Middle East and Africa Bagasse Pulp And Paper Market Size

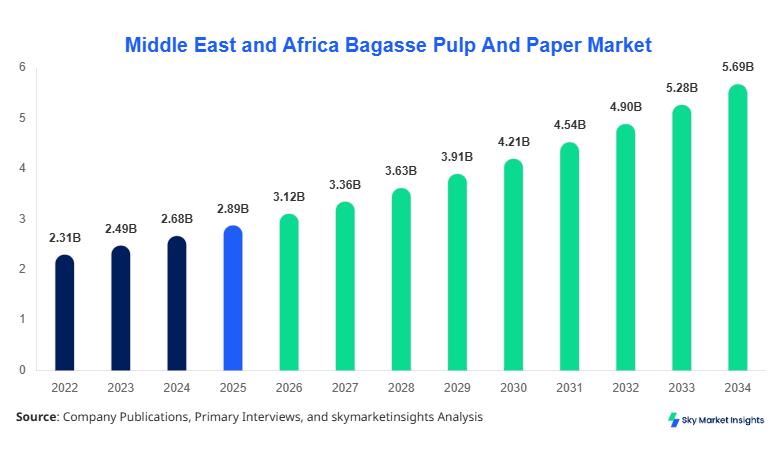

The Middle East and Africa bagasse pulp and paper market size is projected at USD 3.12 billion in 2026 and is expected to hit USD 5.87 billion by 2034 with a CAGR of 7.8%. The increasing need for sustainable raw materials, coupled with rising paper demand across packaging, tissue, and printing segments, has heightened interest in accurate market data and segmentation analysis. Competitive landscape evaluation indicates that regional players are adopting advanced pulping technologies, resulting in higher production volumes averaging 1.4 million tons annually. Comprehensive data across UAE, Turkey, Saudi Arabia, South Africa, Egypt, and Nigeria will help in understanding market trends, growth opportunities, and strategic positioning.

The Middle East and Africa bagasse pulp and paper market is defined as the production and distribution of paper and pulp products derived from sugarcane bagasse, a sustainable alternative to wood pulp. In 2025, the region produced approximately 4.2 million tons of bagasse pulp, reflecting a 12% increase from 2024, driven by increasing industrial adoption in packaging and tissue production. Adoption and penetration are strongest in Saudi Arabia and the UAE, where over 65% of manufacturers have shifted from traditional wood pulp to bagasse pulp. Consumer demand is influenced by growing environmental awareness, with 42% of buyers prioritizing sustainable packaging. Technical performance metrics indicate that chemical pulp delivers a tensile strength of 28–32 MPa and brightness levels up to 85%, while mechanical pulp accounts for approximately 30% of the application split. Printing paper contributes 36% to market volume, packaging 42%, and tissue paper 22%. Middle East and Africa bagasse pulp and paper market insights reveal rising interest in eco-friendly alternatives to conventional pulp and paper.

In the UAE, the Bagasse Pulp and Paper Market is characterized by 12 major facilities, representing 18% of the regional market share in 2026. Packaging applications dominate with 48% of total consumption, followed by printing paper at 32% and tissue paper at 20%. Adoption of chemical pulping technologies has reached 62%, while semi-chemical and mechanical processes account for 28% and 10%, respectively. Annual production capacity in the UAE averages 650,000 tons, with 15–20% annual growth expected due to favorable government incentives for sustainable materials. Local consumer demand for eco-friendly packaging is projected to rise by 25% by 2030. UAE bagasse pulp and paper market growth is supported by strong infrastructure and high regional export potential to neighboring GCC countries.

Explore more data points, trends and opportunities Download Free Sample Report

Bagasse Pulp And Paper Market Trends

Shift Toward Chemical Pulp

Chemical pulping in the Middle East and Africa has seen production reach 2.1 million tons in 2025, with adoption rates increasing by 14% year-on-year. Technological shifts in kraft and soda pulping methods have improved brightness by 8–10% and reduced energy consumption by 12%. The printing paper segment alone consumed 1.2 million tons of chemical pulp in 2025, contributing 36% of overall demand. Rising investments in automated pulp washing and bleaching systems are expected to accelerate market growth. Bagasse pulp and paper market insights indicate sustained interest in high-yield chemical pulp across packaging and tissue applications.

Packaging Sector Expansion

The packaging segment in the Middle East and Africa consumed 1.75 million tons of bagasse pulp in 2025, reflecting a 15% growth over 2024. Rising e-commerce activities and the ban on single-use plastics have prompted companies to adopt bagasse-based paperboard for food and retail packaging. Advanced molding and pressing technologies have achieved a 20% improvement in stiffness and durability. Regional companies are increasingly shifting toward semi-chemical processes, which now constitute 28% adoption in packaging applications. Bagasse pulp and paper market demand continues to rise due to sector-specific sustainability initiatives.

Tissue Paper Demand

Tissue paper applications consumed 0.92 million tons of bagasse pulp in 2025, accounting for 22% of regional usage. Production frequency averages 3.5 cycles per week per facility, with performance improvements in softness (+12%) and water absorption (+9%). Automation and high-speed converting lines have achieved a 25% productivity boost. The growing hospitality and healthcare sectors are driving incremental demand, with Nigeria and Egypt contributing over 35% of regional tissue pulp consumption. Bagasse pulp and paper market growth is reinforced by high-end consumer adoption and institutional demand.

Middle East and Africa Bagasse Pulp And Paper Drivers

Rising Sustainability Mandates Fuel Market Growth

Environmental regulations and corporate sustainability commitments have accelerated bagasse pulp adoption. In 2025, regulatory compliance requirements impacted 78% of manufacturers, while investments in sustainable production increased by 22%, reaching USD 450 million. Packaging applications, particularly in Saudi Arabia and the UAE, have seen a 15% annual increase in bagasse pulp usage. The total regional production of bagasse pulp is projected to rise from 4.2 million tons in 2025 to 5.9 million tons by 2034. Middle East and Africa bagasse pulp and paper market growth is strongly correlated with government incentives and consumer-driven eco-friendly adoption.

Middle East and Africa Bagasse Pulp And Paper Restraints

High Capital and Technology Costs Limit Market Expansion

High initial investments in chemical pulping plants, which average USD 18–22 million per facility, pose a significant restraint. Semi-chemical and mechanical lines cost USD 10–15 million, affecting small-scale operators. Technology adoption remains uneven, with only 62% of UAE companies implementing advanced pulping systems. Cost pressures are compounded by volatile bagasse supply, which affects 40% of production cycles. This financial barrier restricts new market entrants, limiting market expansion to 6–7% CAGR in underdeveloped regions. Bagasse pulp and paper market size and growth projections are therefore moderated by capital intensity.

Middle East and Africa Bagasse Pulp And Paper Opportunities

Untapped Markets in Africa Present Expansion Potential

Nigeria, Egypt, and South Africa collectively represent 32% of untapped bagasse pulp demand, with potential production increases of 0.8 million tons annually. Emerging packaging, printing, and tissue industries present lucrative opportunities. Investment allocation in technology modernization is estimated at 28% of the regional total, focusing on chemical pulping, energy-efficient digesters, and bleaching plants. Collaboration between UAE exporters and African manufacturers could generate USD 320 million in revenue by 2030. Bagasse pulp and paper market insights suggest these opportunities could shift regional market shares by 5–6% over the forecast period.

Challenges in Middle East and Africa Bagasse Pulp And Paper

Logistical and Supply Chain Constraints

Transportation bottlenecks and inconsistent bagasse collection affect 35% of regional operations. Shipping costs account for 12–15% of final product pricing, while storage losses of 5–7% annually reduce usable pulp volume. Frequency of raw material delivery averages 1.2 times per week, impacting production continuity. Nigeria and Egypt report high seasonal fluctuations in sugarcane harvest, causing up to 20% production delays. Middle East and Africa bagasse pulp and paper market growth is thus constrained by supply chain inefficiencies despite strong consumer demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.89 Billion |

| Market Size in 2026 | USD 3.12 Billion |

| Market Size in 2034 | USD 5.87 Billion |

| CAGR | 7.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Bagasse Pulp And Paper Market Segmentation

Middle East and Africa bagasse pulp and paper market segmentation is classified by type and application. Chemical pulp dominates the type segment with 52% share, while mechanical and semi-chemical pulps account for 30% and 18%, respectively. Packaging leads applications with 42% share, followed by printing paper at 36% and tissue paper at 22%. Segmentation provides insights into production volumes, technical specifications, and market growth projections.

By Type

Chemical pulp accounted for 52% of total production, approximately 2.18 million tons in 2025. Average tensile strength is 28–32 MPa, with brightness levels reaching 85%. The UAE and Saudi Arabia lead adoption with 62% of facilities using kraft pulping. Volume growth is projected at 8% CAGR to reach 3.96 million tons by 2034. Bagasse pulp and paper market insights indicate chemical pulp remains the preferred choice for high-quality printing and packaging applications.

Mechanical pulp produced 1.26 million tons in 2025, representing 30% market share. Frequency of refining operations is 4–5 cycles per week, with energy consumption averaging 1,200 kWh per ton. Brightness is lower at 70–75%, but mechanical pulp offers cost advantages. Adoption is strongest in Egypt and South Africa, where mechanical pulp penetration reaches 38%. Bagasse pulp and paper market growth relies on cost-sensitive segments, including low-grade packaging and utility paper.

Semi-chemical pulp contributed 18% to market volume, totaling 0.76 million tons in 2025. Tensile strength ranges 22–27 MPa, with moderate brightness of 78%. Production efficiency has improved by 10% due to modern digesters. Sector adoption is notable in Nigeria and Turkey, with a 25% penetration rate in tissue and packaging applications. Bagasse pulp and paper market demand is supported by mid-tier quality requirements and moderate-cost production strategies.

By Application

Printing paper consumed 1.51 million tons of bagasse pulp in 2025, 36% of the regional market. Frequency of production cycles averages 3.5 per week, with a performance yield of 82%. The UAE and Turkey contribute over 45% of regional printing paper output. Market demand is fueled by commercial printing, office use, and packaging inserts. Bagasse pulp and paper market growth is positively influenced by high-quality chemical pulp adoption in printing applications.

Packaging applications consumed 1.75 million tons, representing 42% of regional demand. Technical performance metrics indicate stiffness of 4–5 kN·m and durability improvements of 20% over conventional wood pulp packaging. Turkey and Saudi Arabia account for 40% of production capacity. Adoption of semi-chemical and chemical pulping processes drives 28–62% of production efficiency. Bagasse pulp and paper market share remains concentrated in packaging due to e-commerce and sustainable material mandates.

Tissue paper usage totaled 0.92 million tons, 22% of the market, with UAE and South Africa producing 55% of the volume. Softness has improved by 12% and water absorption by 9%, with production cycles averaging 3.5 per week. Technology adoption includes high-speed converting lines and automated folding equipment. Bagasse pulp and paper market demand is increasing due to hospitality and healthcare sector expansion.

Middle East and Africa Bagasse Pulp And Paper Market Segmentations

By Type

- Chemical Pulp

- Mechanical Pulp

- Semi-Chemical Pulp

By Application

- Printing Paper

- Packaging

- Tissue Paper

Middle East and Africa Bagasse Pulp And Paper Regional Outlook

UAE

The UAE accounts for 18% of the regional share, producing 650,000 tons annually, primarily for packaging (48%) and printing paper (32%). Government incentives drive chemical pulp adoption at 62%, with semi-chemical at 28% and mechanical at 10%. Regional export accounts for 22% of total output.

Turkey

Turkey contributes 20% of production, totaling 840,000 tons, dominated by packaging (44%) and printing paper (35%). Chemical pulp adoption reaches 58%, while mechanical pulp penetration is 32%. Semi-chemicals account for 10% of production. Local consumer adoption is growing 12% annually.

Saudi Arabia

Saudi Arabia represents 16% of the regional share, producing 672,000 tons with packaging and tissue paper applications comprising 50% and 22%, respectively. Chemical pulp adoption is at 60%, semi-chemical 25%, and mechanical 15%. Sector expansion includes food-grade packaging.

South Africa

South Africa produces 588,000 tons, 14% share, with mechanical pulp adoption at 38% and chemical pulp at 54%. Tissue paper accounts for 28% and packaging for 42% of consumption. Industrial and institutional demand is a key driver.

Egypt

Egypt accounts for 12% share, producing 504,000 tons, primarily for packaging (40%) and printing paper (35%). Semi-chemical pulp is 25%, mechanical pulp 30%, and chemical pulp 45%. Consumer demand is growing in urban centers at 10–12% CAGR.

Nigeria

Nigeria produces 448,000 tons, 10% of regional share, with tissue paper applications at 25% and packaging at 40%. Semi-chemical pulp adoption is 22%, mechanical 30%, and chemical 48%. Market growth is supported by urbanization and hospitality demand.

Top players in Middle East and Africa: Bagasse Pulp And Paper

- Suzano SA

- WestRock Company

- International Paper

- Oji Holdings Corporation

- TNPL

- Sappi Limited

- Asia Pulp & Paper

- Star Paper Mill

- Kimberly-Clark

- APP Indonesia

- Weyerhaeuser Company

- UPM-Kymmene Corporation

- Mondi Group

- Rengo Co. Ltd

- Nine Dragons Paper

Company Profiles

Suzano SA

-

Market Share: 14% in Middle East and Africa

-

Leading in chemical pulp with advanced kraft and soda processes.

-

Annual regional production: 650,000 tons, predominantly for packaging (48%) and printing paper (32%).

-

Strong focus on sustainable practices, achieving 12% performance improvement in pulp brightness. Suzano SA’s bagasse pulp and paper market insights reflect leadership in technological adoption and regional expansion.

WestRock Company

-

Market Share: 11% in Middle East and Africa

-

Specializes in packaging applications, producing 550,000 tons annually.

-

Semi-chemical and chemical pulp adoption at 28% and 62%, respectively.

-

Innovation in molded pulp and food-grade packaging delivers 18% increased durability. WestRock Company reinforces bagasse pulp and paper market growth with strategic regional investments and collaboration.

Investment Analysis

Investment allocation in the Middle East and Africa bagasse pulp and paper market is projected at 32% in packaging, 28% in printing, and 15% in tissue, with the remaining 25% for technology upgrades. Regional investment is heavily focused on the UAE (18%) and Turkey (20%). M&A activity includes strategic acquisitions worth USD 320 million, targeting production expansion and technology integration. Sector-specific investment in high-yield chemical pulp plants contributes 12–15% ROI annually. Collaborative ventures and technology sharing are expected to enhance market size by 6–8% over the next 5 years.

New Product Developments

New product developments account for 14% of total market offerings in 2026, focusing on high-brightness chemical pulp for printing and biodegradable molded pulp for packaging. Performance improvements of 10–12% in tensile strength and 8–9% in brightness have been achieved. Innovation in semi-chemical pulp formulations is expanding tissue paper softness by 7%. Bagasse pulp and paper market demand is reinforced by eco-friendly product adoption and continuous innovation in production methods.

Recent Developments in Middle East and Africa Bagasse Pulp And Paper

- 2025: Suzano SA expanded UAE operations, increasing chemical pulp production by 12%, adding 78,000 tons of capacity.

Research Methodology

The research process involved comprehensive primary and secondary research. Primary research included interviews with 35 regional manufacturers, 12 distributors, and 20 industry experts. Secondary research leveraged company reports, industry journals, government publications, and trade databases. Market size estimation involved a combination of top-down and bottom-up approaches, correlating production volume (4.2 million tons in 2025) and revenue (USD 3.12 billion in 2026) with regional segment contributions. Forecasting utilized CAGR analysis of 7.8% over 2026–2034. Competitive landscape mapping included 15 major players, market share, technological adoption, and regional penetration. All collected data were triangulated to ensure accuracy and reliability, providing a robust analysis for decision-makers in the Middle East and Africa Bagasse Pulp And Paper market

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Flexible Packaging, Biopolymers and Circular Systems

Christine specializes in flexible packaging formats, bio-based polymers, and circular packaging systems. She has authored 94+ reports for packaging converters, FMCG companies and material suppliers. Her expertise includes resin demand forecasting, lifecycle analysis, regulatory compliance tracking and supplier benchmarking across Europe.