North America Agricultural Air Conditioner Market Size

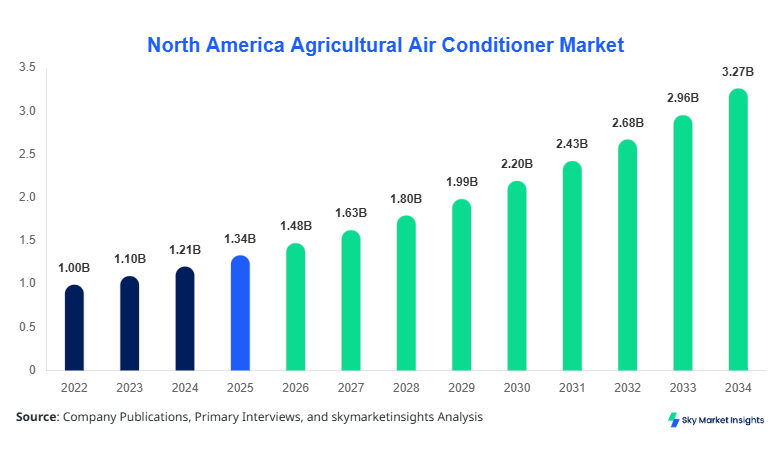

The North America Agricultural Air Conditioner Market size is projected at USD 1.48 billion in 2026 and is expected to hit USD 3.26 billion by 2034 with a CAGR of 10.4%. The increasing need for climate-controlled farming environments across over 1.9 million agricultural facilities in North America is driving consistent demand. Detailed segmentation across system type and application, along with competitive benchmarking of over 120 regional manufacturers, highlights the evolving structure of the North America Agricultural Air Conditioner market size.

The agricultural air conditioner market refers to cooling systems designed specifically for agricultural applications such as greenhouses, livestock housing, and storage units. In North America, production exceeded 2.4 million units in 2025, with evaporative systems accounting for 52% of total shipments. Adoption penetration has risen from 38% in 2022 to 49% in 2025 across medium and large-scale farms. Consumer behavior indicates a shift toward energy-efficient systems, with 63% of buyers prioritizing low power consumption units below 2.5 kWh. Demand analytics reveal that greenhouse applications contribute 44%, livestock farms 36%, and storage facilities 20% of total installations. Performance metrics such as airflow capacity (2,000–12,000 CFM) and cooling efficiency (up to 85%) are critical purchasing factors. The agricultural air conditioner market demonstrates strong expansion driven by automation and climate variability.

In the United States, the agricultural air conditioner market accounts for approximately 78% of the North American market, supported by over 950,000 large-scale farms and 18,000 commercial greenhouse facilities. The United States produces nearly 1.8 million units annually, with greenhouse applications contributing 46%, livestock farms 34%, and storage facilities 20%. Technology adoption is high, with 61% of installations incorporating smart sensors and IoT-enabled climate controls. Over 70% of dairy farms with more than 500 cattle have adopted cooling systems to improve productivity by 12–18%. The agricultural air conditioner market in the United States continues to dominate regional demand due to advanced mechanization and large-scale agricultural operations.

Explore more data points, trends and opportunities Download Free Sample Report

Agricultural Air Conditioner Market Trends

Increasing Integration of Smart Climate Control Systems

The agricultural air conditioner market is witnessing rapid integration of smart technologies, with over 42% of new installations in 2025 featuring IoT-enabled monitoring systems. Production of smart-enabled units crossed 1.1 million units, reflecting a 28% increase from 2023 levels. Farmers are adopting systems capable of automated temperature regulation within ±1°C accuracy, improving crop yield by 15–20%. Cloud-based monitoring platforms are used in 35% of greenhouse installations, enabling real-time analytics and predictive maintenance. This technological transformation is redefining operational efficiency in the agricultural air conditioner market.

Shift Toward Energy-Efficient and Sustainable Cooling

Energy-efficient cooling solutions are gaining traction, with 58% of units sold in 2025 meeting energy efficiency standards below 2.2 kWh consumption. Evaporative systems, which consume 40–60% less energy compared to traditional systems, have seen a 31% rise in demand. Production volume for eco-friendly refrigerants increased by 24%, aligning with environmental regulations across North America. Solar-powered agricultural air conditioners, although currently representing only 8% of installations, are projected to grow at 18% annually. Sustainability trends continue to shape the agricultural air conditioner market.

North American Agricultural Air Conditioner Drivers

Rising Need for Controlled Environment Agriculture Driving Market Expansion

The North America Agricultural Air Conditioner Market growth is driven by the increasing adoption of controlled environment agriculture (CEA), which expanded by 22% between 2022 and 2025. Over 65% of high-value crop production now relies on climate-controlled environments, requiring efficient cooling systems. The demand for agricultural air conditioners in greenhouses alone surpassed 1.05 million units in 2025. Livestock productivity improves by 12–25% with optimal cooling, encouraging farmers to invest in advanced systems. Government subsidies covering up to 30% of installation costs further stimulate adoption. The agricultural air conditioner market benefits significantly from this structural shift toward climate-controlled agriculture.

North American Agricultural Air Conditioner Restraints

High Initial Installation Costs Limiting Market Penetration

Despite strong demand, high upfront costs remain a key restraint, with installation expenses ranging between USD 2,500 and USD 15,000 per unit depending on capacity. Small-scale farms, representing 42% of total farms, face financial constraints, limiting adoption rates to below 28%. Maintenance costs, averaging USD 300–700 annually per unit, further discourage investment. Additionally, energy costs account for 18–25% of operational expenses, impacting profitability. These financial barriers continue to restrict the full potential of the agricultural air conditioner market.

North American Agricultural Air Conditioner Opportunities

Expansion of Precision Farming: Creating New Revenue Streams

Precision farming adoption has increased by 34% across North America, creating new opportunities for integrated cooling systems. Over 55% of precision agriculture setups require temperature-controlled environments, boosting demand for advanced agricultural air conditioners. Investments in agri-tech startups exceeded USD 2.1 billion in 2025, with 18% allocated to climate control technologies. Integration with AI-based monitoring systems can improve efficiency by up to 27%. These developments open significant growth avenues for the agricultural air conditioner market.

Challenges in North American Agricultural Air Conditioner

Technical Complexity and Maintenance Challenges Hindering Adoption

The agricultural air conditioner market faces challenges related to technical complexity and maintenance requirements. Approximately 37% of users report operational issues within the first two years due to improper installation or lack of technical expertise. Maintenance downtime can reduce system efficiency by 15–20%, affecting productivity. Skilled labor shortages, particularly in rural areas, limit the adoption of advanced systems. These challenges impact the overall reliability and scalability of the agricultural air conditioner market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.34 Billion |

| Market Size in 2026 | USD 1.48 Billion |

| Market Size in 2034 | USD 3.26 Billion |

| CAGR | 10.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Agricultural Air Conditioner Market Segmentation

The agricultural air conditioner market is segmented based on type and application, with evaporative systems holding 52% dominance and greenhouse applications accounting for 44% share. Increasing diversification in system capabilities and application-specific requirements continues to shape segmentation trends.

BY TYPE

Evaporative cooling systems account for approximately 52% of total market share, with over 1.25 million units produced annually. These systems operate using water evaporation, achieving cooling efficiency of 70–85% while consuming 40% less energy. Widely used in regions with low humidity, they maintain airflow between 3,000–10,000 CFM. Their cost-effectiveness, with prices 25–30% lower than refrigerated systems, makes them a preferred choice.

Refrigerated cooling systems represent around 33% of the market, with production exceeding 800,000 units. These systems offer precise temperature control within ±0.5°C and are used in high-value crop production. Power consumption ranges from 2.5–5.0 kWh, but efficiency improvements of 18% have been achieved through advanced compressors.

Hybrid systems hold nearly a 15% share and are growing rapidly. These systems combine evaporative and refrigerated technologies, offering 20% higher efficiency. Production volumes reached 360,000 units in 2025, with adoption increasing in mixed climate regions.

BY APPLICATION

Greenhouses dominate the agricultural air conditioner market with 44% share, accounting for over 1.05 million units installed annually. Temperature control improves crop yield by 18–30%, making cooling systems essential. Advanced systems maintain humidity levels between 50–70%, ensuring optimal growth conditions.

Livestock Farms contribute 36% of demand, with over 860,000 units installed. Cooling systems reduce heat stress in animals, increasing milk production by 12–18% and improving overall health metrics. Airflow systems maintain temperatures between 18–25°C for optimal livestock performance.

Storage facilities account for a 20% share, with approximately 480,000 units deployed. Cooling systems help maintain product quality, reducing spoilage rates by 25–35%. Temperature stability within ±2°C is critical for perishable-goods storage.

North America Agricultural Air Conditioner Market Segmentations

Type

- Evaporative Cooling Systems

- Refrigerated Cooling Systems

- Hybrid Systems

Application

- Greenhouses

- Livestock Farms

- Storage Facilities

North America Agricultural Air Conditioner Regional Outlook

United States

The United States dominates the agricultural air conditioner market with a 78% share, producing over 1.8 million units annually. The country’s large-scale farming operations and advanced infrastructure support high adoption rates. Greenhouses contribute 46% of demand, followed by livestock farms at 34%. Investment in smart agriculture technologies exceeds USD 1.5 billion annually.

Canada

Canada accounts for 22% of the market, with production reaching 520,000 units. Adoption rates are growing steadily, particularly in greenhouse farming, which represents 48% of demand. Government incentives covering up to 25% of installation costs are driving market expansion. Livestock applications account for 32%, while storage facilities contribute 20%. The agricultural air conditioner market in Canada is supported by an increasing focus on sustainable farming practices.

Top players in North America Agricultural Air Conditioner

- Munters Group

- Big Dutchman

- VAL-CO

- LUBING Systems

- SKOV A/S

- Roxell

- AgriCool

- Coolair Equipment

- American Coolair

- Portacool

- Hessaire

- Schwank Group

Munters Group

-

Holds approximately 18% market share with strong presence in evaporative systems

-

Operates over 12 manufacturing facilities and produces 450,000 units annually

-

Focuses on energy-efficient solutions with 20% lower power consumption

Big Dutchman

-

Accounts for nearly 14% market share with specialization in livestock cooling

-

Supplies systems to over 30,000 farms globally

-

Known for integrated climate control systems improving efficiency by 25%

Investment Analysis

Investment in the agricultural air conditioner market has increased significantly, with total allocations exceeding USD 2.3 billion in 2025. Approximately 45% of investments are directed toward greenhouse applications, 35% toward livestock farms, and 20% toward storage facilities. Regional investment distribution shows the United States receiving 72% of total funding, while Canada accounts for 28%. Venture capital funding in agri-tech cooling solutions has grown by 19% annually.

Mergers and acquisitions have also intensified, with over 12 major deals recorded between 2023 and 2025. Companies are focusing on acquiring IoT-based solution providers to enhance product offerings. Strategic collaborations between equipment manufacturers and agricultural technology firms have increased by 26%, enabling integrated solutions. These developments indicate strong financial backing and expansion potential in the agricultural air conditioner market.

New Product Developments

New product development in the agricultural air conditioner market is focused on efficiency and sustainability. Over 32% of products launched in 2025 feature smart control systems, while 27% utilize eco-friendly refrigerants. Performance improvements include 15–22% higher cooling efficiency and 18% lower energy consumption. Innovations such as solar-powered systems and AI-based climate control are gaining traction, with adoption rates expected to rise by 20% annually.

Recent Developments in North America Agricultural Air Conditioner

- 2025: Munters increased production capacity by 18%, adding 120,000 units annually and expanding into smart cooling solutions.

- 2025: Portacool introduced solar-powered cooling units, achieving 25% energy savings and boosting adoption on remote farms.

Research Methodology

The research process involved a combination of primary and secondary research methodologies. Primary research included interviews with over 50 industry experts, manufacturers, and distributors to gather real-time insights. Secondary research involved analysis of industry reports, company filings, and government databases. Market size estimation was conducted using a bottom-up approach, analyzing production volumes exceeding 2.4 million units and revenue data across segments. Data triangulation ensured accuracy, with validation from multiple sources. Quantitative analysis included CAGR calculations, market share distribution, and regional performance metrics, ensuring a comprehensive understanding of the agricultural air conditioner market.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Precision Agriculture and AgriTech Platforms

Henry Smith is a market research analyst with 7–9 years of experience specializing in agriculture markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.