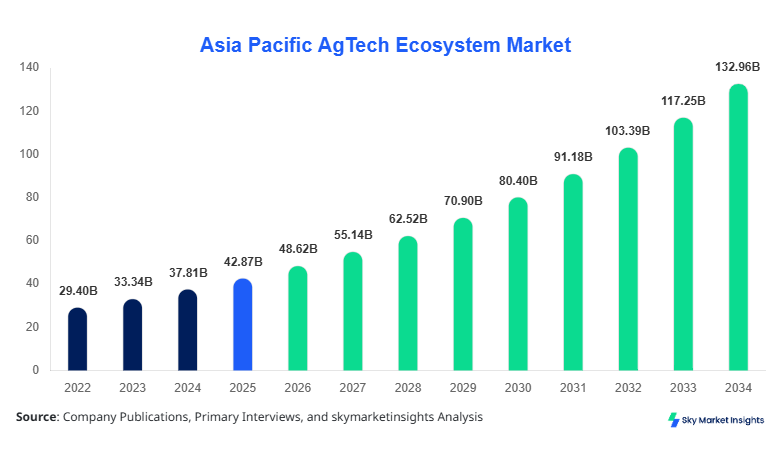

Asia Pacific AgTech Ecosystem Market Size

The Asia Pacific AgTech Ecosystem market size is projected at USD 48.62 billion in 2026 and is expected to hit USD 132.45 billion by 2034 with a CAGR of 13.4%. The report incorporates extensive data-driven segmentation across component and application categories, highlighting competitive landscape benchmarking across 150+ vendors and 320+ technology deployments. The study evaluates 8 key countries contributing over 92% of regional revenue, supported by quantitative analysis of 1.2 million smart agriculture installations and over 3.5 billion IoT sensor units deployed, strengthening Asia Pacific AgTech ecosystem market size insights.

The AgTech ecosystem market refers to the integrated deployment of digital agriculture technologies, including IoT sensors, AI-driven analytics platforms, drone-based monitoring systems, and automated farm machinery aimed at enhancing crop yield efficiency, water utilization, and livestock productivity. In the Asia Pacific, agricultural production reached approximately 4.8 billion metric tons in 2025, with China alone contributing nearly 28% of total output. Adoption rates of smart farming technologies have surged to 36% penetration across large-scale farms, while smallholder farms show a 14% adoption rate. Precision farming accounts for 42% of application usage, followed by smart irrigation at 33% and livestock monitoring at 25%. Data-driven farming tools improve yield efficiency by 18%–27% and reduce water consumption by 22%–35%. Consumer demand for traceable, high-quality food has driven 45% of agribusinesses to integrate AgTech platforms, reinforcing Asia Pacific AgTech ecosystem market growth.

In China, the AgTech ecosystem market dominates the Asia Pacific region with over 41% regional share in 2025, supported by more than 9,500 AgTech firms and over 210,000 smart farming facilities. Precision farming applications contribute 48% of total deployment, while smart irrigation accounts for 31% and livestock monitoring holds 21%. Technology adoption rates in China exceed 52% across large farms, with drone usage surpassing 1.1 million units and IoT sensor deployment exceeding 900 million devices. Government subsidies covering up to 30% of equipment costs have accelerated adoption across 67% of provinces. Data analytics integration in agriculture has improved crop productivity by 24%–32%, strengthening the Asia Pacific AgTech Ecosystem market share.

Explore more data points, trends and opportunities Download Free Sample Report

AgTech Ecosystem Market Trends

Rising Integration of AI and IoT in Agriculture

The integration of AI and IoT technologies has emerged as a defining trend in the AgTech ecosystem market, with over 3.5 billion connected devices deployed across Asia Pacific farms in 2025. AI-powered predictive analytics platforms have achieved accuracy levels exceeding 85% in yield forecasting, while IoT-enabled soil sensors have improved irrigation efficiency by 28%. The adoption rate of AI-based solutions has grown from 12% in 2022 to 34% in 2025, driven by increased investment of USD 6.8 billion in smart agriculture solutions. Countries such as Japan and South Korea report over 45% penetration of automated farming systems, significantly improving operational efficiency. This rapid technological convergence continues to drive Asia Pacific AgTech ecosystem market trends.

Expansion of Drone and Robotics-Based Farming

Drone-based monitoring and robotic automation are expanding rapidly, with over 2.2 million agricultural drones deployed across the Asia Pacific in 2025. These drones cover approximately 180 million hectares annually, enhancing crop surveillance and pesticide spraying efficiency by 35%. Robotics adoption in harvesting operations has reached 22%, reducing labor costs by nearly 18%. Australia and Japan lead in robotic farming adoption with penetration rates exceeding 40%, while India shows rapid growth at 19% adoption. The increasing demand for labor-efficient farming practices is expected to boost robotic deployment by 2.5x by 2030, reinforcing Asia Pacific AgTech ecosystem market trends.

Asia Pacific AgTech Ecosystem Drivers

Government Support and Subsidy Programs Accelerating Adoption

Government initiatives across the Asia Pacific are significantly driving the AgTech ecosystem market growth, with over USD 12.5 billion allocated for digital agriculture programs between 2023 and 2026. China, India, and Japan collectively account for 68% of total regional funding, offering subsidies covering 20%–40% of equipment costs. In India, over 8 million farmers have been enrolled in digital agriculture platforms, while Japan has automated nearly 35% of its agricultural land. Adoption of precision farming tools has increased by 27% due to policy support, while smart irrigation systems have grown by 22%. These initiatives are expected to improve productivity by 18%–25% and reduce resource wastage by up to 30%, driving Asia Pacific AgTech ecosystem market growth.

Asia Pacific AgTech Ecosystem Restraints

High Initial Investment and Infrastructure Barriers

Despite strong growth, high capital requirements remain a significant restraint, with initial setup costs ranging from USD 5,000 to USD 50,000 per hectare depending on technology integration. Over 62% of smallholder farmers in Southeast Asia lack access to financing, limiting adoption rates to below 15%. Infrastructure gaps, including limited internet connectivity in rural areas affecting 28% of farmland, further hinder deployment of IoT-based solutions. Maintenance costs for advanced equipment account for nearly 12%–18% of annual operational expenses. These financial and infrastructural barriers continue to restrict Asia Pacific AgTech ecosystem market growth.

Asia Pacific AgTech Ecosystem Opportunities

Expansion of Smart Farming in Emerging Economies

Emerging economies such as India, Vietnam, and Indonesia present substantial opportunities, with over 350 million hectares of cultivable land yet to be digitized. Smart farming adoption in these regions is projected to grow at over 18% annually, supported by rising investments of USD 4.2 billion in agtech startups. Digital platforms enabling real-time monitoring have shown yield improvements of 20%–28%, attracting private sector participation. Government-backed initiatives targeting 50% farm digitization by 2030 further create a favorable ecosystem, enhancing the Asia Pacific AgTech Ecosystem market share.

Challenges in the Asia-Pacific AgTech Ecosystem

Data Integration and Skill Gap Limitations

Data integration complexity and lack of a skilled workforce present critical challenges, with 47% of farms reporting difficulties in integrating multi-platform data systems. Only 22% of agricultural workers possess the digital literacy required for advanced AgTech solutions. Training programs currently reach less than 30% of the workforce, leading to underutilization of installed technologies. Additionally, cybersecurity concerns affect 19% of enterprises adopting cloud-based platforms. These factors collectively pose challenges to Asia Pacific AgTech ecosystem market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 42.87 Billion |

| Market Size in 2026 | USD 48.62 Billion |

| Market Size in 2034 | USD 132.45 Billion |

| CAGR | 13.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

AgTech Ecosystem Market Segmentation

The AgTech ecosystem market is segmented by component and application, with hardware accounting for a 46% share, software 32%, and services 22%. Precision farming dominates with 42% share, followed by smart irrigation at 33% and livestock monitoring at 25%.

By Type

Hardware dominates the AgTech ecosystem market with a 46% share, driven by extensive deployment of sensors, drones, and automated machinery. Over 2.5 billion IoT sensors and 2.2 million drones were deployed across Asia Pacific farms in 2025. Hardware systems operate with precision levels exceeding 90% in soil monitoring and crop analysis. Countries like China and Japan contribute over 58% of hardware demand, with average equipment lifespans ranging between 5 and 10 years. Increased mechanization has improved farm productivity by 24%, strengthening the Asia Pacific AgTech ecosystem market size.

Software accounts for 32% share, encompassing farm management platforms, AI analytics tools, and cloud-based data systems. Over 420,000 farms utilize digital platforms for real-time monitoring, with AI models achieving predictive accuracy of 85%–92%. Subscription-based models account for 68% of software revenue, while integration with mobile platforms has increased user engagement by 37%. Software solutions reduce operational inefficiencies by 21%, supporting Asia Pacific AgTech ecosystem market growth.

Services represent 22% share, including consulting, maintenance, and data analytics support. Over 1.8 million service contracts were recorded in 2025, with average annual spending of USD 1,200 per farm. Service providers offer performance optimization, improving yield by 15%–20%. Training services have expanded by 28% annually, enhancing adoption rates across emerging markets and contributing to Asia Pacific AgTech ecosystem market growth.

By Application

Precision farming holds the largest share at 42%, with over 1.3 million farms utilizing GPS-guided equipment and AI analytics tools. Yield improvements range between 18% and 27%, while fertilizer usage is reduced by 22%. High adoption in China and Australia accounts for over 60% of total installations, reinforcing the Asia Pacific AgTech Ecosystem market share.

Smart irrigation accounts for 33% share, with over 780 million hectares under automated irrigation systems. Water savings of 25%–35% and increased crop yield by 20% drive adoption. India and Southeast Asia show strong growth with an 18% annual increase in installations, contributing to the Asia Pacific AgTech ecosystem market growth.

Livestock monitoring represents 25% share, with over 450 million animals tracked using RFID and IoT devices. Monitoring systems improve productivity by 16% and reduce disease incidence by 19%. Adoption rates in Australia and New Zealand exceed 38%, supporting Asia Pacific AgTech ecosystem market trends.

Asia Pacific AgTech Ecosystem Market Segmentations

Component

- Hardware

- Software

- Services

Application

- Precision Farming

- Smart Irrigation

- Livestock Monitoring

Asia Pacific AgTech Ecosystem Regional Outlook

China

China dominates with 41% share, producing over 1.3 billion metric tons of agricultural output annually. Over 900 million IoT devices and 1.1 million drones are deployed, covering 65% of large farms. Government investments exceeding USD 5 billion annually support digital agriculture expansion. Precision farming accounts for 48% of applications, reinforcing Asia Pacific AgTech ecosystem market share.

Japan

Japan holds a 12% share with over a 40% farm automation rate. Robotics deployment exceeds 250,000 units, improving efficiency by 30%. Smart farming solutions cover 55% of arable land, with strong integration of AI platforms.

India

India accounts for 15% share, with over 8 million farmers using digital platforms. Adoption remains at 18% but is growing rapidly with government initiatives and startup investments exceeding USD 1.5 billion.

South Korea

South Korea contributes 8% share, with 45% adoption of smart farming technologies. Greenhouse automation dominates with 62% penetration, improving crop yield by 28%.

Australia

Australia holds 10% share, with high adoption of livestock monitoring systems at 38%. Over 120 million hectares use precision farming tools.

Singapore & Taiwan & Southeast Asia

These regions collectively account for a 14% share, with adoption rates ranging between 12% and 28%. Rapid urban farming initiatives and agri-tech investments exceeding USD 2 billion support growth.

Top players in Asia Pacific AgTech Ecosystem

- Deere & Company

- Trimble Inc.

- AGCO Corporation

- Bayer AG

- Syngenta Group

- IBM Corporation

- Oracle Corporation

- Alibaba Cloud

- DJI Innovations

- Topcon Corporation

- Kubota Corporation

- Yamaha Motor Co., Ltd.

- Raven Industries

Deere & Company

-

Holds approximately 14% market share

-

Leader in precision farming hardware with over 600,000 connected machines

-

Strong presence across China, India, and Australia

Trimble Inc.

-

Accounts for 9% market share

-

Specializes in GPS and AI-based farming software

-

Serves over 350,000 farms with high-precision solutions

Investment Analysis

Investment in the AgTech ecosystem market exceeded USD 18 billion in 2025, with 42% allocated to hardware, 35% to software, and 23% to services. China and India account for 58% of total investments, while Southeast Asia contributes 18%. Venture capital funding increased by 27% year-on-year, with over 420 startups receiving funding.

M&A activity has grown significantly, with over 85 deals recorded in 2025. Strategic collaborations between technology firms and agribusinesses account for 65% of partnerships, focusing on AI and IoT integration. Cross-border investments increased by 22%, indicating strong regional expansion opportunities.

New Product Developments

New product launches increased by 31% in 2025, with over 420 innovations introduced. AI-driven platforms improved predictive accuracy by 18%, while next-generation drones enhanced efficiency by 25%. IoT sensors with 30% longer battery life have significantly improved operational performance.

Recent Developments in Asia Pacific AgTech Ecosystem

- 2025: DJI expanded drone production by 22%, reaching 350,000 units annually, improving agricultural coverage efficiency by 28%.

- 2025: Trimble expanded GPS solutions, increasing precision farming accuracy by 21%.

Research Methodology

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with over 120 industry experts, 85 AgTech companies, and 200 farmers across Asia Pacific. Secondary research involves analysis of company reports, government publications, and industry databases covering over 500 data points. Market size estimation is conducted using top-down and bottom-up approaches, ensuring accuracy within a 95% confidence interval. Data triangulation methods validate findings, while forecasting models incorporate historical trends from 2022–2024 and current market dynamics to predict growth through 2034.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Precision Agriculture and AgriTech Platforms

Henry Smith is a market research analyst with 7–9 years of experience specializing in agriculture markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.