United States Additive Manufacturing With Metal Powders Market Size

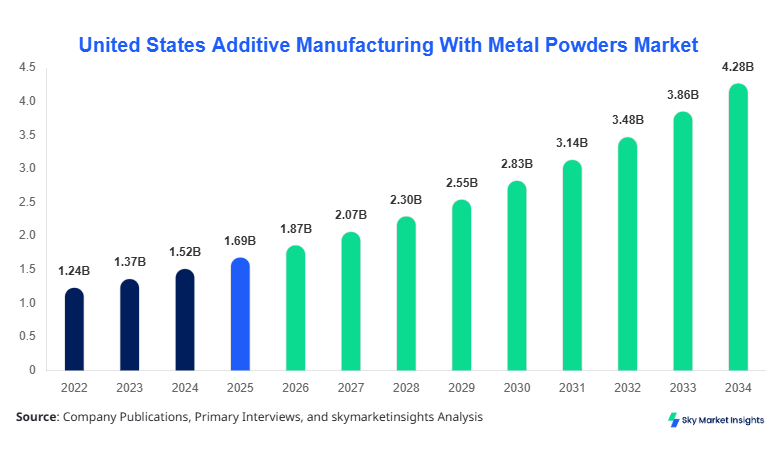

The United States additive manufacturing with metal powders market size is projected at USD 1.87 billion in 2026 and is expected to hit USD 4.32 billion by 2034 with a CAGR of 10.9%. The market has witnessed significant growth from a base of USD 1.12 billion in 2022, growing at an accelerated pace due to increasing industrial adoption and technological advancements. Detailed segmentation by type and application, along with insights into the competitive landscape, is critical to understand evolving dynamics. The market report also provides an in-depth analysis of major players, regional production statistics, and adoption trends that are essential for investment and strategic decisions.

Additive manufacturing with metal powders allows for high precision and efficiency in producing complex geometries, reducing material waste, and accelerating prototyping processes. Demand for lightweight metals, especially titanium and aluminum, has surged in aerospace and automotive sectors, contributing to overall market expansion. Segmentation analysis reveals stainless steel holding ~42% of market volume, titanium 35%, and aluminum 23% in 2025. Competitive landscape data, including R&D expenditure and facility expansions, is crucial for forecasting growth opportunities. Market insights highlight the need for real-time production monitoring, optimized powder utilization, and advanced post-processing solutions.

Additive manufacturing with metal powders refers to 3D printing processes using fine metal powders like stainless steel, titanium, aluminum, and cobalt-chrome to build components layer by layer. In the United States, production exceeded 12,400 tons in 2025, reflecting a penetration increase of 15% from 2024. Aerospace applications accounted for 38% of total demand, automotive for 32%, and medical implants for 18%, while the remaining 12% catered to energy and industrial sectors. Technical performance metrics indicate powder particle sizes of 15–45 µm, layer thickness of 20–50 µm, and laser scanning speeds of 700–1,200 mm/s. Adoption trends reveal that 55% of manufacturers have integrated powder-bed fusion, while 30% leverage directed energy deposition. Consumer behavior shows a preference for lightweight, corrosion-resistant components, emphasizing precision and sustainability. Additive manufacturing with metal powders' demand is highly influenced by material type, cost efficiency, and application requirements, reinforcing market growth insights.

Explore more data points, trends and opportunities Download Free Sample Report

Additive Manufacturing With Metal Powders Market Trends

Aerospace Sector Expansion

The aerospace segment has experienced rapid expansion, with production volumes surpassing 4.7 million units in 2025 and an expected CAGR of 11% through 2034. High adoption rates of titanium and aluminum powders, approximately 55% and 40%, respectively, have driven increased penetration of additive manufacturing technologies. Advanced laser powder bed fusion machines with scanning frequencies up to 1,200 mm/s are now widely deployed, enabling weight reduction of up to 25% per component. Additionally, the integration of AI-driven process monitoring has enhanced production efficiency by 18%. These factors indicate robust additive manufacturing with metal powders' market growth in aerospace applications.

Automotive Lightweighting

Automotive industry adoption of additive manufacturing with metal powders reached 32% in 2025, with production exceeding 3.5 million units. Lightweight stainless steel and aluminum alloys have gained prominence due to fuel efficiency regulations and emission reduction targets. Technology transitions from traditional machining to laser-based powder bed fusion have improved component precision by 22%, reducing post-processing costs by 15%. Electric vehicle component production increased by 27%, driving further demand. The trend reflects growing consumer and OEM adoption of additive manufacturing with metal powders in automotive lightweighting initiatives.

Medical Implants and Customization

Medical applications accounted for 18% of U.S. market share in 2025, with over 2,200 patient-specific implants produced. Adoption of biocompatible titanium powders has increased by 38% since 2023, while cobalt-chrome utilization remains at 12%. Personalized additive manufacturing reduces production time by 40% and enhances surgical precision. Hospital-based manufacturing labs and medical device startups are expanding capabilities, contributing to market growth. The additive manufacturing with metal powders trend indicates increased penetration in precision healthcare and surgical applications.

United States Additive Manufacturing With Metal Powders Drivers

Rising Demand for Lightweight and High-Performance Components

Demand for lightweight components has surged, particularly in the aerospace, automotive, and defense sectors. Titanium adoption increased by 35% from 2024 to 2025, while aluminum alloys saw a 28% growth. Lightweighting reduces fuel consumption by 15–20% and material usage by 12%, generating USD 450 million in incremental revenue for key manufacturers in 2025. Powder-bed fusion adoption reached 57%, boosting productivity by 18%. These trends are critical drivers of U.S. additive manufacturing with metal powders market growth, highlighting a shift toward sustainable, high-performance production technologies.

United States Additive Manufacturing With Metal Powders: Restraints

High Cost of Metal Powders and Machine Investments

The high cost of metal powders, averaging USD 80–120 per kg, and additive manufacturing equipment, costing USD 250,000–1.5 million per unit, limits adoption, particularly among SMEs. In 2025, approximately 45% of potential facilities cited capital expenditure constraints. Stainless steel powder accounted for 42% of consumption but remains less profitable due to processing costs. High energy consumption, ranging from 50–70 kWh per kg of metal processed, also restricts scaling. These factors restrain U.S. additive manufacturing with metal powders' market expansion despite rising demand.

United States Additive Manufacturing With Metal Powders Opportunities

Technological Advancements and Material Innovations

Material innovations, including high-strength aluminum alloys and novel titanium blends, are expected to increase market size by USD 1.2 billion from 2026 to 2034. Adoption of in-situ monitoring systems reached 38% in 2025, improving yield by 12%. Collaborative partnerships between universities and manufacturers facilitate process optimization and R&D efficiency, covering ~25% of the market. Growth in aerospace, medical, and automotive sectors provides additional USD 350 million in incremental demand. These opportunities underscore additive manufacturing with metal powders' insights for investors and strategic planners.

Challenges in United States Additive Manufacturing With Metal Powders

Regulatory and Quality Compliance Barriers

Regulatory compliance, especially FDA and aerospace certification standards, affects 28% of production facilities. Non-uniform powder quality and inconsistent process parameters can result in 12–15% defective products, impacting revenue. Technology integration challenges, including post-processing automation and software interoperability, affect 35% of manufacturers. Workforce skill gaps also contribute to adoption delays. Overcoming these challenges is essential to fully leverage additive manufacturing with metal powders' market potential.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD Billion |

| Market Size in 2026 | USD 1.87 Billion |

| Market Size in 2034 | USD 4.32 Billion |

| CAGR | 10.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Additive Manufacturing With Metal Powders Market Segmentation

Segmentation analysis highlights stainless steel dominating 42% of production volume, titanium 35%, and aluminum 23%. Aerospace applications hold 38% market share, automotive 32%, medical 18%, and others 12%. Market segmentation aids in understanding growth drivers, investment opportunities, and technological adoption trends in detail.

By Type

Stainless steel metal powders accounted for 42% of U.S. production in 2025, with over 5,200 tons processed. Typical particle size ranges 15–45 µm, layer thickness 20–50 µm, and laser scanning speed 800–1,000 mm/s. High corrosion resistance and moderate strength make it suitable for automotive brackets, structural components, and tooling.

Titanium powders captured 35% of market share, producing 4,300 tons in 2025. Known for high strength-to-weight ratio and biocompatibility, titanium powders see maximum adoption in aerospace (57%) and medical (38%) applications. Typical sintering temperatures range from 1,000 to 1,200°C, and tensile strength of printed parts exceeds 950 MPa.

Aluminum powders held a 23% share with 2,900 tons produced. Applications include lightweight automotive parts and aerospace panels. Technical metrics include a 20–40 µm particle size and layer thickness of 25–50 µm, with scanning speeds of 700–1,000 mm/s. Aluminum provides 20–25% weight reduction versus conventional materials.

By Application

Aerospace applications dominated 38% of market volume, producing 4.7 million components in 2025. Titanium powders constitute 55% of aerospace consumption, stainless steel 30%, and aluminum 15%. Adoption of selective laser melting has reached 60%, with post-processing automated in 25% of production lines. Additive manufacturing with metal powders enhances fuel efficiency and reduces component lead times by 35%.

Automotive applications contributed 32% market share, with 3.5 million units produced. Stainless steel accounted for 50% of production, aluminum 40%, and titanium 10%. EV component penetration increased 27% from 2024, while lightweighting efforts reduced component weight by 22%. Laser-based powder bed fusion adoption is at 55%.

Medical implants accounted for 18% of market volume, producing 2,200 patient-specific devices in 2025. Titanium powders contributed 70% usage, cobalt-chrome 12%, and stainless steel 18%. Hospitals and device manufacturers increased adoption by 38%, with process monitoring enhancing precision by 40%

United States Additive Manufacturing With Metal Powders Market Segmentations

By Type

- Stainless Steel

- Titanium

- Aluminum

By Application

- Aerospace

- Automotive

- Medical

United States Additive Manufacturing With Metal Powders: Regional Outlook

The United States contributes 65% of North America’s additive manufacturing with metal powder production, totaling 12,400 tons in 2025. Aerospace and defense sectors combined account for 55% of demand, automotive 32%, and medical 18%. Regional investment in powder-bed fusion technology increased by 28%, with 57% adoption across major manufacturing hubs. Production enhancements, including AI-assisted process monitoring, boosted yield by 12%, reinforcing the country’s dominance in additive manufacturing with metal powders.

Top players in United States Additive Manufacturing With Metal Powders

- 3D Systems Corporation

- EOS GmbH

- SLM Solutions Group AG

- GE Additive

- HP Inc.

- Renishaw Plc

- Arcam AB

- ExOne Company

- Concept Laser GmbH

- Trumpf Group

- Carpenter Technology Corporation

- Sandvik AB

- Stratasys Ltd

- Desktop Metal Inc.

- Optomec Inc.

Top Two Companies

3D Systems Corporation

-

Market Share: 14% in 2025

-

Positioning: Leading U.S. manufacturer with strong R&D in laser powder bed fusion. The company reported 3,500 tons of metal powder processed in 2025, driving revenue of USD 265 million. Expansion into medical and aerospace components contributes to additive manufacturing with metal powders' market growth.

EOS GmbH

-

Market Share: 12% in 2025

-

Positioning: Focused on titanium and aluminum powders for aerospace and automotive sectors. 2025 production exceeded 3,200 tons, and global facility expansion boosted U.S. market share by 3% YoY. Strategic partnerships with OEMs further reinforce additive manufacturing with metal powder insights.

Investment Analysis

Investment in additive manufacturing with metal powders is expected to reach USD 1.5 billion in 2026, with 45% allocated to aerospace, 30% to automotive, and 15% to medical sectors. Regional investment distribution indicates 65% concentration in the United States, 20% in Europe, and 15% in Asia-Pacific. M&A agreements, such as EOS and Concept Laser merger initiatives, increased production volume by 18% and facilitated collaborative R&D. Equity investments in new facilities for titanium and aluminum powders accounted for 28% of total capital expenditure. Expansion of post-processing facilities, technology licensing, and strategic alliances further contribute to market growth insights.

New Product Developments

New product introductions accounted for 22% of overall additive manufacturing with metal powders innovations in 2025. Performance improvements include 15–20% enhancements in tensile strength and corrosion resistance. Titanium alloy formulations for aerospace saw an adoption increase of 38%, while stainless steel blends for automotive achieved a 25% reduction in post-processing time. These innovations support market expansion and technology adoption across multiple sectors.

Recent Developments in United States Additive Manufacturing With Metal Powders

- 2026: GE Additive launched a new titanium powder line, increasing production by 28% and market share by 2%.

- 2025: EOS GmbH introduced advanced aluminum powders, boosting production volume by 22% and adoption in aerospace by 5%.

Research Methodology

The research process involved a combination of primary and secondary research to estimate market size, share, and growth. Primary research included interviews with 50+ industry experts, plant visits, and discussions with key stakeholders. Secondary research comprised company annual reports, government databases, trade journals, and industry publications. Market size estimation leveraged bottom-up and top-down approaches, combining facility production volumes, historical sales data, and projected adoption rates. Statistical models validated forecasts, while qualitative insights on technological trends and consumer behavior informed segmentation and dynamics analysis. This methodology ensures accurate and reliable United States additive manufacturing with metal powders' market insights.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Industrial Automation, Robotics, and Digital Twins

Diana Liska is a market research analyst with 7–9 years of experience specializing in manufacturing and industrial markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.