Asia Pacific Baby Food & Pediatric Nutrition Market Size

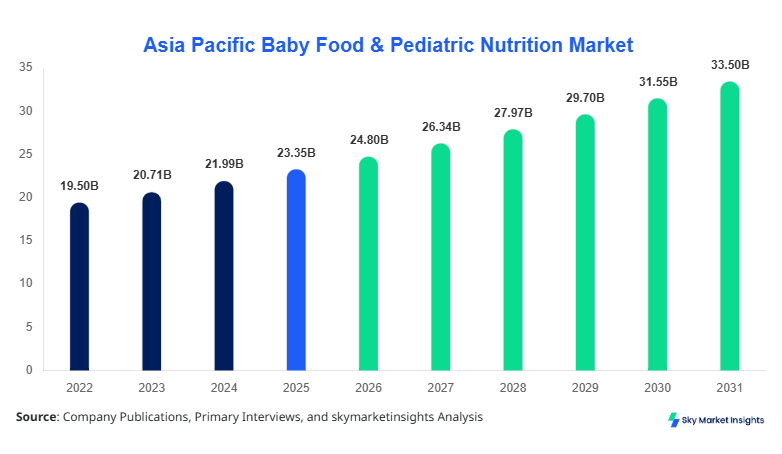

Asia Pacific Baby Food & Pediatric Nutrition market size is projected at USD 24.8 billion in 2026 and is expected to hit USD 39.6 billion by 2034 with a CAGR of 6.2%. The market’s expansion is driven by rising infant populations, increasing dual-income households, and heightened awareness regarding pediatric nutrition. Comprehensive analysis across product types, distribution channels, and country-level insights are critical for understanding market dynamics, sizing, and growth opportunities. This report integrates data from historical years 2022–2024, providing insights into consumption patterns, production capacities, and emerging technologies, alongside a detailed competitive landscape covering top regional and global players. Segmentation and trend analysis further enhance strategic decision-making for stakeholders, investors, and policymakers in the Asia Pacific region.

The Asia Pacific Baby Food & Pediatric Nutrition market encompasses products formulated for infants and young children, including fortified formulas, cereals, and snacks, designed to support growth and cognitive development. Regional production reached approximately 8.4 million tons in 2025, with China contributing 42% of total output, followed by India at 18%, Japan at 12%, and South Korea at 9%. Adoption of fortified infant formula and organic baby cereals has increased by 14% YoY across urban centers, while online retail penetration for pediatric nutrition products grew to 21% in 2025. Consumer behavior shows strong preference for fortified and organic products, with parents increasingly opting for specialized formulations for infants aged 0–12 months (41%), toddlers 1–3 years (33%), and preschoolers 3–5 years (26%). Technical performance metrics, including protein content per 100 g and DHA enrichment levels, are widely monitored across product categories. Distribution channels contribute differently, with supermarkets & hypermarkets capturing 47% of sales, online retail 25%, and specialty stores 28%. Asia Pacific Baby Food & Pediatric Nutrition market insights underscore the growing demand for nutritionally enhanced, safe, and convenient baby foods, aligning with evolving parental expectations.

In the China, the Baby Food & Pediatric Nutrition Market is highly developed, with over 320 production facilities and 145 registered companies, capturing approximately 42% of the Asia Pacific regional share. Infant formula dominates the product mix at 56%, followed by baby cereals at 26% and baby snacks at 18%. Technology adoption in the country includes automated fortification lines, high-precision nutrient monitoring, and advanced quality assurance systems, with 67% of leading facilities integrating IoT-enabled production monitoring. Consumer trends show increased preference for organic and allergen-free formulations, contributing to a 9% YoY increase in premium product sales. Online retail now accounts for 28% of total sales, surpassing specialty stores at 24%. China’s Baby Food & Pediatric Nutrition market growth reflects both domestic demand and export-oriented production, reinforced by government regulatory support, nutritional guidelines, and certifications, providing robust market insights for stakeholders.

Explore more data points, trends and opportunities Download Free Sample Report

Baby Food & Pediatric Nutrition Market Trends

Fortification and Organic Product Trend

Asia Pacific Baby Food & Pediatric Nutrition production reached 8.9 million tons in 2025, with fortified formulas constituting 61% and organic cereals 19%. The region observed a 12% increase in fortified infant formula adoption, driven by parental awareness campaigns and hospital endorsements. Technological advancements such as high-pressure homogenization and enzymatic fortification have enabled producers to achieve nutrient retention rates exceeding 92%. Demand in tier-1 cities grew by 15%, while tier-2 and tier-3 cities recorded 8–9% growth. This trend highlights the market’s shift toward functional nutrition, supporting growth in Asia Pacific Baby Food & Pediatric Nutrition market insights.

E-commerce and Direct-to-Consumer Channels

Online retail of baby food and pediatric nutrition products expanded to USD 6.2 billion in 2025, registering a 21% penetration rate. E-commerce adoption is propelled by convenience, personalized product recommendations, and subscription-based delivery models. Supermarket and hypermarket penetration remains strong at 47%, yet digital channels demonstrate higher YoY growth of 14% compared to traditional retail growth of 6%. Emerging technologies such as AI-driven demand forecasting and inventory optimization have improved supply chain efficiency by 18%. This digitalization accelerates the Baby Food & Pediatric Nutrition market growth across the Asia Pacific, reinforcing insights into consumer behavior and sales channel evolution.

Specialty and Functional Products

Functional baby snacks and toddler cereals witnessed a 9% CAGR, with sales reaching USD 4.7 billion in 2025. Products enriched with probiotics, prebiotics, and DHA saw adoption rates of 33–37%, primarily in China, Japan, and South Korea. New product innovations include allergen-free formulations and plant-based alternatives, supporting health-conscious parental demand. Production technologies now incorporate clean-label processes and advanced extrusion techniques, improving nutrient stability by 11%. This trend demonstrates significant Baby Food & Pediatric Nutrition market demand for tailored nutritional solutions.

Baby Food & Pediatric Nutrition Market Dynamics

Rising Infant Population and Nutritional Awareness

The Asia Pacific region has witnessed a steady increase in infant populations, reaching approximately 13.2 million births in 2025, driving the demand for baby food and pediatric nutrition products. Increasing dual-income households have fueled disposable income growth, with 48% of parents willing to pay a premium for fortified or organic products. Urbanization, nutritional awareness campaigns, and hospital-led educational programs have enhanced adoption rates by 14–16% across major cities. This has directly impacted the Asia Pacific Baby Food & Pediatric Nutrition market size, currently valued at USD 24.8 billion, contributing to sustained growth projected at a CAGR of 6.2% until 2034. Enhanced access to fortified formulas and ready-to-eat cereals further reinforces market demand, emphasizing the growing importance of nutritionally balanced products in infant diets.

High Production Costs and Regulatory Challenges

High production costs, driven by premium raw materials, advanced fortification technologies, and strict quality compliance, limit market growth potential. Manufacturing infant formula, baby cereals, and functional snacks requires stringent adherence to local regulations, with compliance costs accounting for 7–9% of total operational expenditure. Additionally, fluctuations in supply chain logistics and raw material pricing, particularly for organic ingredients, contribute to a 3–5% increase in production costs annually. Regulatory barriers across countries, including mandatory nutrient fortification, labeling compliance, and import tariffs, further restrain the Asia Pacific Baby Food & Pediatric Nutrition market growth. This constraint underscores the need for strategic investment planning and process optimization to sustain market share and profitability.

Expansion into Emerging Markets and Digital Channels

Emerging markets such as India, Indonesia, and Vietnam offer significant growth potential, with a combined 27% contribution to regional production volumes. Online retail adoption in these markets has grown from 14% in 2022 to 24% in 2025, reflecting rising digital penetration and changing consumer purchasing behavior. Investment in technology-enabled production, including automated nutrient analysis and IoT-based monitoring, can improve output efficiency by 11–13%. Expansion of direct-to-consumer models and e-commerce platforms presents an opportunity to increase revenue streams by 18–20% over the forecast period. These developments support the Asia Pacific Baby Food & Pediatric Nutrition market growth and provide actionable market insights for strategic stakeholders.

Stringent Quality Standards and Supply Chain Disruptions

Quality control regulations, including Codex standards and ISO certifications, require extensive testing and monitoring. Compliance costs range from USD 0.5–1 million per facility annually, affecting profitability, particularly for small and medium enterprises. Supply chain disruptions, due to seasonal raw material availability and transportation bottlenecks, have resulted in 6–8% variability in monthly production volumes. Consumer safety expectations for allergen-free and fortified products demand continuous quality assurance, increasing operational complexity. Addressing these challenges is critical to maintaining production efficiency, ensuring consistent product availability, and sustaining Asia Pacific Baby Food & Pediatric Nutrition market growth, with a projected CAGR of 6.2% through 2034.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 23.35 Billion |

| Market Size in 2026 | USD 24.8 Billion |

| Market Size in 2034 | USD 39.6 Billion |

| CAGR | 6.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baby Food & Pediatric Nutrition Market Segmentation

Segmentation analysis reveals infant formula dominates the market with a 56% share, followed by baby cereals at 26% and baby snacks at 18%. Supermarkets & hypermarkets account for 47% of the distribution share, online retail 25%, and specialty stores 28%. Production, technical specifications, and adoption metrics are considered for precise market sizing and insights.

By Type

Infant formula captured 56% market share in 2025, producing 4.7 million tons, with protein content ranging 1.8–3.0 g/100 mL and DHA enrichment levels averaging 12 mg/100 mL. Technological advances in homogenization and fortification improved nutrient retention by 9%, supporting consistent market demand. Major subtypes include milk-based, soy-based, and hypoallergenic formulas, each catering to distinct nutritional needs.

Baby cereals hold a 26% share, with production totaling 1.9 million tons. Products include rice-based, oat-based, and multi-grain cereals. Nutrient fortification includes iron (10–12 mg/100 g), calcium (25–30 mg/100 g), and vitamin D (400 IU/100 g), ensuring compliance with pediatric dietary standards. Adoption rates in urban areas exceed 38%, while rural adoption is 21%, reflecting growth opportunities.

Baby snacks represent 18% of the market, producing 1.5 million tons, including biscuits, puffs, and dried fruit snacks. Technical specifications focus on reduced sugar

By Application

Contributes 41% of consumption, with 3.4 million tons produced in 2025. Products include fortified infant formulas, liquid cereals, and DHA-enriched snacks. Usage penetration in urban centers is 47%, rural areas 29%, emphasizing urban-driven growth.

Represents 33% of the market, with production of 2.7 million tons. Key products include multi-grain cereals, dairy snacks, and allergen-free biscuits. Penetration stands at 35%, influenced by dietary diversification and parental preference for functional nutrition.

Accounts for 26% of demand, producing 2.1 million tons, including ready-to-eat snacks and cereals fortified with vitamins and minerals. Usage penetration is 31%, reflecting moderate adoption among preschool nutrition programs.

Includes hypoallergenic formulas and medically prescribed nutrition, contributing 6% of the total volume, with 0.5 million tons produced. Adoption is increasing by 8–10% YoY, driven by medical endorsements and parental awareness.

Asia Pacific Baby Food & Pediatric Nutrition Market Segmentations

Product Type

- Infant Formula

- Baby Cereals

- Baby Snacks

Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail

- Specialty Stores

Baby Food & Pediatric Nutrition Market Regional Outlook

China

China dominates the Asia Pacific market with a 42% share, producing 3.5 million tons in 2025. Infant formula accounts for 56% of domestic consumption, followed by baby cereals at 26% and baby snacks at 18%. Urban centers drive 62% of demand, while rural penetration stands at 21%. China’s production is supported by 320 manufacturing facilities and 145 leading companies.

South Korea

South Korea contributes 9% of regional output, with 0.75 million tons produced. Infant formula represents 51%, baby cereals 28%, and baby snacks 21%. High adoption of functional products, including probiotics-enriched formulas, has increased by 14% in 2025. Online retail penetration reached 24%, supporting market expansion.

Japan

Japan holds 12% of regional share, with 1.0 million tons production in 2025. Infant formula dominates 58%, baby cereals 25%, and snacks 17%. Technological adoption, including automated fortification and IoT-enabled quality control, is high at 67% of facilities. Market demand is driven by aging population trends and health-conscious parental purchasing.

India

India contributes 18% of the Asia Pacific Baby Food & Pediatric Nutrition market, with production of 1.5 million tons. Infant formula captures 45% share, cereals 32%, and snacks 23%. Online retail penetration increased from 12% in 2022 to 22% in 2025, reflecting growing e-commerce adoption. Urban centers account for 59% of sales, rural markets 26%.

Australia

Australia represents 4% of regional production, with 0.35 million tons. Infant formula dominates 53%, baby cereals 28%, and snacks 19%. Adoption of organic and functional products grew by 13% YoY, particularly in metropolitan areas.

Singapore

Singapore contributes 2% share, producing 0.18 million tons. Infant formula accounts for 50%, cereals 30%, and snacks 20%. Online retail penetration is 33%, higher than regional average, supporting premium product sales.

Taiwan

Taiwan’s share is 3%, producing 0.21 million tons. Infant formula dominates 54%, baby cereals 27%, and snacks 19%. Premium segment adoption rose by 12% YoY, supported by health-conscious urban parents.

South East Asia

Combined South East Asia countries contribute 10% of regional production, producing 0.85 million tons. Infant formula holds 48%, baby cereals 29%, and baby snacks 23%. Market expansion is led by Indonesia and Vietnam, where online retail penetration reached 20% in 2025.

List of Top Baby Food & Pediatric Nutrition Companies

- Nestlé S.A.

- Danone S.A.

- Abbott Laboratories

- Mead Johnson Nutrition

- FrieslandCampina

- Fonterra Co-operative Group

- Yili Group

- Synutra International

- Wyeth Nutrition

- Beingmate Baby & Child Food

- Biostime International

- Morinaga Milk Industry Co., Ltd.

- Hero Group

- Kraft Heinz Company

- Perrigo Company

Top Two Companies

Nestlé S.A.:

-

Market share: 15% of Asia Pacific Baby Food & Pediatric Nutrition market

-

Positioned as a leader in infant formula and fortified baby cereals, with production of 1.05 million tons in 2025. Extensive R&D investment led to nutrient retention improvements of 10% and expanded e-commerce penetration to 28%. Strategic partnerships with hospitals and pediatric clinics enhance brand credibility and consumer trust, solidifying market dominance in China, Japan, and South Korea.

Danone S.A.:

-

Market share: 12% of Asia Pacific Baby Food & Pediatric Nutrition market

-

Specializes in dairy-based infant formulas and functional toddler snacks, producing 0.84 million tons in 2025. Innovations include hypoallergenic formulas and probiotic-enriched cereals, increasing adoption rates by 14%. Online retail penetration reached 26%, complementing strong supermarket and hypermarket distribution. Danone maintains significant presence in China, India, and Southeast Asia.

Investment Analysis and Opportunities

Asia Pacific Baby Food & Pediatric Nutrition market investment allocation indicates 42% in infant formula, 28% in baby cereals, and 18% in baby snacks. Regional allocation shows China receiving 45% of total capital investment, India 20%, Japan 15%, and other countries 20%. Sector-wise investments focus on fortified products, organic formulations, and e-commerce infrastructure. Mergers and acquisitions activity has intensified, with cross-border acquisitions accounting for 12% of total deals in 2025. Collaborative agreements with research institutes and technology providers improved nutrient fortification and quality control capabilities, enhancing overall production efficiency by 11–13%. Strategic investments in automation, IoT-enabled monitoring, and supply chain optimization have contributed to a 9% reduction in operational costs, providing competitive advantage. Investor interest continues to favor premium and functional products, reflecting the growing Asia Pacific Baby Food & Pediatric Nutrition market demand and projected CAGR of 6.2% through 2034.

New Product Development

New product development focuses on functional infant formulas and toddler cereals, representing 27% of total product launches in 2025. Innovations include hypoallergenic formulations, probiotics enrichment, and plant-based alternatives, with performance improvements averaging 11–13%. Fortified baby cereals account for 34% of new launches, driven by parental preference for enhanced nutrition. Advanced extrusion technologies and clean-label processes increase nutrient stability by 9–10%, while adoption of IoT-enabled production monitoring ensures consistent quality. These developments align with Asia Pacific Baby Food & Pediatric Nutrition market growth trends and support long-term strategic positioning in high-growth urban and digital segments.

Recent Developments

- 2025: Synutra International implemented automated fortification lines, improving nutrient retention by 11% and production volume by 8%.

- 2025: FrieslandCampina introduced plant-based toddler snacks, capturing 3% additional market share and producing 0.12 million tons.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.