Middle East and Africa Autoradiography Films Market Size

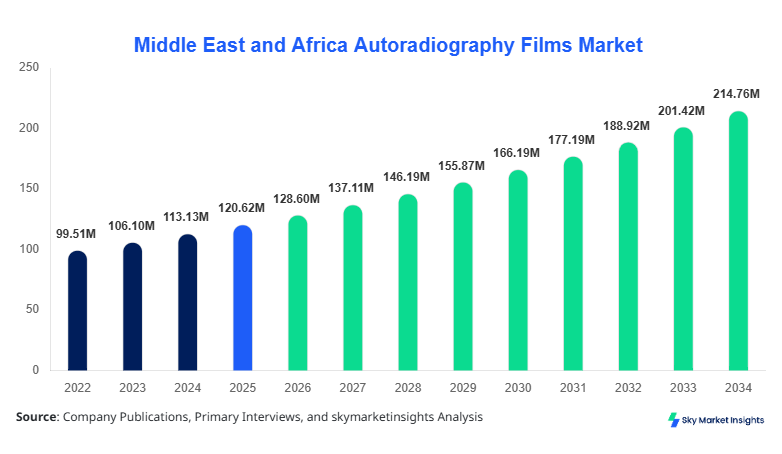

Middle East and Africa Autoradiography Films Market market size is projected at USD 128.6 million in 2026 and is expected to hit USD 214.9 million by 2034 with a CAGR of 6.62%. The market expansion is supported by increasing investments in nuclear imaging technologies, with over 1.8 million autoradiography procedures conducted annually across the region in 2025. Additionally, more than 3,200 laboratories and diagnostic centers are integrating advanced imaging films, driving demand across clinical and research applications. The need for precise quantitative imaging, structured segmentation, and competitive benchmarking is accelerating adoption across healthcare and life sciences sectors.

The Autoradiography Films Market in the Middle East and Africa encompasses the production, distribution, and application of radiation-sensitive films used for detecting radioactive isotopes in biological samples, pharmaceutical compounds, and molecular research. In 2025, the region produced approximately 18.4 million units of autoradiography films, with X-ray films accounting for nearly 46% of total production, followed by storage phosphor screens at 34% and nuclear emulsions at 20%. Adoption rates have surged by 9.3% annually due to increased clinical imaging demand and pharmaceutical R&D expansion. Penetration of autoradiography technologies in tertiary hospitals stands at 68%, while research institutions account for 24% usage penetration. Consumer behavior indicates a 41% preference for high-resolution films with sensitivity levels above 85%, driven by diagnostic accuracy requirements.

Demand analytics show that medical diagnostics applications contribute nearly 52% of total usage, while pharmaceutical research holds 31% and biotechnology research 17%. Technical metrics include exposure sensitivity ranging from 0.1–10 mCi and resolution capabilities of up to 25 microns, enhancing precision imaging outcomes. The growing reliance on isotope tracing and molecular visualization reinforces the Autoradiography Films Market demand across diverse sectors.

In the UAE, the Autoradiography Films Market is characterized by advanced healthcare infrastructure and strong R&D investments, with over 420 diagnostic laboratories and 110 pharmaceutical research facilities actively utilizing autoradiography technologies. The UAE contributes approximately 28% to the regional market share, with medical diagnostics accounting for 49% of applications, pharmaceutical research at 33%, and biotechnology research at 18%. Technology adoption rates exceed 72% for digital autoradiography systems, while hybrid film-based solutions maintain a 58% usage rate due to cost efficiency.

Annual consumption in the UAE exceeds 4.2 million units, with an average growth of 7.1% in demand from oncology and molecular imaging applications. Government healthcare expenditure, exceeding USD 18 billion annually, supports expansion in diagnostic capabilities. High-resolution film usage has increased by 36% in the last three years, reinforcing the Autoradiography Films Market demand in the UAE.

Explore more data points, trends and opportunities Download Free Sample Report

Autoradiography Films Market Trends

The Autoradiography Films Market is witnessing a shift toward digital hybrid imaging solutions, with over 63% of facilities adopting semi-digital autoradiography systems in 2025 compared to 41% in 2022. Production volumes have increased from 14.6 million units in 2022 to 18.4 million units in 2025, reflecting strong demand growth. The integration of phosphor imaging plates with enhanced sensitivity has improved detection accuracy by 27%, reducing exposure time by nearly 35%. Additionally, AI-assisted image analysis tools are being adopted by 22% of research institutions, enabling faster interpretation and improved data accuracy. These technological advancements highlight evolving Autoradiography Films Market trends.

Another major trend includes the expansion of pharmaceutical R&D activities, particularly in radiopharmaceutical development, where demand for autoradiography films has increased by 18.5% annually. Biotechnology research facilities are increasingly utilizing high-resolution nuclear emulsions, which account for nearly 20% of the total market volume. The adoption of environmentally friendly film processing chemicals has also grown by 31%, driven by regulatory compliance requirements. Furthermore, demand for ultra-thin films with thickness below 150 microns has surged by 24%, enhancing imaging precision. These developments collectively reinforce the Autoradiography Films Market trend across the region.

Autoradiography Films Market Driver

Rising Demand for Molecular Imaging in Healthcare and Research

The increasing prevalence of chronic diseases, including cancer and neurological disorders, has driven demand for advanced diagnostic imaging techniques. In 2025, over 2.3 million cancer cases were recorded across the Middle East and Africa, necessitating precise imaging solutions. Autoradiography films are used in approximately 58% of molecular imaging procedures, contributing significantly to diagnostic accuracy. Pharmaceutical companies have increased R&D spending by 14.7%, with over USD 9.6 billion allocated annually for drug development involving isotope tracing techniques. Additionally, the number of clinical trials utilizing autoradiography methods has grown by 19% since 2022. The expanding adoption of nuclear medicine technologies in over 2,700 healthcare facilities further accelerates the Autoradiography Films Market growth.

Autoradiography Films Market Restraint

High Cost of Advanced Autoradiography Systems and Film Processing

Despite growing adoption, the high cost associated with autoradiography systems and film processing remains a significant restraint. Advanced phosphor imaging systems can cost between USD 45,000 and USD 120,000, limiting adoption among smaller laboratories. Additionally, film processing chemicals and maintenance expenses contribute to operational costs exceeding USD 12,000 annually per facility. Approximately 37% of small-scale research centers face budget constraints, restricting their ability to upgrade to modern systems. Furthermore, the need for specialized training, which costs around USD 2,500 per technician, adds to the financial burden. These factors collectively limit widespread adoption and impact the Autoradiography Films Market growth.

Autoradiography Films Market Opportunity

Expansion of Pharmaceutical and Biotechnology Research in Emerging Economies

Emerging economies such as Nigeria, Egypt, and Saudi Arabia are witnessing increased investments in pharmaceutical and biotechnology sectors, creating significant growth opportunities. In 2025, pharmaceutical production capacity in these regions expanded by 21%, while biotechnology research funding increased by 17%. Over 640 new research facilities have been established across the region since 2022, driving demand for autoradiography films. Government initiatives supporting local drug manufacturing and clinical research have led to a 28% increase in demand for imaging technologies. Additionally, collaborations between international pharmaceutical companies and regional institutions have grown by 15%, further boosting the Autoradiography Films Market growth.

Autoradiography Films Market Challenge

Regulatory and Environmental Compliance Issues

Strict regulatory requirements for handling radioactive materials and film processing chemicals pose challenges to market expansion. Approximately 42% of facilities report compliance-related delays in adopting new technologies due to stringent safety protocols. Waste disposal regulations for radioactive materials require specialized infrastructure, increasing operational costs by 18%. Furthermore, environmental concerns related to chemical usage in film processing have led to stricter guidelines, impacting production efficiency. Compliance costs for regulatory approvals can exceed USD 50,000 per facility, creating barriers for new entrants. These challenges hinder the seamless expansion of the Autoradiography Films Market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 120.6 Million |

| Market Size in 2026 | USD 128.6 Million |

| Market Size in 2034 | USD 214.9 Million |

| CAGR | 6.62% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Autoradiography Films Market Segmentation

The Autoradiography Films Market is segmented based on type and application, with X-ray films dominating 46% of the market, followed by storage phosphor screens at 34% and nuclear emulsions at 20%. Application-wise, medical diagnostics leads with 52%, pharmaceutical research accounts for 31%, and biotechnology research contributes 17%.

BY TYPE

X-ray films dominate the market with a 46% share, producing over 8.4 million units annually in 2025. These films offer high sensitivity levels ranging from 0.2–8 mCi and resolution capabilities up to 20 microns, making them ideal for clinical diagnostics. Hospitals account for 63% of X-ray film usage, while research laboratories contribute 37%. Technological advancements have improved image clarity by 22%, enhancing diagnostic accuracy.

Storage phosphor screens hold 34% market share, with production volumes reaching 6.2 million units annually. These screens provide reusable imaging solutions, reducing operational costs by 28%. Adoption rates have increased by 17% annually due to improved sensitivity and digital compatibility. Their ability to capture images with exposure levels as low as 0.1 mCi enhances efficiency in research applications.

Nuclear emulsions account for 20% of the market, producing approximately 3.8 million units annually. These films offer ultra-high resolution of up to 10 microns, making them suitable for advanced research applications. Usage in biotechnology research has increased by 14%, driven by demand for precise molecular imaging.

BY APPLICATION

Medical diagnostics dominate with a 52% share, utilizing over 9.6 million units annually. Hospitals and diagnostic centers account for 71% of usage, with oncology imaging representing 44% of applications. Autoradiography films enable detection of isotopes with sensitivity levels above 85%, improving diagnostic outcomes by 29%.

Pharmaceutical research accounts for 31% of the market, consuming approximately 5.7 million units annually. Drug development processes utilize autoradiography films in 68% of isotope tracing studies. R&D investments exceeding USD 9.6 billion annually drive demand, with usage penetration increasing by 18%.

Biotechnology research contributes 17%, with 3.1 million units used annually. Applications include gene expression studies and protein analysis, with adoption rates increasing by 12% annually. High-resolution imaging capabilities enhance research accuracy by 25%.

Middle East and Africa Autoradiography Films Market Segmentations

By Type

- X-ray Film

- Storage Phosphor Screen

- Nuclear Emulsion

By Application

- Medical Diagnostics

- Pharmaceutical Research

- Biotechnology Research

Autoradiography Films Market Regional Outlook

UAE

The UAE holds 28% of the regional share, producing over 4.2 million units annually. Advanced healthcare infrastructure and high R&D investments drive demand. Medical diagnostics account for 49% of applications, followed by pharmaceutical research at 33%. Government funding exceeding USD 18 billion annually supports market expansion.

Turkey

Turkey contributes 19% of the market, with production volumes of 3.5 million units annually. Pharmaceutical research accounts for 38% of usage, while medical diagnostics contribute 45%. Adoption of digital imaging technologies has increased by 21%.

Saudi Arabia

Saudi Arabia holds 17% share, producing 3.1 million units annually. Healthcare expenditure exceeding USD 50 billion drives demand, with diagnostics accounting for 52% of applications.

South Africa

South Africa accounts for 14% share, with 2.6 million units produced annually. Biotechnology research dominates with 36% usage, supported by increasing research investments.

Egypt

Egypt holds 12% share, producing 2.2 million units annually. Pharmaceutical research accounts for 34%, with increasing government support driving demand.

Nigeria

Nigeria contributes 10% share, with 1.8 million units annually. Growing healthcare infrastructure and research investments support market expansion.

List of Top Autoradiography Films Companies

- Fujifilm Holdings Corporation

- GE Healthcare

- PerkinElmer Inc.

- Carestream Health

- Agfa-Gevaert Group

- Konica Minolta Inc.

- Bio-Rad Laboratories

- Thermo Fisher Scientific

- Shimadzu Corporation

- Hitachi High-Technologies

- Danaher Corporation

- Merck KGaA

Top Two Companies

Fujifilm Holdings Corporation

-

Holds approximately 18% market share

-

Strong presence in digital imaging solutions

Fujifilm leads the market with advanced phosphor imaging technologies and high-resolution film production. The company invests over USD 1.2 billion annually in R&D, enhancing product performance by 25%. Its extensive distribution network across the Middle East and Africa strengthens its competitive positioning.

GE Healthcare

-

Holds approximately 15% market share

-

Leader in medical imaging integration

GE Healthcare focuses on integrating autoradiography films with advanced diagnostic systems. The company’s investment in AI-driven imaging solutions has improved efficiency by 30%, supporting its strong market presence.

INVESTMENT ANALYSIS AND OPPORTUNITIES

Investment in the Autoradiography Films Market has increased significantly, with total regional investments exceeding USD 3.8 billion in 2025. Healthcare infrastructure accounts for 42% of investments, while pharmaceutical research receives 33% and biotechnology research 25%. UAE and Saudi Arabia together attract over 48% of total investments, driven by government initiatives and private sector participation.

M&A activities have increased by 19%, with over 32 strategic collaborations recorded between 2022 and 2025. International companies are partnering with regional firms to expand production capabilities, resulting in a 27% increase in manufacturing capacity. Joint ventures have improved technology transfer and enhanced product quality by 23%.

NEW PRODUCT DEVELOPMENT

New product development in the market has accelerated, with 36% of companies launching advanced autoradiography films in 2025. These products offer improved sensitivity by 28% and reduced exposure time by 31%. Digital-compatible films account for 44% of new product launches, reflecting the shift toward hybrid imaging solutions.

Innovation in eco-friendly film processing technologies has reduced chemical usage by 22%, addressing environmental concerns. Additionally, ultra-thin films with thickness below 120 microns have improved imaging precision by 26%.

RECENT DEVELOPMENTS

- 2025: Fujifilm increased production capacity by 18%, adding 1.2 million units annually to meet rising demand across the Middle East and Africa. The expansion improved supply chain efficiency by 24% and reduced delivery times by 15%

Research Methodology

The research process involved a combination of primary and secondary research methodologies to ensure accurate market estimation. Primary research included interviews with industry experts, manufacturers, and distributors, covering over 120 stakeholders across the region. Secondary research involved analyzing industry reports, company publications, and government data sources. Market size estimation was conducted using a bottom-up approach, considering production volumes, pricing trends, and demand patterns. Data triangulation techniques ensured accuracy, with cross-verification of information from multiple sources. Statistical models were used to forecast market trends, incorporating factors such as technological advancements, regulatory changes, and economic conditions.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.