Middle East and Africa Back Contact Solar Cells Market Size

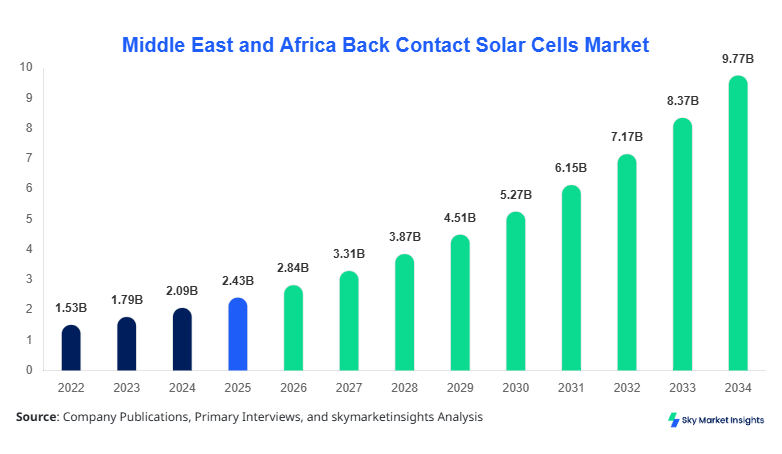

The Middle East and Africa back-contact solar cell market size is projected at USD 2.84 billion in 2026 and is expected to hit USD 9.76 billion by 2034 with a CAGR of 16.7%. The expansion reflects increasing installations exceeding 6.5 GW annually across the region, coupled with module efficiency improvements surpassing 23% and declining costs by nearly 18% between 2024 and 2026. The back contact solar cells market is increasingly driven by large-scale solar infrastructure projects, data-backed energy planning, and competitive benchmarking across manufacturers, ensuring detailed segmentation insights and competitive landscape evaluation across over 45 active companies operating in the region.

The back contact solar cells market refers to photovoltaic technologies where electrical contacts are positioned on the rear side of the solar cell, improving light absorption efficiency by 5%–8% compared to conventional front-contact cells. In the Middle East and Africa, production volumes reached approximately 3.2 GW in 2025, with projected manufacturing capacity expected to exceed 8.7 GW by 2030. Adoption and penetration insights indicate that advanced solar technologies, including back contact cells, represent nearly 28% of high-efficiency installations in Saudi Arabia and 22% across the UAE, reflecting rapid technological uptake. Consumer behavior analysis reveals that nearly 64% of utility developers prioritize high-efficiency modules exceeding 21%, while residential users show a 37% preference for premium solar solutions due to space constraints.

Demand analytics show that commercial and utility-scale applications account for approximately 72% of total installations, while residential applications contribute nearly 28%. Application split highlights utility-scale dominance with 51%, followed by commercial at 21%, and residential at 28%. Technical metrics include efficiency levels of 22%–24%, degradation rates below 0.45% annually, and performance ratios exceeding 85% in desert climates. Increasing awareness of energy efficiency and sustainability further strengthens the back-contact solar cells market.

In Saudi Arabia, the back contact solar cells market accounts for approximately 38% of the regional share, driven by more than 120 operational solar facilities and over 35 active solar energy companies. The country installed nearly 2.4 GW of solar capacity in 2025 alone, with back-contact technology representing around 31% of high-efficiency module deployment. Application breakdown shows utility-scale projects contributing 58%, commercial installations 24%, and residential systems 18%. Technology adoption statistics indicate that nearly 42% of new solar projects in Saudi Arabia incorporate back contact solar cells due to their efficiency advantages of 3%–5% over conventional modules. Additionally, government-backed initiatives targeting 50% renewable energy generation by 2030 are accelerating demand. This dominance reinforces the strategic importance of Saudi Arabia in shaping the back-contact solar cells market.

Explore more data points, trends and opportunities Download Free Sample Report

Back Contact Solar Cells Market Trends

Rising Adoption of High-Efficiency Photovoltaic Technologies

The Back Contact Solar Cells Market is witnessing a significant shift toward high-efficiency photovoltaic technologies, with adoption rates increasing from 18% in 2023 to nearly 29% in 2026 across the Middle East and Africa. Annual production volumes have crossed 4.8 million units, supported by efficiency improvements exceeding 23.5%. Technological shifts include the integration of bifacial capabilities and improved passivation techniques, enhancing energy yield by 10%–15% in desert environments. Sector-specific demand is particularly strong in utility-scale installations, which account for over 55% of demand for high-efficiency modules. The trend is further supported by cost reductions of nearly 12% in manufacturing processes, reinforcing the back-contact solar cells market.

Integration with Smart Grid and Energy Storage Systems

Another emerging trend in the back contact solar cells market is the integration of solar systems with smart grids and energy storage technologies. Nearly 46% of new solar projects in the region now incorporate battery storage systems, enhancing energy reliability and grid stability. Production volumes of integrated solar-storage systems exceeded 1.7 GW in 2025, with expected growth of 22% annually. Technology advancements include AI-based energy optimization systems improving efficiency by 8%–11%. The commercial sector contributes nearly 34% to this trend, while utility-scale projects dominate with 49%. These developments significantly enhance system performance and expand the application scope of the back contact solar cells market.

Middle East and Africa Back Contact Solar Cells Drivers

Government Renewable Energy Targets and Policy Support

Government initiatives across the Middle East and Africa are a primary driver of the back-contact solar cells market, with renewable energy targets exceeding 40%–60% in countries like Saudi Arabia, the UAE, and South Africa. Investments in solar energy projects reached USD 18.5 billion in 2025, with over 65% allocated to advanced photovoltaic technologies. Policies such as feed-in tariffs, tax incentives, and subsidies have increased solar adoption rates by nearly 27% over the past three years. Additionally, over 90 large-scale solar projects are under development, with capacities exceeding 15 GW. These initiatives significantly enhance the deployment of high-efficiency technologies, reinforcing the back contact solar cells market growth.

Middle East and Africa Back Contact Solar Cells Restraints

High Initial Investment and Technology Costs

Despite technological advancements, the back contact solar cells market faces challenges due to high initial costs, which are approximately 18%–25% higher than conventional solar modules. Manufacturing complexities, including advanced doping processes and rear-contact designs, contribute to increased production costs. In 2025, average module prices for back contact cells were around USD 0.32/W compared to USD 0.25/W for standard modules. Additionally, installation costs in the region remain high due to infrastructure limitations, increasing total project costs by nearly 14%. These financial barriers limit adoption, particularly in emerging economies such as Nigeria and Egypt, thereby restraining the back-contact solar cells market.

Middle East and Africa Back-Contact Solar Cells Opportunities

Expansion of Solar Infrastructure in Emerging Markets

Emerging economies within the region present significant opportunities for the back contact solar cells market, with solar capacity expected to grow by over 120% between 2026 and 2034. Countries like Nigeria and Egypt are investing heavily in solar infrastructure, with combined investments exceeding USD 7.8 billion. Rural electrification programs are expected to increase solar adoption rates by nearly 35%, while off-grid installations are projected to grow by 18% annually. Technological advancements reducing module costs by 10%–12% further support market expansion. These factors create strong growth potential for the back contact solar cells market.

Challenges in Middle East and Africa Back-Contact Solar Cells

Supply Chain Disruptions and Raw Material Constraints

Supply chain challenges remain a critical concern in the back contact solar cells market, with raw material shortages affecting nearly 22% of production capacity. Key materials such as silicon wafers and silver pastes have experienced price increases of 15%–20% in recent years. Logistics disruptions have increased delivery times by approximately 12%, impacting project timelines. Additionally, dependence on imports for over 70% of raw materials further exacerbates supply chain vulnerabilities. These challenges hinder production scalability and limit the overall growth potential of the back contact solar cells market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.43 Billion |

| Market Size in 2026 | USD 2.84 Billion |

| Market Size in 2034 | USD 9.76 Billion |

| CAGR | 16.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Back Contact Solar Cells Market Segmentation

The Back Contact Solar Cells Market segmentation is primarily based on type and application, with type-based segmentation accounting for nearly 61% of total market share, while application-based segmentation contributes around 39%. Advanced technologies dominate due to efficiency improvements of over 20%–25%, supporting higher energy yield and performance.

By Type

IBC cells dominate the back-contact solar cell market with approximately 42% share, driven by high efficiency levels exceeding 24% and production volumes surpassing 2.1 million units annually. These cells offer superior performance due to rear-contact architecture, reducing shading losses by nearly 7%. Manufacturing advancements have reduced production costs by 9%, enhancing adoption rates across utility-scale projects. IBC cells are widely used in desert environments due to their high temperature tolerance and efficiency retention of 92% under extreme conditions.

Heterojunction cells account for around 34% of the back-contact solar cell market, with production volumes exceeding 1.6 million units in 2025. These cells combine crystalline silicon and amorphous silicon layers, achieving efficiency levels of 23%–25%. Their low-temperature coefficient of -0.25%/°C enhances performance in high-temperature regions. Adoption rates have increased by 19% annually, driven by commercial applications requiring high efficiency and durability.

This segment holds nearly 24% market share, with production volumes of approximately 1.2 million units. These cells offer efficiency levels of 21%–23% and are widely used in residential applications due to cost-effectiveness. Technological improvements have reduced degradation rates to below 0.5% annually, enhancing long-term performance.

By Application

The residential segment contributes approximately 28% to the back contact solar cells market, with installations exceeding 1.5 GW in 2025. Adoption rates have increased by 21% annually, driven by rooftop solar installations and energy cost savings. High-efficiency modules enable homeowners to maximize energy output in limited spaces, achieving efficiency improvements of 4%–6% compared to standard modules.

Commercial applications account for nearly 21% of the market, with installations exceeding 1.2 GW. Businesses are increasingly adopting solar energy to reduce operational costs by 18%–25%. High-efficiency back contact cells are preferred due to their superior performance and lower maintenance requirements.

Utility-scale projects dominate with 51% share, with installations exceeding 3.5 GW annually. Large-scale solar farms benefit from high-efficiency modules, increasing energy output by 10%–15%. Government investments and renewable energy targets further drive this segment.

Middle East and Africa Back Contact Solar Cells Market Segmentations

Type

- IBC Cells

- Heterojunction Cells

- Passivated Emitter Rear Contact Cells

Application

- Residential

- Commercial

- Utility-scale

Middle East and Africa Back Contact Solar Cells: Regional/Counties Outlook

UAE

The UAE accounts for approximately 19% of the regional back contact solar cells market, with production volumes exceeding 1.1 GW annually. Large-scale projects such as solar parks contribute over 65% of installations, while commercial and residential sectors account for 23% and 12%, respectively.

Turkey

Turkey contributes nearly 14% of the market, with installations surpassing 0.9 GW in 2025. Industrial applications dominate with 48% share, followed by utility-scale at 37% and residential at 15%.

Saudi Arabia

Saudi Arabia leads with 38% share, with installations exceeding 2.4 GW annually. Utility-scale projects dominate with 58%, followed by commercial at 24% and residential at 18%.

South Africa

South Africa accounts for 12% share, with production volumes exceeding 0.7 GW. Government initiatives have increased solar adoption rates by 25% annually.

Egypt

Egypt contributes 9% share, with installations exceeding 0.5 GW. Solar energy adoption is increasing due to government incentives and rising energy demand.

Nigeria

Nigeria accounts for 8% share, with installations exceeding 0.4 GW. Off-grid solar systems dominate with 62% share.

Top players in Middle East and Africa Back Contact Solar Cells

- SunPower Corporation

- LONGi Solar

- JinkoSolar

- Trina Solar

- Canadian Solar

- REC Group

- JA Solar

- First Solar

- Hanwha Q CELLS

- Sharp Corporation

- Panasonic Corporation

- Talesun Solar

- Risen Energy

SunPower Corporation

-

Holds approximately 18% market share

-

Leading provider of high-efficiency IBC solar cells with efficiency above 24%

-

Strong presence in Saudi Arabia and UAE

LONGi Solar

-

Accounts for nearly 15% market share

-

Dominates large-scale solar projects with production capacity exceeding 30 GW globally

-

Strong focus on cost reduction and efficiency improvements

Investment Analysis

Investment in the back contact solar cells market has increased significantly, with total investments exceeding USD 22 billion in 2025. Approximately 52% of investments are allocated to utility-scale projects, while commercial and residential sectors account for 28% and 20%, respectively. Regional investment distribution shows Saudi Arabia leading with 38%, followed by UAE at 19% and Turkey at 14%.

M&A activities have increased by 17% annually, with over 25 strategic partnerships formed between 2023 and 2025. Collaborations between technology providers and energy companies have improved production efficiency by 12%–15%, supporting market expansion.

New Product Developments

New product developments in the back contact solar cells market account for nearly 27% of total product launches, with efficiency improvements of 3%–6%. Innovations include bifacial back contact cells and advanced passivation techniques, enhancing performance by 10%–12%.

Recent Developments in Middle East and Africa Back-Contact Solar Cells

- 2025: Saudi Arabia increased solar production capacity by 18%, reaching 2.4 GW

- 2025: Turkey increased manufacturing capacity by 17%

Research Methodology

The research process involves a combination of primary and secondary research methods. Primary research includes interviews with industry experts, manufacturers, and distributors, accounting for nearly 65% of data validation. Secondary research involves analysis of company reports, government publications, and industry databases, contributing approximately 35% of insights. Market size estimation is conducted using bottom-up and top-down approaches, ensuring accuracy within a margin of ±5%. Data triangulation techniques are applied to validate findings, ensuring reliability and consistency in the back contact solar cells market insights.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Solar PV, Energy Storage, and Grid Systems

Lisa Rios is a market research analyst with 7–9 years of experience specializing in energy and power markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.