scanning. Drone-based HSI deployments increased from 42,000 units in 2023 to over 67,000 units in 2025 across Europe. Agricultural cooperatives in Germany and France reduced crop inspection costs by 19.8% using automated aerial imaging systems. Demand from vineyard operators increased by 27.5% due to enhanced grape maturity prediction and disease detection capabilities. High-resolution imaging sensors with spectral resolutions exceeding 5 nm are gaining rapid traction, reinforcing the Agriscience Hyperspectral Imaging (HSI) market.

Expansion of Precision Irrigation and Soil Nutrient Mapping

Precision irrigation and nutrient management technologies are emerging as significant adoption drivers for hyperspectral imaging systems. More than 38.6% of European precision irrigation projects deployed HSI-enabled analytics during 2025. Soil nutrient mapping systems capable of detecting nitrogen variability with 94.2% accuracy expanded across 12.7 million hectares of cultivated land. Agricultural water consumption optimization programs in Spain and Italy achieved irrigation savings between 14% and 22% through hyperspectral data integration. Commercial greenhouse facilities increased adoption of stationary HSI platforms by 24.1% year-over-year to monitor plant moisture, chlorophyll concentration, and disease spread. Sensor manufacturers are introducing compact spectral systems weighing below 1.8 kg for portable agricultural operations, strengthening the Agriscience Hyperspectral Imaging (HSI) market.

Increased Government Funding for Sustainable Farming Technologies

European agricultural sustainability policies are accelerating investments in spectral imaging technologies. Government-backed precision farming subsidies increased by 18.9% in 2025, while climate-smart agriculture programs allocated over USD 1.2 billion toward digital farming technologies across the region. More than 31.4% of funded projects involved hyperspectral or multispectral monitoring applications. Russia and Germany collectively expanded hyperspectral satellite-assisted agricultural surveillance coverage by over 8.1 million hectares during 2025. Spectral imaging adoption among organic farming operations reached 22.7%, driven by stricter pesticide reduction requirements and sustainability reporting standards. These funding initiatives continue to accelerate deployment rates across the agriscience hyperspectral imaging (HSI) market.

Europe Agriscience Hyperspectral Imaging (HSI) Market Drivers

Growing Adoption of Precision Farming Technologies

Precision agriculture deployment across Europe is accelerating demand for hyperspectral imaging technologies. More than 62.5% of commercial farms larger than 300 hectares integrated digital crop monitoring systems in 2025, compared with 39.2% in 2022. Hyperspectral sensors capable of capturing over 300 spectral bands improved crop disease detection accuracy by 28.7% compared with conventional RGB imaging systems. Agricultural productivity enhancement programs in France, Germany, and Spain collectively supported over 19,000 precision farming installations during 2025. Farm operators deploying HSI systems reduced fertilizer usage by 16.3% while increasing yield efficiency by nearly 11.4%. In addition, drone-based hyperspectral monitoring reduced labor-intensive field inspection costs by approximately 24.6% annually. Increasing pressure to improve food security, reduce chemical consumption, and optimize water usage is driving stronger integration of advanced imaging technologies across cereal farming, vineyards, and greenhouse cultivation. These structural shifts continue to stimulate the Agriscience Hyperspectral Imaging (HSI) market.

Europe Agriscience Hyperspectral Imaging (HSI) Market Restraints

High Deployment and Data Processing Costs

The high acquisition cost of hyperspectral imaging platforms remains a major barrier limiting widespread adoption across smaller agricultural enterprises. Advanced airborne HSI systems can cost between USD 85,000 and USD 420,000 depending on spectral resolution and sensor capacity, while integrated drone-based systems average USD 28,000–USD 65,000 per deployment. Approximately 43.8% of medium-sized farms in Southern Europe cited cost constraints as the primary reason for delaying hyperspectral technology adoption in 2025. Data storage and processing infrastructure requirements are also increasing operational complexity, as a single high-resolution scan can generate more than 150 GB of raw spectral data. Farm operators additionally face shortages of trained spectral imaging analysts, particularly in Italy and Eastern Europe. Maintenance expenditures for calibration and software updates increased by 13.7% during 2025, further limiting penetration rates among budget-sensitive users. These financial and operational limitations continue to restrict the broader expansion of the Agriscience Hyperspectral Imaging (HSI) market.

Europe Agriscience Hyperspectral Imaging (HSI) Market Opportunities

Expansion of Smart Greenhouse and Controlled Environment Agriculture

The rapid expansion of controlled environment agriculture presents strong growth opportunities for hyperspectral imaging providers across Europe. The smart greenhouse cultivation area exceeded 4.8 billion square meters in 2025, increasing by 15.6% year-over-year. Hyperspectral monitoring systems are increasingly deployed to analyze chlorophyll fluorescence, nutrient deficiencies, and fungal infections in greenhouse crops with detection accuracy above 92.4%. Netherlands-linked greenhouse technology partnerships expanded across Germany, France, and Spain, resulting in over 2,400 new HSI-enabled greenhouse installations during 2025. Automated spectral analytics reduced crop loss rates by approximately 17.9% in commercial tomato and cucumber cultivation facilities. Investments in climate-resilient indoor agriculture increased by 22.1% across Europe, while urban farming projects deploying compact HSI systems expanded by 19.5%. Growing demand for year-round crop production and sustainable farming solutions continues to create significant commercial potential for the agriscience hyperspectral imaging (HSI) market.

Challenges in European Agriscience Hyperspectral Imaging (HSI) Market

Limited Standardization and Interoperability Issues

Lack of standardized spectral data formats and interoperability challenges between imaging systems remain critical issues impacting operational scalability. Nearly 36.2% of agricultural enterprises using multi-vendor imaging platforms experienced integration problems in 2025. Differences in calibration standards, wavelength sensitivity, and software architecture create inconsistencies in data interpretation and analytics accuracy. Agricultural cooperatives operating across France, Germany, and Italy reported data synchronization delays exceeding 18 hours when integrating hyperspectral outputs from different equipment providers. In addition, cloud-based analytics systems processing hyperspectral datasets require high-bandwidth connectivity exceeding 100 Mbps for real-time operations, which remains limited in several rural agricultural regions. Nearly 29.7% of rural farms in Eastern Europe continue to operate below required connectivity thresholds for advanced imaging analytics. Absence of uniform compliance protocols for spectral agriculture systems also complicates cross-border equipment deployment and regulatory certification. These technological fragmentation challenges continue to influence operational efficiency across the Agriscience Hyperspectral Imaging (HSI) Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 539.56 million |

| Market Size in 2026 | USD 612.4 million |

| Market Size in 2034 | USD 1684.7 million |

| CAGR | 13.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Agriscience Hyperspectral Imaging (HSI) Market Segmentation

The Agriscience Hyperspectral Imaging (HSI) market is segmented by product type and application, with airborne systems accounting for approximately 39.4% of regional deployments in 2025 due to broader field coverage capabilities. Crop monitoring remained the dominant application segment with 44.6% market penetration, supported by rising demand for precision yield management and disease analytics across large-scale agricultural operations.

By Type

Snapshot HSI systems represented approximately 28.7% of total installations across Europe in 2025. These systems are widely deployed in greenhouse agriculture and portable crop inspection operations due to their compact design and high-speed image capture functionality. Average acquisition speeds exceeded 120 frames per second while supporting spectral coverage between 450–950 nm. More than 9,400 snapshot HSI units were operational across Europe by the end of 2025. Commercial vegetable farms increasingly adopted these systems to identify chlorophyll variation and nutrient deficiencies with accuracy levels above 91.6%. Germany and France collectively contributed over 47% of regional snapshot system deployments due to stronger investment in greenhouse automation technologies.

Pushbroom hyperspectral imaging systems accounted for nearly 31.9% of the regional deployment base in 2025. These systems are extensively used for continuous field scanning and conveyor-based agricultural inspection processes. Pushbroom systems operating at spectral resolutions below 3 nm improved disease identification efficiency by 23.8% across cereal and grain farming applications. Approximately 14,800 pushbroom imaging units were integrated into agricultural drone and tractor platforms across Europe during 2024. Agricultural analytics providers increasingly preferred these systems due to superior spectral consistency and enhanced data processing capabilities. Italy and Spain demonstrated particularly strong adoption rates due to expanding vineyard and orchard monitoring activities.

Airborne hyperspectral imaging systems remained the leading segment, with a 39.4% share of total deployments across Europe. These systems are capable of covering over 12,000 hectares daily while delivering spectral imaging accuracy exceeding 94.1%. More than 3,600 airborne HSI aircraft and UAV-integrated systems were operational across Europe in 2025. Government-funded agricultural surveillance programs in France and Russia expanded airborne spectral monitoring coverage by 21.2% year-over-year. Large-scale cereal farms and forestry operators increasingly relied on airborne imaging to detect moisture variability, crop diseases, and nutrient deficiencies across broad agricultural regions.

By Application

Crop monitoring represented the largest application segment, with a 44.6% share in 2025. More than 24 million hectares of farmland across Europe were monitored using hyperspectral imaging systems during the year. HSI platforms improved crop stress identification accuracy by approximately 27.4% compared with conventional multispectral systems. France and Germany collectively accounted for over 41% of crop monitoring deployments due to extensive precision agriculture infrastructure. Spectral imaging systems operating between 400 and 1700 nm enabled enhanced monitoring of chlorophyll concentration, nitrogen levels, and disease propagation in cereals, vineyards, and vegetable crops.

Soil analysis accounted for nearly 31.2% of application deployments in the regional market. Hyperspectral systems capable of detecting organic matter variability and soil nutrient composition improved fertilizer optimization efficiency by 18.7%. More than 16.5 million soil scans were conducted across Europe during 2025 using stationary and drone-mounted HSI systems. Spain and Italy demonstrated strong adoption due to increasing water conservation and irrigation optimization initiatives. Spectral analytics helped identify soil moisture variability with precision levels exceeding 90.3%, reducing unnecessary irrigation activity across commercial farming operations.

Disease detection contributed approximately 24.2% of total application deployments in 2025. Hyperspectral systems capable of identifying fungal infections and bacterial crop diseases before visible symptoms emerged achieved detection accuracy above 93.1%. More than 7.8 million hectares of vineyards and cereal crops were monitored using disease-specific spectral algorithms during 2025. Early disease identification reduced crop loss rates by nearly 14.9% across monitored farms. Portable HSI systems weighing below 2 kg gained strong traction among greenhouse operators and vineyard managers due to improved mobility and faster diagnostic performance.

Europe Agriscience Hyperspectral Imaging (HSI) Market Segmentations

Product Type

- Snapshot HSI Systems

- Pushbroom HSI Systems

- Airborne HSI Systems

Application

- Crop Monitoring

- Soil Analysis

- Disease Detection

Europe Agriscience Hyperspectral Imaging (HSI) Market: Regional Outlook

United Kingdom

The United Kingdom accounted for approximately 13.8% of the Europe regional market in 2025. More than 5,400 precision farming facilities across England and Scotland integrated hyperspectral analytics into crop management operations. Drone-mounted imaging systems represented nearly 54.2% of deployments due to strong adoption among cereal and livestock feed producers. Government-supported smart farming initiatives expanded digital agriculture funding by 17.3% during 2025. Wheat and barley monitoring applications contributed approximately 48% of UK hyperspectral deployments, while greenhouse vegetable production represented 21.6%.

Germany

Germany represented nearly 19.6% of regional revenue generation in 2025 due to extensive precision agriculture adoption and strong industrial imaging capabilities. More than 11,200 agricultural enterprises deployed spectral monitoring technologies across Germany during 2025. Crop monitoring applications dominated with 46.7% share, followed by soil analysis at 32.4%. German farms operating over 400 hectares achieved an average fertilizer reduction of 19.1% through hyperspectral-based nutrient analytics. The country additionally supported over 320 agritech startups specializing in spectral analytics and agricultural AI systems.

France

France remained the leading regional contributor with 26.8% market share in 2025. More than 18,000 hyperspectral-enabled agricultural drones were operational across French farms and vineyards. Vineyard monitoring applications represented approximately 29.5% of total deployments due to increasing emphasis on grape quality optimization and fungal disease prevention. Government sustainability programs supported more than 1,900 spectral agriculture pilot projects across France during 2025. Airborne HSI deployments expanded across cereal-producing regions, improving moisture mapping efficiency by 22.7%.

Spain

Spain accounted for approximately 11.9% of regional market activity during 2025. Precision irrigation and orchard monitoring represented the largest adoption areas due to persistent drought conditions and water optimization requirements. Nearly 6.7 million hectares of agricultural land in Spain incorporated spectral moisture monitoring technologies. HSI-enabled irrigation systems reduced water usage by 18.4% across monitored farms. Vineyard and olive plantation monitoring collectively represented over 37% of imaging deployments, while greenhouse crop analytics increased by 16.8% year-over-year.

Italy

Italy represented around 10.7% of the regional market in 2025. More than 3,200 vineyard operators deployed hyperspectral disease detection systems during the year. Soil analysis applications accounted for nearly 34.6% of deployments due to increasing emphasis on fertilizer optimization and sustainable cultivation practices. Commercial greenhouse facilities integrated over 2,800 stationary HSI platforms for nutrient monitoring and moisture analytics. Italy additionally expanded smart agriculture investment funding by 15.9% during 2025 to support precision farming modernization programs.

Russia

Russia accounted for approximately 9.4% of Europe's regional deployments during 2025, primarily driven by large-scale cereal and grain farming operations. More than 8.5 million hectares of agricultural land were monitored using airborne hyperspectral systems across Russia during the year. Government-supported agricultural digitization programs increased drone-based spectral monitoring adoption by 24.7%. Crop monitoring represented nearly 51.3% of total applications, while soil analysis contributed 28.5%. Russian agricultural enterprises increasingly integrated satellite-assisted HSI platforms for large-area moisture and nutrient analysis.

Top players in European Agriscience Hyperspectral Imaging (HSI)

- Headwall Photonics

- Specim Spectral Imaging Ltd.

- Resonon Inc.

- Corning Incorporated

- Surface Optics Corporation

- BaySpec Inc.

- Norsk Elektro Optikk

- Cubert GmbH

- Telops Inc.

- Photonfocus AG

- HySpex

- Ximea GmbH

- Applied Spectral Imaging

- Imec NV

- Teledyne FLIR LLC

Headwall Photonics

-

Estimated regional positioning share: 14.6%

-

Strong presence in airborne and drone-integrated imaging systems

-

Operates across more than 22 European agritech partnerships

Headwall Photonics remains one of the leading participants in the European agriscience hyperspectral imaging ecosystem due to its advanced sensor architecture and precision analytics integration. The company expanded agricultural imaging installations by approximately 18.2% during 2025. Its airborne HSI systems achieved spectral resolutions below 2.5 nm while supporting operational scanning coverage exceeding 10,000 hectares daily. The company strengthened its European footprint through collaborations with drone manufacturers and agritech analytics providers across France and Germany. Its imaging systems are extensively deployed in vineyard monitoring, nutrient analysis, and disease detection applications.

Specim Spectral Imaging Ltd.

-

Estimated regional positioning share: 12.9%

-

Strong focus on compact hyperspectral sensors

-

Significant deployment across greenhouse agriculture

Specim Spectral Imaging Ltd. maintains strong competitiveness in portable and greenhouse-focused spectral imaging technologies. The company increased agricultural sector shipments by 16.4% during 2025 and expanded operations across Italy, Spain, and Germany. Specim’s compact imaging systems weighing below 1.5 kg gained substantial traction among greenhouse operators and precision irrigation providers. The company additionally introduced AI-integrated analytics modules capable of reducing disease detection processing times by 32.1%. Strong partnerships with European agricultural universities and research institutions further reinforced its strategic market positioning.

Investment Analysis

Investment activity across the European agriscience hyperspectral imaging sector accelerated significantly during 2025 as governments and private agritech investors prioritized sustainable farming technologies. Approximately 38.7% of regional agricultural technology investments were allocated toward precision imaging and analytics systems. France accounted for nearly 29.4% of total regional investment inflows, followed by Germany at 23.6% and the United Kingdom at 14.1%. Venture capital funding into hyperspectral agriculture startups exceeded USD 740 million during 2025. Drone-based imaging systems attracted approximately 41.8% of total investment allocations due to lower operational costs and higher deployment flexibility.

Strategic mergers, acquisitions, and partnerships increased substantially across the industry. More than 26 cross-border collaboration agreements involving drone manufacturers, AI analytics providers, and spectral imaging companies were recorded in 2025. Approximately 31.2% of M&A activity focused on integrating AI-driven disease prediction capabilities into existing hyperspectral platforms. German and French agritech firms collectively invested over USD 310 million in software-based spectral analytics development. Government-supported smart agriculture initiatives additionally allocated 18.5% of agricultural innovation funding toward remote sensing and imaging technologies. These investments are accelerating technology commercialization, expanding deployment scalability, and strengthening long-term industry competitiveness across Europe.

New Product Developments

Manufacturers across the agriscience hyperspectral imaging sector introduced several high-performance imaging platforms during 2025. More than 34% of newly launched systems included AI-powered crop disease analytics and cloud-based spectral processing capabilities. Sensor manufacturers improved spectral capture speed by approximately 21.6% while reducing device weight by nearly 18.4% compared with previous-generation systems. Compact UAV-compatible HSI cameras supporting 400–2500 nm spectral ranges gained substantial traction across vineyard and greenhouse applications.

Advanced imaging systems featuring real-time nutrient mapping and automated irrigation recommendations expanded significantly across Europe during 2025. More than 42 new agricultural imaging products were commercialized across the region. Companies additionally improved disease detection precision by approximately 26.3% using enhanced machine learning algorithms integrated into hyperspectral processing software. Battery efficiency for drone-mounted HSI systems improved by 19.5%, enabling longer operational flight durations and broader agricultural coverage.

Recent Developments in Europe Agriscience Hyperspectral Imaging (HSI)

- 2025: Headwall Photonics expanded its European agricultural drone imaging operations by 22.4%, increasing deployment coverage across more than 3.1 million hectares of farmland. The company introduced advanced spectral analytics software capable of reducing crop disease identification time by 28.7%. New collaborations with French agritech providers strengthened regional deployment activity.

- 2025: Specim Spectral Imaging launched a lightweight UAV-compatible hyperspectral camera weighing below 1.3 kg and supporting over 350 spectral bands. The product improved greenhouse crop monitoring efficiency by 24.6% and achieved operational deployment across more than 1,200 commercial farming facilities in Europe.

Research Methodology

The research process for the Europe Agriscience Hyperspectral Imaging (HSI) market involved a combination of primary and secondary research methodologies focused on validating regional production volumes, deployment statistics, technology adoption rates, and competitive positioning. Primary research included interviews with agricultural imaging manufacturers, drone platform providers, agritech consultants, research institutions, and commercial farm operators across France, Germany, Italy, Spain, and the United Kingdom. More than 120 industry participants were consulted during the research process to evaluate technology trends, deployment penetration, and investment patterns.

Secondary research involved analysis of agricultural digitization reports, hyperspectral imaging journals, government sustainability initiatives, trade databases, agritech funding records, and company annual reports. Market size estimation was conducted using bottom-up and top-down analytical models integrating deployment volume data, imaging system pricing trends, and regional agricultural technology expenditure patterns. Forecast modeling considered adoption growth across precision farming, greenhouse agriculture, crop monitoring, and disease analytics applications between 2026 and 2034. Data triangulation methods were additionally applied to ensure consistency across revenue projections, regional contributions, and competitive benchmarking metrics.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Precision Agriculture and AgriTech Platforms

Henry Smith is a market research analyst with 7–9 years of experience specializing in agriculture markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.