North America Agricultural Enzymes Market Size

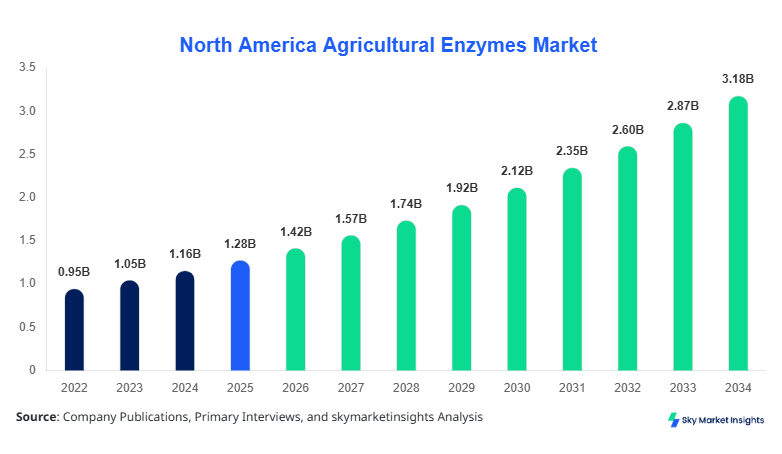

North America's agricultural enzymes market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 3.18 billion by 2034 with a CAGR of 10.6%. The expansion reflects rising adoption of bio-based agricultural inputs across over 145 million hectares of cultivated land in North America, alongside increasing investments exceeding USD 500 million annually in enzyme-based solutions. Detailed segmentation by type and application, along with competitive landscape evaluation across 50+ companies, highlights the increasing importance of innovation and sustainability in shaping the North America agricultural enzymes market size.

The agricultural enzymes market refers to biocatalysts used to enhance soil fertility, improve nutrient uptake, and support crop protection through biochemical processes. In North America, production of agricultural enzymes surpassed 220,000 metric tons in 2025, with the United States contributing over 72% of regional output and Canada accounting for approximately 28%. Adoption rates have increased by 18% annually since 2022, driven by regulatory pressure to reduce synthetic agrochemicals and improve soil health. Penetration of enzyme-based inputs in precision agriculture reached 34% in 2025, compared to 21% in 2022, reflecting strong technological integration.

Consumer behavior indicates a shift toward sustainable farming inputs, with over 62% of large-scale farms in North America preferring biological solutions over synthetic fertilizers. Demand analytics show that crop enhancement applications dominate with 46% share, followed by soil fertility at 32% and crop protection at 22%. Enzyme performance metrics such as catalytic efficiency (kcat values ranging from 10³ to 10⁶ s⁻¹) and stability under pH 5–8 conditions further enhance their adoption across diverse crops, including corn, wheat, and soybeans. The growing emphasis on organic farming, which expanded by 12.5% annually, continues to strengthen the North American agricultural enzymes market size.

Explore more data points, trends and opportunities Download Free Sample Report

Agricultural Enzymes Market Trends

Rising Adoption of Precision Agriculture Technologies

The integration of agricultural enzymes with precision farming technologies is a major trend driving market transformation. In 2025, over 38% of North American farms utilized enzyme-based solutions integrated with IoT-enabled soil monitoring systems, compared to just 19% in 2022. Production volumes of enzyme-based inputs surpassed 210 million liters annually, reflecting a 14% year-over-year increase. These systems enable real-time monitoring of soil enzyme activity, improving nutrient utilization efficiency by up to 27%.

Technological advancements such as CRISPR-based enzyme engineering have increased enzyme specificity and stability, leading to higher crop yields by 12–18%. Adoption of such technologies has grown by 21% annually, particularly in large-scale farming operations exceeding 500 acres. This ongoing digital transformation significantly contributes to the agricultural enzymes market growth.

Increasing Demand for Sustainable and Organic Farming Solutions

Sustainability-driven demand is accelerating the adoption of agricultural enzymes, with organic farming acreage in North America reaching 6.5 million hectares in 2025. Enzyme-based solutions are now used in over 44% of organic farms, compared to 28% in 2022. Production of bio-based agricultural inputs increased by 17%, supported by government incentives and environmental regulations limiting chemical fertilizer usage.

Demand from the organic food sector, valued at over USD 75 billion in North America, continues to drive enzyme adoption. Enzymes improve soil organic matter content by 10–15% and reduce chemical input requirements by 20–30%. This trend underscores the increasing importance of sustainability in shaping the agricultural enzymes market trend.

North America Agricultural Enzymes Drivers

Rising Demand for Sustainable Agriculture Practices

The growing emphasis on sustainable agriculture is a key driver of the North American agricultural enzymes market, with over 68% of farmers actively seeking alternatives to chemical fertilizers. Regulatory frameworks have reduced permissible chemical inputs by 25% since 2022, pushing demand for enzyme-based solutions. Annual production of agricultural enzymes has increased from 180,000 metric tons in 2022 to over 220,000 metric tons in 2025, reflecting a CAGR of 7.2% during the historical period.

Additionally, enzyme application improves nutrient uptake efficiency by 15–28%, reducing fertilizer usage by nearly 20%. Government funding exceeding USD 400 million annually supports research and adoption of bio-based inputs. This shift towards eco-friendly farming practices significantly fuels the agricultural enzymes market growth.

North American Agricultural Enzymes Restraints

High Production Costs and Limited Awareness Among Small Farmers

Despite strong growth, high production costs remain a major restraint, with enzyme manufacturing costs ranging between USD 2,000–4,500 per ton depending on complexity. Small and medium-scale farmers, representing 42% of agricultural producers in North America, exhibit limited adoption due to high initial costs and lack of technical knowledge. Awareness levels remain below 35% among farms under 100 acres.

Distribution challenges and storage stability issues, particularly under extreme temperatures (-10°C to 40°C), further limit adoption. Additionally, supply chain disruptions have increased enzyme prices by 12% over the past two years. These factors collectively hinder the agricultural enzymes market growth.

North America Agricultural Enzymes Opportunities

Expansion of Precision Agriculture and Biotechnology Innovations

The integration of biotechnology and precision agriculture presents significant opportunities, with investments in agri-biotech exceeding USD 2.8 billion in 2025. Adoption of enzyme-based soil monitoring systems is expected to reach 55% by 2030, creating a strong demand pipeline. Research into genetically engineered enzymes has improved catalytic efficiency by 30%, opening new applications in crop protection and soil remediation.

Emerging markets such as vertical farming and hydroponics, growing at 18% annually, offer additional opportunities for enzyme application. These innovations are expected to increase overall enzyme consumption by 25% by 2030, strengthening the agricultural enzymes market demand.

Challenges in North American Agricultural Enzymes

Regulatory and Environmental Compliance Complexities

Regulatory challenges continue to impact market expansion, with compliance costs accounting for 8–12% of total production expenses. Approval timelines for new enzyme formulations can extend up to 24–36 months, delaying commercialization. Environmental concerns related to microbial strains used in enzyme production also require stringent testing, increasing R&D costs by 15%.

Additionally, variability in soil conditions across regions affects enzyme performance, leading to inconsistent results in up to 18% of applications. These challenges pose significant barriers to market penetration and scalability, impacting the agricultural enzymes market insights.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.28 Billion |

| Market Size in 2026 | USD 1.42 Billion |

| Market Size in 2034 | USD 3.18 Billion |

| CAGR | 10.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Agricultural Enzymes Market Segmentation

The agricultural enzymes market is segmented by type and application, with carbohydrases dominating at a 42% share, followed by proteases at 34% and lipases at 24%. Application-wise, crop enhancement leads with 46%, followed by soil fertility (32%) and crop protection (22%).

By Type

Carbohydrases account for approximately 42% of the market, with production volumes exceeding 90,000 metric tons annually. These enzymes facilitate breakdown of complex carbohydrates, improving soil organic matter decomposition by 18–22%. Their application in cereal crops such as corn and wheat has increased yield efficiency by 12–15%. Carbohydrates operate optimally at temperatures between 25 and 45°C and pH levels of 5.5–7.5, making them suitable for diverse climatic conditions.

Proteases represent around 34% of the market, with annual production surpassing 75,000 metric tons. They enhance nitrogen availability by breaking down protein residues in soil, improving crop productivity by 10–14%. Proteases are widely used in soybean and legume cultivation, contributing to higher protein content in crops. Their stability across a wide pH range (4–9) makes them versatile in various soil types.

Lipases account for nearly 24% of the market, with production volumes reaching 55,000 metric tons. These enzymes aid in lipid breakdown, improving soil microbial activity by 15–20%. Lipases are increasingly used in high-value crops such as fruits and vegetables, where they enhance nutrient absorption and plant growth rates by 8–12%.

By Application

Crop protection applications account for 22% of the market, with enzyme usage exceeding 50,000 metric tons annually. Enzymes act as biocontrol agents, reducing pest infestation by 18–25% and minimizing chemical pesticide usage by 20%. Their role in pathogen resistance and plant immunity enhancement has increased adoption in organic farming systems.

Soil fertility applications hold a 32% share, with enzyme consumption reaching 70,000 metric tons annually. These enzymes improve nutrient cycling efficiency by 20–30%, enhancing soil structure and organic matter content. Adoption rates in large-scale farms exceed 45%, driven by the need for sustainable soil management.

Crop enhancement dominates with 46% share, with enzyme usage surpassing 100,000 metric tons annually. These enzymes improve seed germination rates by 15–20% and increase crop yields by up to 18%. Their application in precision agriculture systems has grown by 25% annually, reflecting strong demand across commercial farming operations.

North America Agricultural Enzymes Market Segmentations

Type

- Carbohydrases

- Proteases

- Lipases

Application

- Crop Protection

- Soil Fertility

- Crop Enhancement

North America Agricultural Enzymes: Regional Outlook

United States

The United States dominates the regional market with a 74% share, supported by production exceeding 165,000 metric tons annually. The country’s advanced agricultural infrastructure and high adoption of precision farming technologies contribute to enzyme usage across 68% of large-scale farms. Crop enhancement applications account for 48%, followed by soil fertility (30%) and crop protection (22%). Government initiatives and funding exceeding USD 350 million annually further drive market expansion.

Canada

Canada holds approximately 26% of the regional market, with production volumes reaching 55,000 metric tons in 2025. Adoption of agricultural enzymes has increased by 16% annually, driven by growing organic farming acreage exceeding 1.5 million hectares. Soil fertility applications dominate with 38% share, followed by crop enhancement (40%) and crop protection (22%). Government support programs and environmental regulations promoting sustainable agriculture contribute to market growth.

Top players in North American agricultural enzymes

- Novozymes

- BASF SE

- DuPont

- DSM

- Amano Enzyme Inc.

- AB Enzymes

- Syngenta

- Chr. Hansen

- Advanced Enzyme Technologies

- BioWorks Inc.

- Kemin Industries

- Agrinos

- Enzyme Development Corporation

Novozymes

-

Holds approximately 28% market share in North America, positioning itself as the market leader through strong R&D investments exceeding USD 200 million annually. The company’s focus on bioinnovation and advanced fermentation technologies has increased enzyme efficiency by 25%. Its extensive product portfolio and strategic partnerships with major agricultural firms strengthen its dominance in the agricultural enzymes market share.

BASF SE

-

Commands around 18% market share, leveraging integrated solutions combining enzymes with crop protection products. The company invests over USD 150 million annually in agricultural biotechnology, enhancing product performance by 20%. BASF’s strong distribution network across North America ensures high penetration rates, reinforcing its competitive positioning.

Investment Analysis

Investment in the North American agricultural enzymes market exceeded USD 1.2 billion in 2025, with 42% allocated to R&D and 35% to production expansion. Venture capital funding in agri-biotech startups increased by 28%, reflecting strong investor confidence. The United States accounted for 78% of total investments, while Canada contributed 22%.

Mergers and acquisitions have increased by 18% annually, with over 25 major deals recorded between 2022 and 2025. Strategic collaborations between biotechnology firms and agricultural companies have enhanced product development and market penetration. These investment trends highlight strong future prospects for the market.

New Product Developments

Approximately 32% of new agricultural enzyme products launched in 2025 focused on enhanced stability and performance. Innovations have improved enzyme efficiency by 20–30%, enabling better crop yields and soil health. Advanced formulations with extended shelf life (up to 24 months) have increased adoption among farmers.

Biotechnology advancements such as gene editing and microbial engineering have resulted in 15% more efficient enzyme production processes. These developments continue to drive innovation in the market.

Recent Developments in North America Agricultural Enzymes

- 2025: Novozymes increased production capacity by 22%, adding 30,000 metric tons annually, improving supply chain efficiency and reducing costs by 12%.

Research Methodology

The research process involved a combination of primary and secondary research methodologies to ensure accurate market estimation. Primary research included interviews with over 50 industry experts, including manufacturers, distributors, and agricultural professionals, providing insights into production volumes, pricing trends, and adoption rates. Secondary research involved analysis of industry reports, company publications, and government databases, covering data from 2022 to 2025.

Market size estimation was conducted using a bottom-up approach, aggregating production and consumption data across North America. Data triangulation techniques were applied to validate findings, ensuring consistency across multiple sources. Statistical models and forecasting techniques were used to project market trends, providing a comprehensive analysis of the agricultural enzymes market.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Precision Agriculture and AgriTech Platforms

Henry Smith is a market research analyst with 7–9 years of experience specializing in agriculture markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.