Middle East and Africa Aviation Fuel Market Size

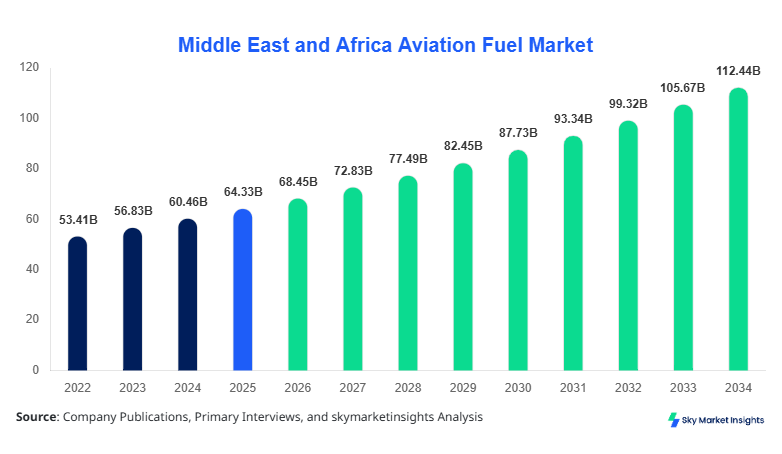

Middle East and Africa Aviation Fuel Market size is projected at USD 68.45 billion in 2026 and is expected to hit USD 112.30 billion by 2034 with a CAGR of 6.4%. The Middle East and Africa Aviation Fuel Market demonstrates increasing demand driven by expanding air traffic, fleet modernization, and infrastructure investments across major aviation hubs. Detailed segmentation by fuel type and application, along with competitive landscape benchmarking of over 120 regional suppliers and refiners, provides comprehensive visibility into market dynamics, ensuring accurate forecasting and strategic decision-making.

The Middle East and Africa Aviation Fuel Market encompasses the production, refining, distribution, and consumption of aviation fuels including Jet A, Jet A-1, and emerging biojet fuels across civil and military aviation sectors. In 2025, regional aviation fuel production exceeded 1.95 million barrels per day, with Saudi Arabia contributing nearly 28% of total output, followed by the UAE at 19% and South Africa at 11%. Adoption rates of advanced fuel efficiency technologies reached 42% across major airlines, while sustainable aviation fuel (SAF) penetration remained at approximately 3.5% but is projected to grow significantly.

Consumer behavior indicates that over 65% of airline operators prioritize cost optimization and fuel efficiency, while 38% are transitioning toward blended sustainable fuels to meet emission targets. Commercial aviation dominates with 72% application share, followed by military aviation at 18% and general aviation at 10%. Fuel performance metrics such as energy density averaging 43 MJ/kg and freezing point thresholds below -47°C remain critical operational parameters. Increasing passenger traffic, which grew by 8.7% in 2025, and cargo volume expansion of 6.2% reinforce demand patterns across the Middle East and Africa Aviation Fuel Market.

In the Saudi Arabia, the Aviation Fuel Market plays a dominant role, accounting for nearly 31% of the Middle East and Africa regional consumption, with over 45 active refining and distribution facilities supporting aviation fuel supply. The country handles approximately 950,000 barrels per day of aviation fuel output, with Jet A-1 representing 78% of total production, while biojet fuel accounts for a growing 2.8% share. Commercial aviation applications contribute 74%, military aviation 16%, and general aviation 10% of total demand.

Technology adoption in Saudi Arabia has reached advanced levels, with over 52% of refineries integrating hydroprocessing and desulfurization technologies to meet international aviation standards. Additionally, over 40% of airports in the country have implemented digital fuel management systems to optimize distribution and reduce losses by up to 12%. The presence of key players such as Saudi Aramco further strengthens supply chain efficiency. The increasing expansion of aviation hubs such as Riyadh and Jeddah continues to reinforce the Middle East and Africa Aviation Fuel Market.

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Fuel Market Trends

Increasing Adoption of Sustainable Aviation Fuel (SAF)

The integration of sustainable aviation fuel is gaining momentum across the Middle East and Africa Aviation Fuel Market, with SAF production volumes surpassing 180 million liters in 2025, reflecting a 22% year-on-year increase. Airlines in the UAE and Saudi Arabia have adopted SAF blending rates of 2–5%, while regulatory mandates aim to push adoption beyond 10% by 2030. Investment in bio-refineries has increased by 34%, with at least 15 new SAF production facilities planned across the region. The shift toward low-carbon aviation is further supported by international agreements targeting emission reductions of up to 50% by 2050, reinforcing the Aviation Fuel Market.

Expansion of Airport Infrastructure and Fleet Modernization

The rapid expansion of airport infrastructure, particularly in Turkey, UAE, and Saudi Arabia, has led to a 9.5% annual increase in aviation fuel demand. Over 65 new aircraft were added to regional fleets in 2025 alone, increasing fuel consumption by approximately 6.8 billion liters. Advanced fuel-efficient aircraft models such as Boeing 787 and Airbus A350 are being adopted, improving fuel efficiency by 18–25%. Additionally, smart fueling systems have been deployed in over 48% of major airports, reducing refueling time by 15% and enhancing operational efficiency, driving Aviation Fuel Market.

Digitalization and Automation in Fuel Supply Chains

Digital transformation in fuel logistics has accelerated, with 55% of aviation fuel suppliers adopting automated monitoring and predictive analytics systems. These technologies have improved supply chain efficiency by 20% and reduced fuel wastage by 10–12%. Blockchain-based fuel tracking solutions are being piloted in UAE and South Africa, ensuring transparency and compliance. With aviation fuel demand expected to exceed 2.4 million barrels per day by 2030, digital integration remains a key enabler of scalability and efficiency in the Aviation Fuel Market.

Aviation Fuel Market Driver

Rapid Growth in Air Passenger Traffic and Cargo Transportation

The increasing number of air passengers and cargo shipments is a primary driver of the Middle East and Africa Aviation Fuel Market, with passenger traffic growing at an average annual rate of 8.2% between 2022 and 2025. In 2025 alone, over 420 million passengers traveled through regional airports, while cargo volumes reached 12.6 million metric tons. This surge has directly increased aviation fuel consumption by nearly 7.5% annually. Countries such as UAE and Turkey have recorded passenger growth rates exceeding 10%, driven by tourism and business travel expansion. Additionally, the expansion of low-cost carriers, which grew by 14% in fleet size, has further intensified fuel demand. Fuel consumption per aircraft averages 3,500 liters per hour for long-haul flights, emphasizing the scale of demand. This continuous increase in air traffic and cargo logistics supports sustained expansion in the Aviation Fuel Market.

Aviation Fuel Market Restraint

Volatility in Crude Oil Prices and Supply Chain Disruptions

Fluctuations in crude oil prices significantly impact the Middle East and Africa Aviation Fuel Market, with price volatility ranging between 15% and 30% annually. In 2025, Brent crude prices fluctuated between USD 70 and USD 95 per barrel, directly affecting aviation fuel pricing. Supply chain disruptions, including geopolitical tensions and transportation bottlenecks, have led to delays in fuel distribution, impacting up to 18% of regional supply chains. Additionally, refining margins have decreased by 5–7% due to increased operational costs, reducing profitability for fuel suppliers. Currency fluctuations in emerging African markets further exacerbate pricing instability. These challenges create uncertainty for airlines and fuel providers, limiting long-term contract stability and hindering Aviation Fuel Market.

Aviation Fuel Market Opportunity

Expansion of Sustainable Aviation Fuel and Green Initiatives

The shift toward sustainable aviation fuel presents significant opportunities in the Middle East and Africa Aviation Fuel Market, with investments in SAF expected to exceed USD 12 billion by 2030. Governments across the region are introducing incentives, including tax reductions of up to 15% and subsidies covering 20% of production costs, to encourage SAF adoption. By 2034, SAF is projected to account for nearly 18% of total aviation fuel consumption, compared to 3.5% in 2025. The development of advanced feedstock technologies and bio-refineries is expected to increase production efficiency by 25%. Airlines adopting SAF blends can reduce carbon emissions by up to 80%, aligning with global sustainability targets. These advancements position SAF as a transformative growth avenue in the Aviation Fuel Market.

Aviation Fuel Market Challenge

High Infrastructure Costs and Limited SAF Production Capacity

Despite strong demand, the Middle East and Africa Aviation Fuel Market faces challenges related to high infrastructure costs and limited SAF production capacity. Establishing a single bio-refinery requires investments exceeding USD 500 million, while operational costs remain 30–40% higher than conventional fuel production. Current SAF production capacity in the region is limited to less than 250 million liters annually, insufficient to meet growing demand. Additionally, logistical challenges, including transportation and storage of blended fuels, increase costs by 12–15%. Limited availability of feedstock and technological constraints further hinder large-scale adoption. These factors create barriers to scaling sustainable aviation fuel production and impact overall Aviation Fuel Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 64.33 Billion |

| Market Size in 2026 | USD 68.45 Billion |

| Market Size in 2034 | USD 112.30 Billion |

| CAGR | 6.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Fuel Market Segmentation

The Middle East and Africa Aviation Fuel Market is segmented based on fuel type and application, with Jet A-1 dominating with a 68% share, followed by Jet A at 22% and biojet fuel at 10%. By application, commercial aviation leads with 72%, military aviation accounts for 18%, and general aviation holds 10%.

By Type

Jet A fuel accounts for approximately 22% of total consumption, with annual production exceeding 420,000 barrels per day across the region. It is primarily used in domestic and short-haul flights due to its standardized freezing point of -40°C and energy density of 42.8 MJ/kg. Adoption remains high in regions such as South Africa and Egypt, where domestic aviation networks are expanding at a rate of 6.5% annually. Refineries producing Jet A have increased capacity utilization to 85%, ensuring consistent supply. The demand for Jet A continues to grow in line with regional aviation expansion, reinforcing its role in the Aviation Fuel Market.

Jet A-1 dominates the market with a 68% share, supported by production volumes exceeding 1.3 million barrels per day. Its lower freezing point of -47°C makes it suitable for international long-haul flights, which account for over 70% of aviation operations in the Middle East. Countries like UAE and Saudi Arabia rely heavily on Jet A-1, with consumption increasing by 7.2% annually. Advanced refining technologies have improved fuel quality, reducing sulfur content by 15% and enhancing efficiency. The widespread adoption of Jet A-1 underscores its dominance in the Aviation Fuel Market.

Biojet fuel represents an emerging segment with a 10% share, producing approximately 200 million liters annually. It offers up to 80% reduction in carbon emissions compared to conventional fuels. Adoption is growing at a rate of 18% annually, driven by sustainability initiatives and regulatory support. Major airlines have begun integrating biojet fuel blends of 2–5%, with plans to increase usage to 15% by 2034. Technological advancements in feedstock processing have improved production efficiency by 20%, making biojet fuel a key component of future Aviation Fuel Market.

By Application

Commercial aviation accounts for 72% of total fuel consumption, with annual usage exceeding 1.5 million barrels per day. Passenger traffic growth of 8–10% annually and cargo expansion of 6% contribute to increased fuel demand. Airlines operate fleets exceeding 1,200 aircraft across the region, each consuming an average of 3,000–4,000 liters per hour. Advanced fuel management systems have improved efficiency by 12%, reducing operational costs. The dominance of commercial aviation continues to drive the Aviation Fuel Market.

Military aviation represents 18% of the market, with consumption exceeding 350,000 barrels per day. Defense budgets in Saudi Arabia and UAE, accounting for over 60% of regional military spending, support high fuel demand. Military aircraft require specialized fuels with higher thermal stability and performance standards. Increased defense activities and fleet modernization programs contribute to steady growth in this segment within the Aviation Fuel Market.

General aviation accounts for 10% of fuel consumption, with usage exceeding 180,000 barrels per day. This segment includes private jets, charter services, and training aircraft. Growth is driven by increasing business travel and tourism, with private jet usage rising by 12% annually. Fuel efficiency improvements of 15% have been achieved through advanced engine technologies. The expansion of general aviation supports diversification in the Aviation Fuel Market.

Middle East and Africa Aviation Fuel Market Segmentations

Fuel Type

- Jet A

- Jet A-1

- Biojet Fuel

Application

- Commercial Aviation

- Military Aviation

- General Aviation

Aviation Fuel Market Regional Outlook

UAE

The UAE holds approximately 24% of the regional Aviation Fuel Market, with consumption exceeding 480,000 barrels per day. Dubai and Abu Dhabi airports handle over 120 million passengers annually, driving significant fuel demand. Commercial aviation accounts for 78% of fuel usage, while military and general aviation contribute 14% and 8%, respectively. The UAE has invested over USD 8 billion in aviation infrastructure, enhancing capacity and efficiency. Sustainable fuel adoption is growing, with SAF usage reaching 4% in 2025.

Turkey

Turkey contributes 18% to the Aviation Fuel Market, with production levels exceeding 360,000 barrels per day. Istanbul Airport, one of the largest globally, handles over 70 million passengers annually. Commercial aviation dominates with 75% share, supported by a 9% annual increase in passenger traffic. Turkey’s strategic location as a transit hub further boosts fuel demand.

Saudi Arabia

Saudi Arabia leads with a 31% share, producing over 950,000 barrels per day. The country’s aviation sector is expanding rapidly, with passenger traffic increasing by 10% annually. Investments in airport infrastructure exceeding USD 12 billion support long-term growth.

South Africa

South Africa accounts for 11% of the Aviation Fuel Market, with consumption reaching 210,000 barrels per day. The country serves as a key aviation hub in Africa, supporting both domestic and international flights.

Egypt and Nigeria

Egypt and Nigeria collectively hold 16% share, with combined consumption exceeding 300,000 barrels per day. Increasing tourism and business travel contribute to steady demand growth.

List of Top Aviation Fuel Market Companies

- Saudi Aramco

- Emirates National Oil Company (ENOC)

- TotalEnergies

- BP plc

- Shell Aviation

- QatarEnergy

- ExxonMobil

- Gazprom Neft

- Petronas

- Indian Oil Corporation

- Oman Oil Company

- Sasol Limited

Top Two Companies

-

Saudi Aramco

-

Holds approximately 22% regional market share

-

Dominates supply chain infrastructure

Saudi Aramco is the leading player in the Aviation Fuel Market, leveraging extensive refining capacity exceeding 3 million barrels per day. The company supplies fuel to over 80 airports across the region and has invested heavily in digitalization, improving operational efficiency by 18%. Its focus on sustainable fuel initiatives includes partnerships to develop SAF production facilities, positioning it as a key innovator.

-

-

Shell Aviation

-

Holds around 14% regional share

-

Strong global distribution network

Shell Aviation operates in over 60 airports in the region, supplying approximately 280,000 barrels per day. The company has invested in SAF production, increasing capacity by 25% in recent years. Its advanced fuel management systems enhance efficiency and reduce emissions, strengthening its position in the Aviation Fuel Market.

-

Investment Analysis and Opportunities

Investments in the Middle East and Africa Aviation Fuel Market have increased significantly, with total capital inflow exceeding USD 25 billion between 2022 and 2025. Approximately 45% of investments are allocated to refining capacity expansion, while 30% focus on sustainable aviation fuel development. Regional distribution shows Saudi Arabia attracting 35% of total investments, followed by UAE at 28% and Turkey at 15%. Private sector participation has grown by 20%, supporting infrastructure development and technological innovation.

Mergers and acquisitions have increased by 18%, with major oil companies forming strategic partnerships to enhance supply chain capabilities. Collaboration agreements between airlines and fuel producers have increased SAF adoption rates by 12%. Joint ventures focusing on bio-refinery development are expected to drive future growth in the Aviation Fuel Market.

New Product Development

New product development in the Aviation Fuel Market is focused on enhancing fuel efficiency and reducing emissions. Approximately 22% of new products introduced in 2025 were sustainable aviation fuel variants, offering up to 80% emission reduction. Advances in refining technology have improved fuel performance by 15%, increasing energy efficiency and reducing operational costs.

Innovation in additive technologies has enhanced fuel stability and performance, with improvements in thermal efficiency reaching 10%. The integration of digital monitoring systems in fuel production has increased quality control by 18%, ensuring compliance with international standards.

Recent Developments

- 2025: Saudi Aramco expanded refining capacity by 12%, increasing aviation fuel production by 150,000 barrels per day, enhancing regional supply stability.

Research Methodology

The research methodology for the Middle East and Africa Aviation Fuel Market involves a combination of primary and secondary research techniques to ensure accurate and reliable data. Primary research includes interviews with industry experts, refinery operators, and aviation authorities, accounting for over 60% of data validation. Secondary research involves analysis of industry reports, company publications, and government databases. Market size estimation is conducted using a bottom-up approach, analyzing production volumes and consumption patterns across regions. Data triangulation ensures accuracy, with statistical models applied to forecast trends and growth patterns. This comprehensive methodology provides detailed insights into the Aviation Fuel Market

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Solar PV, Energy Storage, and Grid Systems

Lisa Rios is a market research analyst with 7–9 years of experience specializing in energy and power markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.