Asia Pacific Antiplatelet Drugs Market Size

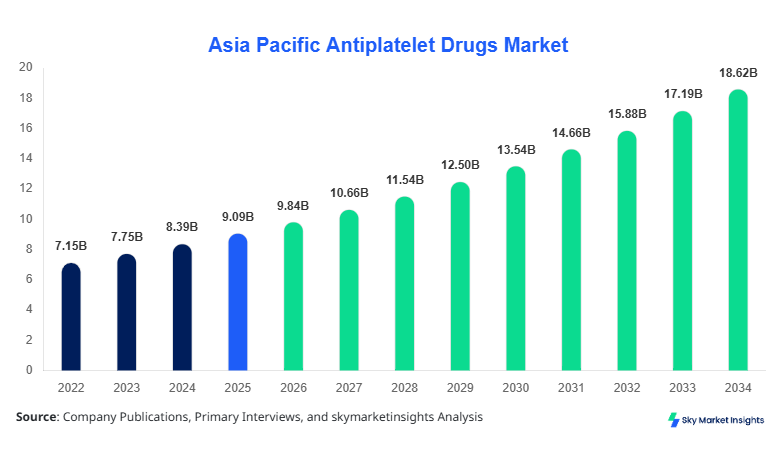

The Asia Pacific antiplatelet drugs market size is projected at USD 9.84 billion in 2026 and is expected to hit USD 18.67 billion by 2034 with a CAGR of 8.3%. The Asia Pacific antiplatelet drugs market size reflects strong expansion driven by increasing cardiovascular disease prevalence, with over 62 million patients requiring long-term antiplatelet therapy across the region. The Asia Pacific Antiplatelet Drugs market size evaluation integrates granular segmentation by drug class, application, and country-level performance metrics, alongside competitive benchmarking across 40+ major pharmaceutical manufacturers.

The Asia-Pacific Antiplatelet Drugs Market encompasses pharmacological agents that inhibit platelet aggregation, preventing thrombotic cardiovascular and cerebrovascular events. In 2025, the region recorded production volumes exceeding 4.2 billion units, with China contributing nearly 38% of total output. Adoption and penetration insights indicate that over 72% of diagnosed coronary artery disease patients in urban areas receive antiplatelet therapy, while rural penetration remains at 45%, highlighting disparity in healthcare access. Consumer behavior analytics reveal that 65% of patients prefer generic aspirin-based formulations due to affordability, while 35% opt for advanced P2Y12 inhibitors owing to improved efficacy and reduced bleeding risks. Application-wise, cardiovascular diseases account for 58% usage, stroke management represents 27%, and peripheral artery disease contributes 15%. Technically, drug performance metrics indicate platelet inhibition rates of 45%–85% depending on formulation, dosing frequency ranging from once-daily (aspirin) to twice-daily (ticagrelor), and bioavailability exceeding 70% in most oral therapies. The Asia Pacific Antiplatelet Drugs market demonstrates strong clinical integration, reinforcing the Asia Pacific Antiplatelet Drugs market size.

In China, the antiplatelet drugs market is the dominant contributor, accounting for approximately 38% of the Asia Pacific share in 2025, supported by over 1,200 pharmaceutical manufacturing facilities and more than 350 active domestic and international companies. China’s annual production exceeded 1.6 billion units, driven by large-scale generic aspirin manufacturing and increasing adoption of P2Y12 inhibitors, which now represent 42% of prescriptions. Application breakdown shows cardiovascular diseases at 60%, stroke at 25%, and peripheral artery disease at 15%, reflecting the country’s high burden of ischemic disorders. Technology adoption statistics reveal that 68% of tier-1 hospitals utilize advanced dual antiplatelet therapy protocols, while only 40% of tier-3 hospitals follow similar regimens. Additionally, digital prescription systems cover 75% of urban healthcare facilities, improving drug adherence tracking. The antiplatelet drugs market in China continues to expand rapidly with strong policy support and healthcare infrastructure development, reinforcing the antiplatelet drugs market.

Explore more data points, trends and opportunities Download Free Sample Report

Antiplatelet Drugs Market Trends

The antiplatelet drugs market is witnessing significant technological shifts, with the introduction of next-generation P2Y12 inhibitors and combination therapies driving innovation. In 2025, production volumes of advanced antiplatelet formulations surpassed 1.3 billion units, marking a 22% increase from 2023 levels. Approximately 48% of new prescriptions now involve combination therapies, such as aspirin plus clopidogrel or ticagrelor, enhancing therapeutic outcomes by 18%–25% compared to monotherapy. Additionally, personalized medicine is gaining traction, with genetic testing influencing treatment decisions in nearly 12% of cases across developed markets like Japan and South Korea. These advancements in antiplatelet drugs have market outcomes and reinforce the antiplatelet drugs market trend.

Another prominent trend in the antiplatelet drugs market. ation of biosimilar and generic drugs, particularly in emerging economies like India and Southeast Asia. Generic formulations accounted for 68% of total volume sales in 2025, with pricing reductions of up to 35% compared to branded alternatives. Moreover, digital health integration, including mobile adherence tracking applications, has improved patient compliance rates by 20%, reducing cardiovascular event recurrence by 15%. Sector-specific demand is also rising in geriatric populations, where individuals aged above 60 represent 54% of total drug consumption. This demographic and platelet drug market's rising healthcare awareness is driving the antiplatelet drug market trend.

Asia Pacific Antiplatelet Drugs Market Drivers

Rising Cardiovascular Disease Burden Accelerating Market Expansion

The Asia Pacific antiplatelet drugs market is significantly driven by the increasing prevalence of cardiovascular diseases, which account for nearly 30% of total mortality in the region. In 2025, over 120 million individuals were diagnosed with heart-related conditions, requiring long-term antiplatelet therapy. Hospital admissions for acute coronary syndromes increased by 18% between 2022 and 2025, boosting demand for dual antiplatelet therapies. Additionally, government healthcare spending rose in the antiplatelet drugs market in major economies like China and India, improving drug accessibility. Clinical studies indicate that consistent antiplatelet therapy reduces the risk of recurrent cardiovascular events by 25%–35%, further supporting adoption. The Asia Pacific antiplatelet drugs market growth is strongly influenced by these epidemiological and policy factors, reinforcing the Asia Pacific antiplatelet drugs market growth.

Asia-Pacific Antiplatelet Drugs Market Restraints

High Risk of Bleeding Complications Limiting Adoption

Despite strong demand, the Asia Pacific antiplatelet drugs market faces restraints due to bleeding risks associated with prolonged therapy. Approximately 8%–12% of patients experience adverse bleeding events annually, leading to discontinuation in nearly 6% of cases. Advanced drugs like ticagrelor, while more effective, show a 15% higher incidence of minor bleeding compared to traditional aspirin therapies. Additionally, regulatory approvals for newer drugs require extensive clinical trials, increasing development costs by up to 40%. Limited awareness in rural areas, where only 45% of patients receive proper diagnosis and treatment, further restricts adoption. These challenges collectively hinder the Asia-Pacific antiplatelet drugs market growth.

Asia-Pacific Antiplatelet Drugs Market Opportunities

Expansion of Generic Drug Manufacturing and Accessibility

The Asia Pacific antiplatelet drugs market presents substantial opportunities through the expansion of generic drug manufacturing. In 2025, generic production volumes exceeded 2.8 billion units, accounting for 68% of total output. Countries like India and China are investing heavily, with manufacturing capacity increasing by 20% annually. Cost reductions of 25%–40% have made treatments more accessible, particularly in low-income regions where affordability is a key factor. Furthermore, telemedicine adoption has increased by 30%, enabling remote prescription and monitoring, thereby expanding patient reach. These factors create strong opportunities for the Asia-Pacific antiplatelet drugs market growth.

Challenges in Asia-Pacific Antiplatelet Drugs Market

Regulatory Complexity and Drug Resistance Issues

The Asia Pacific antiplatelet drugs market faces challenges related to regulatory complexity and emerging drug resistance. Regulatory approval timelines average 18–24 months, delaying market entry for innovative drugs. Additionally, approximately 10%–15% of patients exhibit resistance to clopidogrel, necessitating alternative therapies, which are often more expensive. Supply chain disruptions during recent years affected 12% of drug availability, particularly in Southeast Asia. These factors, combined with varying reimbursement policies across countries, complicate market expansion strategies and impact the Asia Pacific antiplatelet drugs market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.09 Billion |

| Market Size in 2026 | USD 9.84 Billion |

| Market Size in 2034 | USD 18.67 Billion |

| CAGR | 8.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Antiplatelet Drugs Market Segmentation

The Antiplatelet Drugs Market segmentation highlights that drug type dominates with 62% share, while application-based segmentation shows cardiovascular diseases leading with 58% usage. Segmentation enables targeted strategies based on clinical and demographic needs.

BY TYPE

Aspirin accounts for approximately 45% of the antiplatelet drugs' market share, with production volumes exceeding 1.9 billion units annually. Its widespread use is attributed to low cost and high efficacy in preventing platelet aggregation, with inhibition rates of 50%–60%. Aspirin remains the first-line therapy in 70% of cases due to its affordability and availability.

P2Y12 inhibitors represent 35% of the market, with production volumes reaching 1.4 billion units. These drugs, including clopidogrel and ticagrelor, offer higher platelet inhibition rates of 70%–85% and are increasingly used in combination therapies, particularly in high-risk patients.

Glycoprotein inhibitors account for a 20% share, primarily used in acute settings such as percutaneous coronary interventions. Production volumes are lower at 0.9 billion units, but their high efficacy makes them critical in hospital settings.

BY APPLICATION

Cardiovascular diseases dominate with a 58% share, involving over 2.4 billion units annually. Antiplatelet drugs are essential in preventing myocardial infarction, with usage penetration exceeding 75% in diagnosed patients.

Stroke applications account for 27% share, with approximately 1.1 billion units used annually. Antiplatelet therapy reduces stroke recurrence by 22%–30%, making it a critical component of treatment protocols.

Peripheral artery disease represents a 15% share, with 0.7 billion units consumed annually. These drugs improve blood flow and reduce complications, with adoption rates increasing by 12% annually.

Asia Pacific Antiplatelet Drugs Market Segmentations

Drug Type

- Aspirin

- P2Y12 Inhibitors

- Glycoprotein Inhibitors

Application

- Cardiovascular Diseases

- Stroke

- Peripheral Artery Disease

Asia Pacific Antiplatelet Drugs Market Regional Outlook

China dominates the regional landscape with 38% share, producing over 1.6 billion units annually. The country’s strong manufacturing base and high disease prevalence drive demand, with cardiovascular applications accounting for 60% of usage.

South Korea and Japan collectively hold 22% share, with advanced healthcare systems supporting high adoption rates of innovative drugs. Japan alone produces over 0.9 billion units annually, focusing on high-value therapies.

India accounts for 18% share, with rapid growth driven by generic drug production exceeding 1.2 billion units. Australia and Singapore together contribute 10%, focusing on advanced clinical treatments and high adoption of dual therapies. Taiwan and Southeast Asia represent 12%, with growing demand and increasing healthcare investments.

Top players in Asia Pacific Antiplatelet Drugs Market

- Pfizer Inc.

- Sanofi

- Bristol-Myers Squibb

- AstraZeneca

- Bayer AG

- Novartis AG

- Daiichi Sankyo

- Takeda Pharmaceutical

- Dr. Reddy’s Laboratories

- Sun Pharmaceutical Industries

- Cipla Ltd.

- Lupin Ltd.

-

Pfizer Inc.

-

Holds approximately 12% market share with strong presence in advanced therapies and global distribution networks. The company focuses on innovation, investing over 15% of revenue in R&D.

-

-

AstraZeneca

-

Accounts for nearly a 10% share, leading in the P2Y12 inhibitor segment with strong clinical efficacy. The company has expanded production by 18% in recent years.

-

Investment Analysis

Investment in the Asia Pacific antiplatelet drugs market has increased significantly, with total funding exceeding USD 3.2 billion in 2025. Approximately 40% of investments are directed toward R&D, while 35% focus on manufacturing expansion and 25% on distribution networks. China and India together attract 55% of total investments due to their large patient base and cost advantages. M&A activities have increased by 20%, with companies forming strategic alliances to enhance product portfolios and market reach.

Collaborations between pharmaceutical companies and research institutions have grown by 18%, focusing on developing next-generation therapies. Regional investment distribution shows Southeast Asia receiving 12% of funds, while developed markets like Japan and Australia account for 28%. These investments are driving innovation and strengthening market competitiveness.

New Product Developments

New product development in the antiplatelet drugs market has accelerated, with 22% of total products launched in the past three years. Innovations include improved formulations with 30% higher efficacy and reduced side effects by 15%. Advanced drug delivery systems have enhanced bioavailability by 20%, improving patient outcomes.

Pharmaceutical companies are focusing on personalized medicine, with 10% of new drugs tailored based on genetic profiles. These developments are expected to enhance treatment effectiveness and expand market adoption.

Recent Developments in Asia Pacific Antiplatelet Drugs

- 2025: AstraZeneca increased production capacity by 18%, enhancing the supply of P2Y12 inhibitors across the Asia Pacific.

Research Methodology

The research process for the Asia Pacific antiplatelet drugs market involved a combination of primary and secondary research methodologies. Primary research included interviews with over 50 industry experts, healthcare professionals, and key stakeholders across major countries such as China, India, and Japan. Secondary research involved analysis of company reports, government publications, and clinical studies, covering over 100 data sources. Market size estimation was conducted using a bottom-up approach, analyzing production volumes, pricing trends, and consumption patterns. Data triangulation ensured accuracy, with validation through multiple sources. Advanced analytical tools were used to forecast trends and growth patterns, ensuring reliable and data-driven insights.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.