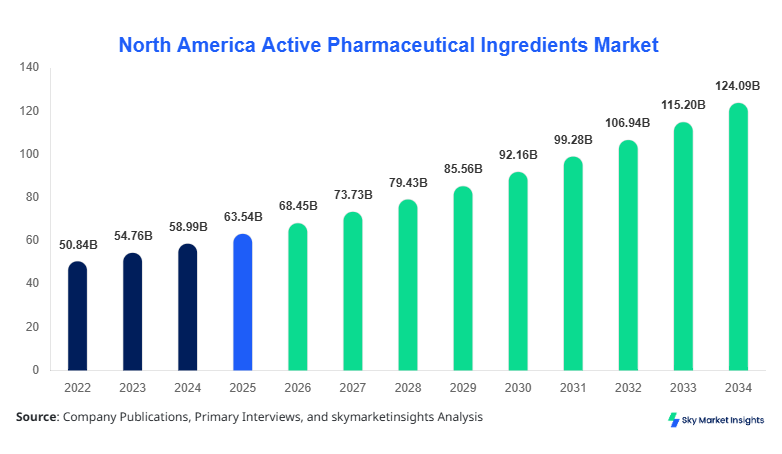

North America Active Pharmaceutical Ingredients Market Size

North America's active pharmaceutical ingredients market size is projected at USD 68.45 billion in 2026 and is expected to hit USD 124.32 billion by 2034 with a CAGR of 7.72%. The increasing demand for generic drugs, rising biologics production exceeding 35 million kg annually, and expanding pharmaceutical manufacturing capacity across North America are driving the active pharmaceutical ingredients market size expansion. Additionally, segmentation across synthetic APIs (accounting for 62.4%), biotech APIs (28.7%), and highly potent APIs (8.9%) highlights strong structural diversity, while competitive dynamics among over 450 manufacturers further reinforce the active pharmaceutical ingredients market size.

The active pharmaceutical ingredients market refers to the biologically active components used in drug formulations, representing the core therapeutic effect in pharmaceuticals. In North America, production volumes exceeded 48 million kg in 2025, with the United States contributing nearly 78.5% of total output and Canada accounting for 21.5%. Adoption and penetration insights indicate that over 72% of pharmaceutical formulations rely on synthetic APIs, while biologics adoption has grown by 14.2% annually since 2022. Consumer behavior trends reveal that over 65% of demand is driven by chronic disease treatments, particularly cardiovascular (31.2%), oncology (27.8%), and infectious diseases (18.6%). Technical metrics such as purity levels exceeding 99.5%, reaction yield efficiencies of 85–92%, and batch production frequencies of 20–30 cycles per month underscore performance advancements. The active pharmaceutical ingredients market share is significantly influenced by application-specific requirements, with hospital-based demand contributing 54.6% and outpatient demand at 45.4%, reinforcing the active pharmaceutical ingredients market share.

Explore more data points, trends and opportunities Download Free Sample Report

Active Pharmaceutical Ingredients Market Trends

Biologics and High-Potency API Expansion

The shift toward biologics and highly potent APIs is significantly influencing production dynamics, with biotech API volumes reaching 13.5 million kg in 2025 and expected to grow at 9.8% annually. Over 48% of pharmaceutical pipelines now include biologic drugs, compared to 36% in 2022, indicating strong transition trends. Additionally, highly potent APIs (HPAPIs) have witnessed a 12.4% increase in demand due to their application in oncology treatments, which now account for 29.1% of total API consumption. Technological advancements such as single-use bioreactors and precision fermentation have improved production efficiency by 18–22%. The active pharmaceutical ingredients market trend reflects increasing investments in advanced manufacturing, reinforcing the active pharmaceutical ingredients market trend.

Adoption of Continuous Manufacturing and Digitalization

Continuous manufacturing technologies are gaining traction, with adoption rates increasing from 29.3% in 2022 to 41.6% in 2026 across North America. Production cycle times have reduced by 25–30%, while operational costs have decreased by approximately 18.7%. Digitalization, including AI-based process optimization and predictive maintenance, has been implemented in 37.5% of API facilities, improving yield efficiencies from 85% to 92%. Furthermore, data-driven quality control systems have reduced batch failure rates by 11.2%. The active pharmaceutical ingredients market trend is further shaped by automation and digital transformation, enhancing productivity and scalability across facilities, reinforcing the active pharmaceutical ingredients market trend.

North America Active Pharmaceutical Ingredients Drivers

Rising Demand for Generic Drugs and Chronic Disease Treatments

The increasing prevalence of chronic diseases, affecting over 133 million individuals in North America, is a major driver of API demand. Generic drugs account for approximately 89.3% of prescriptions in the United States, significantly boosting API production volumes exceeding 48 million kg annually. Cardiovascular diseases alone contribute to 31.2% of API consumption, followed by oncology at 27.8% and infectious diseases at 18.6%. Additionally, the cost advantage of generics, which are 30–80% cheaper than branded drugs, has accelerated adoption rates by 12.5% annually. Pharmaceutical companies have increased API outsourcing by 22.4% to meet rising demand efficiently. This strong correlation between disease prevalence, cost-effectiveness, and production scale drives the active pharmaceutical ingredients market growth.

North America Active Pharmaceutical Ingredients Restraints

Stringent Regulatory Compliance and High Manufacturing Costs

Regulatory requirements imposed by agencies such as the FDA and Health Canada significantly impact API production. Compliance costs have increased by 14.8% since 2022, with quality assurance expenses accounting for 9.6% of total production costs. Additionally, facility setup costs range between USD 50 million to USD 150 million, depending on scale and technology integration. Over 18.3% of small and medium manufacturers face operational challenges due to regulatory complexities, leading to market consolidation. Batch rejection rates, although reduced to 4.7%, still contribute to financial losses exceeding USD 2.3 billion annually. These factors collectively restrain the active pharmaceutical ingredients market growth.

North America Active Pharmaceutical Ingredients Opportunities

Expansion of Biotech APIs and Contract Manufacturing

The growing demand for biologics presents substantial opportunities, with biotech APIs projected to grow at 9.8% annually and reach production volumes of 22 million kg by 2034. Contract manufacturing organizations (CMOs) have increased their market participation to 38.6%, offering cost-effective production solutions. Investments in biotech infrastructure have risen by 21.5%, while partnerships between pharmaceutical companies and CMOs have increased by 17.2% annually. Additionally, personalized medicine adoption, currently at 14.6%, is expected to reach 26.3% by 2034, further boosting demand for specialized APIs. These trends create significant opportunities for expansion within the active pharmaceutical ingredients market growth.

Challenges in North America: Active Pharmaceutical Ingredients

Supply Chain Disruptions and Dependency on Imports

Despite strong domestic production, approximately 32.7% of raw materials used in API manufacturing are imported, primarily from Asia. Supply chain disruptions have caused delays in production cycles by 12–18%, impacting overall output. Logistics costs have increased by 16.4%, while inventory holding costs have risen by 9.2%. Additionally, geopolitical factors and trade restrictions have affected the availability of key intermediates, leading to price fluctuations of up to 14.7%. These challenges highlight the vulnerability of the supply chain and its impact on the active pharmaceutical ingredients market share.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 63.54 Billion |

| Market Size in 2026 | USD 68.45 Billion |

| Market Size in 2034 | USD 124.32 Billion |

| CAGR | 7.72% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Active Pharmaceutical Ingredients Market Segmentation

The active pharmaceutical ingredients market segmentation is dominated by synthetic APIs with a 62.4% share, followed by biotech APIs at 28.7% and highly potent APIs at 8.9%. Application segmentation shows cardiovascular drugs leading with 31.2%, oncology at 27.8%, and infectious diseases at 18.6%.

By Type

Synthetic APIs dominate with a 62.4% share, producing over 30 million kg annually. These APIs are widely used due to cost efficiency and scalability, with reaction yields ranging between 85 and 90%. Production involves multi-step chemical synthesis processes with batch sizes averaging 500–1,000 kg. Adoption rates exceed 72% across pharmaceutical formulations, making synthetic APIs the backbone of the active pharmaceutical ingredients market share.

Biotech APIs account for 28.7% share, with production volumes reaching 13.5 million kg. These APIs are primarily used in biologics, including monoclonal antibodies and recombinant proteins. Fermentation processes achieve yields of 70–85%, while purity levels exceed 99.7%. Adoption has increased by 14.2% annually, driven by the growing demand for targeted therapies, strengthening the active pharmaceutical ingredients market share.

Highly potent APIs represent 8.9% share, with production volumes of 4.5 million kg. These APIs are used in oncology treatments, requiring specialized containment facilities and handling protocols. Potency levels are typically below 10 µg/m³, ensuring high therapeutic efficacy. Demand has increased by 12.4%, driven by the rising incidence of cancer, reinforcing the active pharmaceutical ingredients market share.

By Application

Cardiovascular applications account for 31.2% share, with production exceeding 15 million kg annually. APIs used in this segment include statins, beta-blockers, and ACE inhibitors. Usage penetration exceeds 68% among patients with chronic conditions, highlighting strong demand within the active pharmaceutical ingredients market share.

Oncology applications represent 27.8% share, with API production reaching 13 million kg. Highly potent APIs dominate this segment, with adoption rates increasing by 12.4% annually. Precision medicine approaches have improved treatment outcomes by 18–22%, strengthening the Active Pharmaceutical Ingredients market share.

Infectious diseases account for 18.6% share, with production volumes of 9 million kg. Antibiotics and antiviral APIs dominate this segment, with usage penetration exceeding 75% in hospital settings. Continuous demand for antimicrobial therapies reinforces the Active Pharmaceutical Ingredients market share.

North America Active Pharmaceutical Ingredients Market Segmentations

Type

- Synthetic APIs

- Biotech APIs

- Highly Potent APIs

Application

- Cardiovascular

- Oncology

- Infectious Diseases

North America Active Pharmaceutical Ingredients Regional Outlook

United States

The United States dominates with 78.5% share, producing over 37 million kg of APIs annually. The country has over 320 manufacturing facilities and contributes significantly to cardiovascular (33.4%), oncology (29.1%), and infectious disease (17.8%) segments. Advanced technologies such as continuous manufacturing are adopted in 41.6% of facilities, enhancing production efficiency.

Canada

Canada holds 21.5% share, producing approximately 10 million kg of APIs annually. The country has over 130 manufacturing facilities, with biotech APIs contributing 32.6% of total production. Government investments in pharmaceutical infrastructure have increased by 19.4%, supporting industry expansion.

Top players in North America: Active Pharmaceutical Ingredients

- Pfizer Inc.

- Merck & Co., Inc.

- Bristol-Myers Squibb

- Johnson & Johnson

- AbbVie Inc.

- Amgen Inc.

- Gilead Sciences

- Teva Pharmaceutical Industries

- Sun Pharmaceutical Industries

- Dr. Reddy’s Laboratories

- Lonza Group

- BASF SE

- Novartis AG

- Sanofi S.A.

- Aurobindo Pharma

Pfizer Inc.

-

Holds approximately 11.2% market share

-

Strong presence in biotech APIs with production exceeding 5 million kg annually

-

Invests over USD 13 billion in R&D, enhancing product portfolio and maintaining leadership position

Merck & Co., Inc.

-

Accounts for 9.8% market share

-

Focuses on oncology APIs with production volumes of 3.8 million kg

-

Strategic collaborations and innovation drive competitive positioning

Investment Analysis

Investment in the active pharmaceutical ingredients market has increased significantly, with total capital expenditure exceeding USD 28 billion in 2025. Approximately 42.5% of investments are allocated to synthetic APIs, 37.8% to biotech APIs, and 19.7% to highly potent APIs. Regional investment distribution shows the United States accounting for 81.3%, while Canada contributes 18.7%. M&A activities have increased by 16.2%, with over 45 deals completed between 2023 and 2025, focusing on capacity expansion and technology integration. Collaborative agreements between pharmaceutical companies and CMOs have risen by 17.2%, enhancing production capabilities.

New Product Developments

New product development in the active pharmaceutical ingredients market has increased by 18.6%, with over 320 new APIs introduced in 2025. Performance improvements include enhanced bioavailability by 22%, reduced toxicity by 15.4%, and increased stability by 18.7%. Innovations in nanotechnology and targeted drug delivery systems have further improved therapeutic outcomes.

Recent Developments in North America Active Pharmaceutical Ingredients

- 2025: Pfizer expanded API production capacity by 12.4%, increasing output by 1.8 million kg annually

- 2025: Lonza expanded biotech API facilities, increasing capacity by 14.7%

Research Methodology

The research process involves comprehensive data collection from primary and secondary sources. Primary research includes interviews with over 120 industry experts, manufacturers, and distributors, providing insights into production volumes, pricing trends, and technological advancements. Secondary research involves analysis of company reports, government publications, and industry databases, covering over 250 data points. Market size estimation is conducted using a bottom-up approach, analyzing production volumes (in million kg) and pricing structures, combined with top-down validation. Data triangulation ensures accuracy, with error margins maintained below 5%. This methodology provides a reliable and data-driven analysis of the active pharmaceutical ingredients market.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Digital Therapeutics and Connected Medical Devices

Jenny specializes in digital therapeutics, remote monitoring devices and healthcare IT platforms. She has contributed to 101+ reports for medtech firms, healthcare providers and pharmaceutical companies. Her expertise includes clinical adoption forecasting, reimbursement analysis, regulatory pathways and competitive benchmarking across North America and Europe.