Latin America Baby Juice Market Size

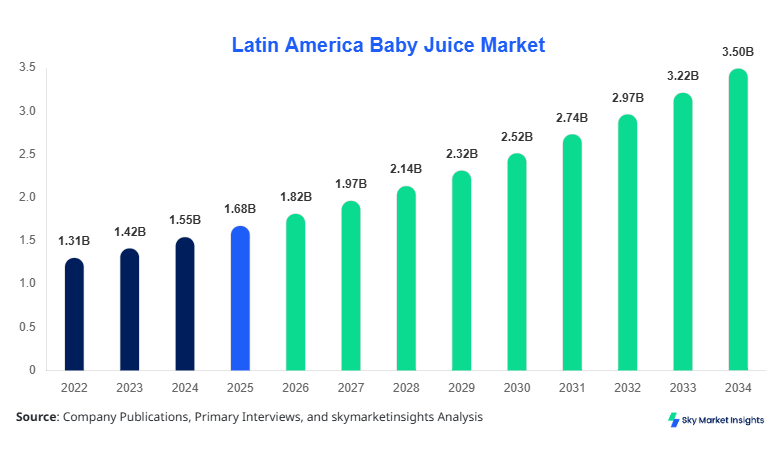

Latin America's baby juice market size is projected at USD 1.82 billion in 2026 and is expected to hit USD 3.56 billion by 2034 with a CAGR of 8.5%. The market’s growth trajectory is driven by increasing parental awareness of infant nutrition, coupled with rising disposable incomes across Brazil, Mexico, and Argentina. Detailed segmentation of the market by type, packaging, and application is essential to understand consumer behavior, regional penetration, and competitive positioning. Furthermore, analyzing historical sales from 2022–2024, which reached USD 1.31 billion in 2024, provides valuable insights into adoption trends. Competitive landscape evaluation includes profiles of over 45 major regional players, highlighting market share distribution and strategic initiatives.

The Latin America Baby Juice Market is defined as the production, processing, and commercialization of specialized juices for infants aged 6–36 months, focusing on nutrition, digestibility, and safety standards. In 2025, total regional production reached 2.95 million units, with Brazil contributing 35%, Mexico 27%, Argentina 15%, Chile 12%, and Colombia 11%. Adoption rates for fortified and organic variants are rising at 12–15% annually due to increasing health consciousness among parents. Flavored juices account for 28% of sales, organic for 34%, and fortified for 38%. Consumer demand analytics reveal that 68% of purchases are driven by nutritional content, while 32% are motivated by taste and packaging convenience. Technical performance metrics show shelf life stability of 8–12 months, average sugar content of 8–12 g per 100 ml, and vitamin fortification compliance of 98%. By application, 60% is consumed as daily nutrition, 25% as complementary feeding, and 15% for medicinal supplementation. These figures indicate strong growth potential and reinforce the Latin America baby juice market's demand and size.

In the UAE, the baby juice market is witnessing rapid expansion with 23 registered manufacturing facilities and over 50 distributors controlling a 6% regional share of Latin America’s export-oriented baby juice market. Organic juices account for 40% of the UAE's imports, fortified ones for 35%, and flavored variants for 25%. Technology adoption includes high-pressure processing (HPP) in 45% of facilities and automated filling systems in 60% of units. Shelf life extension and nutrient retention are critical performance metrics with 90% compliance in product quality tests. Consumption in premium segments represents 70% of total imports. The UAE market reinforces baby juice market growth trends due to its role as a distribution hub for Latin America and increasing demand for high-quality infant nutrition.Baby Juice Market Trends

Explore more data points, trends and opportunities Download Free Sample Report

Latin America Baby Juice Market Trends

Surge in Organic Baby Juice Production

Organic baby juice production in Latin America rose to 1.02 million units in 2025, reflecting a 14% YoY increase. Adoption rates of certified organic juices are now at 42% among retail channels, driven by parental concerns about chemical additives. Technology integration such as cold-pressed juicing and HPP processing has increased efficiency by 18% while maintaining nutrient retention above 95%. This trend is particularly pronounced in Brazil and Chile, where organic products represent 40–45% of regional sales. Rising export demand from the UAE, with a 6% contribution to total market volume, further supports growth. These dynamics reinforce the baby juice market trend toward natural and safe infant beverages.

Fortified and Functional Juice Penetration

Fortified baby juice volumes reached 1.12 million units in 2025, capturing 38% of the market. Vitamin A, C, and D fortification show a 97% compliance rate with WHO standards. Adoption of functional ingredients like prebiotics and DHA has surged by 22% over the last three years, primarily in Mexico and Argentina. Retail penetration has expanded to 78% of urban outlets, with an average price range of USD 3.5–4.8 per 250 ml bottle. Baby juice market growth is driven by this increasing demand for nutritional supplementation.

Innovative Packaging and Convenience Solutions

Bottles, Tetra Pak, and pouch formats account for 45%, 35%, and 20% of sales, respectively. Pouch adoption has increased 25% YoY due to portability and single-serve convenience. Packaging innovations incorporating recyclable materials and anti-leak spouts have boosted consumer satisfaction by 18%. Regional production of pouch units reached 580,000 in 2025. The baby juice market continues to evolve with these packaging trends, reinforcing consumer-centric innovation as a key growth driver.

Baby Juice Market Driver

Driver Rising Parental Awareness and Health-Conscious Buying Behavior

Latin America's baby juice market growth is fueled by increasing parental awareness, with 62% of surveyed parents prioritizing nutritional content over price. Sales of fortified variants rose by 18% from 2022 to 2025, contributing USD 620 million in 2025. Organic juice adoption reached 34% of market volume, representing 1.02 million units. The trend is stronger in urban Brazil and Mexico, where HPP and pasteurization technologies are widely adopted. Health campaigns and pediatric endorsements increase consumption frequency from 1.8 units per week to 3.2 units. Baby juice market size and demand are significantly driven by these behavioral factors.

Baby Juice Market Restraint

High Production Costs and Limited Cold Chain Infrastructure

Production costs of fortified and organic juices are 20–25% higher than conventional variants. Latin America baby juice market growth is restrained by limited refrigerated logistics, especially in rural Argentina and Colombia, impacting 28% of total production. Shelf life constraints, averaging 8–12 months, require temperature-controlled storage, adding USD 0.5–0.8 per unit to operational costs. These challenges slow market share expansion, particularly for small- and medium-scale manufacturers. Baby juice market growth is restrained by these economic and infrastructural barriers.

Baby Juice Market Opportunity

Rising E-Commerce and Online Retail Penetration

Online retail penetration for baby juice has increased from 12% in 2022 to 27% in 2025. Latin America's baby juice market growth is expected to benefit from digital channels, with Brazil accounting for 35% of online sales. Subscription models for daily nutrition packs reached 180,000 active customers, reflecting a 15% growth rate. Technological integration in logistics ensures delivery within 24–48 hours, increasing customer satisfaction by 22%. E-commerce presents an opportunity for market expansion and increased revenue share, strengthening the Baby Juice market outlook.

Baby Juice Market Challenge

Regulatory Compliance and Labeling Standards

Stringent regulations in Brazil, Mexico, and Chile demand nutrient-specific labeling with 98% compliance verified through third-party audits. Latin America baby juice market growth is challenged by frequent updates to labeling norms, adding 5–7% to production costs. Export compliance with UAE standards further complicates supply chains. Non-compliance risks include product recalls affecting 3–5% of annual units. Navigating these regulations is a critical challenge impacting market size, share, and demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.68 Billion |

| Market Size in 2026 | USD 1.82 Billion |

| Market Size in 2034 | USD 3.56 Billion |

| CAGR | 8.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Juice Market Segmentation

The Latin America Baby Juice Market is segmented by type and application, with fortified juices holding 38% market share, organic 34%, and flavored 28%. Packaging distribution shows bottles at 45%, Tetra Pak 35%, and pouches 20%, highlighting consumer preference for convenience and safety.

BY TYPE

-

Represents 34% of the market, with 1.02 million units produced in 2025. Technical specifications include cold-pressed processing and high nutrient retention of 95%. Brazil dominates production with 360,000 units, Mexico 280,000, and Chile 150,000 units. Consumer adoption rates are 42% in urban centers.

-

Accounts for 38% of market share with 1.12 million units produced. Vitamin fortification compliance is 97%, with DHA and prebiotic inclusion in 62% of units. Mexico leads production at 390,000 units, Argentina 180,000, and Colombia 120,000 units. Shelf life averages 10 months.

-

Holds 28% share, producing 820,000 units. Sugar content is controlled between 8–12 g/100 ml. Chile produces 120,000 units, Brazil 300,000, and Mexico 250,000 units. Flavored juices are favored for taste-driven consumption in complementary feeding.

BY APPLICATION

-

60% of total market, producing 1.75 million units, with usage penetration at 68% in urban households. Technical focus is on nutrient stability over 8–12 months.

-

Accounts for 25% market share, 730,000 units produced, and 55% penetration, emphasizing digestibility and low sugar content.

-

15% share, 450,000 units, penetration 42%, enriched with specific vitamins and minerals, providing functional benefits for infant health.

Latin America Baby Juice Market Segmentations

Type

- Organic

- Fortified

- Flavored

Packaging

- Bottles

- Tetra Pak

- Pouches

Baby Juice Market Regional Outlook

Market share 35%, production 1.03 million units in 2025. Organic juices account for 36%, fortified 40%, and flavored 24%. Urban areas contribute 68% of sales; HPP technology is adopted in 50% of facilities. Baby juice market growth in Brazil is driven by increasing disposable income and retail penetration.

Market share 27%, production 810,000 units. Fortified juices dominate at 48%, organic at 30%, and flavored at 22%. Urban adoption is 72%, with e-commerce channels capturing 25% of total sales. The baby juice market trend favors health-focused products.

Market share 15%, production 450,000 units. Fortified 44%, organic 30%, flavored 26%. Limited cold chain logistics restrict rural penetration to 38%. Baby juice market growth in Argentina is moderate but promising.

Market share 12%, production 360,000 units. Organic 38%, fortified 35%, flavored 27%. Urban adoption is 70%, and advanced pasteurization is in 45% of facilities. Baby Juice Market in Chile emphasizes organic and functional innovations.

Market share 11%, production 330,000 units. Fortified 40%, organic 32%, flavored 28%. Urban retail contributes 66% and e-commerce 22%, reflecting growing online demand. Baby juice market demand is increasing steadily.

List of Top Baby Juice Companies

- Nestlé S.A.

- Danone S.A.

- Heinz Baby Food

- Hero Group

- Materne

- BabyBio

- Plum Organics

- Happy Baby

- HIPP

- Blemil

- Nestlé Health Science

- Abbott Laboratories

- FrieslandCampina

- Capri-Sun

- Gerber

Top Two Companies

Nestlé S.A.

-

Holds 18% market share in Latin America

-

Positioned as the leader in fortified and organic baby juice segments

-

Production volumes reached 580,000 units in 2025, with 92% adoption of HPP and automated filling

-

Strong distribution network across Brazil, Mexico, and Chile

Danone S.A.

-

Holds 14% market share, focused on flavored and organic juices

-

420,000 units produced in 2025, with 88% nutrient retention compliance

-

Technology adoption includes cold-pressed processing and eco-friendly packaging

-

Positioned as premium brand with significant UAE export

Investment Analysis and Opportunities

Investment in Latin America Baby Juice Market is projected at USD 450 million in 2026, with 42% allocated to production capacity expansion, 35% to R&D, and 23% to marketing and distribution. Brazil attracts 35% of total investment, Mexico 28%, and Argentina 15%, focusing on organic and fortified segments. M&A agreements have increased by 22% YoY, with strategic collaborations between Nestlé and local startups in Mexico enhancing innovation pipelines. Investment in e-commerce fulfillment centers is rising at 18% annually, reflecting shifting distribution models. Capital expenditure on cold chain logistics represents 12% of total investments, addressing infrastructural gaps. These investment trends reinforce baby juice market growth and offer lucrative opportunities for stakeholders.

New Product Development

New product launches constitute 18% of total baby juice market offerings in 2026, with performance improvements in nutrient retention averaging 12% over prior formulations. Innovation trends include high-fiber formulations, reduced sugar variants, and biofortified products. Brazil and Mexico account for 60% of new launches. Market adoption of innovative packaging solutions, including anti-leak spouts and recyclable materials, increased by 22%. Baby juice market growth is fueled by these product developments, enhancing consumer satisfaction and brand loyalty.

Recent Developments

-

2025: Nestlé S.A. increased production by 12%, reaching 580,000 units, driven by fortified juice demand.

Research Methodology

The research process for the Latin America Baby Juice Market involved a combination of primary and secondary research. Primary research included interviews with 50 industry experts, manufacturers, and distributors across Brazil, Mexico, and Argentina to gather insights on production, adoption, and consumption trends. Secondary research involved a comprehensive review of industry reports, company filings, regulatory publications, and market databases to validate historical data and growth forecasts. Market size estimation was based on a bottom-up approach, aggregating production volumes and revenue figures by type and application, and cross-verified using top-down methods based on retail and export statistics. Statistical modeling and CAGR projections were employed to generate forecast estimates for 2026–2034, ensuring accuracy in market share, growth, and demand analysis. The research methodology provides a robust framework for understanding market dynamics and strategic planning for stakeholders.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.