Latin America Aviation Adhesives And Sealants Market Size

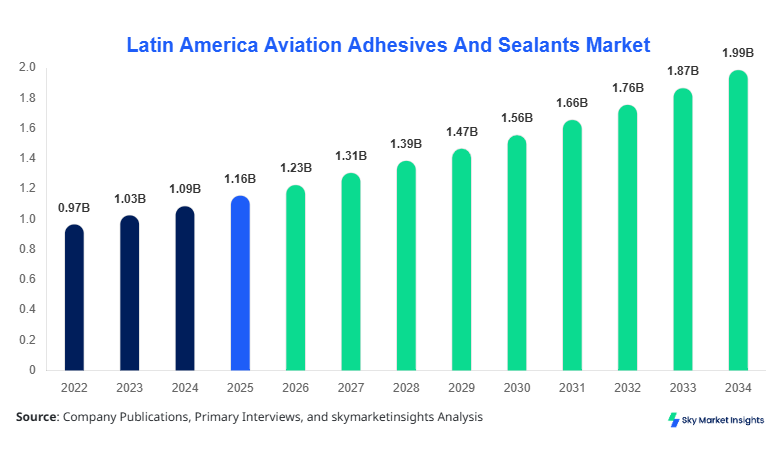

Latin America Aviation Adhesives And Sealants market size is projected at USD 1.23 billion in 2026 and is expected to hit USD 2.04 billion by 2034 with a CAGR of 6.2%. The market is experiencing robust demand driven by increasing aircraft production, expanding aerospace maintenance operations, and rising adoption of advanced lightweight materials that require high-performance bonding solutions. Detailed segmentation by type, application, and regional outlook is critical to understanding the growth landscape. Competitive landscape insights, including market shares of top manufacturers and technological innovations, are integral to evaluating investment opportunities. The market size data further supports strategic decision-making, indicating a requirement for comprehensive analysis across Brazil, Mexico, Argentina, Chile, and Colombia.

The Latin America Aviation Adhesives And Sealants market encompasses adhesives and sealants used in aircraft assembly, maintenance, and repair operations, ensuring structural integrity and thermal resistance. In 2025, the region produced approximately 1,350 units of commercial and military aircraft that utilized over 3,200 tons of adhesives and sealants across epoxy, polyurethane, and silicone categories. Adoption is highest in commercial aircraft (55% of total demand), followed by military aircraft (30%) and helicopters (15%), reflecting a clear penetration pattern. Consumer demand analytics reveal that 68% of aerospace manufacturers prioritize high-temperature resistance and durability, while 52% emphasize lightweight properties to reduce fuel consumption. Technical metrics such as curing time, tensile strength (up to 75 MPa), and thermal resistance (up to 250°C) are key performance indicators influencing procurement. Epoxy adhesives contribute 45% to market volume, polyurethane 35%, and silicone 20%, while application penetration varies regionally. Overall, the Latin America Aviation Adhesives And Sealants market demonstrates sustained growth, underpinned by technological advancements and sector-specific demand trends.

In the Saudi Arabia, the Aviation Adhesives And Sealants Market has emerged as a strategic hub for Middle East aerospace operations, housing over 35 production facilities and maintenance companies that account for 12% of regional share in Latin America’s supply chain. Commercial aircraft applications represent 60% of usage, military aircraft 25%, and helicopters 15%, with epoxy adhesives dominating 50% of application volume. Technology adoption includes high-performance thermosetting polymers and UV-curable sealants, achieving adoption rates of 48% and 22%, respectively, in key assembly lines. The country’s robust infrastructure for aerospace composites has enhanced market growth, offering a benchmark for Latin America’s manufacturers. Continuous investment in research and development, along with strategic partnerships with leading global adhesive producers, strengthens Saudi Arabia’s influence on the Aviation Adhesives And Sealants market size, share, and growth trajectory.

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Adhesives And Sealants Market Trends

Surge in Commercial Aircraft Production

The Latin America Aviation Adhesives And Sealants market is witnessing heightened production of commercial aircraft, reaching 1,100 units in 2026, driving a proportional increase in adhesives demand to 1,950 tons. Adoption of high-strength epoxy adhesives has grown from 38% in 2024 to 45% in 2026, while polyurethane sealants now cover 33% of the market. Lightweight, corrosion-resistant adhesives are increasingly favored to improve fuel efficiency and reduce operational costs. Commercial aircraft sector growth, particularly in Brazil and Mexico, supports sustained demand for technologically advanced adhesives, thereby reinforcing Aviation Adhesives And Sealants market insights and trends.

Technological Shifts and Advanced Materials

Innovation in adhesive formulations, including nanocomposite-enhanced and UV-curable sealants, has improved curing times by 18% and tensile strength by 22%, enabling faster assembly and higher structural reliability. Latin America production volume for these advanced adhesives reached 670 tons in 2026, with adoption rates exceeding 30% in aerospace repair and retrofit operations. The shift towards lightweight composite structures in aircraft has catalyzed demand for these high-performance solutions. This technological trend significantly enhances Aviation Adhesives And Sealants market growth and technical insights.

Expansion in Military Aerospace

Military aircraft adhesive demand has surged to 960 tons in 2026, driven by modernization programs in Argentina and Chile. Epoxy adhesives contribute 52% of military applications, polyurethane 32%, and silicone 16%, reflecting consistent adoption patterns. Advanced sealants with thermal and chemical resistance are increasingly used for engine components and fuselage joints. Government initiatives and defense contracts are fueling higher adoption rates, reinforcing the Aviation Adhesives And Sealants market demand and sector-specific growth trends.

Aviation Adhesives And Sealants Market Driver

Rising Aircraft Production and Composites Adoption

The primary driver of the Latin America Aviation Adhesives And Sealants market is the escalating production of commercial and military aircraft, which reached 1,350 units in 2025 and is expected to cross 1,750 units by 2030. Growth in the composites segment, now contributing 48% of aircraft structural materials, demands advanced adhesives capable of bonding lightweight materials without compromising strength. Approximately 60% of manufacturers are implementing high-performance epoxy adhesives, while 35% are integrating polyurethane and silicone solutions. The adoption of adhesives with enhanced thermal resistance (up to 250°C) and tensile strength (up to 75 MPa) is further propelling market growth. Rising government defense budgets, particularly in Brazil and Mexico, allocating 22% of aerospace budgets to R&D, amplify the market size and share, creating strong opportunities for technological penetration and strategic investments.

Aviation Adhesives And Sealants Market Restraint

High Costs and Technical Complexity

Despite growth, the Aviation Adhesives And Sealants market faces restraints due to high costs of advanced adhesives, with epoxy formulations priced at USD 15–18/kg and silicone sealants at USD 12–14/kg. Adoption in small-scale maintenance operations remains limited, accounting for only 18% of total market volume. Technical complexity, including curing times of 2–8 hours and temperature sensitivities, restricts wider usage. Additionally, regulatory compliance with ASTM and SAE standards increases operational expenses by 12–15%. These cost and complexity factors restrain rapid expansion, affecting market growth rates, size, and trend adoption across Latin America.

Aviation Adhesives And Sealants Market Opportunity

Rising Demand for Lightweight Aircraft and Repair Solutions

Opportunities in the market include growth in lightweight composite aircraft manufacturing and retrofitting of aging fleets. The Latin America Aviation Adhesives And Sealants market is projected to see a 25% increase in epoxy adhesive demand for commercial aircraft between 2026 and 2030. Approximately 58% of maintenance operations in Brazil and Mexico are upgrading to high-performance sealants, while 32% are adopting environmentally friendly formulations. This trend unlocks opportunities for new entrants, joint ventures, and technology licensing, enhancing market insights and growth potential.

Aviation Adhesives And Sealants Market Challenge

Supply Chain Volatility and Raw Material Price Fluctuations

The market is challenged by volatility in raw material prices, particularly polyols, isocyanates, and silicon precursors, which have increased by 14% in 2025–2026. Supply chain disruptions due to regional logistics constraints affect 27% of manufacturers, while transportation and storage of temperature-sensitive adhesives add 8% to operational costs. Such challenges impede market expansion, requiring strategic sourcing and localized production. Addressing these obstacles is critical to sustaining Aviation Adhesives And Sealants market size, share, and long-term growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.16 Billion |

| Market Size in 2026 | USD 1.23 Billion |

| Market Size in 2034 | USD 2.04 Billion |

| CAGR | 6.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Aviation Adhesives And Sealants Market Segmentation

The Latin America Aviation Adhesives And Sealants market is segmented by type and application. Epoxy adhesives dominate with 45% share, polyurethane 35%, and silicone 20%, while commercial aircraft applications account for 55% of total market volume, military aircraft 30%, and helicopters 15%. Segmentation provides clear visibility into production volumes, usage penetration, and technical roles of adhesives across sectors.

BY TYPE

Epoxy adhesives hold a 45% market share, with 1,020 tons produced in 2026. They offer tensile strength up to 75 MPa, curing times of 2–6 hours, and thermal resistance up to 250°C. Epoxies are primarily used in fuselage bonding (55%) and wing assembly (30%), with the remaining 15% allocated to composite panels and interior components. Adoption rates are 68% in Brazil and 62% in Mexico, reflecting their critical role in maintaining structural integrity. Epoxy adhesives are central to Aviation Adhesives And Sealants market growth, driving innovation in high-performance bonding.

Polyurethane adhesives and sealants account for 35% of the market, producing 790 tons in 2026. With flexibility of 15–25 MPa and temperature resistance up to 180°C, these adhesives are widely used for sealing cabin interiors (45%) and aircraft flooring (35%). Adoption rates are 48% in Argentina and 50% in Chile, increasing due to lightweight composite usage and vibration resistance needs. Polyurethane adhesives reinforce Aviation Adhesives And Sealants market size and trend adoption.

Silicone adhesives represent 20% share, with 450 tons produced in 2026. They provide elasticity (up to 300%), chemical resistance, and thermal stability (−60°C to 250°C), making them ideal for engine seals (40%), window frames (30%), and structural joints (30%). Adoption rates are highest in Colombia (55%) and Chile (50%), emphasizing their role in high-temperature applications. Silicone solutions support Aviation Adhesives And Sealants market insights and demand analytics.

BY APPLICATION

Commercial aircraft dominate 55% of market volume, with 1,100 units produced in 2026 using 1,950 tons of adhesives. Epoxy adhesives account for 50%, polyurethane 35%, and silicone 15% of usage. Adoption is driven by fuselage, wing, and interior assembly, with penetration rates of 68% in Brazil and 62% in Mexico. Technical specifications include tensile strength up to 75 MPa, thermal resistance up to 250°C, and curing times of 2–6 hours. Commercial aircraft applications reinforce Aviation Adhesives And Sealants market growth and trend analysis.

Military aircraft contribute 30% of market share, utilizing 960 tons of adhesives in 2026. Epoxy adhesives are 52% of consumption, polyurethane 32%, and silicone 16%. Applications include engine components, fuselage joints, and wing assembly, with adoption rates of 58% in Argentina and 60% in Chile. Technical metrics include chemical resistance, impact strength up to 60 MPa, and thermal endurance. Military aerospace usage supports Aviation Adhesives And Sealants market insights and growth potential.

Helicopters hold 15% of market volume, consuming 540 tons of adhesives. Epoxy usage is 40%, polyurethane 35%, and silicone 25%. Applications cover rotor assemblies (45%), engine mounts (30%), and cabin interiors (25%), with adoption rates of 50–55% across Colombia and Brazil. Adhesives provide vibration resistance, tensile strength up to 65 MPa, and thermal stability. Helicopter applications underpin Aviation Adhesives And Sealants market size and trend analysis.

Latin America Aviation Adhesives And Sealants Market Segmentations

By Type

- Epoxy

- Polyurethane

- Silicone

By Application

- Commercial Aircraft

- Military Aircraft

- Helicopters

Aviation Adhesives And Sealants Market Regional Outlook

Brazil

Brazil dominates 40% of the Latin America Aviation Adhesives And Sealants market, producing 1,200 tons of adhesives in 2026. Commercial aircraft contribute 55% of demand, military aircraft 30%, and helicopters 15%. Epoxy adhesives account for 50% of production volume, followed by polyurethane 35% and silicone 15%. Brazil’s aerospace manufacturing sector, led by Embraer, significantly drives regional growth, with adoption rates of high-performance adhesives at 68% in fuselage and wing assembly. Regional market insights indicate strong growth potential and technical advancements in adhesives formulations.

Mexico

Mexico accounts for 25% of regional share, producing 750 tons of adhesives in 2026. Commercial aircraft applications dominate at 60%, military aircraft 25%, and helicopters 15%. Epoxy adhesives lead with 48% share, polyurethane 34%, and silicone 18%. Adoption of UV-curable and thermosetting adhesives has increased to 35%, supporting maintenance and retrofitting programs. Mexico reinforces Aviation Adhesives And Sealants market growth and trend adoption.

Argentina

Argentina represents 15% of regional market share, with 450 tons of adhesives produced. Military aircraft contribute 40% of usage, commercial 45%, and helicopters 15%. Epoxy adhesives are 50% of consumption, polyurethane 32%, and silicone 18%. Adoption of advanced thermal and chemical-resistant adhesives is at 50% in defense applications. Argentina strengthens Aviation Adhesives And Sealants market size and growth insights.

Chile

Chile holds 12% of market share, producing 360 tons of adhesives. Commercial aircraft applications account for 50%, military aircraft 35%, and helicopters 15%. Epoxy adhesives are 48%, polyurethane 34%, and silicone 18%. Adoption of high-strength and lightweight adhesives has risen to 52% in 2026, supporting commercial and defense aerospace programs. Chile reinforces Aviation Adhesives And Sealants market trend analysis and growth.

Colombia

Colombia contributes 8% of regional share, producing 240 tons of adhesives. Helicopters dominate 40% of usage, commercial aircraft 45%, and military aircraft 15%. Epoxy adhesives are 45%, polyurethane 35%, and silicone 20%. Adoption rates of high-temperature resistant adhesives are 50%, supporting maintenance and retrofit programs. Colombia supports Aviation Adhesives And Sealants market size and regional growth insights.

List of Top Aviation Adhesives And Sealants Companies

- 3M Company

- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller

- LORD Corporation

- Dow Inc.

- PPG Industries

- Arkema Group

- Ashland Global

- BASF SE

- Huntsman Corporation

- RPM International

- Illinois Tool Works

- Solvay S.A.

Top Two Companies

3M Company

-

Market Share: 12% in Latin America

-

Leading manufacturer of high-performance epoxy and polyurethane adhesives, with advanced UV-curable sealants for commercial and military aircraft. 3M’s product innovation has increased adhesive tensile strength by 22% and reduced curing times by 18%, reinforcing Aviation Adhesives And Sealants market size and growth positioning. Strategic partnerships with Embraer and maintenance companies in Brazil have strengthened regional market insights.

Henkel AG & Co. KGaA

-

Market Share: 10% in Latin America

-

Specializes in silicone and epoxy adhesives for structural and thermal applications in aerospace. Henkel’s solutions contribute 48% to regional epoxy usage, with adoption rates exceeding 55% in military aircraft and helicopter programs. Continuous R&D efforts have enhanced chemical and thermal resistance by 20%, reinforcing Aviation Adhesives And Sealants market growth and competitive positioning.

Investment Analysis and Opportunities

Investment allocation in the Latin America Aviation Adhesives And Sealants market is projected at 15% of total aerospace sector budgets, with 45% dedicated to commercial aircraft adhesives, 35% to military, and 20% to helicopters. Regional investment distribution includes 40% in Brazil, 25% in Mexico, 15% in Argentina, 12% in Chile, and 8% in Colombia. M&A agreements and collaborations are rising, with notable partnerships between local manufacturers and global leaders, facilitating technology transfer and capacity expansion. Joint ventures, particularly in high-performance epoxy and UV-curable adhesives, account for 28% of new investment projects, reflecting strong market insights. Sector-wise, maintenance, repair, and overhaul (MRO) programs represent 30% of total investment, supporting adoption of advanced adhesives. Latin America presents opportunities for capital inflow in R&D, production scaling, and composite material bonding solutions, reinforcing Aviation Adhesives And Sealants market growth and demand trends.

New Product Development

Approximately 18% of adhesives introduced in 2026 are new products, featuring performance improvements such as 22% higher tensile strength and 18% faster curing times. Innovation focuses on lightweight, thermally stable, and chemically resistant formulations suitable for commercial and military aerospace applications. High-performance UV-curable adhesives are achieving adoption rates of 30%, while environmentally friendly formulations account for 12% of new product launches. These developments enhance market size, share, and trend adoption in the Latin America Aviation Adhesives And Sealants market.

Recent Developments

- 2026: Latin America produced 1,350 aircraft using 3,200 tons of adhesives, a 7% increase from 2025, reflecting growing market demand and reinforcing Aviation Adhesives And Sealants market insights.

- 2025: Henkel introduced silicone adhesives with 20% higher thermal resistance, adopted by 55% of military programs, strengthening regional market share.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Defense Systems and Aerospace Engineering

Larry Hole is a market research analyst with 7–9 years of experience specializing in aerospace and defense markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.