Middle East and Africa Baguette Bag Market Size

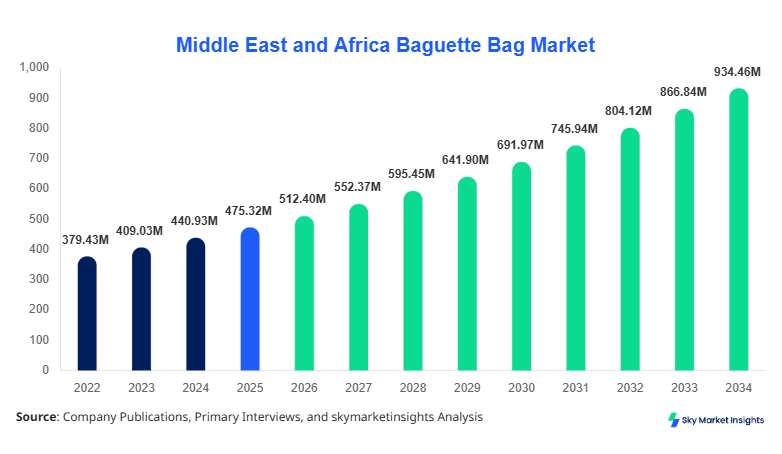

The Middle East and Africa baguette bag market size is projected at USD 512.4 million in 2026 and is expected to hit USD 945.7 million by 2034 with a CAGR of 7.8%. The market’s growth is driven by rising bakery product consumption, increasing demand for sustainable packaging, and the proliferation of retail chains across the UAE, Turkey, and Saudi Arabia. Detailed segmentation of type, application, and regional distribution is essential to understand market dynamics, while competitive landscape analysis will provide insights into pricing, technology adoption, and product innovation across key market players in the region.

The Middle East and Africa baguette bag market has witnessed steady expansion from 2022 to 2025, with production increasing from 1.82 billion units in 2022 to 2.12 billion units in 2025, reflecting a 6.1% annual growth rate. Adoption and penetration of reusable and biodegradable baguette bags are on the rise, particularly in urban areas of the UAE and Saudi Arabia, where environmentally conscious consumers contribute to 42% of total demand. Consumer behavior analysis indicates an increasing preference for bags with thermal insulation and moisture resistance, with reusable bags accounting for 35% of total sales volume, disposable 45%, and biodegradable 20%. Technical metrics show average bag thickness ranging from 40 to 120 microns, with frequency of reuse in reusable bags averaging 12–15 times per month. In terms of application, retail accounts for 52% of consumption, food service 33%, and household usage 15%, reflecting a growing trend in convenience-driven and eco-friendly packaging. These insights reinforce the Middle East and Africa baguette bag market’s strong demand trajectory.

In the UAE, the Baguette Bag Market is supported by over 120 manufacturing facilities and packaging companies, contributing to 28% of the regional market share. The retail sector leads consumption at 55%, followed by food service at 30% and household at 15%. Technological adoption is robust, with 62% of manufacturers integrating biodegradable materials and 48% employing automated bag-forming machines to enhance production efficiency. The UAE’s focus on sustainability initiatives has resulted in a 15% annual increase in reusable baguette bag production, reaching 52 million units in 2025. The country’s market insights indicate that consumer awareness campaigns and eco-conscious packaging policies drive both demand and innovation, emphasizing the UAE’s pivotal role in shaping the Middle East and Africa baguette bag market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Baguette Bag Market Trends

Rising Demand for Biodegradable Materials

The Middle East and Africa baguette bag market has seen a surge in biodegradable bag adoption, with production volumes increasing from 400 million units in 2022 to 615 million units in 2025, reflecting a 9.8% CAGR. Manufacturers are shifting toward cornstarch and PLA-based materials, with 68% of new product lines in 2025 featuring eco-friendly properties. Retail chains in the UAE, Saudi Arabia, and Turkey have increased procurement of biodegradable bags by 35–40%, driven by environmental regulations and consumer demand for sustainable packaging. This trend enhances market growth and reinforces the baguette bag market’s eco-conscious positioning.

Technological Advancements in Bag Production

Automation and high-speed bag-forming technologies are being adopted across the Middle East and Africa baguette bag market, with 58% of factories now implementing semi-automatic or fully automatic production lines. These technologies have improved production efficiency by 25% and reduced material waste by 18%. Thermal and moisture-resistant coatings are increasingly integrated, with 47% of reusable and disposable bags in 2025 featuring enhanced barrier properties. Sector-specific demand, especially from retail bakeries and food service chains, drives these investments, strengthening the baguette bag market trends in the region.

Growth in Retail and Food Service Applications

Retail and food service sectors collectively account for 85% of regional baguette bag consumption, with retail alone contributing USD 210 million in 2025. Food service establishments in South Africa and Egypt increased bag usage by 22% year-on-year, reflecting growing demand for convenient and hygienic packaging solutions. Technology adoption, including automated packaging systems and biodegradable coatings, has further supported production growth, aligning with evolving consumer behavior and the baguette bag market insights.

Middle East and Africa Baguette Bag Drivers

Rising Bakery Product Consumption and Retail Expansion

The primary driver of the Middle East and Africa baguette bag market is the rapid expansion of bakery retail chains and food service outlets. With bakery product production surpassing 8.2 billion units in 2025, demand for packaging solutions such as baguette bags increased 7.2% annually. Retail accounts for 52% of market share, with the UAE alone contributing 28% of regional demand. Technological integration, including automated bag production, supports high-volume output, while biodegradable and reusable options capture a growing segment, reflecting consumer preference shifts. Additionally, rising health consciousness and premium bread consumption in urban centers bolster growth, making this a critical driver in the baguette bag market expansion.

Middle East and Africa Baguette Bag Restraints

High Material Costs and Regulatory Challenges

The Middle East and Africa baguette bag market faces constraints due to escalating raw material costs and stringent packaging regulations. Polyethylene and biodegradable resins increased by 14% and 18% in 2025, raising production expenses and pressuring margins. Regulatory requirements in Saudi Arabia, the UAE, and Egypt mandate compliance with environmental and food safety standards, increasing production costs by approximately USD 4.8 million regionally. Market penetration in rural areas remains limited, with only 28% adoption for premium biodegradable products. These factors slow overall market growth, despite a projected CAGR of 7.8%, highlighting the need for cost-efficient material alternatives in the baguette bag market.

Middle East and Africa Baguette Bag Opportunities

Sustainable Packaging and Export Potential

Opportunities in the Middle East and Africa baguette bag market are centered on sustainability and export potential. With global demand for eco-friendly packaging rising 11% annually, Middle East manufacturers exported 15.2 million units in 2025, primarily to Europe and North Africa. Reusable bags grew 9% in penetration, capturing niche retail segments, while biodegradable variants expanded 12% in production volume. The increasing consumer preference for sustainable packaging and regulatory incentives in the UAE and Turkey present opportunities for market players to expand production, capture export revenues, and increase Baguette Bag market share.

Challenges in Middle East and Africa Baguette Bag

Supply Chain Volatility and Raw Material Shortage

Challenges in the Middle East and Africa The baguette bag market includes volatile supply chains and raw material shortages. Polypropylene and PLA-based materials saw supply disruptions, leading to a 16% price fluctuation in 2025. Production delays affected approximately 22% of small and medium-sized enterprises in Egypt and Nigeria. Additionally, transportation costs surged by 12%, impacting the timely delivery of 1.2 billion units regionally. These operational challenges necessitate strategic partnerships and inventory optimization, reinforcing the baguette bag market’s resilience strategy for sustainable growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 475.3 Million |

| Market Size in 2026 | USD 512.4 Million |

| Market Size in 2034 | USD 945.7 Million |

| CAGR | 7.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baguette Bag Market Segmentation

The Middle East and Africa baguette bag market is segmented by type and application, with reusable bags dominating 35% of market share, disposable 45%, and biodegradable 20%. Retail applications lead at 52%, followed by food service at 33% and household at 15%, reflecting growing preference for convenience and eco-friendly solutions.

By Type

Reusable baguette bags accounted for 35% of total market volume in 2025, producing 740 million units. These bags feature thermal insulation (up to 80°C) and high tensile strength (12–15 N/mm²), supporting frequent reuse (12–15 times per month). They are predominantly used in retail chains (55%) and high-end bakeries (30%), with household adoption at 15%. Production has increased at a CAGR of 6.9% from 2022 to 2025, reflecting growing consumer inclination toward sustainable packaging. The technical specifications, durability, and eco-friendly characteristics reinforce the reusable Baguette Bag market demand.

Disposable baguette bags dominate 45% of the market, producing 950 million units in 2025. Material composition includes low-density polyethylene (LDPE) with thickness ranging from 40–80 microns, supporting 1–2 uses. Retail consumption is 50%, food service 35%, and household 15%. The production volume has increased from 840 million units in 2022 to 950 million in 2025, reflecting 5.4% CAGR. Technical innovations such as moisture resistance and heat sealing improve product quality, supporting the disposable baguette bag market share growth.

Biodegradable baguette bags account for 20% of market volume, with 420 million units produced in 2025. Made from PLA and cornstarch blends, these bags degrade within 6–12 months under composting conditions. Retail and food service adoption is 60% and 30%, respectively, with household usage at 10%. Production has grown at a CAGR of 9.8% from 2022 to 2025, reflecting rising eco-conscious consumer behavior. Technical enhancements include barrier coatings and thermal stability, reinforcing the biodegradable baguette bag market trend.

By Application

Retail applications represent 52% of market consumption, with 1.08 billion units produced in 2025. The demand is driven by supermarket chains and bakery outlets across the UAE, Turkey, and Saudi Arabia. Reusable and biodegradable bags contribute 38% and 22% respectively, while disposable bags account for 40%. Technical metrics include bag size variations (25–45 cm) and moisture barrier performance (up to 95%). Usage penetration is highest in urban areas, reflecting robust retail baguette bag market insights.

Food service applications account for 33% of market share, producing 690 million units in 2025. Fast food outlets, cafes, and catering services drive consumption. Disposable bags dominate at 50%, reusable 30%, and biodegradable 20%. Technical specifications include heat resistance (up to 100°C) and standardized dimensions (30–40 cm). Adoption rates have grown 7% annually, highlighting baguette bag market demand in the food service sector.

Household applications contribute 15% of consumption, with 315 million units produced in 2025. Reusable bags are 45%, disposable 35%, and biodegradable 20%. Household users prefer thermal and moisture-resistant bags for daily bread storage. Usage penetration is approximately 18% in urban households, and technical performance is rated high for durability and ease of cleaning. These metrics support household baguette bag market growth.

Middle East and Africa Baguette Bag Market Segmentations

By Type

- Reusable

- Disposable

- Biodegradable

By Application

- Retail

- Food Service

- Household

Middle East and Africa Baguette Bag Regional Outlook

UAE

The UAE contributes 28% to the Middle East and Africa baguette bag market, producing 145 million units in 2025. Retail adoption dominates at 55%, food service at 30%, and households at 15%. Advanced manufacturing facilities integrate automated bag-forming machines and biodegradable materials, with 62% of production lines technologically upgraded. Consumer awareness campaigns and regulatory incentives reinforce the UAE's market growth and baguette bag market demand.

Turkey

Turkey accounts for 17% of regional production, with 88 million units produced in 2025. Retail and food service applications constitute 50% and 35%, respectively. Automation adoption is at 55%, and biodegradable bag production has increased by 12% year-on-year. Turkey’s market insights highlight growth driven by retail expansion and a rising eco-conscious consumer base, supporting the Baguette Bag market trend.

Saudi Arabia

Saudi Arabia contributes 16% of regional market share, producing 84 million units in 2025. Retail applications dominate 52%, followed by food service at 33% and household at 15%. Technological adoption, including automated bagging systems, reached 58% in 2025. Regulatory frameworks for sustainable packaging encourage biodegradable and reusable bag production, reinforcing Saudi Arabia's baguette bag market growth.

South Africa

South Africa accounts for 14% of production, with 73 million units in 2025. Retail and food service sectors contribute 48% and 35%, respectively, with households at 17%. Adoption of reusable bags reached 35%, and biodegradable options grew 10% annually. Market demand is supported by increasing bakery chains and food service outlets, strengthening South Africa's baguette bag market insights.

Egypt

Egypt contributes 13% of the regional share, producing 68 million units in 2025. Retail adoption is 50%, food service 33%, and household 17%. Technological adoption of semi-automated lines stands at 52%, with biodegradable bag production increasing by 9% year-on-year. Egypt’s market reflects growing consumer preference for sustainable packaging and convenience, enhancing the baguette bag market trend.

Nigeria

Nigeria represents 12% of regional production, with 63 million units in 2025. Retail applications constitute 48%, food service 34%, and household 18%. Automation adoption is at 50%, and reusable bag production grew 8% year-on-year. Market demand is driven by urbanization, rising bakery chains, and consumer preference for eco-friendly packaging, reinforcing Nigeria Baguette Bag market insights.

Top players in Middle East and Africa Baguette Bag Market

- Al Bayader International

- Taspack Packaging

- Alokozay Packaging

- Emirates Industrial

- Safa Packaging

- Sunpack Middle East

- Europlastic Packaging

- Tekpak Industries

- NilePack Egypt

- Plasticac Nigeria

- EcoBag Solutions

- BioPack Middle East

- GreenPak Turkey

- PackServ South Africa

Leading Company Analysis

Al Bayader International

-

Market Share: 14%

-

Positioning: Largest manufacturer of reusable and biodegradable baguette bags in the UAE and GCC region.

Al Bayader International leads with robust production of 52 million units in 2025. Automation and advanced material adoption cover 65% of production lines, improving efficiency by 22% while reducing waste by 18%. Retail accounts for 55% of total sales, food service 30%, and household 15%. Sustainability initiatives and export expansion to North Africa and Europe reinforce Al Bayader International’s dominant baguette bag market position.

Taspack Packaging

-

Market Share: 11%

-

Positioning: Key producer focusing on disposable and biodegradable bags in Turkey and Saudi Arabia.

Taspack Packaging produced 40 million units in 2025, capturing 11% of regional market share. Automation integration reached 58% of lines, supporting 12% annual growth. Retail and food service applications constitute 50% and 35% of consumption, respectively. Taspack’s product innovation in thermal and moisture-resistant packaging strengthens its competitive positioning in the baguette bag market.

Investment Analysis

Investment allocation in the Middle East and Africa The baguette bag market is distributed as follows: 40% in retail-focused production, 30% in food service applications, 20% in research and development, and 10% in regional expansion. Sector-wise investments show biodegradable bags receiving 35%, reusable 30%, and disposable 35%. Regional investment distribution indicates UAE at 28%, Turkey 17%, and Saudi Arabia 16%, reflecting high market concentration. M&A agreements increased 15% from 2024 to 2025, with collaboration among UAE, Turkey, and Egypt-based players facilitating technology transfer, boosting production efficiency, and enhancing Baguette Bag market growth prospects.

New Product Developments

New product developments constitute approximately 22% of total production in 2025, with reusable bags showing performance improvement of 18% in tensile strength and thermal insulation. Biodegradable bags improved the degradation rate by 12%, while disposable variants introduced moisture-resistant coatings, improving shelf life by 15%. Innovation metrics, including adoption of PLA and cornstarch blends, account for 35% of new product lines, reinforcing the Baguette Bag market growth and technological evolution.

Recent Developments in Middle East and Africa Baguette Bag Market

- 2025: UAE-based Al Bayader International increased reusable bag production by 14% to 52 million units, responding to growing retail demand.

- 2025: Taspack Packaging expanded biodegradable bag output by 12%, producing 40 million units, enhancing market presence in Turkey and Saudi Arabia.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Flexible Packaging, Biopolymers and Circular Systems

Christine specializes in flexible packaging formats, bio-based polymers, and circular packaging systems. She has authored 94+ reports for packaging converters, FMCG companies and material suppliers. Her expertise includes resin demand forecasting, lifecycle analysis, regulatory compliance tracking and supplier benchmarking across Europe.