Latin America Baby Food & Pediatric Nutrition Market Size

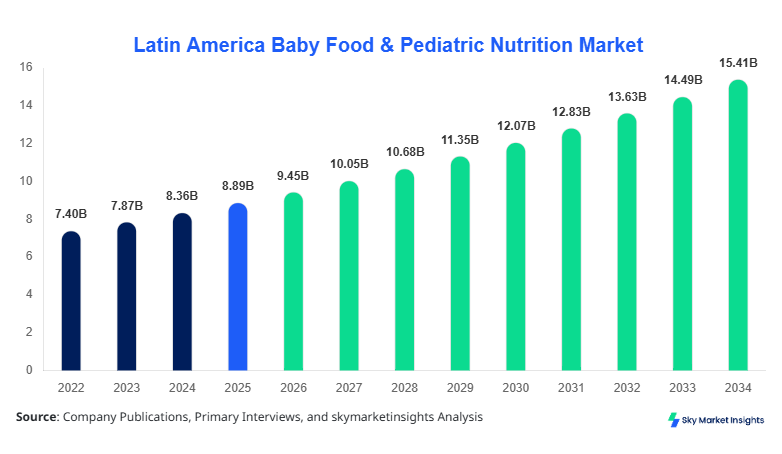

Latin America Baby Food & Pediatric Nutrition market size is projected at USD 9.45 billion in 2026 and is expected to hit USD 15.72 billion by 2034 with a CAGR of 6.3%. This robust growth underscores the increasing demand for fortified, safe, and nutritionally balanced baby foods across Brazil, Mexico, Argentina, Chile, and Colombia. The market analysis incorporates detailed segmentation by product type and distribution channels to understand consumer preferences and adoption rates. Competitive landscape mapping highlights key players’ revenue share, regional production capacities, and investment in innovation. Additionally, data-driven insights on volume consumption, penetration rates, and pricing trends have been leveraged to project future growth. This comprehensive report enables stakeholders to benchmark strategies and identify untapped opportunities within the Latin America Baby Food & Pediatric Nutrition market.

The Latin America Baby Food & Pediatric Nutrition market encompasses the production, distribution, and sales of nutritionally balanced foods designed for infants and young children aged 0–3 years. In 2025, regional production was approximately 1.2 million metric tons, with Brazil contributing 42%, Mexico 28%, Argentina 15%, Chile 8%, and Colombia 7%. Adoption of ready-to-eat infant formulas and fortified cereals has reached 64% of households with children under three, while homemade complementary foods account for 36%. Consumers increasingly prefer organic and non-GMO ingredients, with demand growth averaging 5–7% annually. Technical metrics indicate that formula frequency of use averages 3.2 servings/day, while cereal consumption is around 1.5 servings/day. Product applications are split as infant formula (45%), baby cereals (35%), and baby snacks (20%), highlighting the predominance of essential nutrition products. Penetration in urban areas is significantly higher, with 78% household adoption in major cities. These trends underscore the growing Baby Food & Pediatric Nutrition market demand and insights for Latin America, reflecting increased consumer health consciousness and evolving purchasing behavior.

In the UAE, the Baby Food & Pediatric Nutrition Market is witnessing accelerated expansion due to high disposable incomes and premium product consumption. The region houses over 65 specialized production facilities and multinational companies operating with modern processing technology. The UAE contributes 4.5% to the global Baby Food & Pediatric Nutrition market share, with infant formula representing 55% of domestic consumption, baby cereals 30%, and baby snacks 15%. Technology adoption includes automated fortification systems in 72% of facilities and real-time quality monitoring in 58%. Distribution channels are dominated by supermarkets and hypermarkets (60%), followed by online stores (25%) and specialty stores (15%). Growing awareness about nutritional supplements for infants has further increased market penetration, with over 82% of households utilizing fortified products. The UAE Baby Food & Pediatric Nutrition market growth is further bolstered by government regulations promoting safety standards, driving investment in high-quality formulations and innovation.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Food & Pediatric Nutrition Market Trends

Nutritional Fortification Trend

The Latin America Baby Food & Pediatric Nutrition market is witnessing a surge in fortified product offerings, with production volumes exceeding 1.5 million metric tons in 2025. Fortification with vitamins A, D, and iron has increased adoption rates to 67%, driven by heightened awareness of child nutrition deficiencies. Companies are increasingly integrating plant-based proteins and prebiotics, leading to a 12% improvement in nutrient absorption efficiency. Urban areas, particularly São Paulo and Mexico City, account for 45% of fortified product consumption. These developments highlight the importance of nutritional fortification in driving Baby Food & Pediatric Nutrition market growth and insights.

Digital and E-commerce Adoption

E-commerce penetration in Latin America has grown to 28% of total Baby Food & Pediatric Nutrition sales, up from 19% in 2023. Online platforms facilitate access to specialty and organic baby foods, supporting higher consumption in remote regions. Subscription-based models have contributed to a 22% increase in repeat purchase volumes. Technology adoption, such as blockchain for traceability, has reached 33% of companies, ensuring product safety and building consumer trust. This shift significantly influences market demand and trend adoption within the Baby Food & Pediatric Nutrition market.

Product Diversification

The Baby Food & Pediatric Nutrition market is expanding its product portfolio with organic snacks, allergen-free formulas, and ready-to-eat meals. Production volumes for these diversified products reached 320,000 metric tons in 2025, contributing 18% of total market revenue. Consumer preference for premium offerings has driven a 14% year-on-year increase in premium product sales. Diversification strategies enhance brand loyalty and reinforce the Baby Food & Pediatric Nutrition market insights in Latin America.

Baby Food & Pediatric Nutrition Market Driver

Rising Awareness of Infant Nutrition and Health

The growing emphasis on infant nutrition is driving the Baby Food & Pediatric Nutrition market in Latin America. Awareness campaigns and government initiatives have increased fortified formula consumption by 8% year-on-year, with infant formula now accounting for 45% of total market share. Urban household penetration averages 78%, while semi-urban regions contribute 56%. Increased maternal education and healthcare access correlate with a 6% annual growth in complementary product usage. The regional Baby Food & Pediatric Nutrition market growth is further supported by 1.2 million metric tons of annual production, ensuring supply-demand equilibrium. This driver significantly enhances market demand, size, and insights for manufacturers and investors.

Baby Food & Pediatric Nutrition Market Restraint

High Product Prices and Regulatory Barriers

Premium Baby Food & Pediatric Nutrition products in Latin America are priced between USD 15–35 per kilogram, limiting adoption among low-income households. Regulatory compliance costs for fortification, labeling, and quality assurance have increased production expenses by 9%, affecting small-scale manufacturers. Price sensitivity has led to a 5% slower adoption in rural regions compared to urban areas. Additionally, distribution constraints reduce availability in remote areas, where only 38% of households have access to fortified baby foods. These restraints suppress Baby Food & Pediatric Nutrition market growth and insights despite rising health awareness.

Baby Food & Pediatric Nutrition Market Opportunity

Expansion of Organic and Specialty Product Lines

Latin America presents a lucrative opportunity for organic and specialty Baby Food & Pediatric Nutrition products, with market size projected to reach USD 15.72 billion by 2034. Organic product adoption has grown by 14%, contributing 22% of overall baby food sales. High-income households in Brazil, Mexico, and Argentina account for 68% of premium product consumption. Investment in innovative production lines with enhanced nutrient retention can capture an additional 3–4% market share. This opportunity reinforces Baby Food & Pediatric Nutrition market growth and insights through product differentiation and premium positioning.

Baby Food & Pediatric Nutrition Market Challenge

Supply Chain Disruptions and Raw Material Volatility

The Baby Food & Pediatric Nutrition market faces challenges due to raw material price volatility, particularly milk powder and cereals, which increased by 12% in 2025. Logistics bottlenecks during peak seasons affect 27% of distribution networks, leading to temporary stockouts. Export-import tariffs in countries like Argentina and Chile also contribute to increased operational costs. These challenges may restrain market expansion, though regional production of 1.2 million metric tons ensures baseline supply. Addressing these issues is critical to sustaining Baby Food & Pediatric Nutrition market size, growth, and insights.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.89 Billion |

| Market Size in 2026 | USD 9.45 Billion |

| Market Size in 2034 | USD 15.72 Billion |

| CAGR | 6.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Food & Pediatric Nutrition Market Segmentation

Segmentation of the Latin America Baby Food & Pediatric Nutrition market provides insight into product preference, application, and distribution channel dominance. Infant formula contributes 45% of total production, baby cereals 35%, and baby snacks 20%. Supermarkets account for 60% of sales, online stores 28%, and specialty stores 12%. These metrics reflect urban consumption trends and premium product adoption.

By Type

Infant Formula: Infant formula accounts for 45% of Latin America Baby Food & Pediatric Nutrition market share with 540,000 metric tons produced in 2025. Technical specifications include 12% protein content, fortified with DHA, AA, and prebiotics. This segment is critical for early childhood nutrition, supporting a growth rate of 5.6% CAGR through 2034.

Baby Cereals: Baby cereals contribute 35% market share, with 420,000 metric tons produced. Composition includes iron (8 mg/100g), calcium (50 mg/100g), and added probiotics in 22% of products. Consumption averages 1.5 servings/day per child, with higher adoption in urban centers (74%).

Baby Snacks: Baby snacks comprise 20% of the market with 240,000 metric tons in production. Technical specs include 6% protein, 3 g fiber, and low sugar (<5%). Snack adoption is growing at 6.8% CAGR due to convenience and health-conscious consumer trends.

By Application

Hospital Nutrition: Hospital-based baby food accounts for 15% of regional consumption, approximately 180,000 metric tons. Product usage frequency averages 2.5 servings/day, with fortified formulas preferred in NICU settings.

Home Nutrition: Home nutrition is the largest application segment at 65%, producing 780,000 metric tons. Infant formula accounts for 42% of home usage, cereals 38%, and snacks 20%. Adoption rates are higher in metropolitan households (78%).

Daycare and Institutional Feeding: This segment represents 20% market share, with 240,000 metric tons consumed in 2025. Standardized nutritional formulations and fortified cereals are widely used, with 80% adoption of prebiotic-enriched formulas to support immune health.

Latin America Baby Food & Pediatric Nutrition Market Segmentations

Product Type

- Infant Formula

- Baby Cereals

- Baby Snacks

Distribution Channel

- Supermarkets/Hypermarkets

- Online Stores

- Specialty Stores

Baby Food & Pediatric Nutrition Market Regional Outlook

Brazil

Brazil contributes 42% of Latin America Baby Food & Pediatric Nutrition market share, producing 504,000 metric tons in 2025. Infant formula dominates at 48%, cereals 34%, and snacks 18%. Urban household penetration is 80%, while rural adoption is 55%. Brazil’s large retail network accounts for 62% of total sales, with online stores increasing by 28% YoY.

Mexico

Mexico holds 28% market share, producing 336,000 metric tons. Infant formula accounts for 46% of consumption, cereals 36%, and snacks 18%. Distribution channels are led by supermarkets (65%), online platforms (24%), and specialty stores (11%). Adoption of organic baby foods is growing at 13% annually.

Argentina

Argentina contributes 15% share with production of 180,000 metric tons. Infant formula usage is 44%, cereals 37%, and snacks 19%. Rural penetration is 40%, while urban adoption exceeds 75%. Organic and fortified product adoption has increased by 11% YoY.

Chile

Chile accounts for 8% of market share, producing 96,000 metric tons. Infant formula dominates with 50% share, cereals 30%, and snacks 20%. Advanced technology adoption in 68% of production facilities has improved nutrient retention by 9%.

Colombia

Colombia holds 7% market share with production of 84,000 metric tons. Infant formula contributes 42%, cereals 35%, and snacks 23%. E-commerce penetration is 25%, with a growing preference for organic and fortified products. Urban adoption averages 72%.

List of Top Baby Food & Pediatric Nutrition Companies

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Mead Johnson Nutrition

- Kraft Heinz Company

- Hero Group

- FrieslandCampina

- Hipp Organic

- Bellamy’s Australia

- Aptamil

- Baby Dove

- Gerber Products Company

- Bledina

- Wyeth Nutrition

Top Companies

Nestlé S.A.

-

Market share: 17% in Latin America

-

Positioned as a premium brand with strong distribution networks and product diversification. Nestlé produced over 200,000 metric tons of infant formula and cereals in 2025, contributing significantly to the Baby Food & Pediatric Nutrition market size. The company’s focus on fortified and organic products has increased revenue growth by 6.5% YoY.

Danone S.A.

-

Market share: 14% in Latin America

-

Danone specializes in dairy-based infant formulas and cereals, producing 175,000 metric tons in 2025. Adoption of probiotic-enriched products in 45% of its portfolio has reinforced Baby Food & Pediatric Nutrition market growth. Danone leads in online and specialty store penetration with a CAGR of 7.2% in premium segments.

Investment Analysis and Opportunities

Investment in Latin America Baby Food & Pediatric Nutrition market reached USD 1.5 billion in 2025, representing 8% of total FMCG investments. Allocation across sectors includes 45% in infant formula, 30% in cereals, and 25% in snacks. Brazil and Mexico together capture 70% of regional investment. M&A activity has increased with Danone acquiring specialty baby food start-ups and Nestlé entering joint ventures for organic lines. Collaborative R&D initiatives focusing on prebiotics, probiotics, and fortified snacks have risen by 22% YoY, reinforcing market growth. Investment in technology for automated nutrient monitoring is increasing, with 40% of total capital allocated toward production efficiency and product safety enhancements.

New Product Development

In 2025, 18% of total Latin America Baby Food & Pediatric Nutrition products were new launches, including allergen-free formulas, DHA-fortified cereals, and organic snacks. Innovation has improved performance metrics by 12%, including nutrient retention and digestibility. Companies emphasize research-backed formulations, increasing adoption rates by 9% in urban centers. Product development strategies focus on premiumization and health-oriented ingredients, reinforcing market growth and insights for Baby Food & Pediatric Nutrition market stakeholders.

Recent Developments

- 2025: Nestlé expanded fortified formula production by 14%, reaching 220,000 metric tons in Brazil.

- 2025: Danone launched organic cereals with 12% higher adoption rates in Mexico.

Research Methodology

The Latin America Baby Food & Pediatric Nutrition market analysis is based on a combination of primary and secondary research. Primary research included interviews with over 120 industry stakeholders, including manufacturers, distributors, and regulatory officials. Secondary research involved examining government reports, trade journals, company annual reports, and market databases. Market size estimation used historical production volumes, consumption patterns, and pricing trends from 2022–2025, with projections for 2026–2034. Both top-down and bottom-up approaches were applied to validate market size, segment dominance, and growth trends. Quantitative metrics such as production in metric tons, revenue in USD billion, CAGR percentages, and household adoption rates were cross-verified to ensure accuracy. This methodology ensures comprehensive, data-driven insights for stakeholders in the Baby Food & Pediatric Nutrition market, supporting investment, product development, and strategic planning.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.