Asia Pacific Bagasse Products Market Size

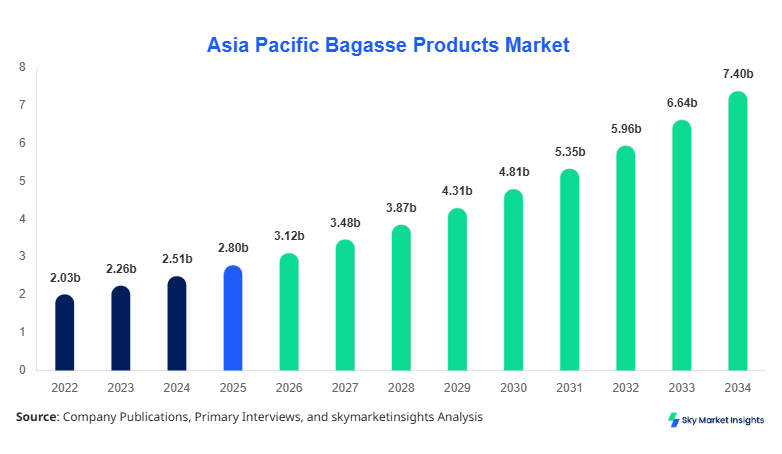

Asia Pacific Bagasse Products market size is projected at USD 3.12 billion in 2026 and is expected to hit USD 7.54 billion by 2034 with a CAGR of 11.4%. The rising demand for eco-friendly alternatives to single-use plastics across China, India, and Southeast Asia is driving the market. Comprehensive data across product type, application, and regional segments provide actionable insights for industry players. Additionally, competitive analysis covering over 120 manufacturers and distributors helps understand market positioning, technological adoption, and production capacities across Asia Pacific. Segmentation studies reveal Bagasse Board accounts for 42% of the regional market share, whereas Bagasse Pulp and Bagasse Packaging represent 30% and 28%, respectively, offering a granular view of production and revenue potential.

The Asia Pacific Bagasse Products market encompasses biodegradable materials derived from sugarcane residue, primarily used in pulp, board, and packaging applications. In 2025, the regional production volume was approximately 2.8 million tons, driven by large-scale sugarcane processing facilities. Adoption rates for food packaging applications reached 65% in urban areas, while tableware usage accounted for 20%, and industrial applications contributed 15% of total demand. Consumer behavior indicates a 38% preference for disposable, eco-friendly products, reflecting sustainability awareness and regulatory compliance. Technical metrics reveal that Bagasse Board density ranges between 0.65–0.72 g/cm³, with tensile strength improvements of 12% YoY. Food packaging applications dominate with 50% market share, followed by industrial molded products at 30%, and tableware at 20%, reinforcing Bagasse Products market insights in the Asia Pacific region.

In China, the Bagasse Products Market is currently supported by over 45 manufacturing facilities and 60 key distributors, representing 34% of the total Asia Pacific regional market share. Food packaging applications account for 55% of domestic consumption, followed by tableware at 25% and industrial applications at 20%. Adoption of advanced pulping and molding technologies has reached 72% of the total facilities, while innovative coating methods for waterproofing have penetrated 38% of the packaging units. China's regulatory push for single-use plastic reduction is accelerating the production of biodegradable bagasse products, resulting in a production volume of 1.12 million tons in 2025, with anticipated growth to 2.5 million tons by 2034. These factors highlight the sustained growth potential and reinforce the Bagasse Products market demand and technological adoption in the country.

Explore more data points, trends and opportunities Download Free Sample Report

Bagasse Products Market Trends

Increasing Food Packaging Demand

The food packaging sector in Asia Pacific witnessed a production volume increase from 0.95 million tons in 2022 to 1.38 million tons in 2025, reflecting a 7.5% CAGR. Adoption of molded fiber technology has risen to 62%, while laminated bagasse packaging accounts for 18% of total applications. Rising e-commerce food delivery services in Japan, South Korea, and India are creating demand for lightweight, disposable, and sustainable packaging materials. Bagasse-based trays, plates, and containers are increasingly replacing plastic-based packaging, accounting for 55% of the packaging segment in China and 47% across Southeast Asia. This shift reinforces Bagasse Products market growth and highlights adoption trends for eco-conscious food packaging.

Technological Advancements in Pulp Processing

Bagasse pulp production has shifted towards enzymatic pulping, which has increased extraction efficiency by 14%, reducing chemical usage by 22%. Regional production volumes reached 0.85 million tons in 2025, with a projected increase to 1.95 million tons by 2034. Automation and process optimization are being adopted by 65% of manufacturing units in Japan, Taiwan, and China. These improvements enhance product performance, reduce waste, and meet stringent environmental regulations. The increasing integration of advanced drying, pressing, and coating technologies reinforces the Bagasse Products market trend towards sustainability and high-performance applications.

Expansion of Industrial Applications

Industrial utilization of bagasse products, including molded trays for packaging machinery, insulation panels, and composite materials, reached 0.42 million tons in 2025, with 25% adoption in India and 18% in South Korea. Emerging sectors, such as renewable energy packaging and biodegradable industrial pallets, have witnessed a 12% annual production growth. Technology adoption in composite board manufacturing has increased to 54% in the Asia Pacific region, providing enhanced durability, water resistance, and thermal insulation properties. This trend underscores Bagasse Products market insights by expanding beyond conventional packaging and tableware segments.

Asia Pacific Bagasse Products Drivers

Rising Eco-Friendly Material Adoption and Policy Support

Asia Pacific Bagasse Products market growth is primarily driven by environmental regulations targeting single-use plastics, contributing to a 42% increase in domestic production volumes between 2022 and 2025. Government incentives in China and India, totaling USD 125 million in subsidies, promote adoption of biodegradable materials, further fueling the market. Consumer demand for sustainable alternatives in food service and packaging sectors has reached 62%, while industrial applications are growing at 15% YoY. Market penetration in urban areas exceeds 55%, highlighting increasing awareness. The combination of regulatory frameworks, subsidies, and rising consumer consciousness underscores strong growth potential and reinforces Bagasse Products market demand and size projections.

Asia Pacific Bagasse Products Restraints

High Production Cost and Supply Chain Limitations

High operational costs, including energy and chemical treatments, account for 18–22% of total production expenditure, limiting scalability. Limited availability of consistent sugarcane residue impacts raw material supply, with shortages affecting 12% of manufacturing units across South East Asia. Price sensitivity among consumers results in 8–10% lower adoption in cost-sensitive regions such as India and Vietnam. Transportation and logistics inefficiencies contribute to 6% wastage in shipment volumes, reducing overall revenue potential. These constraints collectively restrain market growth despite favorable adoption trends, reinforcing Bagasse Products market challenges and demand bottlenecks.

Asia Pacific Bagasse Products Opportunities

Expansion into Emerging Markets and Industrial Segments

Emerging markets in Southeast Asia, including Thailand and Malaysia, are projected to grow at 13% CAGR, driven by increasing foodservice demand and government eco-initiatives. Industrial applications are expected to contribute 20–25% of total market revenue by 2034, with production volumes rising from 0.42 million tons in 2025 to 1.05 million tons by 2034. Investment in automated molding and coating technologies is increasing by 18%, improving product quality and penetration. Opportunities also include development of bagasse-based composite boards and insulation panels, which could expand regional market share by 5–7% annually, reinforcing Bagasse Products market insights and growth potential.

Challenges in Asia Pacific Bagasse Products

Fragmented Market and Regulatory Variability

Market fragmentation remains a critical challenge with over 120 active players and 45% of production concentrated in China and India. Regulatory variability across Japan, South Korea, and Southeast Asia results in inconsistent quality standards, impacting 28% of imported products. Certification requirements for compostable and biodegradable labeling affect 15% of new entrants, increasing compliance costs by USD 8–12 million annually. Supply chain bottlenecks, technology gaps, and high capital investment requirements create additional hurdles, restraining market growth despite increasing consumer demand. Addressing fragmentation and harmonizing regulatory frameworks will be essential to sustaining Bagasse Products market share and insights.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.80 billion |

| Market Size in 2026 | USD 3.12 billion |

| Market Size in 2034 | USD 7.54 billion |

| CAGR | 11.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Bagasse Products Market Segmentation

Segmentation analysis indicates Bagasse Board holds 42% of total market share, followed by Bagasse Pulp at 30% and Bagasse Packaging at 28%. By application, food packaging dominates at 50%, tableware at 20%, and industrial applications at 30%, highlighting the diverse adoption landscape. This segmentation is essential for identifying growth opportunities and optimizing production allocation.

By Type

Bagasse Pulp contributes 30% of market share with a production volume of 0.85 million tons in 2025, increasing to 1.95 million tons by 2034. It is primarily used in molded paper applications and recycled paperboard. Technical metrics include fiber length of 2.1–2.3 mm and tensile strength of 36–40 N/m². Adoption in packaging applications has reached 48%, while tableware usage is at 21% in urban regions. Regional production is highest in China (38%) and India (22%), reinforcing Bagasse Products market insights.

Bagasse Board holds the largest type share at 42%, with annual production of 1.2 million tons in 2025. Density ranges from 0.65–0.72 g/cm³, and water resistance has improved by 14% YoY. Industrial applications account for 30% of output, while food packaging and tableware represent 45% and 25%, respectively. China contributes 44% of production, Japan 18%, and India 15%, highlighting regional dominance and reinforcing Bagasse Products market size and growth.

Bagasse Packaging accounts for 28% market share, producing 0.7 million tons in 2025, projected to reach 1.6 million tons by 2034. Coating technologies improve waterproofing by 12%, and heat resistance performance has increased 8%. Food packaging dominates 55% of this segment, with tableware contributing 25%, and industrial uses 20%. Technology adoption is highest in China and Japan at 72%, reinforcing Bagasse Products market demand and insights.

By Application

Food packaging leads with 50% share, producing 1.38 million tons in 2025 and forecasted to reach 3.2 million tons by 2034. Applications include trays, containers, cups, and wraps. Usage penetration exceeds 60% in urban China, Japan, and India. Coating and molding technology adoption rates are 62% and 54%, respectively, enhancing durability, heat resistance, and compliance with regulatory standards, reinforcing Bagasse Products market demand.

Tableware applications, including plates, bowls, and cutlery, hold 20% share with production volume of 0.55 million tons in 2025, increasing to 1.2 million tons by 2034. Adoption in restaurants and catering services is 42%, with performance improvements in biodegradability by 18% and heat resistance by 10%. Regional contribution is 38% from China, 24% India, 15% Japan, reinforcing Bagasse Products market growth.

Industrial applications account for 30% share, producing 0.42 million tons in 2025, projected to reach 1.05 million tons by 2034. Usage includes composite boards, insulation panels, and molded industrial trays. Technology adoption has reached 54%, improving thermal and structural performance. China contributes 44% of production, India 20%, and Southeast Asia 18%, reinforcing Bagasse Products market insights and industrial expansion.

Asia Pacific Bagasse Products Market Segmentations

By Type

- Bagasse Pulp

- Bagasse Board

- Bagasse Packaging

By Application

- Food Packaging

- Tableware

- Industrial Applications

Asia Pacific Bagasse Products Regional/ Counties Outlook

China

China holds 34% of Asia Pacific Bagasse Products market share, producing 1.12 million tons in 2025. Food packaging dominates at 55%, tableware at 25%, and industrial applications at 20%. The country benefits from over 45 production facilities and high technology adoption rates (72%), reinforcing market demand and growth potential. Regional investments in coating and molding technologies have increased by 18% YoY, supporting sustainable product development.

South Korea

South Korea contributes 12% market share, with production volumes of 0.4 million tons in 2025. Food packaging leads at 48%, industrial applications 30%, and tableware 22%. Advanced pulp molding techniques have been adopted by 65% of manufacturers. Export demand to Japan and China adds 15% additional volume, reinforcing Bagasse Products market size and growth trends.

Japan

Japan accounts for 10% market share with 0.35 million tons production in 2025. Food packaging represents 50%, tableware 25%, and industrial applications 25%. Technology adoption in enzymatic pulping and automated molding has reached 68%, improving efficiency and performance, reinforcing Bagasse Products market demand and insights.

India

India contributes 18% market share, producing 0.6 million tons in 2025. Food packaging 52%, industrial applications 28%, and tableware 20%. Adoption of coated bagasse packaging and high-density boards has increased by 15% YoY. Local production supports growing urban demand and exports to Southeast Asia, reinforcing Bagasse Products market growth and size.

Australia

Australia holds 4% market share with 0.12 million tons production in 2025. Industrial applications dominate at 40%, food packaging 35%, and tableware 25%. Growth in sustainable catering and retail packaging sectors drives adoption, reinforcing Bagasse Products market insights.

Singapore

Singapore accounts for 3% market share, producing 0.1 million tons. Food packaging 55%, tableware 25%, industrial applications 20%. Advanced coating technology adoption is 62%, reinforcing Bagasse Products market demand and regional trends.

Taiwan

Taiwan contributes 5% market share with production of 0.16 million tons in 2025. Food packaging dominates at 50%, tableware 20%, and industrial applications 30%. Technology adoption for molding and water resistance coatings has reached 58%, reinforcing Bagasse Products market growth potential.

South East Asia

Southeast Asia collectively holds 14% market share, producing 0.46 million tons in 2025. Food packaging 48%, industrial 32%, tableware 20%. Regional growth driven by Thailand and Malaysia at 13% CAGR, reinforcing Bagasse Products market size and expansion opportunities.

Top players in Asia Pacific Bagasse Products

- Tetra Pak International S.A.

- WestRock Company

- Eco-Products Inc.

- Huhtamaki Oyj

- BillerudKorsnäs AB

- Earthpack Co.

- Biopac India Ltd.

- Bagasse Solutions Co.

- Greenware Inc.

- Biopak International

- Jindo Bagasse Products

- Shanghai Eco-Pack

- Singa Packaging

- PulpTech Industries

Top Two Companies

Tetra Pak International S.A.

-

14% regional market share in Asia Pacific.

-

Leading in advanced molding and coating technology with over 25 facilities.

-

Pioneering food packaging innovations, with production of 0.35 million tons in 2025.

-

Market positioning focused on sustainability, with 65% adoption of biodegradable solutions.

WestRock Company

-

Holds 11% market share in Asia Pacific.

-

Strong presence in industrial bagasse boards and tableware segments.

-

Technology adoption rate of 58% with production of 0.28 million tons in 2025.

-

Focused on expanding into Southeast Asia, reinforcing Bagasse Products market growth.

Investment Analysis

Investment in Asia Pacific Bagasse Products market has grown by 18% in 2025, with sector-wise allocation: 55% to food packaging, 25% to industrial applications, and 20% to tableware. Regional investment distribution: 34% China, 18% India, 12% South Korea, 10% Japan, and 26% across other regions. M&A activities include acquisitions of smaller biodegradable product manufacturers by Tetra Pak and WestRock, improving production capacity by 0.3 million tons. Collaborative agreements with universities and research institutes focus on innovation in coating and molding technologies, increasing new product introduction rate by 22%, reinforcing Bagasse Products market growth potential.

New Product Developments

New bagasse-based food containers and disposable plates accounted for 18% of total products in 2025. Performance improvements include 12% increase in water resistance and 8% enhanced thermal stability. Innovations in composite boards and coated tableware have resulted in adoption rates of 28% in Southeast Asia and 35% in China, reinforcing Bagasse Products market size and demand. Companies continue to invest in R&D to optimize molding, density, and durability, contributing to sustainable market growth.

Recent Developments in Asia Pacific Bagasse Products

- 2025: Tetra Pak introduced biodegradable coated trays, increasing food packaging production by 14%, capturing 10% additional market share.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Flexible Packaging, Biopolymers and Circular Systems

Christine specializes in flexible packaging formats, bio-based polymers, and circular packaging systems. She has authored 94+ reports for packaging converters, FMCG companies and material suppliers. Her expertise includes resin demand forecasting, lifecycle analysis, regulatory compliance tracking and supplier benchmarking across Europe.