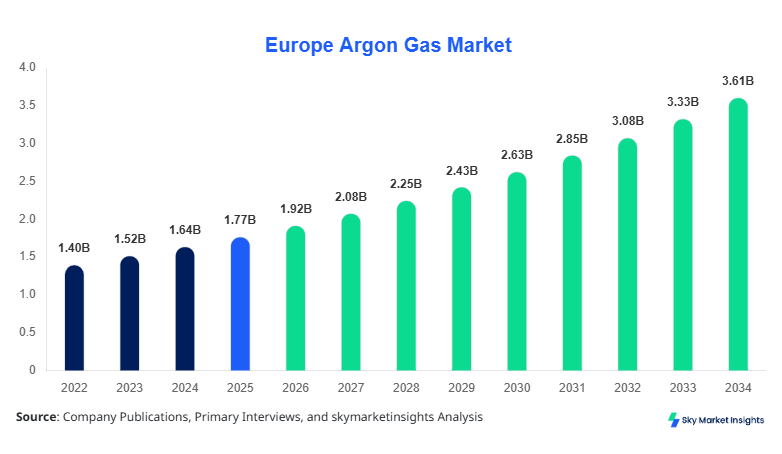

Europe Argon Gas Market Size

Europe Argon Gas market size is projected at USD 1.92 billion in 2026 and is expected to hit USD 3.61 billion by 2034 with a CAGR of 8.2%. The market recorded an estimated valuation of USD 1.78 billion in 2025, while total regional argon consumption exceeded 5.8 million metric tons across industrial and specialty applications. Increasing investment in electronics manufacturing, steel processing, and healthcare infrastructure is supporting sustained demand across Europe. Competitive intensity remains high, with over 45 major industrial gas producers and distributors operating across the region, while long-term supply contracts and technological integration continue to shape the competitive landscape.

Argon gas is an inert noble gas primarily utilized in welding, metal fabrication, semiconductor manufacturing, healthcare equipment production, and scientific research activities. Europe produced more than 6.2 million metric tons of industrial argon in 2025, supported by over 320 cryogenic air separation facilities operating across the United Kingdom, Germany, France, Italy, Spain, and Russia. Adoption rates in automated welding applications surpassed 71% in heavy manufacturing sectors, while high-purity argon penetration in semiconductor production reached nearly 64% across advanced electronics facilities. Consumer demand analytics indicate that automotive manufacturing contributed approximately 28% of total regional argon consumption, followed by electronics at 22%, healthcare at 14%, and metal fabrication at 31%. Technical metrics show that ultra-high-purity argon exceeding 99.999% purity is increasingly preferred in semiconductor and laser manufacturing environments due to contamination sensitivity below 5 ppm. Liquid argon accounted for nearly 48% of total supply volumes, while gaseous argon represented 39% and high-purity specialty grades held 13% share. Rising steel output, increasing robotic welding penetration, and expansion of healthcare cryogenic storage systems continue to accelerate Europe Argon Gas market growth.

Explore more data points, trends and opportunities Download Free Sample Report

Argon Gas Market Trends

Increasing Adoption of High-Purity Argon in Semiconductor Manufacturing

The semiconductor industry across Europe witnessed substantial growth in high-purity argon utilization during 2025, with total consumption volumes crossing 740,000 metric tons. Germany, the United Kingdom, and France collectively represented over 63% of semiconductor-grade argon demand due to expanding wafer fabrication capacity and rising investments in advanced electronics production. High-purity argon with 99.9999% purity levels is increasingly utilized in plasma etching, sputtering, and inert atmospheric processing applications. Approximately 58% of newly commissioned semiconductor facilities adopted closed-loop argon recovery systems capable of reducing gas waste by nearly 21%. The growing integration of electric vehicles and industrial automation systems is also accelerating chip production demand, thereby strengthening Europe's argon gas market trend.

Expansion of Automated Welding and Metal Fabrication Technologies

Automated welding technologies accounted for more than 54% of industrial welding operations across Europe during 2025, significantly increasing argon consumption in shielding gas applications. Total argon usage in metal fabrication exceeded 2.1 million metric tons, particularly across automotive, shipbuilding, railway, and heavy machinery sectors. Robotic welding systems using argon-rich shielding mixtures improved weld precision by approximately 18% while reducing oxidation defects by 26%. Spain and Italy together added over 18,000 new robotic welding installations during the year, supporting strong industrial gas utilization. The adoption rate of liquid argon bulk delivery systems increased by 17% among medium-scale manufacturers seeking operational efficiency and reduced cylinder handling costs. Expanding industrial modernization initiatives continue supporting Europe's argon gas market trend.

Rising Healthcare and Cryogenic Storage Applications

Healthcare applications for argon gas expanded steadily in Europe, with total medical and cryogenic usage exceeding 810,000 metric tons during 2025. Hospitals and biotechnology facilities increasingly adopted argon-based cryopreservation systems for stem cell storage, blood plasma preservation, and surgical technologies. Cryosurgery procedures utilizing argon plasma coagulation systems grew by 13.8% year-over-year across Europe. France and the United Kingdom collectively represented nearly 41% of medical argon demand due to strong healthcare infrastructure and increasing surgical procedures. Investments in pharmaceutical cold chain logistics also accelerated demand for liquid argon storage systems with thermal stability efficiencies above 98%. Expanding healthcare innovation continues to reinforce Europe's argon gas market demand.

Europe Argon Gas Drivers

Rising Steel Production and Welding Activities Across Europe

The expansion of steel manufacturing and fabrication industries across Europe remains a primary driver for argon consumption. Europe produced more than 136 million metric tons of crude steel during 2025, with Germany, Italy, and Spain collectively accounting for nearly 58% of total production volumes. Argon is extensively used in arc welding, stainless steel manufacturing, and oxygen decarburization processes due to its inert shielding characteristics. Industrial manufacturers increasingly adopted argon-rich gas mixtures in automated welding systems, resulting in approximately a 22% improvement in welding efficiency and a 16% reduction in defect rates. The automotive sector alone consumed over 1.3 million metric tons of argon for robotic welding operations in 2025. Additionally, shipbuilding and railway manufacturing industries expanded demand by 11.5% due to large-scale infrastructure modernization projects across Europe. Investments exceeding USD 8.7 billion in manufacturing automation and industrial expansion further accelerated argon utilization. Increasing demand from industrial fabrication and advanced metallurgy sectors continues supporting Europe's argon gas market growth.

Europe Argon Gas Restraints

High Energy Costs and Supply Chain Volatility Impact Production

Argon production heavily depends on cryogenic air separation technology, which requires substantial electricity consumption and advanced infrastructure investment. During 2025, industrial electricity prices across Europe increased by nearly 18%, significantly impacting production costs for industrial gas manufacturers. Germany and Italy recorded energy cost increases above 21%, resulting in temporary supply disruptions and reduced operational margins among medium-scale gas producers. Transportation and storage expenses for liquid argon also increased by approximately 14.6% due to higher fuel and logistics costs. Europe experienced periodic shortages of industrial gases during maintenance shutdowns at major air separation facilities, affecting nearly 9% of downstream manufacturers. Additionally, fluctuating raw material costs and geopolitical instability in Eastern Europe constrained long-term supply agreements and capital expenditure planning. Small-scale industrial users increasingly shifted toward optimized gas recycling technologies to reduce consumption, thereby moderating demand growth. Persistent operational and infrastructure-related challenges continue to restrain Europe's argon gas market growth.

Europe Argon Gas Opportunities

Expansion of Green Hydrogen and Renewable Energy Infrastructure

Rapid expansion of renewable energy and green hydrogen infrastructure across Europe presents significant opportunities for argon suppliers. Europe allocated more than USD 42 billion toward hydrogen production and clean energy manufacturing projects during 2025, with the United Kingdom, Germany, and France accounting for over 61% of investments. Argon gas is increasingly utilized in solar panel manufacturing, fuel cell production, and advanced welding processes for hydrogen pipeline construction. Offshore wind energy infrastructure projects generated demand for approximately 290,000 metric tons of industrial argon in fabrication activities during 2025. The adoption of laser welding systems in renewable energy equipment manufacturing increased by 19%, boosting high-purity argon consumption. Several industrial gas companies also introduced argon recovery and recycling technologies capable of lowering operating costs by nearly 24%. Growing decarbonization initiatives and sustainable manufacturing investments are expected to create substantial European argon gas market opportunities throughout the forecast period.

Challenges in Europe: Argon Gas

Limited Availability of High-Purity Gas Infrastructure

The availability of advanced purification and distribution infrastructure for high-purity argon remains a significant challenge across Europe. Semiconductor and electronics manufacturers require ultra-high-purity argon exceeding 99.9999% purity levels, but only approximately 27% of regional production facilities currently possess advanced purification capabilities. Establishing new cryogenic separation and purification units requires investments exceeding USD 120 million per facility, limiting rapid expansion. Transportation losses for liquid argon also averaged nearly 7% due to temperature-sensitive logistics and storage constraints. Russia and Spain experienced supply inconsistencies during peak industrial demand periods, affecting nearly 12% of semiconductor and specialty manufacturing operations. Additionally, skilled labor shortages in cryogenic engineering and gas processing technologies increased operational complexity and delayed infrastructure upgrades. Regulatory compliance requirements regarding emissions and industrial safety standards further added approximately 9% to operational expenditures. These infrastructure and operational limitations continue to challenge Europe's argon gas market demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.77 Billion |

| Market Size in 2026 | USD 1.92 Billion |

| Market Size in 2034 | USD 3.61 Billion |

| CAGR | 8.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Argon Gas Market Segmentation

The Europe argon industry is segmented by type and application, with liquid argon dominating nearly 48% of total consumption due to large-scale industrial welding and cryogenic applications. By application, metal fabrication accounted for approximately 31% of overall regional demand, followed by electronics at 22% and healthcare at 14%. Growing adoption of high-purity industrial gases and automated manufacturing technologies continues supporting segmentation expansion across Europe.

BY TYPE

Liquid argon represented the largest segment with approximately 48% regional consumption share in 2025. Total liquid argon production exceeded 2.8 million metric tons across Europe, supported by increasing demand from steel manufacturing, cryogenic storage, and industrial welding sectors. Liquid argon storage systems operating at temperatures below -185°C demonstrated thermal retention efficiencies above 97%, enabling cost-effective transportation and large-scale industrial deployment. Germany and the United Kingdom collectively contributed nearly 44% of regional liquid argon demand due to strong automotive and aerospace manufacturing activity. Bulk liquid argon systems also reduced operational distribution costs by approximately 16% compared to compressed cylinder systems.

Gaseous argon accounted for nearly 39% of regional consumption and remained widely utilized in metal fabrication, electronics assembly, and laboratory environments. Europe consumed more than 2.2 million metric tons of gaseous argon during 2025, with average industrial purity levels ranging between 99.9% and 99.99%. Automotive welding operations represented approximately 42% of gaseous argon demand due to increasing robotic welding adoption across vehicle manufacturing facilities. Spain and Italy experienced strong growth in small-scale industrial usage, supported by expansion in machinery manufacturing and construction sectors.

High-purity argon emerged as the fastest-growing type segment, accounting for around 13% of total regional demand. Semiconductor-grade argon production crossed 760,000 metric tons during 2025, with purity levels exceeding 99.9999%. Electronics manufacturing facilities increasingly utilized high-purity argon in plasma deposition, laser optics, and microchip fabrication processes. France and Germany represented nearly 57% of specialty-grade consumption, driven by rising investments in semiconductor research and advanced electronics manufacturing infrastructure.

BY APPLICATION

Metal fabrication remained the leading application segment, accounting for approximately 31% of total argon consumption across Europe in 2025. Industrial welding operations consumed more than 1.8 million metric tons of argon for shielding gas applications in automotive, aerospace, railway, and heavy machinery manufacturing. Robotic welding systems improved operational productivity by nearly 24% while reducing oxidation defects by 18%. Germany alone operated over 35,000 automated welding units requiring continuous argon supply. Increasing adoption of TIG and MIG welding technologies continues driving industrial gas demand across fabrication sectors.

The electronics application segment accounted for nearly 22% of regional demand due to increasing semiconductor manufacturing and electronics assembly activities. Europe consumed approximately 1.27 million metric tons of argon in semiconductor processing, display manufacturing, and photovoltaic applications during 2025. High-purity argon usage in wafer fabrication improved contamination control by nearly 31%, enabling precision chip manufacturing below 5 nm process technologies. France, Germany, and the United Kingdom collectively contributed over 68% of electronics-related argon demand due to expanding investments in advanced manufacturing infrastructure.

Healthcare applications represented around 14% of total argon utilization across Europe during 2025. Hospitals, biotechnology laboratories, and pharmaceutical companies consumed nearly 810,000 metric tons of liquid and gaseous argon for cryopreservation, laser surgeries, and plasma coagulation technologies. Medical-grade argon systems demonstrated thermal efficiency improvements above 22% in cryogenic storage environments. Increasing cancer treatment procedures and stem cell preservation activities significantly boosted demand across major healthcare economies including the United Kingdom, France, and Italy.

Europe Argon Gas Market Segmentations

By Type

- Liquid Argon

- Gaseous Argon

- High-Purity Argon

By Application

- Metal Fabrication

- Electronics

- Healthcare

Europe Argon Gas Regional Outlook

United Kingdom

The United Kingdom accounted for nearly 24% of Europe argon consumption during 2025, supported by strong industrial manufacturing and healthcare infrastructure. The country produced approximately 1.36 million metric tons of industrial argon annually through more than 48 air separation facilities. Automotive and aerospace sectors together represented nearly 39% of domestic demand due to high adoption of automated welding systems and advanced material processing technologies. Healthcare applications contributed 18% of national consumption, while electronics manufacturing held approximately 16% share. Investments in offshore wind infrastructure and hydrogen pipeline manufacturing accelerated demand for high-purity argon across fabrication industries.

Germany

Germany represented the largest regional consumer with approximately 27% market share in 2025. The country operated over 72 industrial gas production facilities and consumed nearly 1.58 million metric tons of argon annually. Automotive manufacturing alone accounted for nearly 41% of industrial gas demand, supported by extensive robotic welding integration and electric vehicle production. Semiconductor manufacturing investments exceeding USD 5.2 billion further accelerated high-purity argon utilization. Germany also expanded cryogenic storage infrastructure for biotechnology and pharmaceutical applications, increasing healthcare-related argon consumption by 12.6%.

France

France accounted for nearly 15% of total regional consumption and produced approximately 920,000 metric tons of industrial argon during 2025. Electronics and semiconductor manufacturing contributed around 26% of domestic demand due to expanding advanced chip fabrication facilities. Healthcare applications represented 19% share, supported by increasing cryosurgery and biotechnology activities. France also invested heavily in hydrogen infrastructure and renewable energy equipment manufacturing, generating substantial demand for precision welding gases. Industrial automation adoption exceeded 61% among large-scale fabrication facilities, reinforcing stable argon consumption growth.

Spain

Spain contributed approximately 11% of Europe argon demand during 2025, supported by rising construction equipment manufacturing and automotive production. The country consumed nearly 640,000 metric tons of argon, with metal fabrication applications accounting for around 37% of usage. Robotic welding installations increased by nearly 14% year-over-year, accelerating industrial gas demand. Renewable energy manufacturing and solar panel assembly sectors also boosted high-purity argon consumption across electronics and photovoltaic applications. Expansion of industrial export activities continues strengthening domestic argon utilization.

Italy

Italy held approximately 13% regional share and consumed over 760,000 metric tons of argon during 2025. Industrial welding and metal processing applications represented more than 43% of domestic consumption due to strong machinery manufacturing and automotive component production. Italy also expanded medical gas infrastructure across hospitals and biotechnology centers, increasing healthcare argon demand by approximately 10.8%. Investments in advanced laser welding technologies and aerospace manufacturing further accelerated specialty-grade argon utilization across industrial sectors.

Russia

Russia accounted for nearly 10% of Europe argon production and consumption during 2025, supported by heavy industrial manufacturing and steel production activities. Total argon consumption exceeded 590,000 metric tons, with metallurgy and welding operations representing approximately 52% of total demand. The country operated more than 36 major cryogenic gas facilities supplying industrial and energy sectors. Despite logistical and geopolitical constraints, domestic investments in infrastructure manufacturing and defense-related production continued sustaining industrial gas utilization.

Top players in Europe Argon Gas

- Linde plc

- Air Liquide

- Air Products and Chemicals Inc.

- Messer Group GmbH

- Nippon Gases

- SOL Group

- Praxair Technology Inc.

- Taiyo Nippon Sanso Corporation

- SIAD S.p.A.

- BASF SE

- BOC Limited

- Gazprom Industrial Holdings

- Cryotec Anlagenbau GmbH

- Coregas Pty Ltd

- Westfalen AG

Linde plc

-

Linde plc accounted for approximately 22% regional revenue share in 2025 through its extensive industrial gas production network across Europe.

-

The company operated more than 85 air separation facilities and supplied over 1.4 million metric tons of argon annually to automotive, electronics, and healthcare industries.

-

Linde expanded semiconductor-grade gas production capacity by nearly 18% in Germany and the United Kingdom to address increasing electronics manufacturing demand.

-

The company also invested in argon recycling technologies capable of reducing industrial gas waste by approximately 20%, strengthening its leadership position in specialty industrial gases.

Air Liquide

-

Air Liquide held nearly 18% market share across Europe during 2025 and maintained strong positioning in healthcare and electronics applications.

-

The company supplied more than 1.1 million metric tons of industrial and specialty argon annually through integrated pipeline and bulk distribution systems.

-

Air Liquide expanded cryogenic storage infrastructure across France and Italy, increasing liquid argon supply efficiency by approximately 16%.

-

Investments in hydrogen infrastructure, renewable energy manufacturing, and semiconductor supply agreements further strengthened the company’s regional industrial gas portfolio.

Investment Analysis

Europe attracted more than USD 42 billion in industrial gas and clean manufacturing investments during 2025, with approximately 36% allocated toward semiconductor manufacturing and advanced electronics infrastructure. Renewable energy manufacturing accounted for nearly 28% of total investments, while healthcare and biotechnology sectors represented 17%. Germany and the United Kingdom together contributed more than 49% of total industrial gas infrastructure investments across Europe. Large-scale expansion of cryogenic air separation facilities increased argon production capacity by approximately 11.3% year-over-year.

Mergers, acquisitions, and strategic collaborations intensified across the industrial gas sector as companies sought supply security and regional expansion. More than 18 major collaboration agreements were announced during 2025 involving semiconductor manufacturers, steel producers, and industrial gas suppliers. Air Liquide and several renewable energy developers signed long-term supply agreements supporting hydrogen pipeline manufacturing and offshore wind infrastructure fabrication. Linde plc also invested over USD 1.2 billion in advanced industrial gas purification technologies and semiconductor-grade gas facilities. Joint ventures focused on gas recycling technologies improved operational efficiency by approximately 19%, while reducing industrial emissions and waste generation.

Investments in healthcare and biotechnology infrastructure also accelerated regional argon demand. Cryogenic storage systems and plasma coagulation technologies attracted approximately 14% of total industrial gas investments across Europe during 2025. France and Italy expanded medical gas distribution networks and surgical technology facilities, supporting long-term specialty argon demand growth.

New Product Developments

Industrial gas manufacturers increasingly introduced advanced high-purity argon solutions designed for semiconductor and aerospace manufacturing applications. During 2025, more than 22% of newly launched industrial gas products focused on ultra-high-purity formulations exceeding 99.9999% purity levels. These innovations improved contamination control by approximately 28% in wafer fabrication and precision laser applications. Automated gas monitoring systems integrated with AI-enabled leak detection technologies reduced operational losses by nearly 17%.

Several manufacturers also introduced compact liquid argon storage systems capable of improving thermal efficiency above 98% while reducing transportation costs by approximately 14%. Healthcare-focused innovations included argon plasma coagulation systems with enhanced energy precision and reduced tissue damage rates by 11%. Sustainable gas recycling systems capable of recovering nearly 75% of industrial argon volumes from fabrication environments further strengthened technological advancement across Europe.

Recent Developments in Europe Argon Gas

- 2025: Linde plc expanded its semiconductor-grade argon purification facility in Germany by 18%, increasing annual production capacity above 210,000 metric tons. The project supported rising semiconductor fabrication demand and reduced delivery lead times by approximately 12% across Europe.

- 2025: Air Liquide signed a long-term supply agreement with multiple hydrogen infrastructure developers in the United Kingdom, increasing industrial argon supply volumes by nearly 15% for renewable energy manufacturing and pipeline fabrication activities.

Research Methodology

The Europe argon industry analysis was developed using a combination of primary and secondary research methodologies to ensure accurate market forecasting and competitive assessment. The research process included extensive data collection from industrial gas manufacturers, distributors, semiconductor producers, healthcare institutions, and manufacturing companies across Europe. Primary research involved interviews with over 65 industry executives, plant managers, technology specialists, and procurement professionals to evaluate production capacities, pricing trends, technological adoption, and demand distribution patterns.

Secondary research incorporated industrial databases, trade publications, financial reports, government manufacturing statistics, and industrial gas association data covering the historical period from 2022 to 2024. Market size estimation utilized bottom-up and top-down analytical approaches supported by consumption volume analysis, production benchmarking, and sector-wise revenue mapping. Forecast modeling considered industrial automation rates, semiconductor investment trends, healthcare expansion, renewable energy infrastructure growth, and regional manufacturing output. Data triangulation techniques and validation through multiple supply-side and demand-side indicators ensured reliable forecasting accuracy for the Europe argon industry during the 2026–2034 forecast period.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.