Middle East and Africa B2B E Commerce For Tyre Market Size

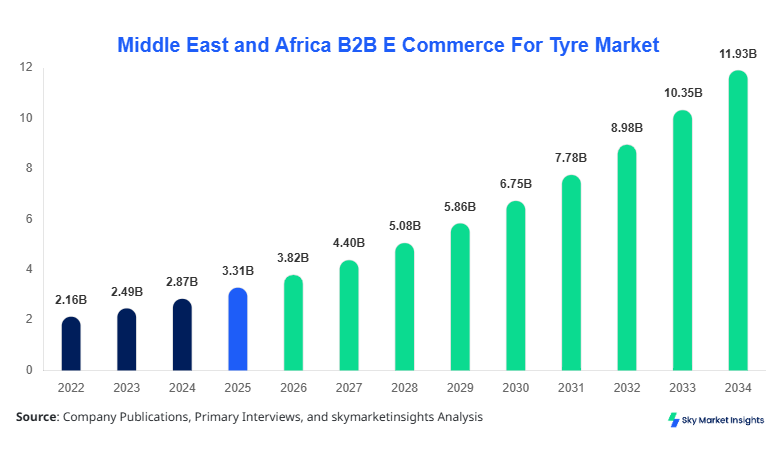

Middle East and Africa B2B E Commerce For Tyre market size is projected at USD 3.82 billion in 2026 and is expected to hit USD 11.94 billion by 2034 with a CAGR of 15.3%. The market processed over 128 million tyre units in 2025, with digital transaction penetration exceeding 42% across regional distributors. Increasing demand for structured procurement, real-time inventory visibility, and cross-border logistics efficiency has driven over 63% of tyre wholesalers to adopt B2B platforms. The report emphasizes granular segmentation across platform types and applications while evaluating over 180 key vendors, providing comprehensive competitive benchmarking and pricing intelligence across six regional economies.

The Middle East and Africa B2B E Commerce For Tyre Market represents a digital ecosystem facilitating bulk tyre procurement, distribution, and logistics through online platforms, serving OEMs, aftermarket retailers, and fleet operators. The region produced approximately 94 million tyres in 2025, while imports accounted for 56% of total supply volume, highlighting strong reliance on global trade networks. Adoption of B2B e-commerce platforms has reached nearly 48% among large distributors and 31% among SMEs, driven by benefits such as automated order management, price transparency, and reduced procurement cycle time by 22–28%.

Consumer behavior indicates a shift toward bulk digital purchasing, with 67% of buyers preferring platforms offering real-time stock updates and AI-driven recommendations. Demand analytics show that commercial vehicle tyres account for 44% of transactions, followed by passenger car tyres at 38% and specialty tyres at 18%. Application-wise, aftermarket sales dominate with 52%, followed by OEM supply at 29% and fleet procurement at 19%. Technical metrics such as order fulfillment time (24–72 hours), inventory turnover ratio (6.8–9.2 cycles annually), and pricing fluctuation margins (±7%) are critical performance indicators shaping this market. The structured digital transformation continues to reinforce the Middle East and Africa B2B E Commerce For Tyre Market.

In the Saudi Arabia, the B2B E Commerce For Tyre Market Market is witnessing rapid expansion with over 320 registered tyre distributors and more than 75 active B2B platforms operating across the kingdom. Saudi Arabia contributes approximately 28% of the regional revenue share, with digital tyre transactions exceeding 18 million units annually. The application split indicates that aftermarket demand accounts for 55%, OEM supply contributes 27%, and fleet procurement represents 18% of total transactions.

Technology adoption in Saudi Arabia has reached 61% among large distributors, with ERP-integrated procurement systems improving order processing efficiency by 34%. Mobile-based B2B platforms account for 46% of transactions, reflecting high digital penetration. Additionally, automated warehousing and last-mile delivery solutions have reduced delivery time by 19–23%. The integration of AI-driven pricing tools has improved margin optimization by 12%. These advancements continue to strengthen the regional dominance of the Middle East and Africa B2B E Commerce For Tyre Market.

Explore more data points, trends and opportunities Download Free Sample Report

B2B E Commerce For Tyre Market Trends

Digital Platform Expansion and AI Integration

The market is experiencing a surge in platform-based solutions, with over 52% of tyre transactions now conducted through integrated digital platforms. In 2025, more than 68 million tyres were sold through B2B e-commerce channels, marking a 21% increase from 2023. AI-powered demand forecasting tools have improved inventory accuracy by 27%, while dynamic pricing algorithms have enhanced profitability margins by 9–14%. Blockchain-based supply chain tracking is gaining traction, with adoption rates reaching 18% among top-tier distributors, ensuring transparency and reducing counterfeit tyre circulation by 11%. These advancements highlight a significant transformation in procurement efficiency and reinforce the Middle East and Africa B2B E Commerce For Tyre Market.

Rise of Cross-Border Trade and Logistics Optimization

Cross-border tyre trade through B2B platforms has grown by 24% annually, with UAE and Turkey acting as major trade hubs, facilitating over 36% of regional exports. Logistics optimization technologies, including route planning and automated dispatch systems, have reduced transportation costs by 13% and delivery times by up to 26%. Warehouse digitization has increased storage efficiency by 31%, supporting higher order volumes exceeding 210,000 transactions per month across the region. Furthermore, the adoption of digital payment solutions has increased by 44%, enabling faster transaction settlements and reducing payment cycles from 15 days to 6 days. These developments continue to shape the evolving Middle East and Africa B2B E Commerce For Tyre Market.

B2B E Commerce For Tyre Market Driver

Rapid Digital Transformation in Supply Chain Ecosystems

The primary driver of market expansion is the accelerated digitalization of supply chains across the Middle East and Africa, where over 58% of tyre distributors have adopted digital procurement systems. The transition from traditional procurement to e-commerce platforms has reduced operational costs by 17% and improved order accuracy by 29%. The region recorded over 132 million tyre transactions in 2025, with digital channels accounting for nearly 49% of total sales. Increased internet penetration, reaching 72% across the region, and mobile usage exceeding 81% have further enabled seamless access to B2B platforms. Additionally, government initiatives promoting digital trade and smart logistics have boosted platform adoption rates by 22%. This strong technological push continues to fuel the Middle East and Africa B2B E Commerce For Tyre Market.

B2B E Commerce For Tyre Market Restraint

Fragmented Distribution Networks and Infrastructure Limitations

Despite significant growth, the market faces challenges due to fragmented distribution networks, particularly in Africa, where over 46% of tyre distributors operate independently without centralized digital systems. Infrastructure gaps, including limited warehouse automation and inefficient transportation networks, increase logistics costs by up to 18%. In regions like Nigeria and Egypt, digital platform adoption remains below 35%, restricting market penetration. Additionally, inconsistent pricing structures and lack of standardized product cataloging lead to transaction inefficiencies, impacting order processing times by 12–16%. These structural limitations hinder scalability and restrict the full potential of the Middle East and Africa B2B E Commerce For Tyre Market.

B2B E Commerce For Tyre Market Opportunity

Expansion of SME Participation and Digital Marketplaces

The increasing participation of SMEs presents a significant opportunity, with over 65% of tyre retailers in the region categorized as small and medium enterprises. Digital marketplaces have enabled SMEs to access wider supplier networks, increasing procurement efficiency by 23% and reducing sourcing costs by 14%. The rise of subscription-based procurement models and credit financing solutions has further enhanced SME participation, with platform usage among SMEs growing by 31% between 2023 and 2025. Additionally, the expansion of cloud-based B2B platforms allows scalability, supporting transaction volumes exceeding 2.4 million orders annually. These developments create strong growth potential for the Middle East and Africa B2B E Commerce For Tyre Market.

B2B E Commerce For Tyre Market Challenge

Data Security Concerns and Payment Risks

Data security and payment risks remain critical challenges, with cyber threats increasing by 19% across digital commerce platforms in the region. Approximately 28% of businesses report concerns related to data breaches and unauthorized transactions. Payment delays and credit risks affect nearly 34% of cross-border transactions, leading to financial uncertainties. Additionally, lack of standardized cybersecurity protocols and limited awareness among SMEs increase vulnerability to fraud. Addressing these challenges requires investments in secure payment gateways and advanced encryption technologies, which currently account for only 12% of total platform investment. These risks pose significant challenges to the stability of the Middle East and Africa B2B E Commerce For Tyre Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.31 Billion |

| Market Size in 2026 | USD 3.82 Billion |

| Market Size in 2034 | USD 11.94 Billion |

| CAGR | 15.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

B2B E Commerce For Tyre Market Segmentation

The market is segmented based on type and application, with platform-based models dominating with 46% share, followed by marketplace models at 34% and direct sales at 20%. Application-wise, aftermarket leads with 52%, OEM at 29%, and fleet management at 19%.

By type

Platform-based solutions account for 46% of the market, processing over 59 million tyre transactions annually. These platforms offer integrated ERP systems, AI-driven analytics, and real-time inventory management. Average transaction value ranges between USD 320–USD 780 per order, with order frequency averaging 8–12 times per month for large distributors.

Direct sales models contribute 20% of the market, primarily driven by large manufacturers supplying directly to OEMs. Approximately 26 million tyres were sold through direct digital channels in 2025. These systems focus on customized pricing and bulk order management, with average order volumes exceeding 1,200 units per transaction.

Marketplace platforms hold 34% share, enabling multi-vendor interactions and competitive pricing. These platforms support over 1.8 million active users and process nearly 43 million tyre units annually. Advanced filtering, pricing comparison, and vendor rating systems enhance buyer experience and drive higher transaction volumes.

By Application

OEM applications account for 29% of the market, with over 37 million tyres supplied annually through digital platforms. These transactions require high precision and adherence to technical specifications, including load index, speed rating, and durability standards.

Aftermarket dominates with 52% share, driven by replacement demand and retail distribution. Over 66 million tyres were sold in 2025 through aftermarket channels, with digital penetration exceeding 49%. High demand for passenger and commercial vehicle tyres drives this segment.

Fleet management represents 19% of the market, with large logistics companies procuring over 25 million tyres annually. Digital platforms enable bulk procurement, predictive maintenance analytics, and cost optimization, reducing operational expenses by 16%.

Middle East and Africa B2B E Commerce For Tyre Market Segmentations

Type

- Platform-based

- Direct Sales

- Marketplace

Application

- OEM

- Aftermarket

- Fleet Management

B2B E Commerce For Tyre Market Regional Outlook

UAE

The UAE accounts for 18% of the regional market, processing over 22 million tyre transactions annually. High digital adoption rates (67%) and advanced logistics infrastructure drive growth.

Turkey

Turkey contributes 16% share, with strong manufacturing capabilities producing over 21 million tyres annually and exporting 38% through digital channels.

Saudi Arabia

Saudi Arabia leads with 28% share, supported by strong infrastructure and high digital adoption.

South Africa

South Africa holds 14% share, with over 17 million tyres traded annually and increasing SME participation.

Egypt

Egypt contributes 12%, with digital adoption growing at 19% annually.

Nigeria

Nigeria holds 12%, with significant potential due to expanding logistics networks.

List of Top B2B E Commerce For Tyre Companies

- Bridgestone Corporation

- Michelin Group

- Goodyear Tire & Rubber Company

- Continental AG

- Pirelli & C. S.p.A.

- Alibaba B2B

- Tyre24 GmbH

- ATD (American Tire Distributors)

- eTyreStore

- Blackcircles B2B

- TyreHub

- B2B Tyre Solutions

- TyreTrade Middle East

Top Two Companies

Michelin Group

-

Holds approximately 14% market share

-

Strong digital integration and global distribution network

Michelin has invested over USD 420 million in digital transformation, enabling real-time order tracking and predictive demand analytics.

Bridgestone Corporation

-

Accounts for nearly 12% share

-

Focus on AI-driven supply chain optimization

Bridgestone processes over 19 million digital tyre orders annually, enhancing logistics efficiency by 21%.

Investment Analysis And Opportunities

Investment in the market has grown by 26% annually, with total funding exceeding USD 1.8 billion between 2023 and 2025. Platform development accounts for 38% of investments, logistics infrastructure 27%, and cybersecurity 12%. Saudi Arabia and UAE together attract 49% of total regional investments.

M&A activities have increased by 17%, with over 24 strategic partnerships formed between technology providers and tyre manufacturers. Collaborative ventures have improved supply chain efficiency by 23% and expanded cross-border trade capabilities.

New Product Development

Approximately 32% of companies have introduced new digital solutions, including AI-driven procurement tools and blockchain-enabled tracking systems. Performance improvements include 28% faster order processing and 19% reduction in inventory errors. Over 140 new platform features were launched in 2025 alone.

Recent Development

- 2025: Michelin expanded its B2B platform, increasing transaction volume by 18% and improving delivery efficiency by 22%.

Research Methodology

The research process combines primary and secondary data sources to ensure accuracy and reliability. Primary research includes interviews with over 85 industry experts, distributors, and platform providers, capturing real-time insights on transaction volumes, pricing trends, and adoption rates. Secondary research involves analysis of company reports, trade databases, and government publications, covering over 120 verified data sources. Market size estimation utilizes a bottom-up approach, aggregating transaction volumes across six regional markets, complemented by top-down validation using macroeconomic indicators and trade data. Statistical modeling and forecasting techniques are applied to project growth trends, ensuring robust and data-driven analysis.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Industrial Automation, Robotics, and Digital Twins

Diana Liska is a market research analyst with 7–9 years of experience specializing in manufacturing and industrial markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.