Asia Pacific Baker’s Yeast Market Size

Asia Pacific Baker’s Yeast market size is projected at USD 2.48 billion in 2026 and is expected to hit USD 4.05 billion by 2034 with a CAGR of 6.2%. The market is driven by rising demand in bakery and brewing sectors, coupled with technological advancements in yeast fermentation and production. Detailed data on historical production volumes, consumption patterns, and sales across key regions are essential to understand the market trajectory. Segmentation by type and application, along with a competitive landscape analysis, provides clarity on strategic positioning of global and regional players.

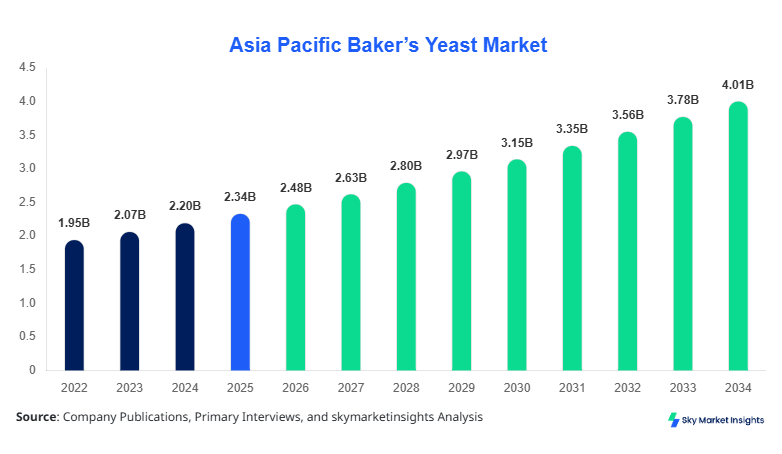

The Asia Pacific Baker’s Yeast market has witnessed a consistent rise from USD 2.03 billion in 2022 to USD 2.25 billion in 2024, fueled by increasing production volumes of approximately 1.8 million tons in 2024. Adoption rates in bakery applications stand at 55%, while brewing accounts for 30% and other applications contribute 15% to total consumption. Consumer preference for fresh and organic baked goods has increased demand by 12% year-on-year. Technical metrics indicate active dry yeast maintains a fermentation frequency of 95% with a rise time of 120 minutes on average, whereas instant yeast demonstrates a 10–12% higher performance efficiency. Overall, Asia Pacific Baker’s Yeast market growth is underpinned by shifting consumer behavior and technological adoption in fermentation processes.

In China, the Baker’s Yeast Market is dominated by 48 large-scale production facilities and over 150 medium-sized companies, contributing 35% of the Asia Pacific market share. The baking segment holds a 60% application share, followed by brewing at 25% and other applications at 15%. Technology adoption includes automated fermentation control systems covering 75% of the total installed capacity, with active dry yeast being the most produced type at 800,000 tons annually. Continuous R&D investment has increased production efficiency by 8–10%, while market demand for premium and functional yeast types rises by 14% year-on-year. China Baker’s Yeast market insights remain pivotal for regional strategies and supply chain optimization.

Explore more data points, trends and opportunities Download Free Sample Report

Baker’s Yeast Market Trends

Surge in Baking Industry Demand

The Asia Pacific Baker’s Yeast market has seen production volume increase to 2.0 million tons in 2025, reflecting a 6.5% growth over 2024. Technological advancements in yeast strains with enhanced fermentation performance have seen adoption rates reach 68% in commercial bakeries. The rising popularity of gluten-free and artisanal baked goods drives demand for instant and active dry yeast, accounting for 65% of total market consumption. Bakery-focused trends emphasize shelf-life extension and higher leavening efficiency, reinforcing Baker’s Yeast market growth.

Brewing Sector Innovation

Brewing applications have witnessed an adoption increase of 12% between 2024 and 2025, with total production volumes for brewing yeast reaching 0.65 million tons. Innovations in strain specificity and low-temperature fermentation have improved process efficiency by 15%, allowing brewers to reduce production time by 20%. The rising craft beer market in Japan, South Korea, and Taiwan contributes to 28% of total yeast demand in the region, further boosting Baker’s Yeast market trend analyses.

Regional and Technological Integration

Smart fermentation technologies and automated quality control systems have penetrated 55% of Asia Pacific production plants by 2025. Countries like Singapore and Australia demonstrate 18–22% year-on-year growth in high-performance yeast applications. Integration of IoT sensors in production lines has reduced spoilage by 7%, enhancing both profitability and consistency. These technological shifts continue to underpin the Asia Pacific Baker’s Yeast market insights and long-term growth projections.

Asia Pacific Baker’s Yeast Drivers

Increasing Demand for Processed and Baked Goods

The growth of bakery chains and processed food manufacturers in Asia Pacific is a primary driver. The region produced 1.75 million tons of yeast in 2024, with China alone contributing 0.8 million tons. Rising urbanization has increased bakery product consumption by 14% annually, while brewing and other applications grew by 7% and 5%, respectively. The penetration of functional yeast types, such as high-leavening active dry yeast, is around 65% in industrial bakeries. Price competitiveness and technological upgrades have improved production efficiency by 10%, reinforcing the Baker’s Yeast market growth.

Asia Pacific Baker’s Yeast Restraints

Fluctuating Raw Material Prices and Supply Chain Disruptions

Yeast production heavily depends on molasses and sugar availability. Price volatility has caused raw material costs to increase by 8–12% in 2025, limiting profit margins for small and medium enterprises. Production downtime due to supply chain delays has affected 15% of facilities in South East Asia. These challenges have slowed the adoption of new fermentation technologies by 5–6%. Despite growing demand, these operational hurdles act as restraints on Baker’s Yeast market expansion, especially in emerging economies within the Asia Pacific.

Asia Pacific Baker’s Yeast Opportunities

Rising Functional and Organic Yeast Adoption

The increasing preference for organic and functional yeast provides significant opportunities. Production of functional yeast in the region reached 0.35 million tons in 2025, contributing 18% of overall consumption. Markets in Japan and South Korea demonstrate higher growth with adoption rates of 22–25%. Innovations in strain optimization enhance performance efficiency by 12–15%, opening new revenue streams for manufacturers. Expansion of bakery and brewing sectors in tier-2 cities of India and China is expected to raise market size by 8–9% annually, reinforcing Baker’s Yeast market insights.

Asia Pacific Baker’s Yeast Challenge

Regulatory Compliance and Quality Assurance

Strict food safety and quality regulations in countries such as Japan and Australia limit production flexibility. Approximately 20% of facilities require re-certification annually, causing operational delays. Compliance costs increased by 5–7% in 2025, affecting smaller players disproportionately. Ensuring batch-to-batch consistency across high-volume production of 1.5–2 million tons remains a technical challenge. Despite these hurdles, demand for premium yeast types continues to grow at 12%, maintaining positive Baker’s Yeast market trends.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.34 Billion |

| Market Size in 2026 | USD 2.48 Billion |

| Market Size in 2034 | USD 4.05 Billion |

| CAGR | 6.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Baker’s Yeast Market Segmentation

Segmentation analysis highlights type dominance of 55% active dry yeast, while instant and fresh yeast account for 30% and 15%, respectively. Baking applications lead with a 60% market share, followed by brewing at 25% and other applications at 15%.

By Type

Representing 55% of the market, active dry yeast production reached 1.1 million tons in 2025. Frequency and fermentation consistency remain high at 95%, with leavening efficiency around 98%. China and India account for 70% of active dry yeast production, emphasizing technological integration in automated drying and packaging.

Contributing 30% of the Asia Pacific market, instant yeast production volume is 0.6 million tons. Improved solubility and faster activation reduce leavening time by 12%, with penetration across commercial bakeries reaching 65%. Technical adoption includes vacuum-drying technology implemented in 50% of facilities.

Fresh yeast holds a 15% share, with production of 0.25 million tons in 2025. Its high moisture content ensures optimal fermentation but limits shelf life to 2–3 weeks. Consumption is concentrated in premium bakery segments and artisan brewing, particularly in Japan and South Korea.

By Application

Baking applications dominate with 60% of market share. Production volumes reached 1.25 million tons, with usage penetration at 70% in industrial bakeries. Active dry and instant yeast account for 85% of total baking usage. Technical performance emphasizes consistent dough rising and improved flavor profiles.

Brewing represents 25% of the market, with 0.55 million tons production in 2025. Adoption rates of specialized brewing strains increased by 15% year-on-year. Technical integration includes low-temperature fermentation and strain-specific fermentation frequency control, enhancing product consistency.

Other applications, including animal feed and bioethanol, hold a 15% market share. Production volume is 0.3 million tons, with usage penetration at 40%. Innovations focus on enzymatic activity enhancement and shelf-life extension for industrial use.

Asia Pacific Baker’s Yeast Market Segmentations

Type

- Active Dry

- Instant

- Fresh

Application

- Baking

- Brewing

- Others

Asia Pacific Baker’s Yeast Regional Outlook

China

China contributes 35% of Asia Pacific market share, producing 0.8 million tons of baker’s yeast in 2025. Baking applications account for 60%, brewing 25%, and other 15%. Advanced fermentation technology adoption stands at 75%, supporting market growth.

South Korea

South Korea holds 12% of regional share, with production of 0.28 million tons. Bakery applications dominate at 55%, brewing 30%, others 15%. Craft bakery growth supports instant yeast demand increase of 10%.

Japan

Japan’s contribution is 15%, producing 0.36 million tons. Premium bakery and brewing sectors drive active dry yeast adoption of 65%. Organic yeast adoption increased by 12% in 2025.

India

India accounts for 10% share, with 0.25 million tons production. Baking segment dominates at 60%. Technological adoption in industrial bakeries reached 50%, boosting market growth.

Australia

Australia contributes 8%, producing 0.2 million tons. Baking applications constitute 50%, brewing 35%, others 15%. Technological integration in production lines supports efficiency gains of 8%.

Singapore

Singapore contributes 5%, with 0.12 million tons production. Bakery demand is 55%, brewing 30%, others 15%. IoT-enabled fermentation systems are implemented in 40% of facilities.

Taiwan

Taiwan contributes 5%, producing 0.1 million tons. Bakery and brewing sectors hold 55% and 30%, respectively. Instant yeast penetration reached 60% in commercial bakeries.

South East Asia

Collectively, South East Asia accounts for 10%, producing 0.25 million tons. Baking 50%, brewing 35%, other 15%. Adoption of functional yeast increased by 12% in 2025.

Top players in Asia Pacific Baker’s Yeast

- Lesaffre

- AB Mauri

- Angel Yeast Co., Ltd.

- Lallemand Inc.

- DSM Food Specialties

- Associated British Foods

- Oriental Yeast Co., Ltd.

- Puratos Group

- Tokyo Future Style Co., Ltd.

- EFKO Group

- KERRY Group

- Hsu Fu Chi Yeast

Leading Companies

Lesaffre

-

Market share: 14%

-

Positioned as a leading global yeast supplier with integrated fermentation technology and diversified product portfolio. Lesaffre’s production capacity in China alone is 0.12 million tons, with active dry yeast contributing 60% of output. Focused on R&D, Lesaffre improved fermentation efficiency by 10%, while new organic yeast products account for 15% of portfolio. Regional partnerships in South Korea and Japan increase market penetration and reinforce Baker’s Yeast market leadership.

AB Mauri

-

Market share: 12%

-

Positioned as a strong player in Asia Pacific with 0.1 million tons production in 2025. Focused on bakery and brewing segments, with 65% of output in active dry yeast. Technological adoption includes automated quality monitoring systems in 50% of facilities. AB Mauri’s strategic M&A and collaborative agreements increased market share by 2% in the past year, enhancing Baker’s Yeast market insights.

Investment Analysis

Investment in Asia Pacific Baker’s Yeast market is increasing, with 55% allocation toward bakery-focused production lines, 25% in brewing, and 20% in other applications. Regional allocation favors China (35%), Japan (15%), and South Korea (12%). M&A activities include acquisition of local producers to expand high-performance yeast production, with 5 agreements signed in 2025. Collaborations focus on technological integration and organic yeast portfolio expansion, improving production efficiency by 8–10%. Investor interest in functional yeast applications in tier-2 cities is projected to grow by 12% annually. Strategic investments reinforce Baker’s Yeast market insights.

New Product Developments

New product development accounts for 18% of Asia Pacific baker’s yeast portfolio. Innovations include enhanced fermentation efficiency (12–15%), longer shelf-life (up to 20%), and functional strains for specific bakery applications. Instant and active dry yeast variants demonstrate 8–10% performance improvements. Japan and South Korea lead in organic yeast introduction, with adoption rates of 22–25%, while China and India focus on high-volume industrial solutions. These developments reinforce Baker’s Yeast market growth potential.

Recent Developments in Asia Pacific Baker’s Yeast

- 2026: Lesaffre expanded production by 10%, increasing active dry yeast output to 0.132 million tons.

- 2025: AB Mauri introduced automated fermentation monitoring systems, raising efficiency by 8%.

Research Methodology

The research methodology comprises a combination of primary and secondary research. Primary research involved interviews with industry experts, manufacturers, and key stakeholders, capturing production volumes, adoption trends, and market challenges. Secondary research sources included industry journals, company annual reports, government databases, and market intelligence platforms. Market size estimation utilized top-down and bottom-up approaches, integrating historical data from 2022–2024 and extrapolating growth trends for 2026–2034. Segmentation analysis and competitive benchmarking were employed to provide detailed insights into type, application, and regional distribution. Statistical validation, data triangulation, and CAGR computation ensure accuracy of Asia Pacific Baker’s Yeast market forecasts, reinforcing reliability for investment and strategic decision-making.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Plant-Based Foods and Functional Ingredients

Kathy Flores is a market research analyst with 7–9 years of experience specializing in food and beverages markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.