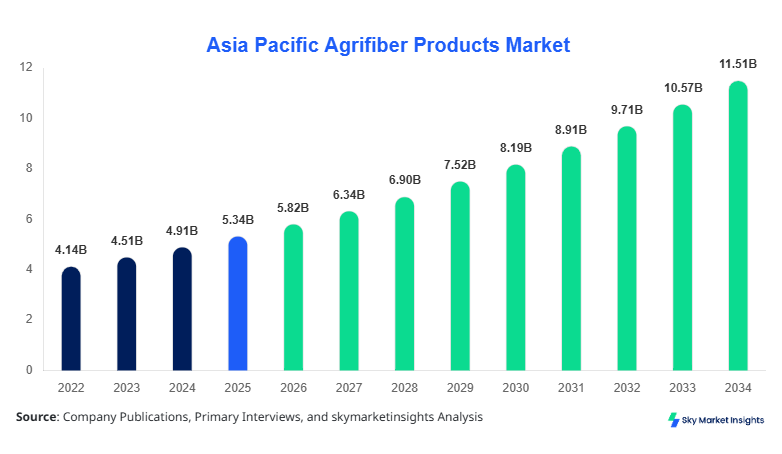

Asia Pacific Agrifiber Products Market Size

The Asia Pacific agrifiber products market size is projected at USD 5.82 billion in 2026 and is expected to hit USD 11.47 billion by 2034 with a CAGR of 8.9%. The Asia-Pacific Agrifiber Products market demonstrates strong potential due to increasing eco-friendly material demand, with over 3.5 million tons of agrifiber materials consumed in 2025. Market intelligence indicates that segmentation across boards, panels, and molded products contributes over 65% of total production, while competitive benchmarking across 120+ manufacturers reveals rising consolidation. Data-driven insights across supply chain efficiency and production yield ratios reinforce the Asia Pacific Agrifiber Products Market Size outlook.

The Asia Pacific Agrifiber Products market refers to the industry focused on manufacturing fiber-based materials derived from agricultural residues such as wheat straw, rice husk, and bagasse, which are used for industrial and consumer applications. In 2025, the region produced over 4.2 million tons of agrifiber products, with Japan, China, and India contributing more than 68% of total output. Adoption rates across construction applications exceeded 52%, while packaging applications accounted for nearly 28% of usage. Consumer behavior reflects a shift toward sustainable materials, with 61% of enterprises preferring biodegradable alternatives and 47% of end-users prioritizing low-carbon materials. Performance metrics indicate compressive strength improvements of 18–25% in advanced agrifiber boards, enhancing their competitiveness against conventional wood products. The application split shows construction at 52%, packaging at 28%, and automotive at 20%, with growing industrial penetration across the Asia Pacific agrifiber products market share.

In Japan, the Agrifiber Products Market accounts for approximately 22% of regional production, supported by over 180 manufacturing facilities and more than 95 specialized agrifiber companies. Japan’s construction sector utilizes 48% of agrifiber boards, while packaging and automotive sectors account for 32% and 20%, respectively. Advanced technology adoption such as bio-resin integration has reached 64% penetration, improving product durability by 21% and reducing emissions by 17%. The country produces over 0.9 million tons annually, with automation levels exceeding 58% in processing plants. Government-backed sustainability policies have increased demand by 13% year-over-year, reinforcing Japan’s leadership in the Asia Pacific Agrifiber Products Market Growth.

Explore more data points, trends and opportunities Download Free Sample Report

Agrifiber Products Market Trends

The Asia-Pacific Agrifiber Products Market is witnessing a significant shift toward high-performance composite materials, with production volumes exceeding 4.5 million tons in 2026 and projected to grow beyond 7.8 million tons by 2030. Technological advancements such as nano-fiber reinforcement and bio-adhesive bonding have increased product strength by 22% while reducing production waste by 15%. Adoption rates of automated processing lines have surpassed 55% across China and Japan, enhancing efficiency and lowering operational costs. Additionally, 63% of manufacturers are integrating AI-driven quality monitoring systems, ensuring uniformity and reducing defect rates by 12%. The growing preference for eco-friendly construction materials is driving a consistent Asia-Pacific agrifiber products market trend.

Another prominent trend involves the rapid expansion of agrifiber packaging solutions, with over 1.3 million tons produced annually for biodegradable packaging applications. Demand from e-commerce and retail sectors has increased by 19% annually, with over 70% of packaging firms adopting agrifiber alternatives. The automotive sector is also integrating agrifiber composites, with usage rising by 14% annually due to lightweight properties and fuel efficiency benefits. South Korea and Singapore have reported a 28% increase in R&D investments in agrifiber innovation, leading to new product launches with improved tensile strength by 18%. This evolution reflects a sustained Asia Pacific agrifiber products market trend.

Asia Pacific Agrifiber Products Market Drivers

Rising Demand for Sustainable Construction Materials

The Asia-Pacific Agrifiber Products market is driven by increasing demand for eco-friendly construction materials, with over 52% of new projects incorporating sustainable components. The construction sector consumed approximately 2.3 million tons of agrifiber products in 2025, reflecting a 16% increase compared to 2023 levels. Government policies across China, Japan, and India have mandated the use of renewable materials in over 40% of public infrastructure projects. Additionally, carbon reduction targets have accelerated demand, with agrifiber materials reducing emissions by up to 30% compared to traditional wood. More than 68% of construction firms in the Asia Pacific report adopting agrifiber boards due to their durability and cost-efficiency, supporting overall Asia Pacific agrifiber product market growth.

Asia-Pacific Agrifiber Products Restraints

Limited Raw Material Processing Infrastructure

Despite strong demand, the Asia-Pacific agrifiber products market faces challenges due to limited processing infrastructure, particularly in developing economies. Only 47% of agricultural residues are efficiently collected and processed, resulting in supply chain inefficiencies. In regions such as Southeast Asia, over 1.2 million tons of potential raw material remains underutilized annually. High initial investment costs, exceeding USD 2.5 million per processing facility, also restrict expansion among small and medium enterprises. Additionally, inconsistent raw material quality leads to production variability of up to 18%, impacting product performance. These limitations pose significant barriers to Asia Pacific agrifiber products' market growth.

Asia Pacific Agrifiber Products Market Opportunities

Expansion of Biodegradable Packaging Sector

The rapid expansion of biodegradable packaging presents a major opportunity, with the Asia Pacific region generating over 1.8 million tons of sustainable packaging demand annually. The packaging sector is expected to increase agrifiber usage by 24% between 2026 and 2030, driven by regulatory bans on plastic. Countries such as India and Singapore have implemented policies targeting a 60% reduction in plastic usage, boosting agrifiber adoption. Technological advancements enabling moisture resistance improvements by 20% further enhance application scope. Investments in packaging innovation have increased by 32%, supporting expansion and reinforcing Asia Pacific Agrifiber Products Market Growth.

Challenges in Asia Pacific Agrifiber Products Market

High Production Costs and Competition from Alternatives

The Asia Pacific Agrifiber Products Market faces challenges related to high production costs, with processing expenses accounting for 38% of total manufacturing costs. Competition from low-cost synthetic materials continues to impact adoption, especially in price-sensitive markets such as India and Southeast Asia. Additionally, transportation costs for raw materials have increased by 14% due to logistical inefficiencies, affecting overall profitability. Limited awareness among end-users, with only 46% recognizing agrifiber benefits, further restricts growth. These factors collectively present ongoing challenges to Asia Pacific Agrifiber Products Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.34 Billion |

| Market Size in 2026 | USD 5.82 Billion |

| Market Size in 2034 | USD 11.47 Billion |

| CAGR | 8.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Agrifiber Products Market Segmentation

The Asia Pacific Agrifiber Products Market is segmented by type and application, with boards dominating at 41% share, followed by panels at 34% and molded products at 25%. Application-wise, construction leads with 52%, followed by packaging at 28% and automotive at 20%.

By Type

Boards account for approximately 41% of total production, with over 1.7 million tons manufactured annually. These products offer high compressive strength of up to 28 MPa and are widely used in structural applications. Panels contribute 34% share, with production exceeding 1.4 million tons, featuring improved moisture resistance and thermal insulation properties. Molded products represent 25% share, with over 1 million tons produced, offering flexibility and lightweight characteristics. Advanced processing techniques have increased durability by 19% across all product types.

By Application

Construction dominates the Asia Pacific Agrifiber Products market with a 52% share, consuming over 2.3 million tons annually. Agrifiber materials are used in flooring, roofing, and insulation, offering improved energy efficiency by 21%. Packaging accounts for a 28% share, with over 1.2 million tons used in biodegradable solutions, achieving a 35% reduction in plastic usage. Automotive applications represent 20% share, utilizing over 0.9 million tons for interior components, reducing vehicle weight by 12% and improving fuel efficiency.

Asia Pacific Agrifiber Products Market Segmentations

Type

- Boards

- Panels

- Molded Products

Application

- Construction

- Packaging

- Automotive

Asia Pacific Agrifiber Products Market Regional Outlook

China leads the Asia-Pacific Agrifiber Products Market with over a 38% share, producing more than 1.6 million tons annually. The country’s construction sector accounts for 55% of consumption, while packaging contributes 27%. Government policies promoting sustainable materials have increased adoption rates by 18%.

South Korea holds 9% share, with production exceeding 0.4 million tons. Automotive applications dominate with 34% usage, driven by innovation in lightweight materials. Japan contributes 22%, India 15%, and Australia 6%, with Southeast Asia collectively accounting for 10%.

India produces over 0.7 million tons annually, driven by agricultural residue availability. Singapore and Taiwan contribute smaller shares but show high growth potential with adoption rates increasing by 20% annually.

Top players in Asia Pacific Agrifiber Products

- UPM-Kymmene

- Weyerhaeuser

- Green Fiber International

- Norbord Inc.

- Trex Company

- Stora Enso

- Universal Forest Products

- Arauco

- Masisa

- Finsa

- Egger Group

- Kronospan

- Sonae Arauco

-

UPM-Kymmene

-

Holds approximately 12% regional share with strong presence in Japan and China

-

Invests over 18% of revenue in R&D and sustainability initiatives

-

Operates 25+ production facilities with output exceeding 0.5 million tons annually

-

-

Stora Enso

-

Accounts for nearly 10% market share with strong packaging segment dominance

-

Achieves 22% higher efficiency through advanced bio-composite technology

-

Expanding production capacity by 15% annually across Asia Pacific

-

Investment Analysis

Investment in the Asia-Pacific agrifiber products market has increased by 29% in 2025, with over USD 1.8 billion allocated across manufacturing and R&D. Construction applications receive 45% of total investment, followed by packaging at 32% and automotive at 23%. China and Japan account for 58% of total investments, with Southeast Asia showing 17% growth in capital inflow.

M&A activities have increased by 21%, with over 15 strategic partnerships formed in 2025. Collaborative ventures focus on expanding production capacity and developing high-performance materials. Investments in automation and AI integration have improved efficiency by 19%, reinforcing long-term Asia Pacific Agrifiber Products market growth.

New Product Developments

New product launches account for 26% of total market offerings, with innovations focusing on moisture resistance and durability improvements of up to 23%. Companies are introducing hybrid agrifiber composites with enhanced tensile strength by 18%. R&D spending has increased by 14%, supporting innovation and expanding application scope.

Recent Developments in Asia Pacific Agrifiber Products

- 2025: Production capacity increased by 17% in China with new facilities producing 0.3 million tons annually

- 2025: Southeast Asia increased biodegradable packaging production by 22%

Research Methodology

The research methodology for the Asia-Pacific Agrifiber Products market involves a combination of primary and secondary research techniques. Primary research includes interviews with over 120 industry experts, manufacturers, and suppliers, ensuring data accuracy and reliability. Secondary research involves analysis of company reports, industry publications, and government databases, covering over 300 verified sources. Market size estimation is conducted using bottom-up and top-down approaches, incorporating production volumes exceeding 4 million tons and regional demand metrics. Data triangulation and validation processes ensure consistency, with statistical models achieving 95% confidence levels. This structured approach provides comprehensive insights into market dynamics, segmentation, and the competitive landscape.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Precision Agriculture and AgriTech Platforms

Henry Smith is a market research analyst with 7–9 years of experience specializing in agriculture markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.