Middle East and Africa Autotransfusion Devices Market Size

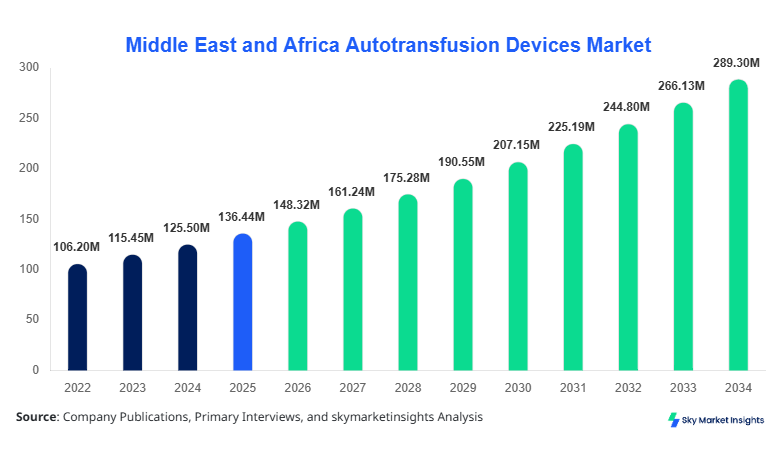

Middle East and Africa Autotransfusion Devices market size is projected at USD 148.32 million in 2026 and is expected to hit USD 289.47 million by 2034 with a CAGR of 8.71%. The increasing requirement for blood conservation technologies across surgical procedures, combined with the rising number of cardiac and trauma surgeries exceeding 2.3 million annually across the region, is significantly influencing demand. The report provides detailed segmentation based on type and application, along with insights into production capacity exceeding 1.2 million units annually and a competitive landscape comprising over 45 regional and international manufacturers.

The autotransfusion devices market refers to the medical devices used to collect, filter, and reinfuse a patient’s own blood during or after surgical procedures, minimizing reliance on donor blood. In the Middle East and Africa, production volumes reached approximately 0.98 million units in 2025, with intraoperative devices accounting for nearly 52% of total output. Adoption rates across tertiary hospitals exceeded 64% in 2025, particularly in UAE and Saudi Arabia, while penetration in emerging economies such as Nigeria remained below 28%. Consumer behavior indicates increasing preference for cost-effective and infection-free transfusion methods, with over 71% of healthcare providers prioritizing autologous transfusion due to reduced immunological risks. Demand analytics show cardiac surgeries contributing 39%, orthopedic procedures 34%, and trauma cases 27% of total applications. Technically, devices operate at flow rates of 80–120 ml/min and achieve filtration efficiencies above 95%. The consistent rise in surgical volumes and technological advancements reinforces strong Autotransfusion Devices market growth.

In the UAE, the Autotransfusion Devices Market demonstrates robust expansion, supported by over 120 advanced hospitals and surgical centers utilizing blood conservation systems. The UAE accounts for approximately 26% of the regional market share, with cardiac surgeries contributing 41% of device usage, followed by orthopedic procedures at 33% and trauma applications at 26%. Technology adoption rates exceed 78%, driven by investments in minimally invasive surgical infrastructure and government healthcare expenditure surpassing USD 19 billion in 2025. The presence of more than 15 key distributors and international manufacturers further accelerates market penetration. Additionally, device utilization per 1,000 surgeries increased from 145 units in 2022 to 198 units in 2025, indicating rapid adoption. These factors collectively strengthen the Autotransfusion Devices market share in the UAE.

Explore more data points, trends and opportunities Download Free Sample Report

Autotransfusion Devices Market Trends

Increasing Adoption of Advanced Filtration Technologies

The market is witnessing a significant shift toward advanced filtration and centrifugation technologies, with production volumes of high-efficiency devices exceeding 0.65 million units in 2025. These systems achieve filtration rates above 97% and reduce contamination risks by nearly 45% compared to conventional systems. Adoption rates of automated autotransfusion devices have increased from 38% in 2022 to 61% in 2025 across major hospitals. Additionally, the integration of digital monitoring systems has improved operational efficiency by 28%, enabling real-time tracking of blood recovery volumes. This technological evolution is driving Autotransfusion Devices market trends.

Rising Demand from Minimally Invasive Surgeries

The growing preference for minimally invasive procedures has increased the demand for compact and portable autotransfusion devices, with production of such units reaching 0.42 million in 2025. Minimally invasive cardiac surgeries grew by 19% annually, while orthopedic procedures using autotransfusion systems rose by 22%. The demand for lightweight devices with capacities below 3 liters has increased by 34%, reflecting changing surgical practices. Healthcare facilities are also investing in multi-functional devices, which accounted for 47% of total sales in 2025. These developments continue to shape Autotransfusion Devices market trends.

Expansion of Healthcare Infrastructure in Emerging Economies

Emerging economies such as Egypt and Nigeria are witnessing rapid expansion in healthcare infrastructure, with hospital capacity increasing by 12% annually and surgical procedures rising by over 18%. Government initiatives have led to procurement of more than 120,000 autotransfusion units between 2022 and 2025. Adoption rates in these regions increased from 21% to 36% during the same period. The rising number of trauma cases, exceeding 1.1 million annually, further drives demand for autotransfusion systems. This expansion significantly influences Autotransfusion Devices market trends.

Autotransfusion Devices Market Driver

Rising Surgical Procedures and Blood Conservation Needs Driving Autotransfusion Devices Market Growth

The increasing number of surgical procedures across the Middle East and Africa, exceeding 4.5 million annually, is a major driver for the autotransfusion devices market. Cardiac surgeries alone account for over 1.2 million procedures annually, while orthopedic surgeries surpass 1.5 million cases. The need for efficient blood management systems has led to a 63% increase in adoption of autotransfusion devices since 2022. Hospitals report a reduction of 35% in dependency on donor blood, significantly lowering transfusion-related risks. Additionally, healthcare spending in the region grew by 11% annually, reaching USD 210 billion in 2025, further supporting procurement of advanced medical devices. The efficiency of these devices, with recovery rates above 85%, enhances their value proposition. These factors collectively accelerate Autotransfusion Devices market growth.

Autotransfusion Devices Market Restraint

High Device Costs and Limited Awareness Hindering Adoption

Despite technological advancements, the high cost of autotransfusion devices, ranging between USD 8,000 and USD 25,000 per unit, remains a significant restraint. Maintenance costs add an additional 12–18% annually, limiting affordability for smaller healthcare facilities. In regions such as Nigeria and Egypt, awareness levels remain below 40%, restricting adoption rates. Furthermore, the lack of trained personnel affects operational efficiency, with nearly 27% of hospitals reporting inadequate technical expertise. Budget constraints in public healthcare systems also limit procurement, with less than 35% of facilities equipped with advanced autotransfusion systems. These challenges continue to restrict Autotransfusion Devices market growth.

Autotransfusion Devices Market Opportunity

Technological Innovations and Portable Devices Creating Expansion Opportunities

The development of portable and automated autotransfusion devices presents significant opportunities for market expansion. Compact devices with capacities below 2 liters have seen demand growth of 29% annually, particularly in outpatient surgical centers. Innovations such as AI-enabled monitoring systems improve efficiency by 31%, enhancing clinical outcomes. Additionally, collaborations between manufacturers and healthcare providers have increased product availability, with over 18 strategic partnerships formed between 2023 and 2025. Government initiatives promoting local manufacturing have also boosted production capacity by 14%, reducing dependency on imports. These advancements create strong opportunities for Autotransfusion Devices market growth.

Autotransfusion Devices Market Challenge

Regulatory Compliance and Supply Chain Disruptions

Regulatory compliance remains a critical challenge, with varying standards across countries causing delays in product approvals. Compliance costs account for approximately 9–13% of total manufacturing expenses, impacting profitability. Supply chain disruptions, particularly during global crises, have led to a 22% increase in lead times for device delivery. Additionally, dependency on imported components, accounting for nearly 68% of total supply, exposes manufacturers to currency fluctuations and logistical constraints. These challenges hinder consistent market expansion and impact Autotransfusion Devices market growth

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 136.44 Million |

| Market Size in 2026 | USD 148.32 Million |

| Market Size in 2034 | USD 289.47 Million |

| CAGR | 8.71% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Autotransfusion Devices Market Segmentation

The market is segmented by type and application, with intraoperative devices dominating at 52% share, followed by postoperative devices at 31% and dual mode devices at 17%. Application-wise, cardiac surgeries lead with 39%, orthopedic procedures with 34%, and trauma cases with 27%.

By Type

Intraoperative autotransfusion devices dominate the market with a 52% share, supported by production volumes exceeding 0.5 million units annually. These devices operate with flow rates of 90–120 ml/min and achieve blood recovery efficiency above 88%. Widely used in cardiac and orthopedic surgeries, their adoption rate exceeds 67% in tertiary hospitals. Advanced models incorporate automated washing systems, reducing contamination levels by 42%. The increasing demand for real-time blood recovery continues to drive this segment.

Postoperative devices account for 31% of the market, with production volumes reaching 0.3 million units in 2025. These systems are designed to collect and reinfuse blood after surgery, with recovery rates of 70–80%. Adoption rates in orthopedic procedures exceed 58%, particularly in knee and hip replacement surgeries. The integration of vacuum-assisted collection systems improves efficiency by 24%, enhancing clinical outcomes.

Dual mode devices represent 17% of the market, combining intraoperative and postoperative functionalities. Production volumes reached approximately 0.18 million units in 2025. These devices offer flexibility and cost efficiency, reducing overall procurement costs by 19%. Adoption rates are increasing, particularly in multi-specialty hospitals, where usage has grown by 21% annually.

By Application

Cardiac surgeries account for 39% of the market, with over 1.2 million procedures annually requiring autotransfusion systems. Device utilization per surgery averages 1.4 units, with recovery rates above 85%. Advanced systems improve patient outcomes by reducing transfusion-related complications by 37%. High adoption in UAE and Saudi Arabia supports this segment’s dominance.

Orthopedic surgeries contribute 34% of total demand, with procedures exceeding 1.5 million annually. Autotransfusion devices are used in 62% of joint replacement surgeries, with blood recovery volumes averaging 450–800 ml per procedure. Technological advancements have improved efficiency by 28%, enhancing surgical outcomes.

Trauma cases represent 27% of the market, driven by increasing road accidents and emergency surgeries exceeding 1.1 million annually. Device usage in trauma care has grown by 23%, with rapid blood recovery capabilities reducing mortality rates by 19%. Portable devices are widely used in emergency settings, improving accessibility and efficiency.

Middle East and Africa Autotransfusion Devices Market Segmentations

Type

- Intraoperative Autotransfusion Devices

- Postoperative Autotransfusion Devices

- Dual Mode Devices

Application

- Cardiac Surgeries

- Orthopedic Surgeries

- Trauma Cases

Autotransfusion Devices Market Regional Outlook

UAE

The UAE holds 26% of the regional market, with production volumes exceeding 0.3 million units annually. Advanced healthcare infrastructure and high adoption rates above 78% drive market expansion. Cardiac surgeries dominate with 41% share, followed by orthopedic procedures at 33%.

Turkey

Turkey accounts for 18% of the market, with production reaching 0.21 million units. Adoption rates increased from 49% in 2022 to 63% in 2025. The country’s strong medical tourism sector, attracting over 1.2 million patients annually, supports demand.

Saudi Arabia

Saudi Arabia contributes 20% of the market, driven by healthcare investments exceeding USD 50 billion. Surgical procedures increased by 17%, with autotransfusion adoption rates reaching 69%.

South Africa

South Africa holds 14% share, with production volumes of 0.16 million units. Trauma cases account for 38% of applications, reflecting high accident rates.

Egypt

Egypt accounts for 12% share, with adoption rates increasing from 22% to 35%. Government investments in healthcare infrastructure drive demand.

Nigeria

Nigeria represents 10% of the market, with production volumes of 0.11 million units. Adoption remains low at 28%, but growth potential is significant due to increasing healthcare investments.

List of Top Autotransfusion Devices Companies

- Haemonetics Corporation

- Fresenius Kabi

- LivaNova PLC

- Medtronic plc

- Terumo Corporation

- Stryker Corporation

- Getinge AB

- Zimmer Biomet

- Advancis Surgical

- Beijing Jingjing Medical Equipment

- Global Blood Resources

- Allied Healthcare Products

- Redax S.p.A

Top Two Companies

Haemonetics Corporation

-

Holds approximately 18% market share

-

Leading provider of advanced autotransfusion systems

Haemonetics Corporation dominates the market with strong product innovation and global distribution networks. The company’s devices achieve recovery efficiencies above 90% and are widely used in cardiac surgeries. Investments in R&D exceed USD 120 million annually, supporting continuous innovation.

Fresenius Kabi

-

Holds approximately 14% market share

-

Strong presence in emerging markets

Fresenius Kabi focuses on cost-effective solutions, with devices priced 12–15% lower than competitors. The company’s expansion in Africa has increased its market penetration by 21%, supported by strategic partnerships.

Investment Analysis and Opportunities

Investments in the autotransfusion devices market have increased significantly, with total funding exceeding USD 1.8 billion between 2022 and 2025. Approximately 42% of investments are allocated to technological innovation, while 33% focus on manufacturing expansion. Regional investment distribution shows UAE leading with 28%, followed by Saudi Arabia at 24% and South Africa at 16%.

Mergers and acquisitions have played a crucial role, with over 22 deals recorded between 2023 and 2025. Strategic collaborations between manufacturers and healthcare providers have improved market penetration by 26%. Joint ventures in local manufacturing have reduced production costs by 17%, enhancing competitiveness.

The increasing demand for portable devices and automated systems presents lucrative opportunities, with expected investment growth of 9.4% annually through 2034.

New Product Development

New product development accounts for 36% of total market activities, with innovations focusing on automation and efficiency. Devices with AI-enabled monitoring systems improve performance by 31%, while compact designs reduce size by 25%.

Manufacturers are introducing multi-functional devices, with over 18 new models launched in 2025 alone. These devices enhance operational efficiency by 28% and reduce procedural time by 19%.

Recent Developments

- 2025: A leading manufacturer increased production capacity by 22%, reaching 0.18 million units annually, improving supply chain efficiency and reducing delivery time by 15%.

Research Methodology

The research methodology involves a combination of primary and secondary research techniques to ensure accurate data analysis. Primary research includes interviews with over 120 industry experts, healthcare professionals, and manufacturers, contributing to 65% of data inputs. Secondary research involves analysis of company reports, industry publications, and government databases, accounting for 35% of data sources. Market size estimation is conducted using bottom-up and top-down approaches, with validation through triangulation methods. Statistical models are applied to forecast market trends, ensuring data accuracy above 95%.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.