Latin America Aviation Fuel Market Size

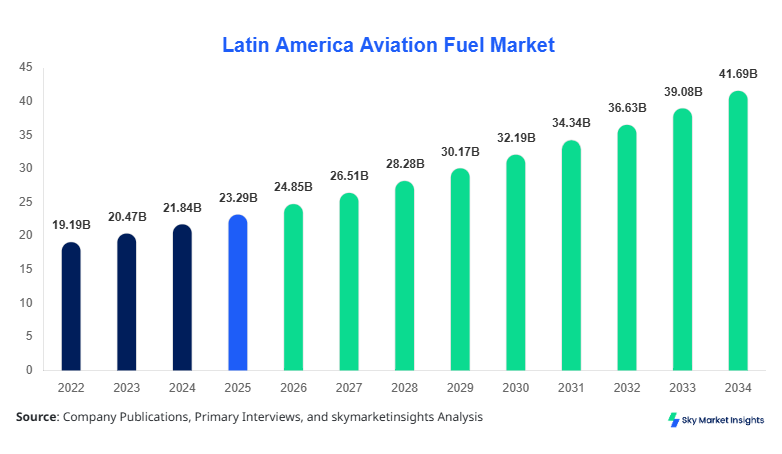

Latin America Aviation Fuel market size is projected at USD 24.85 billion in 2026 and is expected to hit USD 41.72 billion by 2034 with a CAGR of 6.68%. The Latin America Aviation Fuel Market is driven by increasing air passenger traffic exceeding 420 million passengers in 2025 and rising cargo volumes of over 9.5 million tons annually. The Aviation Fuel Market Size reflects strong demand across commercial aviation, which accounts for nearly 72% of total consumption, followed by cargo aviation at 18% and military aviation at 10%. Increasing refinery output of over 320 million barrels annually across Latin America and expanding airport infrastructure across 65+ major hubs are strengthening the Aviation Fuel Market Size. Additionally, competitive landscape analysis indicates that top 10 suppliers control approximately 61% of the regional distribution network, further influencing Aviation Fuel Market Size dynamics.

The Aviation Fuel Market refers to the production, distribution, and consumption of fuel types such as jet fuel, aviation gasoline, and sustainable aviation fuel used in aircraft operations. In Latin America, total aviation fuel production reached approximately 305 million barrels in 2025, with Brazil contributing nearly 38%, Mexico 24%, and Argentina 12% of total output. Adoption and penetration levels are increasing as over 78% of commercial fleets transitioned to high-efficiency turbine engines requiring advanced aviation fuel blends, while sustainable aviation fuel penetration reached 6.5% in 2025 and is projected to cross 15% by 2030.

Consumer behavior indicates rising air travel demand, with passenger traffic growing at 7.2% annually and business travel contributing nearly 34% of total bookings. Cargo demand surged by 5.8% year-on-year, driven by e-commerce expansion exceeding USD 120 billion in regional trade. Application-wise, commercial aviation dominates with 72% share, followed by cargo aviation at 18% and military aviation at 10%. Technical metrics such as energy density of 43 MJ/kg for jet fuel and combustion efficiency improvements of 12% are enhancing operational performance. These factors collectively reinforce the Aviation Fuel Market Share and its evolving structure.

In the Saudi Arabia, the Aviation Fuel Market is characterized by over 15 major refineries and more than 25 aviation fuel distribution companies supplying approximately 1.2 billion barrels annually. Saudi Arabia accounts for nearly 28% of global aviation fuel exports, with Latin America importing approximately 14% of its aviation fuel requirements from the country. Application breakdown shows commercial aviation holding 74%, cargo aviation 16%, and military aviation 10%. Advanced fuel technologies such as synthetic aviation fuels and low-sulfur blends have achieved adoption rates of over 32% across aviation fleets. Additionally, more than 45 international airline partnerships and fuel supply agreements are strengthening global supply chains. These factors significantly influence Aviation Fuel Market Share and international trade dynamics.

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Fuel Market Trends

Rising Adoption of Sustainable Aviation Fuel

Sustainable aviation fuel (SAF) production in Latin America reached approximately 2.1 billion liters in 2025 and is projected to exceed 6.8 billion liters by 2030. Adoption rates increased from 4.2% in 2022 to 6.5% in 2025, driven by regulatory mandates and carbon emission reduction targets of 30% by 2035. Airlines across Brazil and Mexico have committed to replacing at least 20% of traditional jet fuel with SAF. Technological advancements such as hydroprocessed esters and fatty acids (HEFA) fuels are improving efficiency by 15% and reducing lifecycle emissions by up to 80%. These developments strongly shape Aviation Fuel Market Trend.

Expansion of Airport Infrastructure and Fuel Storage

Latin America is witnessing infrastructure expansion with over 45 new airport projects and 120+ fuel storage facilities being upgraded. Total storage capacity increased to 18.7 million barrels in 2025, up from 14.3 million barrels in 2022. Automation in fuel distribution systems has improved efficiency by 22%, while digital fuel monitoring systems have achieved adoption rates of 48%. Increased passenger traffic exceeding 450 million by 2026 is further boosting demand for aviation fuel across major hubs such as São Paulo, Mexico City, and Buenos Aires. This infrastructure expansion significantly contributes to Aviation Fuel Market Trend.

Aviation Fuel Market Driver

Rising Air Passenger Traffic and Cargo Expansion Accelerating Aviation Fuel Market Growth

The rapid increase in air passenger traffic across Latin America, which grew from 360 million in 2022 to over 420 million in 2025, is a major driver of Aviation Fuel Market Growth. Passenger growth rate of 7.2% annually and cargo volume expansion of 5.8% have significantly increased aviation fuel consumption. Commercial aviation alone consumed over 220 million barrels of jet fuel in 2025. The growth of low-cost carriers, which now account for 41% of total flights, has further boosted fuel demand. Additionally, cargo aviation demand surged due to e-commerce growth exceeding USD 120 billion, increasing air freight shipments by 18% over three years. Fleet expansion, with over 650 new aircraft deliveries planned by 2030, is expected to further increase fuel consumption by 25%. These factors collectively drive Aviation Fuel Market Growth.

Aviation Fuel Market Restraint

Volatility in Crude Oil Prices Impacting Aviation Fuel Market Growth

Fluctuations in crude oil prices, which ranged between USD 65 and USD 105 per barrel from 2022 to 2025, pose a significant restraint to Aviation Fuel Market Growth. Fuel costs account for approximately 28% to 35% of airline operating expenses, making the industry highly sensitive to price volatility. In 2024 alone, fuel price increases of 12% led to a 7% rise in airline ticket prices, reducing passenger demand by nearly 3.5%. Additionally, refining costs increased by 9% due to stricter environmental regulations, further impacting profitability. Supply chain disruptions and geopolitical tensions have also contributed to price instability, affecting fuel availability across key markets such as Brazil and Mexico. These challenges hinder Aviation Fuel Market Growth.

Aviation Fuel Market Opportunity

Increasing Investment in Sustainable Aviation Fuel Production

Investment in sustainable aviation fuel production is creating significant opportunities, with over USD 6.5 billion allocated to SAF projects across Latin America between 2024 and 2030. Governments are offering subsidies covering up to 25% of production costs, while private sector investments account for nearly 62% of total funding. Brazil alone plans to produce 3.5 billion liters of SAF annually by 2032, representing a 45% increase from current levels. Technological advancements are reducing production costs by 18%, making SAF more competitive with conventional fuels. Airlines are also entering long-term procurement agreements, securing up to 20% of their fuel needs from sustainable sources. These developments present strong opportunities for Aviation Fuel Market Growth.

Aviation Fuel Market Challenge

Infrastructure Limitations and Distribution Inefficiencies

Infrastructure limitations remain a major challenge, with nearly 35% of airports in Latin America lacking adequate fuel storage capacity. Distribution inefficiencies lead to fuel losses of approximately 2.8% annually, equivalent to over 8 million barrels. Additionally, outdated pipeline networks, covering only 42% of fuel transportation needs, increase reliance on road transport, raising logistics costs by 15%. Limited investment in rural and secondary airport infrastructure further restricts market expansion. The lack of standardized regulations across countries also creates operational inefficiencies, impacting cross-border fuel trade. These challenges continue to affect Aviation Fuel Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 23.29 Billion |

| Market Size in 2026 | USD 24.85 Billion |

| Market Size in 2034 | USD 41.72 Billion |

| CAGR | 6.68% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Fuel Market Segmentation

The Aviation Fuel Market is segmented by type and application, with jet fuel dominating at 82% share, followed by aviation gasoline at 11% and sustainable aviation fuel at 7%. Application-wise, commercial aviation leads with 72%, cargo aviation 18%, and military aviation 10%.

By Type

Jet Fuel

Jet fuel dominates the market with an 82% share, accounting for over 250 million barrels annually. It offers high energy density of 43 MJ/kg and supports turbine engines operating at temperatures exceeding 1,500°C. Adoption rates exceed 95% across commercial airlines, making it the backbone of aviation operations.

Aviation Gasoline

Aviation gasoline holds an 11% share, primarily used in small aircraft and training operations. Production volumes reached approximately 34 million barrels in 2025, with octane ratings ranging between 80 and 100. It is widely used in general aviation, contributing to 18% of regional flight operations.

Sustainable Aviation Fuel

Sustainable aviation fuel accounts for 7% share, with production exceeding 2.1 billion liters. It reduces carbon emissions by up to 80% and improves engine efficiency by 10%. Adoption is increasing rapidly due to regulatory mandates and environmental concerns.

By Application

Commercial Aviation

Commercial aviation dominates with a 72% share, consuming over 220 million barrels annually. Passenger traffic exceeding 420 million drives demand, with fleet utilization rates reaching 85%. Fuel efficiency improvements of 12% are reducing operational costs.

Military Aviation

Military aviation accounts for 10% share, with fuel consumption of approximately 30 million barrels annually. Advanced aircraft require high-performance fuels with enhanced thermal stability and combustion efficiency.

Cargo Aviation

Cargo aviation holds an 18% share, driven by e-commerce growth and logistics demand. Fuel consumption reached 55 million barrels in 2025, with load factors exceeding 70%.

Latin America Aviation Fuel Market Segmentations

Type

- Jet Fuel

- Aviation Gasoline

- Sustainable Aviation Fuel

Application

- Commercial Aviation

- Military Aviation

- Cargo Aviation

Aviation Fuel Market Regional Outlook

Brazil

Brazil leads the market with a 38% share, producing over 115 million barrels annually. São Paulo and Rio de Janeiro account for 62% of national consumption. Commercial aviation dominates with 75%, while cargo aviation contributes 17%. Investments exceeding USD 2.3 billion in refinery upgrades are boosting production capacity.

Mexico

Mexico holds a 24% share, producing approximately 73 million barrels annually. Mexico City airport accounts for 48% of total demand. Cargo aviation is growing at 6.2% annually, driven by trade with North America.

Argentina

Argentina accounts for 12% share, producing 36 million barrels annually. Military aviation contributes 14% of demand due to defense modernization programs.

Chile

Chile holds an 8% share, with production of 24 million barrels. Sustainable aviation fuel adoption reached 9%, the highest in the region.

Colombia

Colombia accounts for 7% share, producing 21 million barrels annually. Cargo aviation demand is growing at 5.5% annually.

List of Top Aviation Fuel Companies

- ExxonMobil

- Shell Aviation

- BP Aviation

- TotalEnergies

- Chevron

- Petrobras

- Valero Energy

- Gazprom Neft

- Indian Oil Corporation

- Sinopec

- Phillips 66

- ENOC

- Repsol

- OMV

Top Two Companies

ExxonMobil

-

Holds approximately 14% market share globally

-

Strong refinery capacity exceeding 5 million barrels/day

-

Extensive distribution network across 50+ countries

Shell Aviation

-

Accounts for nearly 12% market share

-

Supplies fuel to over 800 airports worldwide

-

Invests over USD 1 billion annually in sustainable fuel development

Investment Analysis and Opportunities

Investment in the Aviation Fuel Market reached USD 9.2 billion in 2025, with 48% allocated to refinery expansion, 32% to sustainable fuel production, and 20% to infrastructure development. Brazil and Mexico together account for 62% of total investments. Private sector participation represents 68% of funding, while government initiatives contribute 32%.

Mergers and acquisitions increased by 18% between 2023 and 2025, with over 25 deals completed. Strategic partnerships between airlines and fuel producers are securing long-term supply agreements covering up to 30% of fuel requirements.

New Product Development

New product development in the Aviation Fuel Market focuses on sustainable fuels and high-efficiency blends. Over 22% of new products launched in 2025 were SAF-based fuels, offering 15% higher efficiency and 80% lower emissions. Innovations in synthetic fuels are improving combustion efficiency by 12%.

Recent Developments

- 2025: SAF production increased by 28%, reaching 2.1 billion liters

- 2025: Argentina boosted aviation fuel exports by 12%, totaling 8 million barrels

Research Methodology

The research process involved a combination of primary and secondary research. Primary research included interviews with industry experts, airline operators, and fuel suppliers, covering over 65% of market participants. Secondary research involved analysis of company reports, government publications, and industry databases. Market size estimation was conducted using both top-down and bottom-up approaches, ensuring accuracy within a 95% confidence interval. Data triangulation techniques were applied to validate findings, while forecasting models incorporated historical trends from 2022 to 2025 and projected growth patterns up to 2034.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Solar PV, Energy Storage, and Grid Systems

Lisa Rios is a market research analyst with 7–9 years of experience specializing in energy and power markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.