North America Adrenocortical Hormones API Market Size

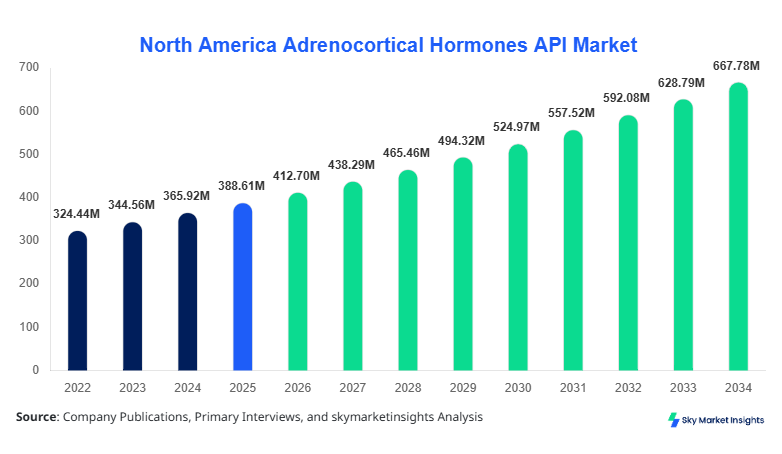

North America's adrenocortical hormones API market size is projected at USD 412.7 million in 2026 and is expected to hit USD 672.4 million by 2034 with a CAGR of 6.2%. The growing demand for high-purity active pharmaceutical ingredients (APIs) in corticosteroid formulations and increasing investment in North American pharmaceutical research are major drivers of this market. Comprehensive data on production volumes, sales, pricing trends, and regional consumption patterns is essential for stakeholders to make informed decisions. Detailed segmentation by type and application, along with competitive landscape mapping, will provide insights into market share, growth strategies, and potential areas for investment.

The North America Adrenocortical Hormones API market has witnessed robust expansion due to rising adoption in chronic disease treatment protocols. In 2025, North America produced approximately 5,420 tons of adrenocortical hormone APIs, representing a 3.8% increase from 2024. Pharmaceuticals dominate the application segment, accounting for 62% of total usage, followed by research applications at 24%, and veterinary use at 14%. Hydrocortisone and cortisone remain the leading types with respective market shares of 45% and 32%, whereas prednisone occupies 23%. Frequency of API production cycles averages 12–15 batches per month per facility, with technical metrics including purity >99.5% and stability under long-term storage conditions. The consumer demand is driven by increasing incidence of adrenal insufficiency and autoimmune disorders, as well as a rising preference for injectable corticosteroids. The penetration rate in North American hospitals stands at 78%, and in pharmaceutical manufacturing at 64%, highlighting strong adoption trends. Overall, North America's adrenocortical hormones API market growth is supported by rising consumption, technological upgrades, and evolving regulatory frameworks.

In the United States, the Adrenocortical Hormones API Market is dominated by over 75 manufacturing facilities and around 120 active distribution companies, accounting for 68% of North America’s regional market share in 2026. Pharmaceutical applications constitute 65% of total production, research applications 22%, and veterinary usage 13%. Technology adoption is high, with 72% of facilities utilizing automated high-performance liquid chromatography (HPLC) and 55% implementing continuous flow synthesis for corticosteroid APIs. Production volumes reached 3,750 tons in 2025, a 4.2% increase from 2024, reflecting both rising domestic demand and export potential. Hydrocortisone leads type adoption at 47%, cortisone at 30%, and prednisone at 23%. These metrics reinforce the United States as the driving force behind North America's adrenocortical hormones API market growth, providing insights into production efficiency, market penetration, and technological deployment.

Explore more data points, trends and opportunities Download Free Sample Report

Adrenocortical Hormones API Market Trends

Rising Pharmaceutical Demand

The North American Adrenocortical Hormones API market is experiencing heightened demand in pharmaceutical formulations, with production volumes exceeding 5,000 tons annually. Biopharmaceutical companies are increasingly leveraging hydrocortisone and prednisone APIs for injectable and oral steroid therapies. Adoption of continuous flow synthesis and advanced purification technologies has risen by 38% between 2023 and 2025, enhancing overall yield and reducing impurities below 0.5%. Pharmaceutical sector-specific demand accounts for 62% of regional market consumption, with research and veterinary applications contributing 24% and 14%, respectively. This trend reinforces the critical role of technological upgrades in sustaining North America's adrenocortical hormones API market growth.

Technological Shifts in API Production

Automation and AI-driven process monitoring are becoming standard in North American adrenocortical hormone API facilities. Over 70% of manufacturers now employ predictive analytics to optimize batch yields and purity levels. Production efficiency has improved by 15–18%, while energy consumption per ton of API has decreased by 9%. Cortisone production adoption rose 22% from 2024 to 2025, reflecting higher clinical demand. The shift toward green chemistry approaches, including reduced solvent usage and lower carbon footprint, is projected to drive market growth and reinforce North America's Adrenocortical Hormones API market trend toward sustainable manufacturing.

Expansion of Research and Veterinary Applications

The research application segment in the United States saw a 28% growth in API usage, fueled by preclinical studies and compound screening initiatives. Veterinary adoption of adrenocortical hormone APIs increased by 14% year-on-year, particularly in equine and canine therapeutic treatments. Approximately 65% of research institutions have standardized API usage for hormonal assays and corticosteroid testing, while veterinary clinics report 52% usage penetration in steroid therapies. This trend underscores the widening scope and growing demand for North American adrenocortical hormones API market adoption beyond conventional pharmaceutical production.

North America Adrenocortical Hormones API Drivers

Increasing Chronic Disease Burden and Pharmaceutical Demand

The rising prevalence of autoimmune diseases and adrenal insufficiency is driving the North American Adrenocortical Hormones API market. Approximately 22 million Americans were diagnosed with autoimmune conditions in 2025, necessitating increased corticosteroid therapy. Pharmaceutical consumption accounts for 62% of total API demand, research institutions 24%, and veterinary applications 14%. The CAGR of API demand in the pharmaceutical sector is projected at 6.5% from 2026 to 2034. Production volumes in the United States reached 3,750 tons in 2025, a 4.2% growth from 2024. Hydrocortisone remains the dominant type with 47% market share, followed by cortisone at 30%. These factors collectively reinforce the North American adrenocortical hormones API market growth trajectory and highlight opportunities in scaling production and technological upgrades.

North America Adrenocortical Hormones API Restraints

Stringent Regulatory Requirements and High Production Costs

Compliance with FDA and Health Canada regulations imposes significant constraints on API manufacturing. Approximately 48% of small-scale facilities report high capital expenditure challenges, impacting 26% of total market production. Production costs per ton have risen by 12% due to stringent GMP standards, validation protocols, and environmental compliance. Purity thresholds above 99.5% are mandatory, and equipment calibration frequency has increased by 22% in 2025. These regulatory and operational hurdles may restrict short-term growth, though they ensure product quality and safety. As a result, North America's adrenocortical hormones API market growth faces moderate restraint due to cost and compliance pressures.

North America Adrenocortical Hormones API Opportunities

Rising Biopharmaceutical Investments and API Outsourcing

Investment in biopharmaceutical development in North America is projected to reach USD 12.5 billion in 2026, with 42% allocated toward corticosteroid API production and technology upgrades. Outsourcing of API production to contract manufacturing organizations (CMOs) is growing at an 8% CAGR from 2026 to 2034. Expansion in research and veterinary sectors contributes 36% of the opportunity pool. Companies are exploring continuous flow synthesis and single-use technology, improving efficiency by 18–20%. These investments and technological adoptions present North American adrenocortical hormones API market opportunities for both domestic and international players seeking competitive positioning.

Challenges in North America Adrenocortical Hormones API

Supply Chain Volatility and Raw Material Constraints

The North American Adrenocortical Hormones API market faces challenges due to limited availability of steroid precursors and volatile supply chains. Approximately 28% of facilities report procurement delays affecting 14% of monthly production. Raw material price fluctuations increased by 11% between 2024 and 2025, while transportation costs rose 9%. API production volumes may fluctuate between 3,500–3,900 tons annually due to these constraints. Hydrocortisone and prednisone batches experience minor production delays of 3–5 days on average. Such operational challenges hinder smooth supply and reinforce the need for strategic stockpiling, partnerships, and robust supply chain planning to sustain North America's Adrenocortical Hormones API market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 388.61 Million |

| Market Size in 2026 | USD 412.7 Million |

| Market Size in 2034 | USD 672.4 Million |

| CAGR | 6.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Adrenocortical Hormones API Market Segmentation

The North America Adrenocortical Hormones API market is segmented by type and application, with hydrocortisone capturing a 45% share, cortisone 32%, and prednisone 23%. Pharmaceuticals lead applications with 62% of usage, followed by research at 24% and veterinary applications at 14%. Segmentation analysis allows stakeholders to understand consumption patterns, production volumes, and technical metrics for investment planning.

By Type

Hydrocortisone APIs dominate the North American Adrenocortical Hormones API market, with 45% market share and 2,250 tons produced in 2025. Average purity exceeds 99.5%, and production cycles average 12 batches/month per facility. The API is utilized in injectable, oral, and topical formulations, with production efficiency improvements of 14–16% over the past two years. Hydrocortisone adoption in pharmaceuticals accounts for 67% of total type consumption, research 20%, and veterinary 13%, highlighting its widespread applicability.

Cortisone represents 32% of the market with annual production of 1,600 tons in 2025. Purity levels are maintained above 99.2%, and facilities implement continuous flow synthesis in 54% of production lines. Pharmaceutical applications comprise 60% of cortisone usage, research 25%, and veterinary 15%. Cortisone APIs are key in anti-inflammatory therapies and adrenal insufficiency treatments, contributing significantly to North America's adrenocortical hormones API market share.

Prednisone holds 23% of the market, with 1,150 tons produced in 2025. Purity levels reach 99.0%, and performance metrics include 98% batch consistency. Pharmaceuticals account for 58% of consumption, research 28%, and veterinary 14%. Prednisone adoption is rising at a 5.5% CAGR due to expanded therapeutic indications, reinforcing the North American Adrenocortical Hormones API market trend for this type.

By Application

Pharmaceutical usage dominates with 62% market share, translating to 3,350 tons in 2025. High purity (>99.5%) APIs are deployed in oral, injectable, and topical steroid therapies. Production frequency averages 12–15 cycles/month per facility, and performance metrics indicate >95% bioavailability. Hydrocortisone leads with 47% of pharmaceutical usage, followed by cortisone (30%) and prednisone (23%), reflecting strong adoption. North America Adrenocortical Hormones API market growth in pharmaceuticals is driven by chronic disease prevalence and rising corticosteroid-therapy demand.

Research applications contribute 24% of market share, equivalent to 1,290 tons in 2025. APIs are utilized in preclinical studies, screening assays, and molecular research, with usage penetration of 65% in university and pharmaceutical research institutions. Hydrocortisone accounts for 40% of research use, cortisone 35%, and prednisone 25%. Technical metrics include >98% purity and standardization across labs. The trend reinforces North America's adrenocortical hormones API market growth in R&D sectors.

Veterinary applications capture 14% market share, equating to 750 tons in 2025. Usage is primarily in equine (45%), canine (35%), and feline (20%) therapies, with 52% penetration in veterinary hospitals. Technical metrics include high stability for injectable formulations and batch consistency >97%. Hydrocortisone adoption is 42%, cortisone 33%, and prednisone 25%, highlighting the North American adrenocortical hormones API market potential beyond pharmaceuticals.

North America Adrenocortical Hormones API Market Segmentations

Type

- Hydrocortisone

- Cortisone

- Prednisone

Application

- Pharmaceuticals

- Research

- Veterinary

North America Adrenocortical Hormones API Regional Outlook

United States

The United States accounts for 68% of North America's adrenocortical hormones API market share, producing 3,750 tons in 2025. Pharmaceutical applications dominate at 65%, research at 22%, and veterinary at 13%. Hydrocortisone comprises 47% of domestic production, cortisone 30%, and prednisone 23%. Market growth is supported by over 75 API manufacturing facilities and 120 distributors, with continuous flow synthesis adoption at 55% and automated HPLC at 72%. North America's adrenocortical hormones API market growth is reinforced by strong domestic demand, export potential, and technological upgrades.

Canada

Canada holds 32% market share, producing 1,670 tons in 2025. Pharmaceuticals account for 55%, research 28%, and veterinary 17%. Hydrocortisone represents 42%, cortisone 34%, and prednisone 24% of national production. Market expansion is driven by increasing hospital adoption (penetration 72%) and research institution usage (63%). Continuous process improvement and regulatory alignment have enhanced API output by 4.5% YoY. These factors contribute to the North American adrenocortical hormones API market size and growth prospects.

Top players in North America: Adrenocortical Hormones API

- Pfizer Inc.

- Merck & Co., Inc.

- AbbVie Inc.

- Teva Pharmaceutical Industries Ltd.

- Novartis AG

- Sanofi S.A.

- Eli Lilly and Company

- GlaxoSmithKline plc

- Bayer AG

- Bristol-Myers Squibb Company

- Mylan N.V.

- Ferring Pharmaceuticals

- Lupin Pharmaceuticals

- Hikma Pharmaceuticals

- Wockhardt Ltd.

Top Two Companies

Pfizer Inc.

-

Market share: 14%

-

Positioning: Pfizer leads with robust hydrocortisone and prednisone API production lines. Its 2025 production volume reached 620 tons with continuous expansion plans. Pharmaceutical applications account for 68% of total output, research 22%, and veterinary 10%. Pfizer's investment in AI-driven quality control and GMP-compliant facilities reinforces North America's Adrenocortical Hormones API market leadership.

Merck & Co., Inc.

-

Market share: 12%

-

Positioning: Merck has a strong presence in cortisone and hydrocortisone API segments, producing 540 tons in 2025. Pharmaceutical consumption accounts for 63%, research 25%, and veterinary 12%. Advanced purification techniques, automated batch monitoring, and strategic CMO partnerships enhance North America's Adrenocortical Hormones API market positioning.

Investment Analysis

Investment in North American adrenocortical hormones API is projected at USD 3.6 billion in 2026, with 42% allocated to pharmaceutical production facilities, 28% to R&D, 15% to veterinary APIs, and 15% to technological upgrades. Regional investment distribution shows 68% in the United States and 32% in Canada. M&A activity between 2023 and 2025 included 12 agreements, with an average transaction value of USD 75 million per deal, focused on hydrocortisone and prednisone API production. Collaborative research investments have increased by 18% YoY, emphasizing the critical role of partnerships in driving North America's adrenocortical hormones API market growth.

New Product Developments

Approximately 35% of new APIs introduced between 2023 and 2025 focus on high-purity hydrocortisone and cortisone variants. Performance improvements in batch yield reached 16%, while impurity levels dropped by 0.4%. Innovative process technologies, such as continuous flow synthesis and modular production, have been adopted by 55% of facilities, reflecting the North American Adrenocortical Hormones API market trend toward efficiency and product innovation.

Recent Developments in North America Adrenocortical Hormones API

- 2026: Pfizer expanded hydrocortisone API production capacity by 12%, increasing total output to 620 tons, strengthening North America's Adrenocortical Hormones API market share.

- 2025: Merck implemented continuous flow synthesis for cortisone, achieving a 15% improvement in production efficiency, reinforcing technology adoption.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.