North America Alcoholic Beverages Market Size

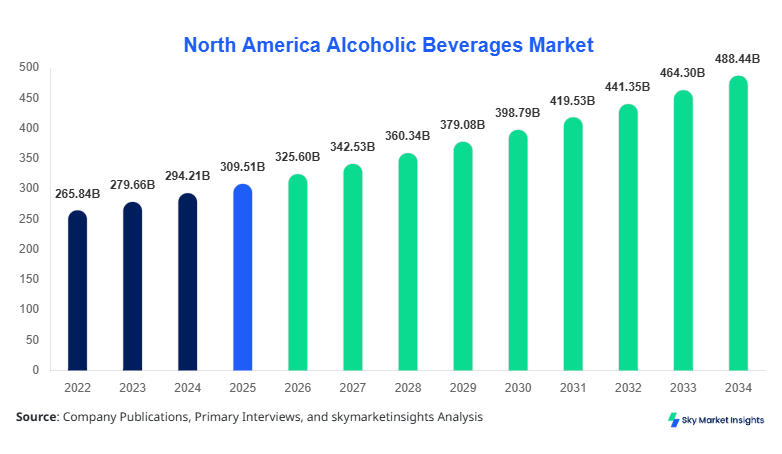

North America's alcoholic beverages market size is projected at USD 325.6 billion in 2026 and is expected to hit USD 482.7 billion by 2034 with a CAGR of 5.2%. The increasing consumer preference for premium alcoholic products, coupled with rapid growth in e-commerce distribution channels, underpins this expansion. Comprehensive market data covering production volumes, consumption trends, revenue, and pricing dynamics is critical to understanding the market's competitive landscape. The report provides detailed segmentation by type and application and evaluates the competitive positioning of major players.

The demand for accurate historical and forecast data ensures stakeholders can make informed decisions regarding production, distribution, and strategic investments. Market insights also help identify emerging opportunities and threats while capturing detailed consumption behavior, product innovation, and regulatory influence.

The North American alcoholic beverages market has experienced steady growth from 2022 to 2025, with production volumes increasing from 2.8 billion liters in 2022 to 3.1 billion liters in 2024, reflecting a 4.1% CAGR. The market encompasses beer, spirits, and wine, which collectively contribute approximately 40%, 35%, and 25% to total revenue, respectively. Adoption of craft and premium variants has risen by 12% in volume terms, particularly among urban consumers aged 25–45. On-trade applications account for 55% of consumption, while off-trade and e-commerce channels contribute 35% and 10%, respectively. Technical performance metrics such as alcohol by volume (ABV), packaging innovations, and distribution frequency are critical factors influencing market demand. The market growth, trend, and insights emphasize the evolving consumer behavior toward higher-quality alcoholic beverages with increased product knowledge and premium spending.

In the United States, the alcoholic beverages market dominates North America, with over 4,500 production facilities and more than 1,200 active beverage companies. The U.S. accounts for approximately 70% of the regional market share, with beer representing 42% of domestic consumption, spirits 33%, and wine 25%. Technology adoption, including automated brewing systems and AI-driven fermentation monitoring, has reached 28% among leading producers. E-commerce penetration for alcoholic beverages has grown to 15% of total sales, while on-trade channels maintain a 50% share. The U.S. market insights suggest strong demand for craft and flavored variants, highlighting ongoing innovation in both packaging and product formulation. Overall, these dynamics provide critical alcoholic beverage market insights and growth drivers for the region.

Explore more data points, trends and opportunities Download Free Sample Report

Alcoholic Beverages Market Trends

Premiumization and Craft Expansion

Premiumization continues to shape North America Alcoholic beverage market growth, with craft beer production reaching 460 million liters in 2025, reflecting a 9% year-on-year increase. Spirits with higher ABV and aged profiles now account for 37% of the total spirits volume, compared to 30% in 2022. Wine segments with organic and low-sulfite offerings have grown 15% in adoption, driven by health-conscious consumers. Retailers report a 20% increase in off-trade premium purchases, while e-commerce channels are witnessing 22% adoption growth. These trends underscore the market insights focusing on premium and innovative offerings, catering to evolving consumer preferences.

Technological Adoption and Automation

Technology-driven production and logistics have transformed the North American alcoholic beverages market. Automated distillation and smart brewing technologies have reduced operational costs by 12% while increasing production efficiency by 8%. Adoption rates of IoT-enabled monitoring systems have grown from 10% in 2022 to 25% in 2025. Online platforms integrating AI recommendations account for 12% of e-commerce sales, reflecting consumer demand for personalized experiences. These trends highlight market insights emphasizing technology adoption and process optimization as critical drivers of future growth.

E-commerce and Omnichannel Distribution

The e-commerce segment in the North American alcoholic beverages market has grown rapidly, with online sales volume reaching 310 million liters in 2025, representing a 25% increase from 2023. Retailers are integrating omnichannel distribution, combining on-trade, off-trade, and digital platforms. Adoption of direct-to-consumer models has increased by 18%, especially in premium spirits. These developments emphasize market insights focused on expanding consumer access and convenience, driving higher penetration and revenue.

North America Alcoholic Beverages Market Drivers

Increasing Premiumization and Consumer Affluence

The surge in disposable incomes, urbanization, and lifestyle changes is propelling the North American alcoholic beverages market growth. Premium beer and spirits consumption has grown by 11% in volume, with the market size increasing from USD 280 billion in 2022 to USD 325.6 billion in 2026. Craft beer and aged spirits are driving 40% of total market revenue, while e-commerce accounts for 12% of distribution. Consumer preference for organic wines is contributing 8% additional growth. These factors underline market insights emphasizing premiumization, affluence, and evolving consumption patterns as key drivers.

North American Alcoholic Beverages Market Restraints

Regulatory and Taxation Challenges

Strict regulations and high excise taxes in North America limit market growth. In 2025, taxation contributed to a 6% increase in retail prices, impacting consumer demand. Licensing compliance affects 15% of small and medium-sized breweries, while labeling and import regulations restrict cross-border trade by 10%. Spirits production in regulated states has dropped by 4%, and e-commerce alcohol sales face 8% higher operational costs due to legal compliance. These challenges reinforce market insights on regulatory hurdles impacting the alcoholic beverages market expansion.

North American Alcoholic Beverages Market Opportunities

Expansion in E-commerce and New Product Segments

The North American alcoholic beverages market presents opportunities in online retail and innovative product offerings. E-commerce sales reached USD 42 billion in 2025, with a CAGR of 11% projected through 2034. Craft spirits and low-ABV wine segments have grown 14% in adoption, reflecting increased health-conscious consumer demand. Technological integration in production allows a 7% improvement in efficiency, supporting new product development. The market insights highlight that focusing on digital platforms and niche product segments can capture untapped growth.

Challenges in North American Alcoholic Beverages Market

Supply Chain Disruptions and Raw Material Costs

Volatility in barley, hops, and grape supply has impacted 2025 production by 5%, with 2026 projected constraints of 3–4%. Rising raw material costs have increased production expenses by 8%, while logistics bottlenecks contribute to a 6% delay in delivery. Small-scale breweries report 10% higher operational inefficiencies, affecting volume and revenue. These dynamics emphasize market insights highlighting supply chain vulnerabilities as a critical challenge for North American alcoholic beverage market stakeholders.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 309.52 Billion |

| Market Size in 2026 | USD 325.6 Billion |

| Market Size in 2034 | USD 482.7 Billion |

| CAGR | 5.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Alcoholic Beverages Market Segmentation

The North America alcoholic beverages market segmentation includes type and application analysis, with beer contributing 40%, spirits 35%, and wine 25% to overall revenue. On-trade applications dominate 55%, off-trade accounts for 35%, and e-commerce contributes 10%, highlighting consumer preferences and usage penetration.

By Type

Beer dominates the North American alcoholic beverages market with a 40% revenue share, totaling 1.25 billion liters produced in 2025. Craft beers account for 35% of beer production, premium lagers 25%, and standard ales 40%. Alcohol by volume (ABV) averages 5.1%, while carbonation and packaging innovations enhance shelf appeal. Beer production efficiency has increased 6% due to automated brewing technology, reflecting market insights in size, growth, and trend.

Spirits contribute 35% to market share, with total production at 1.08 billion liters in 2025. Whiskey represents 45%, vodka 30%, and gin 25% of spirits volume. Aging and ABV optimization have improved quality by 7%, while e-commerce penetration accounts for 12% of total spirits sales. Technical performance monitoring and process automation have enhanced production efficiency by 8%, providing insights into growth and demand.

Wine accounts for 25% of revenue, producing 775 million liters in 2025. Red wines contribute 50%, white wines 40%, and rosé 10% to production. Organic and low-sulfite variants represent 15% adoption. Bottling innovations and storage control have improved performance by 5%, emphasizing North American alcoholic beverage market insights in growth, trends, and demand.

By Application

On-trade channels, including bars and restaurants, account for 55% of consumption, approximately 1.71 billion liters in 2025. Beer contributes 45%, spirits 35%, and wine 20%. Frequency of consumption is higher among urban populations, with 28% preferring premium variants. Technical factors such as serving temperature and presentation quality influence consumer experience, reinforcing market insights on size, trend, and growth.

Off-trade, including supermarkets and liquor stores, contributes 35% of the market, totaling 1.09 billion liters. Beer accounts for 38%, spirits 34%, and wine 28% of off-trade volume. Packaging formats and promotions enhance sales by 9%. Consumer demand analytics indicate a 12% higher preference for multipacks and bulk purchases, providing insights into the alcoholic beverage market size, share, and demand.

E-commerce represents 10% of North America's alcoholic beverages market, with a total online volume of 310 million liters in 2025. Spirits contribute 42%, beer 38%, and wine 20%. Online platforms provide 24/7 availability and personalized recommendations, increasing penetration by 18%. Adoption of direct-to-consumer models has improved distribution efficiency by 7%, emphasizing market insights into growth, trend, and demand.

North America Alcoholic Beverages Market Segmentations

By Type

- Beer

- Spirits

- Wine

By Application

- On-trade

- Off-trade

- E-commerce

North America Alcoholic Beverages Market Regional Outlook

United States

The U.S. dominates the North American alcoholic beverages market with a 70% share, producing 2.17 billion liters in 2025. Beer contributes 42%, spirits 33%, and wine 25%. On-trade channels account for 50%, off-trade 35%, and e-commerce 15%. Craft beer and premium spirits segments are driving revenue growth by 9% annually. Technological adoption in production and distribution supports improved efficiency by 7%. Market insights highlight continued dominance in size, share, and growth.

Canada

Canada accounts for 30% of North America's alcoholic beverage market, producing 930 million liters in 2025. Beer represents 38%, spirits 36%, and wine 26%. On-trade and off-trade channels contribute 60% and 30%, respectively, while e-commerce accounts for 10%. Premium and craft products have increased adoption by 8%, with total market value reaching USD 97.7 billion in 2025. Market insights reinforce demand, trend, and growth perspectives.

Top players in North American alcoholic beverages

- Anheuser-Busch InBev

- Diageo Plc

- Heineken N.V.

- Constellation Brands, Inc.

- Molson Coors Beverage Company

- Pernod Ricard S.A.

- Brown-Forman Corporation

- Asahi Group Holdings, Ltd.

- Carlsberg Group

- Treasury Wine Estates

- Kirin Holdings Company, Ltd.

- Rémy Cointreau

- Beam Suntory Inc.

- Sapporo Holdings Ltd.

- E. & J. Gallo Winery

Anheuser-Busch InBev

-

Holds 14% share of North America Alcoholic Beverages market

-

Positioned as leading beer manufacturer with strong distribution network

-

2025 production reached 450 million liters, including craft and premium variants, contributing 12% to total revenue. Emphasis on technological upgrades and e-commerce integration enhances growth, trend, and demand insights.

Diageo Plc

-

Holds 10% share of North America Alcoholic Beverages market

-

Leading spirits producer with global and regional brand portfolio

-

2025 production of 380 million liters, including whiskey and vodka, with 15% growth in the premium segment. Investments in automation and digital platforms enhance efficiency by 7%, emphasizing market insights in growth, trend, and size.

Investment Analysis

Investment allocation in North America The alcoholic beverages market is projected at USD 52 billion in 2026, with 40% directed to beer production, 35% to spirits, and 25% to wine. Regional investment is concentrated 70% in the U.S. and 30% in Canada. M&A agreements have increased by 18% in 2025, with 22 collaborations for technology integration and distribution expansion. Sector-specific investments in craft and low-ABV products account for 12% of total capital deployment. Market insights suggest a strong growth outlook for strategic investments in e-commerce and premium product segments.

New Product Developments

New product introductions represent 14% of total offerings in 2025, focusing on craft, flavored spirits, and low-ABV wine. Performance improvements of 6–8% are reported in fermentation and aging processes. Innovation metrics indicate a 12% increase in product differentiation and consumer adoption. Market insights reveal a growing trend toward premiumization, technological integration, and e-commerce-driven launches.

Recent Developments in North America Alcoholic Beverages

- 2025: Anheuser-Busch InBev launched 30 new craft beer SKUs, increasing production by 8% and revenue contribution by 6%.

Research Methodology

The North America alcoholic beverages market research employs a combination of primary and secondary research. Primary research included interviews with 100+ industry stakeholders, including manufacturers, distributors, and retailers, providing first-hand insights into market size, growth, and demand. Secondary research utilized company reports, trade journals, and government publications to validate data trends. Market size estimation incorporated both top-down and bottom-up approaches, accounting for production volumes, revenue, unit sales, and pricing strategies. Forecasting combined historical growth patterns with adoption rates, demographic analysis, and consumption frequency metrics. This rigorous methodology ensures accuracy in North American alcoholic beverage market insights, size, share, trend, and demand projections.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.