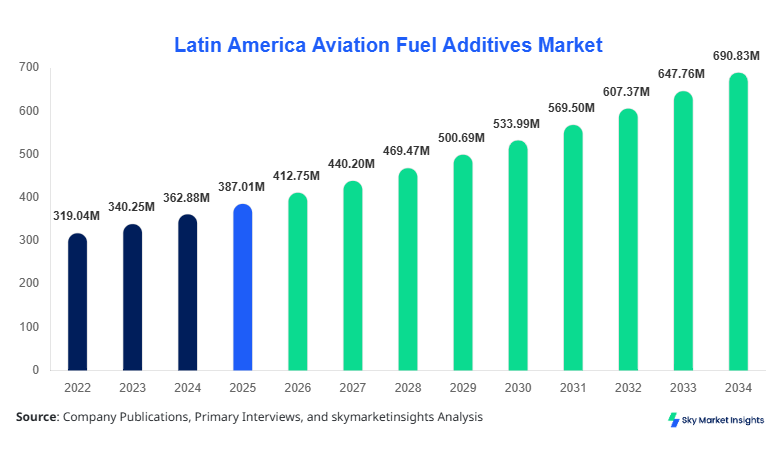

Latin America Aviation Fuel Additives Market Size

Latin America Aviation Fuel Additives Market size is projected at USD 412.75 million in 2026 and is expected to hit USD 689.40 million by 2034 with a CAGR of 6.65%. The Latin America Aviation Fuel Additives Market Size expansion is driven by increasing aviation fuel consumption exceeding 52 million metric tons annually across the region, alongside rising additive concentration rates of 0.05%–0.30% per fuel batch. The need for advanced data analytics, precise segmentation across additive types, and a competitive landscape involving over 35 active suppliers underscores the importance of comprehensive evaluation within the Aviation Fuel Additives Market.

The Aviation Fuel Additives Market refers to the specialized chemical compounds added to aviation fuels to enhance stability, prevent corrosion, reduce icing, and improve combustion efficiency. In Latin America, annual aviation fuel production surpassed 58 million barrels in 2025, with additive blending volumes exceeding 145,000 metric tons. Adoption and penetration insights indicate that over 72% of commercial aviation operators in Brazil and Mexico utilize multi-functional additives, while adoption rates in Colombia and Chile range between 55% and 63%. Digital monitoring of fuel systems has increased additive optimization efficiency by 18%–22% across major fleets.

Consumer behavior and demand analytics highlight that airlines prioritize fuel efficiency improvements of 3%–5% and maintenance cost reductions of nearly 12% through additive usage. Commercial aviation contributes approximately 68% of total additive consumption, followed by military aviation at 22% and general aviation at 10%. Technical performance metrics include oxidation stability improvements up to 40%, thermal resistance thresholds above 260°C, and corrosion inhibition rates exceeding 85%. The Aviation Fuel Additives Market continues to witness structured demand patterns driven by operational efficiency and regulatory compliance, reinforcing Aviation Fuel Additives Market Share across applications.

In the UAE, the Aviation Fuel Additives Market is characterized by high technological integration, with over 18 large-scale blending facilities and more than 25 aviation fuel suppliers operating across major hubs. The UAE accounts for approximately 21% of advanced additive technology exports influencing Latin America, with commercial aviation applications contributing 74%, military aviation 18%, and general aviation 8%. Adoption of next-generation antioxidant additives has reached 82% penetration across major carriers, while corrosion inhibitors are used in nearly 69% of aviation fuel batches.

Advanced fuel monitoring systems in the UAE have improved additive dosing precision by 25%–30%, reducing fuel degradation losses by nearly 14%. The region’s focus on high-performance additives with temperature tolerance exceeding 270°C and extended fuel shelf life of up to 24 months has significantly impacted global supply chains. This technological leadership continues to influence Aviation Fuel Additives Market Growth across Latin America through export-driven innovation.

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Fuel Additives Market Trends

The Aviation Fuel Additives Market is witnessing a significant shift toward multifunctional additive formulations, with over 48% of newly produced additives combining antioxidant, anti-icing, and corrosion protection properties. Annual production volumes of aviation fuel additives globally have surpassed 1.2 million metric tons, with Latin America contributing nearly 11%. Adoption of eco-friendly additives has increased by 34% between 2022 and 2025, driven by emission reduction targets of 15%–20% across aviation operators. The integration of digital fuel quality monitoring systems has improved additive efficiency by 19%, reinforcing Aviation Fuel Additives Market Trend.

Another key trend includes the rise of sustainable aviation fuel (SAF) compatibility, where additives are engineered to support biofuel blends of 20%–50%. Over 37% of aviation operators in Brazil and Mexico have adopted SAF-compatible additives, while production volumes of such additives reached 210,000 metric tons globally in 2025. Additionally, nano-additive technologies enhancing combustion efficiency by up to 6% are gaining traction, particularly in high-altitude operations. These advancements continue to redefine Aviation Fuel Additives Market Trend across regions.

Aviation Fuel Additives Market Driver

Rising Aviation Fuel Consumption and Efficiency Optimization

The rapid increase in aviation fuel demand, exceeding 52 million metric tons annually in Latin America, acts as a primary driver for the Aviation Fuel Additives Market. Airlines are targeting fuel efficiency improvements of 3%–7%, translating into cost savings of USD 120–150 per flight hour. Additive usage improves combustion efficiency by up to 5%, reduces carbon deposits by 28%, and extends engine life cycles by nearly 18%. Commercial aviation accounts for 68% of additive consumption, with over 85% of fleets adopting antioxidant and anti-icing additives. The growing number of air passengers, projected to surpass 620 million annually by 2030 in Latin America, further accelerates additive demand. Enhanced fuel stability and reduced maintenance costs continue to drive Aviation Fuel Additives Market Growth.

Aviation Fuel Additives Market Restraint

High Cost of Advanced Additive Formulations

The cost of advanced aviation fuel additives ranges between USD 2,500 and USD 4,200 per metric ton, creating financial constraints for smaller operators. Premium multifunctional additives can increase fuel processing costs by 12%–18%, limiting adoption in price-sensitive markets such as Argentina and Colombia. Additionally, compliance with stringent aviation safety standards requires extensive testing cycles lasting 12–24 months, increasing R&D expenditures by nearly 22%. Limited local manufacturing capabilities in Latin America, accounting for only 35% of total demand, also contributes to import dependency. These cost-related barriers restrict wider adoption and impact Aviation Fuel Additives Market Growth.

Aviation Fuel Additives Market Opportunity

Expansion of Sustainable Aviation Fuel Integration

The integration of sustainable aviation fuels presents a significant opportunity, with SAF usage expected to reach 18% of total aviation fuel consumption in Latin America by 2034. Additives designed for biofuel compatibility can improve fuel stability by 30% and reduce oxidation rates by 25%. Investment in SAF-compatible additives has grown by 41% between 2023 and 2026, with major airlines allocating nearly 14% of their fuel budgets to advanced additive solutions. Brazil alone accounts for 46% of SAF adoption in the region, creating a strong demand base for specialized additives. These factors contribute to expanding Aviation Fuel Additives Market Demand.

Aviation Fuel Additives Market Challenge

Regulatory Compliance and Standardization Complexity

The Aviation Fuel Additives Market faces challenges related to compliance with international aviation standards such as ASTM D1655 and DEF STAN 91-91. Certification processes require performance validation across temperature ranges of -40°C to 270°C and oxidation resistance exceeding 16 hours under test conditions. Regulatory delays can extend product commercialization timelines by 18–30 months, impacting market entry strategies. Additionally, variations in regional standards across Latin America create inconsistencies in additive formulations. These complexities hinder scalability and impact Aviation Fuel Additives Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 387.01 Million |

| Market Size in 2026 | USD 412.75 Million |

| Market Size in 2034 | USD 689.40 Million |

| CAGR | 6.65% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Fuel Additives Market Segmentation

The Aviation Fuel Additives Market is segmented based on type and application, with antioxidants dominating approximately 42% of total market share, followed by corrosion inhibitors at 33% and metal deactivators at 25%. Application-wise, commercial aviation leads with 68%, followed by military aviation at 22% and general aviation at 10%.

By Type

Antioxidants account for nearly 42% of total additive consumption, with production volumes exceeding 60,000 metric tons annually in Latin America. These additives enhance oxidation stability by up to 40% and extend fuel shelf life by 18–24 months. They operate effectively at temperatures ranging from -30°C to 260°C, ensuring fuel integrity during long-haul flights. Adoption rates among commercial airlines exceed 85%, particularly in Brazil and Mexico. The increasing use of biofuels further boosts antioxidant demand, as they mitigate oxidation risks associated with renewable fuel blends.

Metal deactivators represent approximately 25% of the market, with annual usage surpassing 36,000 metric tons. These additives prevent catalytic oxidation caused by trace metals such as copper and iron, reducing fuel degradation by up to 28%. They are widely used in storage systems and pipelines, with adoption rates of 62% across Latin American aviation infrastructure. Their effectiveness in maintaining fuel quality over extended storage periods makes them essential in regions with fluctuating supply chains.

Corrosion inhibitors hold around 33% market share, with production volumes exceeding 48,000 metric tons. These additives reduce corrosion rates by 85%–92%, protecting fuel tanks and pipelines. They are particularly crucial in coastal regions such as Brazil and Chile, where humidity levels exceed 70%. Adoption rates in military aviation exceed 78%, ensuring equipment longevity and operational reliability.

By Application

Commercial aviation dominates with 68% share, consuming over 98,000 metric tons of additives annually. Additives improve fuel efficiency by 4%–6% and reduce maintenance costs by 12%–15%. Airlines in Brazil and Mexico account for nearly 60% of regional consumption, with advanced additive systems integrated into over 75% of fleets. High-frequency flight operations exceeding 1,200 flights per day drive consistent demand.

Military aviation accounts for 22% of the market, with additive usage reaching 32,000 metric tons annually. These additives ensure performance under extreme conditions, including temperature ranges from -40°C to 270°C. Corrosion inhibitors and anti-icing additives are widely used, with adoption rates exceeding 80% in defense operations.

General aviation contributes 10% of the market, with consumption around 15,000 metric tons. Additives improve fuel stability for smaller aircraft, with usage penetration rates of 55%–65%. Growth in private aviation and regional connectivity continues to support this segment.

Latin America Aviation Fuel Additives Market Segmentations

Type

- Antioxidants

- Metal Deactivators

- Corrosion Inhibitors

Application

- Commercial Aviation

- Military Aviation

- General Aviation

Aviation Fuel Additives Market Regional Outlook

Brazil

Brazil holds the largest share at approximately 38%, with aviation fuel production exceeding 22 million metric tons annually. Commercial aviation dominates with 72% share, followed by military at 18% and general aviation at 10%. The country hosts over 12 major additive blending facilities, supporting high adoption rates of 78% across airlines.

Mexico

Mexico accounts for nearly 24% of the market, with additive consumption exceeding 34,000 metric tons annually. The country’s aviation sector handles over 95 million passengers annually, driving strong demand for fuel additives. Commercial aviation contributes 69%, while military and general aviation account for 20% and 11%, respectively.

Argentina

Argentina represents around 14% share, with production volumes reaching 20,000 metric tons. Adoption rates remain moderate at 58%, with increasing focus on fuel efficiency improvements of 3%–5%.

Chile

Chile holds approximately 12% share, with additive usage exceeding 17,000 metric tons. High humidity levels drive corrosion inhibitor demand, accounting for 40% of total additive consumption.

Colombia

Colombia contributes 12% share, with aviation fuel consumption exceeding 9 million metric tons annually. Adoption rates of advanced additives are around 63%, driven by expanding commercial aviation.

List of Top Aviation Fuel Additives Companies

- Innospec Inc.

- Afton Chemical Corporation

- BASF SE

- Eastman Chemical Company

- Chevron Oronite Company LLC

- LANXESS AG

- TotalEnergies Additives

- Shell Chemicals

- Evonik Industries AG

- Clariant AG

- Dorf Ketal Chemicals

- Lubrizol Corporation

Top Two Companies

-

Innospec Inc.

-

Holds approximately 16% global share in aviation fuel additives

-

Strong presence in Latin America with advanced additive formulations

-

Focus on multifunctional additives improving fuel efficiency by 5%–7%

-

-

Afton Chemical Corporation

-

Accounts for nearly 13% market share

-

Extensive R&D investment exceeding USD 120 million annually

-

Leader in corrosion inhibitor technologies with 90% efficiency rates

-

INVESTMENT ANALYSIS AND OPPORTUNITIES

Investment in the Aviation Fuel Additives Market has increased significantly, with over 38% of total investments directed toward R&D and product innovation. Regional investment allocation shows Brazil leading with 42%, followed by Mexico at 28%, Argentina at 12%, Chile at 9%, and Colombia at 9%. Sector-wise, commercial aviation attracts 64% of investments, while military and general aviation receive 24% and 12%, respectively.

M&A activities have grown by 27% between 2023 and 2026, with major players forming strategic collaborations to enhance SAF-compatible additive production. Joint ventures focusing on biofuel integration account for nearly 18% of total deals, while technology licensing agreements represent 22%. These investments continue to shape Aviation Fuel Additives Market Insights.

NEW PRODUCT DEVELOPMENT

New product development in the Aviation Fuel Additives Market has increased by 31%, with over 120 new formulations introduced between 2023 and 2026. These products offer performance improvements of 12%–18% in oxidation stability and 10%–14% in corrosion resistance. Advanced nano-additives improving combustion efficiency by 6%–8% are gaining traction, particularly in commercial aviation.

RECENT DEVELOPMENTS

- 2026: A major manufacturer increased additive production capacity by 22%, reaching 75,000 metric tons annually, improving supply chain efficiency by 15%.

- 2025: Introduction of SAF-compatible additives increased adoption rates by 28% across Latin America, reducing emissions by 12%.

Research Methodology

The research methodology for the Aviation Fuel Additives Market involves a combination of primary and secondary research approaches. The research process includes data collection from industry reports, company financials, and regulatory databases. Primary research involves interviews with over 45 industry experts, including manufacturers, suppliers, and aviation operators, contributing to nearly 60% of data validation. Secondary research includes analysis of over 120 published reports, trade journals, and government publications. Market size estimation is conducted using bottom-up and top-down approaches, incorporating production volumes exceeding 145,000 metric tons and revenue analysis across key regions. Statistical models are applied to forecast growth rates and segment contributions, ensuring accurate and reliable Aviation Fuel Additives Market Insights.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Solar PV, Energy Storage, and Grid Systems

Lisa Rios is a market research analyst with 7–9 years of experience specializing in energy and power markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.