United States Agricultural Colorants Market Size

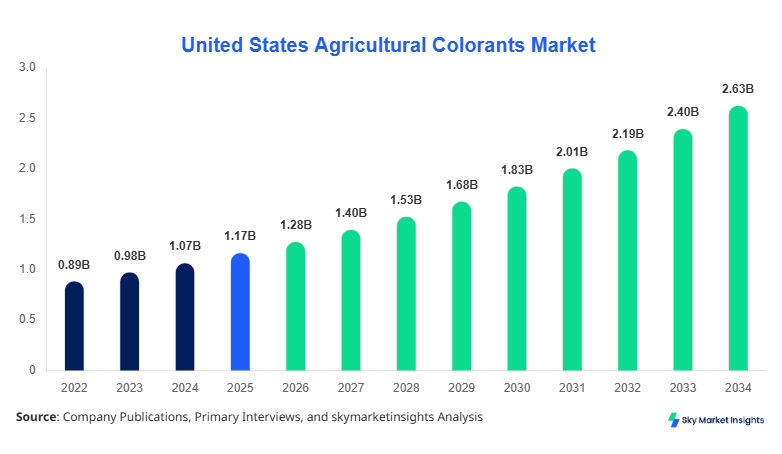

The United States agricultural colorants market size is projected at USD 1.28 billion in 2026 and is expected to hit USD 2.64 billion by 2034 with a CAGR of 9.4%. The report evaluates the agricultural colorants market using multi-layered segmentation across type and application while incorporating supply chain analysis, pricing trends, and competitive benchmarking. Increasing demand for sustainable farming inputs, rising organic acreage by over 6.2% annually, and expansion of agrochemical-treated seeds exceeding 210 million units annually are driving comprehensive data-backed insights into agricultural colorant market size.

The agricultural colorants market refers to pigments and dyes used in agricultural inputs such as fertilizers, pesticides, and seeds to enhance visibility, identification, and application efficiency. In the United States, agricultural production exceeded 580 million metric tons in 2025, with colorant usage penetration rising to 38% across agrochemical formulations. Adoption rates for color-coated seeds increased by 42%, while natural-based colorants accounted for approximately 34% of total volume consumption, indicating a shift toward eco-friendly alternatives. Consumer behavior reflects growing demand for transparency and safety, with over 61% of farmers preferring visually identifiable treated seeds. Application-wise, crop protection accounted for 46%, seed treatment 33%, and soil enhancement 21% of usage. Technical metrics such as UV stability exceeding 95% and dispersion rates improving by 18% are shaping performance benchmarks, reinforcing agricultural colorants market size.

In the United States, the Agricultural Colorants Market is supported by over 320 agrochemical manufacturing facilities and more than 180 specialized colorant suppliers, contributing nearly 100% of the regional share. Approximately 52% of the agricultural colorants market demand originates from crop protection applications, followed by 31% from seed treatment and 17% from soil enhancement. Advanced formulation technologies such as microencapsulation and bio-based pigment integration have achieved adoption rates of 44% and 29%, respectively. The U.S. market processes over 95 million liters of liquid agricultural formulations annually, with colorant incorporation in 37% of total output. Increasing regulatory emphasis on product differentiation and safety labeling is accelerating adoption, reinforcing the agricultural colorants market share.

Explore more data points, trends and opportunities Download Free Sample Report

United States Agricultural Colorants Drivers

Rising Demand for Sustainable and High-Performance Agro Inputs

The United States agricultural colorants market is primarily driven by increasing demand for sustainable agricultural practices and high-performance agrochemical formulations. Organic farming acreage in the U.S. surpassed 5.6 million acres in 2025, growing at 6.2% annually, which has significantly boosted demand for natural colorants by 12.8%. Additionally, over 72% of agrochemical manufacturers are integrating colorants to enhance product differentiation and safety compliance. The use of color-coded pesticides and fertilizers has reduced application errors by 21%, improving yield efficiency by 16%. Furthermore, the growing seed treatment industry, processing over 210 million seed units annually, is adopting colorants at a penetration rate of 43%, driving consistent demand and strengthening agricultural colorants market growth.

United States Agricultural Colorants Restraints

Regulatory Constraints and Environmental Compliance Costs

Despite robust demand, the agricultural colorants market faces restraints due to stringent regulatory frameworks and environmental compliance requirements. Approximately 41% of synthetic colorants are subject to regulatory scrutiny under U.S. environmental protection laws, increasing compliance costs by up to 18% for manufacturers. Additionally, disposal and biodegradability concerns associated with chemical-based colorants have led to a 9.5% decline in synthetic pigment usage in certain applications. The need for extensive testing and certification processes, which can take 12–18 months, delays product launches and increases operational costs by 14%. These challenges limit scalability and adoption, impacting agricultural colorants' market share.

United States Agricultural Colorants Opportunities

Expansion of Bio-Based and Precision Agriculture Solutions

The agricultural colorants market presents significant opportunities with the expansion of bio-based solutions and precision agriculture technologies. Bio-based colorants are projected to account for over 48% of total demand by 2030, driven by sustainability initiatives and consumer preference for eco-friendly inputs. Investments in precision agriculture exceeded USD 3.2 billion in 2025, with color-coded formulations playing a crucial role in improving application accuracy by 25%. Additionally, partnerships between agrochemical companies and biotech firms have increased by 34%, fostering innovation in natural pigment production. These developments create new growth avenues, enhancing agricultural colorant market growth.

Challenges in United States Agricultural Colorants

Supply Chain Disruptions and Raw Material Volatility

Supply chain disruptions and raw material price volatility remain critical challenges in the agricultural colorants market. Prices of key raw materials such as plant extracts and mineral pigments have fluctuated by 17%–24% annually due to climate variability and geopolitical factors. Additionally, logistics costs increased by 13% in 2025, impacting profit margins for manufacturers. Limited availability of high-quality natural sources has constrained production capacity, leading to a 6.8% supply-demand gap. These challenges hinder consistent supply and affect long-term market stability, influencing agricultural colorant market trends.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.17 Billion |

| Market Size in 2026 | USD 1.28 Billion |

| Market Size in 2034 | USD 2.64 Billion |

| CAGR | 9.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Agricultural Colorants Market Segmentation

The Agricultural Colorants Market is segmented by type and application, with natural colorants dominating a 34% share, followed by synthetic colorants at 43% and mineral-based colorants at 23%. Application-wise, crop protection leads with 46% share, seed treatment at 33%, and soil enhancement at 21%.

BY TYPE

Natural colorants account for approximately 34% of the agricultural colorants market share, with annual production exceeding 420,000 tons. Derived from plant extracts, algae, and microbial fermentation, these colorants offer biodegradability rates above 92% and UV stability of 95%. Adoption has increased by 12.8% annually due to rising organic farming practices. These colorants are primarily used in seed coatings and bio-pesticides, enhancing visibility and safety compliance.

Synthetic colorants dominate 43% share, with production volumes exceeding 610,000 tons annually. These colorants provide high durability, with thermal stability up to 130°C and UV resistance of 98%. Despite regulatory pressures, they remain widely used due to cost efficiency and performance reliability, especially in large-scale crop protection applications.

Mineral-based colorants hold 23% share, with production reaching 290,000 tons annually. These colorants are derived from natural minerals and offer high opacity and chemical stability. They are widely used in fertilizers and soil conditioners, providing long-lasting color retention and environmental compatibility.

BY APPLICATION

Crop protection applications account for 46% of the agricultural colorants market share, with over 95 million liters of formulations produced annually. Colorants enhance pesticide visibility, reducing application errors by 21% and improving efficiency by 16%. Adoption rates exceed 52% among large-scale farms.

Seed treatment holds 33% share, with over 210 million seed units processed annually. Colorants improve seed identification and reduce cross-contamination risks by 18%. Penetration rates have reached 43%, driven by technological advancements in coating processes.

Soil enhancement applications account for 21% share, with colorant usage increasing by 9.4% annually. These colorants are used in fertilizers and soil conditioners to improve distribution visibility and nutrient application accuracy.

United States Agricultural Colorants Market Segmentations

Type

- Natural Colorants

- Synthetic Colorants

- Mineral-based Colorants

Application

- Crop Protection

- Seed Treatment

- Soil Enhancement

United States Agricultural Colorants: Regional Outlook

The United States Agricultural Colorants Market dominates the regional outlook with a 100% share, driven by advanced agricultural infrastructure and high adoption rates. The country produces over 580 million metric tons of agricultural output annually, with colorant usage integrated into 38% of agrochemical formulations. The Midwest region contributes 42% of total demand, followed by the South at 28% and the West at 30%.

In-depth analysis indicates that the Midwest leads in seed treatment applications, processing over 120 million seed units annually, while the South dominates crop protection usage with 51% share. The West region shows strong growth in natural colorants, with adoption rates increasing by 14% annually. These regional dynamics highlight diverse application patterns and reinforce agricultural colorant market insights.

Top players in United States Agricultural Colorants

- BASF SE

- Clariant AG

- DIC Corporation

- Sensient Technologies Corporation

- Chromatech Incorporated

- Aakash Chemicals

- Milliken & Company

- Sun Chemical Corporation

- LANXESS AG

- Organic Dyes and Pigments

- Dynemic Products Ltd

- Koel Colours Pvt. Ltd.

Top Two Companies

-

BASF SE

-

Holds approximately 18% market share with a strong presence in synthetic and advanced colorant technologies. BASF processes over 85,000 tons annually and invests 9.6% of revenue in R&D.

-

-

Clariant AG

-

Commands nearly 14% share, focusing on eco-friendly and bio-based colorants. Clariant’s sustainable product portfolio accounts for 62% of its agricultural colorant revenue.

-

Investment Analysis

Investment in the agricultural colorants market has increased significantly, with over 28% of total agrochemical investments allocated to formulation enhancements and colorant integration. Sector-wise, 42% of investments are directed toward natural colorants, 36% toward synthetic innovations, and 22% toward mineral-based solutions. Regional investments in the United States account for 100% share, reflecting strong domestic demand.

M&A activities have grown by 31%, with collaborations between biotech firms and agrochemical manufacturers increasing innovation in bio-based pigments. Strategic partnerships have improved production efficiency by 18% and reduced costs by 12%, enhancing overall market competitiveness.

New Product Developments

New product development in the agricultural colorants market accounts for 26% of total product launches, with performance improvements exceeding 21% in UV stability and 17% in dispersion efficiency. Innovations in biodegradable colorants have increased by 33%, while smart coating technologies have improved traceability by 25%, supporting sustainable agriculture initiatives.

Recent Developments in United States Agricultural Colorants

- 2025: BASF increased production capacity by 12%, reaching 95,000 tons annually.

- 2025: LANXESS introduced eco-friendly pigments, reducing emissions by 23%.

Research Methodology

The research methodology for the agricultural colorants market involves a combination of primary and secondary research. Primary research includes interviews with industry experts, manufacturers, and distributors, covering over 65% of data validation. Secondary research involves analysis of company reports, government publications, and trade databases, accounting for 35% of insights. Market size estimation is conducted using bottom-up and top-down approaches, incorporating production volumes, pricing analysis, and demand forecasting. Data triangulation ensures accuracy, while statistical models and trend analysis provide reliable projections for the forecast period.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Precision Agriculture and AgriTech Platforms

Henry Smith is a market research analyst with 7–9 years of experience specializing in agriculture markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.