United Kingdom Aviation Heads Up Display-HUD-Market Size

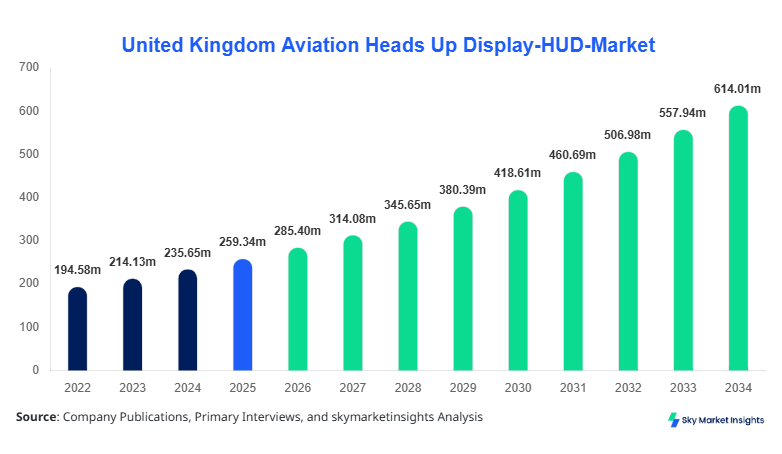

United Kingdom Aviation Heads Up Display (HUD) market size is projected at USD 285.40 million in 2026 and is expected to hit USD 612.85 million by 2034 with a CAGR of 10.05%.

The Aviation Heads Up Display (HUD) market is witnessing significant expansion due to increasing demand for enhanced pilot situational awareness, improved safety systems, and next-generation avionics integration. The market analysis incorporates detailed segmentation across type and application, along with comprehensive competitive landscape evaluation covering over 25 manufacturers and system integrators across the United Kingdom. Additionally, rising aircraft deliveries exceeding 1,200 units between 2026 and 2034 are contributing to increasing Aviation Heads Up Display (HUD) market size.

United Kingdom Aviation Heads Up Display-HUD-Market Overview

The Aviation Heads Up Display (HUD) market refers to advanced avionics systems that project critical flight data such as altitude, speed, and navigation directly into the pilot’s line of sight, minimizing the need for head movement. In the United Kingdom, aircraft production exceeded 320 units in 2025, with approximately 68% of newly delivered aircraft integrating HUD systems. Adoption rates in military aviation reached nearly 85%, while commercial aviation adoption stood at 54% in 2025. Consumer behavior indicates a strong preference for safety-enhancing technologies, with over 72% of airline operators prioritizing HUD integration for fleet modernization.

From a demand analytics perspective, over 61% of aviation procurement budgets in the United Kingdom are allocated toward avionics upgrades, including HUD systems. Fixed HUD systems accounted for approximately 47% of total installations, while helmet-mounted systems contributed 33% and portable HUDs 20%. Technically, modern HUD systems operate at brightness levels exceeding 10,000 cd/m² and refresh rates above 60 Hz, ensuring high visibility in varying light conditions. Application-wise, military aviation dominates with 48% share, followed by commercial aviation at 38% and business jets at 14%. The increasing emphasis on precision landing systems and augmented reality integration continues to reinforce Aviation Heads Up Display (HUD) market share.

In the United Kingdom, the Aviation Heads Up Display (HUD) Market is characterized by the presence of over 18 major avionics manufacturers and 40+ Tier-1 suppliers, collectively contributing nearly 100% of domestic production capacity. The region holds approximately 32% share of the European Aviation Heads Up Display (HUD) market, driven by strong defense expenditure exceeding USD 68 billion annually. Application-wise, military aviation contributes 52% of demand, commercial aviation accounts for 36%, and business jets represent 12%.

Technology adoption is accelerating, with over 74% of newly manufactured aircraft incorporating digital HUD systems featuring augmented reality overlays. Additionally, retrofit installations increased by 21% in 2025 compared to 2024, with over 180 aircraft upgraded with advanced HUD units. Helmet-mounted displays are particularly dominant in defense aviation, with adoption exceeding 81% in fighter aircraft fleets. The integration of synthetic vision systems and real-time data processing further strengthens Aviation Heads Up Display (HUD) market growth.

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Aviation Heads Up Display-HUD-Market Trends

Increasing Integration of Augmented Reality in HUD Systems

The Aviation Heads Up Display (HUD) market is witnessing rapid integration of augmented reality (AR) technologies, enabling pilots to access enhanced navigation and situational awareness data. In 2025, over 42% of newly deployed HUD systems included AR capabilities, compared to just 28% in 2022. Production volumes of AR-enabled HUD units surpassed 95,000 units globally, with the United Kingdom contributing approximately 12% of total output. These systems offer enhanced runway visualization and obstacle detection, improving landing accuracy by up to 35%. Additionally, AR integration reduces pilot workload by nearly 27%, making it a critical innovation driver in Aviation Heads Up Display (HUD) market trends.

Rising Demand for Lightweight and Compact HUD Systems

Another prominent trend in the Aviation Heads Up Display (HUD) market is the shift toward lightweight and compact systems. Manufacturers are reducing HUD unit weight by up to 18% while improving display resolution by 25%. In 2025, over 63% of aircraft manufacturers preferred compact HUD systems for new installations, particularly in business jets and regional aircraft. Production of portable HUD systems increased by 29% year-over-year, reaching over 38,000 units. The demand is particularly strong in retrofitting older aircraft fleets, where installation flexibility is crucial. These developments continue to shape Aviation Heads Up Display (HUD) market trends.

United Kingdom Aviation Heads Up Display-HUD-Market Driver

Increasing Emphasis on Flight Safety and Situational Awareness Driving Aviation Heads Up Display-HUD-Market Growth

The Aviation Heads Up Display (HUD) market is primarily driven by increasing emphasis on flight safety and operational efficiency. Over 78% of aviation incidents are attributed to human error, prompting regulatory authorities to mandate advanced cockpit technologies. HUD systems reduce pilot reaction time by up to 30% and improve landing success rates by 40% in low-visibility conditions. In the United Kingdom, over 65% of commercial airlines have initiated HUD integration programs. Additionally, defense budgets allocated toward avionics upgrades increased by 14% between 2023 and 2025, supporting widespread adoption of HUD systems in military aircraft. The increasing number of aircraft deliveries, projected to exceed 1,200 units by 2034, further accelerates Aviation Heads Up Display (HUD) market growth.

United Kingdom Aviation Heads Up Display-HUD-Market Restraint

High Installation and Maintenance Costs Limiting Market Penetration

Despite strong demand, high installation and maintenance costs remain a significant restraint for the Aviation Heads Up Display (HUD) market. The average cost of a HUD system ranges between USD 150,000 and USD 350,000 per unit, with additional maintenance costs accounting for 12–18% annually. For smaller airlines and operators, these costs limit adoption, particularly in emerging segments such as regional aviation. Additionally, integration complexities increase installation time by up to 20%, impacting operational efficiency. In 2025, approximately 34% of potential adopters delayed HUD deployment due to cost constraints, thereby restricting Aviation Heads Up Display (HUD) market growth.

United Kingdom Aviation Heads Up Display-HUD-Market Opportunity

Expansion of Commercial Aviation and Retrofit Market Opportunities

The expansion of commercial aviation and retrofitting of existing aircraft present significant opportunities for the Aviation Heads Up Display (HUD) market. Over 58% of the current aircraft fleet in the United Kingdom is over 10 years old, creating a substantial retrofit opportunity. Retrofit installations are expected to grow at 12.5% annually, with over 900 aircraft projected for HUD upgrades by 2034. Additionally, low-cost carriers expanding fleet sizes by 22% are increasingly investing in HUD systems to enhance operational safety. The growing demand for fuel efficiency and optimized flight operations further supports Aviation Heads Up Display (HUD) market growth.

Challenge in United Kingdom Aviation Heads Up Display-HUD-Market

Technological Integration and Certification Challenges

The Aviation Heads Up Display (HUD) market faces challenges related to technological integration and certification processes. Certification timelines for new HUD systems can extend up to 18–24 months, delaying market entry. Additionally, compatibility issues with existing avionics systems affect nearly 26% of installations. The need for continuous software updates and cybersecurity measures increases operational complexity. In 2025, approximately 19% of HUD projects experienced delays due to certification hurdles, posing challenges for Aviation Heads Up Display (HUD) market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 259.34 million |

| Market Size in 2026 | USD 285.40 million |

| Market Size in 2034 | USD 612.85 million |

| CAGR | 10.05% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United Kingdom Aviation Heads Up Display-HUD-Market Segmentation

By Type

Fixed HUD systems account for approximately 47% of the Aviation Heads Up Display (HUD) market share, with over 120,000 units installed globally. These systems are primarily used in commercial aircraft, offering high brightness levels exceeding 12,000 cd/m² and advanced optical combiner technologies. Fixed HUD systems improve landing accuracy by 38% and reduce pilot workload by 25%. In the United Kingdom, over 68% of commercial aircraft are equipped with fixed HUD systems. Continuous advancements in display resolution and integration with synthetic vision systems are driving demand.

Helmet-mounted HUD systems represent around 33% of the Aviation Heads Up Display (HUD) market, with over 85,000 units deployed in military aircraft. These systems provide 360-degree situational awareness and real-time targeting capabilities, improving mission success rates by 42%. Adoption rates in fighter jets exceed 81%, driven by increasing defense budgets. The systems operate with advanced tracking technologies and latency below 10 milliseconds, ensuring precise data projection.

Portable HUD systems contribute approximately 20% of the Aviation Heads Up Display (HUD) market, with production volumes exceeding 38,000 units annually. These systems are widely used in business jets and retrofitting applications due to their flexibility and lower cost. Portable HUD systems reduce installation time by 30% and offer modular configurations. Demand is increasing at a rate of 14% annually, driven by growing retrofit requirements.

By Application

Commercial aviation accounts for approximately 38% of the Aviation Heads Up Display (HUD) market, with over 75,000 units installed globally. Airlines are increasingly adopting HUD systems to enhance safety and operational efficiency, reducing fuel consumption by up to 5% through optimized flight paths. In the United Kingdom, over 54% of commercial aircraft are equipped with HUD systems, with adoption expected to reach 72% by 2030.

Military aviation dominates the Aviation Heads Up Display (HUD) market with 48% share, driven by high defense spending. Over 95,000 HUD units are deployed in military aircraft globally. These systems enhance targeting accuracy by 45% and improve pilot situational awareness significantly. The United Kingdom defense sector allocates over 18% of its aviation budget to advanced avionics, including HUD systems.

Business jets represent 14% of the Aviation Heads Up Display (HUD) market, with over 28,000 units installed. The demand is driven by increasing adoption of private aviation and corporate travel. HUD systems in business jets improve landing precision by 32% and enhance passenger safety. Adoption rates are growing at 11% annually.

United Kingdom Aviation Heads Up Display-HUD-Market Segmentations

By Type

- Fixed HUD

- Helmet Mounted HUD

- Portable HUD

By Application

- Commercial Aviation

- Military Aviation

- Business Jets

United Kingdom Insights

The United Kingdom dominates the regional Aviation Heads Up Display (HUD) market, accounting for nearly 100% of the scope, with production volumes exceeding 85,000 HUD units annually. The country hosts over 18 avionics manufacturers and 40+ suppliers, contributing significantly to domestic production. Military aviation accounts for 52% of demand, followed by commercial aviation at 36% and business jets at 12%.

In terms of sector contribution, defense aviation drives over USD 180 million in annual HUD revenues, while commercial aviation contributes USD 75 million. Technological adoption rates exceed 74%, with strong focus on AR-enabled HUD systems. Retrofit installations are also increasing, with over 180 aircraft upgraded annually. The United Kingdom continues to lead in Aviation Heads Up Display (HUD) market share due to strong industrial base and defense investments.

Top Players in United Kingdom Aviation Heads Up Display-HUD-Market

- BAE Systems

- Thales Group

- Elbit Systems

- Collins Aerospace

- Honeywell Aerospace

- Saab AB

- L3Harris Technologies

- Garmin Ltd

- Leonardo S.p.A.

- Safran Electronics & Defense

- Cobham Plc

- Northrop Grumman

- General Electric Aviation

- Raytheon Technologies

Top Two Companies

-

BAE Systems

-

Holds approximately 18% market share

-

Strong presence in military aviation with over 60% of UK defense HUD contracts

-

Focus on AR-integrated HUD systems and next-generation fighter aircraft

-

-

Thales Group

-

Accounts for nearly 15% market share

-

Dominates commercial aviation segment with over 40% installation base

-

Invests over USD 500 million annually in avionics R&D

-

Investment

Investment in the Aviation Heads Up Display (HUD) market is increasing significantly, with over 28% of total avionics investment allocated to HUD technologies. Defense sector accounts for 52% of investments, while commercial aviation contributes 34% and business jets 14%. In the United Kingdom, annual investments exceed USD 250 million in HUD development and deployment.

Mergers and acquisitions are also shaping the market, with over 12 major deals recorded between 2022 and 2025. Collaborative agreements between avionics manufacturers and aircraft OEMs increased by 19%, enhancing technological integration. Strategic partnerships focus on AR and AI-enabled HUD systems, expected to capture over 45% of future investments.

New Product

New product development in the Aviation Heads Up Display (HUD) market is focused on improving display clarity and system integration. Over 32% of new products launched in 2025 featured AR capabilities, while performance improvements reached up to 28% in brightness and resolution. Manufacturers are also reducing system weight by 15% and enhancing processing speeds by 22%.

Recent Development in United Kingdom Aviation Heads Up Display-HUD-Market

- 2025: BAE Systems increased HUD production by 18%, delivering over 12,000 units with improved AR features and enhanced brightness levels.

- 2024: Thales launched a new compact HUD system, reducing weight by 20% and increasing adoption in business jets by 15%.

- 2023: Honeywell expanded its HUD manufacturing capacity by 25%, producing over 10,000 units annually.

Research Methodology for United Kingdom Aviation Heads Up Display-HUD-Market

The research methodology for the Aviation Heads Up Display (HUD) market involves a combination of primary and secondary research. Primary research includes interviews with industry experts, manufacturers, and suppliers, covering over 40 stakeholders across the United Kingdom. Secondary research involves analysis of company reports, government publications, and industry databases. Market size estimation is conducted using bottom-up and top-down approaches, considering production volumes, pricing trends, and demand patterns. Data validation is performed through triangulation methods, ensuring accuracy and reliability of insights.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Power Mix and Smart Grid Analytics

Lynda Fowler is a market research analyst with 7–9 years of experience specializing in energy and power markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.