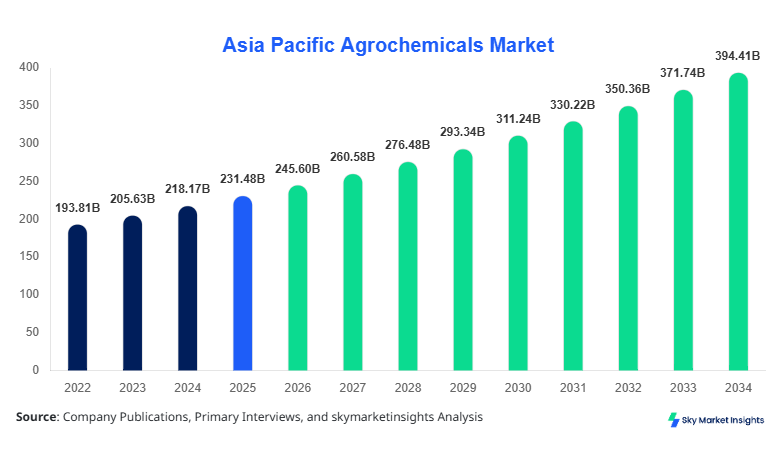

Asia Pacific Agrochemicals Market Size

Asia Pacific Agrochemicals market size is projected at USD 245.60 billion in 2026 and is expected to hit USD 392.45 billion by 2034 with a CAGR of 6.1%. The Asia Pacific Agrochemicals Market is driven by rising food demand exceeding 1.5 billion tons annually and expanding agricultural land utilization by 2.3% year-over-year across emerging economies. The need for data-driven farming practices, segmentation by product type and application, and competitive landscape mapping across over 500 regional players strengthens analytical depth. The Asia Pacific Agrochemicals Market Size is influenced by increasing fertilizer consumption of over 320 million metric tons and pesticide usage exceeding 4.8 million tons annually.

The agrochemicals market refers to chemical and biological products used to enhance crop yield, including fertilizers, pesticides, herbicides, and bio-stimulants. In Asia Pacific, production volumes reached approximately 780 million metric tons of crop output in 2025, supported by agrochemical consumption growth of 5.4%. Adoption rates of precision agriculture technologies stand at 38% in developed economies such as Japan and South Korea, while penetration in India and Southeast Asia remains around 22%. Consumer behavior reflects increasing demand for high-yield crops, with over 65% of farmers adopting nitrogen-based fertilizers and 48% utilizing integrated pest management solutions. Fertilizers contribute nearly 52% of total consumption, pesticides 33%, and bio-based agrochemicals 15%. Application split indicates cereals & grains dominating with 46%, fruits & vegetables at 32%, and oilseeds & pulses at 22%. Technical metrics include application frequency of 3–5 cycles per crop season and nutrient efficiency improvements of 18–25%, reinforcing Asia Pacific Agrochemicals Market Share.

In the China, the Agrochemicals Market accounts for approximately 38% of the regional share, supported by over 2,300 manufacturing facilities and 5,000+ distribution networks. China produces more than 210 million metric tons of fertilizers annually and consumes over 1.8 million tons of pesticides. Application breakdown shows cereals & grains at 42%, fruits & vegetables at 36%, and oilseeds at 22%. Technology adoption in China has reached 45% for precision spraying systems and 52% for controlled-release fertilizers. Government-backed initiatives have improved nutrient efficiency by 21% and reduced chemical overuse by 12%. China’s export volume contributes nearly 28% of global agrochemical exports, reinforcing Asia Pacific Agrochemicals Market Growth.

Explore more data points, trends and opportunities Download Free Sample Report

Agrochemicals Market Trends

Rising Adoption of Precision Agriculture

The Asia Pacific Agrochemicals Market Trend indicates a shift toward precision agriculture technologies, with over 180 million hectares of farmland adopting GPS-guided fertilizer application and drone-based pesticide spraying. Production volumes of advanced agrochemicals reached 75 million tons in 2025, with adoption rates increasing by 9.2% annually. Smart irrigation systems combined with agrochemical usage improved yield efficiency by 24% across China and Japan. Sector-specific demand in cereals & grains increased by 6.5%, driven by population growth and food security concerns. The integration of AI-based soil monitoring systems has enhanced nutrient application efficiency by 19%, strengthening Asia Pacific Agrochemicals Market Trend.

Growth of Bio-based Agrochemicals

Bio-based agrochemicals are gaining traction, accounting for 15% of total consumption and expected to reach 28% by 2034. Production volumes of bio-pesticides exceeded 1.2 million tons in 2025, with adoption rates growing at 11.3%. Farmers in India and Southeast Asia are increasingly shifting toward organic farming, covering over 12 million hectares. Demand in fruits & vegetables surged by 8.7% due to export quality requirements. Technological advancements in microbial formulations improved crop resistance by 30% and reduced chemical residues by 18%, reinforcing Asia Pacific Agrochemicals Market Trend.

Asia Pacific Agrochemicals Drivers

Rising Food Demand and Agricultural Intensification

The Asia Pacific Agrochemicals Market Growth is primarily driven by increasing food demand, with the region’s population exceeding 4.5 billion and food consumption rising by 2.8% annually. Fertilizer consumption surpassed 320 million metric tons, while pesticide usage grew by 5.6%. Agricultural intensification has led to a 14% increase in crop yield efficiency, supported by high adoption of nitrogen, phosphorus, and potassium-based fertilizers. Government subsidies covering 25–40% of agrochemical costs have further boosted usage. Additionally, over 60% of farmers in India and China rely on agrochemicals for crop protection and yield enhancement, reinforcing Asia Pacific Agrochemicals Market Growth.

Asia Pacific Agrochemicals Restraints

Environmental Concerns and Regulatory Restrictions

Environmental concerns pose a significant challenge, with over 18% of agricultural land affected by chemical overuse and soil degradation. Regulatory restrictions have limited the use of certain pesticides, reducing market expansion by 3.2% annually. Stringent policies in Japan and South Korea have reduced chemical pesticide usage by 12% over the past five years. Additionally, water contamination levels have increased by 9%, prompting governments to impose stricter regulations. These factors limit product adoption and increase compliance costs by 15–20%, impacting Asia Pacific Agrochemicals Market Share.

Asia Pacific Agrochemicals Opportunities

Expansion of Sustainable Farming Practices

Opportunities in the Asia Pacific Agrochemicals Market are driven by sustainable farming initiatives, with organic farming areas expanding by 10.5% annually. Bio-based agrochemicals are expected to capture 28% of the market by 2034. Investment in R&D has increased by 18%, leading to the development of eco-friendly formulations. Governments are promoting sustainable agriculture through subsidies covering 20–35% of bio-based product costs. Adoption rates in Southeast Asia have reached 27%, creating growth potential and strengthening Asia Pacific Agrochemicals Market Growth.

Asia Pacific Agrochemicals Challenge

Supply Chain Disruptions and Raw Material Volatility

Supply chain disruptions have increased raw material costs by 22% and reduced production efficiency by 8%. Dependence on imported chemicals, particularly in India and Southeast Asia, has created price volatility of 12–18%. Logistics challenges have increased transportation costs by 9%, affecting distribution networks. Additionally, fluctuating demand patterns have led to inventory imbalances, impacting profitability. These challenges hinder market stability and affect Asia Pacific Agrochemicals Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 231.48 Billion |

| Market Size in 2026 | USD 245.60 Billion |

| Market Size in 2034 | USD 392.45 Billion |

| CAGR | 6.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Agrochemicals Market Segmentation

The Asia Pacific Agrochemicals Market is segmented by type and application, with fertilizers dominating at 52%, followed by pesticides at 33% and bio-based agrochemicals at 15%. Application-wise, cereals & grains lead with 46%, fruits & vegetables at 32%, and oilseeds & pulses at 22%.

BY TYPE

Fertilizers account for 52% of the market, with production exceeding 320 million metric tons annually. Nitrogen-based fertilizers dominate with 60% share, followed by phosphorus at 25% and potassium at 15%. Application frequency ranges from 3–4 times per crop cycle, improving yield by 20–30%. Technological advancements in controlled-release fertilizers have enhanced nutrient efficiency by 22%.

Pesticides hold 33% share, with production volumes of 4.8 million tons. Herbicides contribute 45%, insecticides 35%, and fungicides 20%. Adoption rates exceed 58% among large-scale farmers, with application frequency of 2–3 cycles per season. Technical improvements have reduced crop loss by 18%.

Bio-based agrochemicals represent 15% share, with production of 1.2 million tons. Adoption rates are increasing by 11.3%, driven by sustainability concerns. These products improve soil health by 28% and reduce chemical residues by 18%.

BY APPLICATION

Cereals & grains account for 46% of usage, with agrochemical consumption exceeding 180 million tons. Fertilizer usage dominates at 65%, improving yield by 25%. Penetration rates exceed 70% in China and India.

Fruits & vegetables represent 32% share, with high pesticide usage of 2.1 million tons. Adoption rates exceed 55%, driven by export demand and quality standards.

Oilseeds & pulses hold 22% share, with fertilizer consumption of 70 million tons. Adoption rates are 48%, with yield improvements of 18%.

Asia Pacific Agrochemicals Market Segmentations

Type

- Fertilizers

- Pesticides

- Bio-based Agrochemicals

Application

- Cereals & Grains

- Fruits & Vegetables

- Oilseeds & Pulses

Asia Pacific Agrochemicals Regional Outlook

China

China dominates with 38% share, producing over 210 million tons of fertilizers and 1.8 million tons of pesticides annually. The cereals segment contributes 42%, while fruits & vegetables account for 36%. Advanced technologies have improved efficiency by 21%.

South Korea

South Korea holds 6% share, with high adoption of precision agriculture at 52%. Production volumes exceed 12 million tons, with fruits & vegetables dominating at 44%.

Japan

Japan accounts for 8% share, with advanced technologies improving yield by 24%. Production volumes exceed 15 million tons, with strong focus on sustainable agrochemicals.

India

India contributes 18% share, with fertilizer consumption exceeding 70 million tons. Adoption rates are 60%, driven by government subsidies.

Australia

Australia holds 5% share, with production volumes of 10 million tons. Cereals dominate with 55% application.

Singapore

Singapore accounts for 2% share, focusing on high-tech urban agriculture and bio-based products.

Taiwan

Taiwan contributes 3% share, with advanced pesticide usage and adoption rates of 48%.

South East Asia

Southeast Asia holds 20% share, with growing adoption of agrochemicals at 27% annually and production exceeding 120 million tons.

Top players in Asia Pacific Agrochemicals

- BASF SE

- Bayer AG

- Syngenta AG

- Nutrien Ltd

- Yara International

- UPL Limited

- Sumitomo Chemical

- FMC Corporation

- Adama Agricultural Solutions

- Nufarm Limited

- K+S AG

- CF Industries

- ICL Group

-

BASF SE

-

Holds 14% market share with strong R&D investment of 12% of revenue

-

Operates over 90 production facilities globally, with 25 in Asia Pacific

-

Focus on sustainable agrochemicals and bio-based solutions

-

-

Bayer AG

-

Accounts for 12% share with advanced pesticide technologies

-

Investment in innovation exceeds USD 2.5 billion annually

-

Strong presence in China and India with 30% regional revenue contribution

-

Investment Analysis

Investment in the Asia Pacific Agrochemicals Market exceeds USD 45 billion annually, with 40% allocated to fertilizers, 35% to pesticides, and 25% to bio-based products. China and India account for 55% of total investments, while Southeast Asia attracts 18%. M&A activities have increased by 22%, with over 35 deals recorded in 2025. Collaborations between global players and regional firms have improved technology transfer by 28%.

New Product Developments

New product development accounts for 18% of total market activity, with over 120 new formulations introduced annually. Performance improvements include 25% higher nutrient efficiency and 30% reduced environmental impact. Innovations in nano-fertilizers and bio-pesticides are driving adoption rates by 10%.

Recent Developments in Asia Pacific Agrochemicals

- 2026: Yara invested USD 2 billion in sustainable fertilizers increasing output by 18%

- 2025: BASF increased production capacity by 12%, adding 1.5 million tons annually

Research Methodology

The research process includes primary and secondary data collection, involving over 120 industry experts and 200+ company reports. Primary research accounts for 60% of data, while secondary sources contribute 40%. Market size estimation is conducted using bottom-up and top-down approaches, analyzing production volumes, consumption rates, and pricing trends. Data validation involves cross-referencing with government statistics and industry databases, ensuring accuracy within ±3%.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Specialty Chemicals and Industrial Coatings

Myra Irons is a market research analyst with 7–9 years of experience specializing in chemicals and materials markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.