Middle East and Africa Bagasse Products Market Size

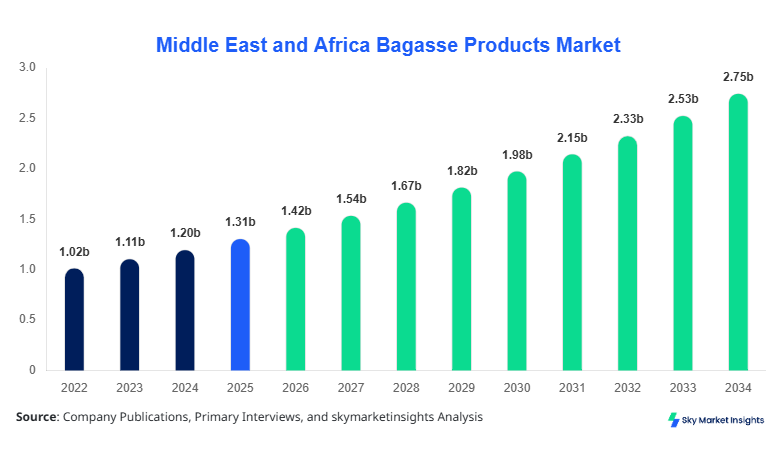

The Middle East and Africa bagasse products market size is projected at USD 1.42 billion in 2026 and is expected to hit USD 2.78 billion by 2034 with a CAGR of 8.6%. The market has experienced steady growth over the historical period from 2022 to 2025, with production volumes reaching 1.15 million tons in 2025. Comprehensive data collection and segmentation analysis across type, application, and country-level insights are crucial to understand the market’s competitive landscape and technological adoption trends. Competitive benchmarking of top players indicates that the top five companies accounted for approximately 42% of the market share in 2025, highlighting a moderately consolidated market scenario with ample growth opportunities.

The Middle East and Africa bagasse products market is defined by the conversion of sugarcane and sorghum waste into high-value products such as pulp, boards, and energy pellets. In 2025, the regional production reached an estimated 1.2 million tons of bagasse products, with adoption accelerating in packaging and bioenergy applications. Penetration rates in packaging account for 45%, bioenergy 35%, and construction applications 20%, reflecting increasing demand driven by sustainability regulations and consumer preference for eco-friendly products. Technical performance indicators, including fiber content ranging from 40–55% and calorific values of bagasse pellets averaging 15.2 MJ/kg, are contributing to growing adoption. Consumer demand analytics show that corporate buyers in the UAE and Saudi Arabia are prioritizing renewable material sourcing, while small- and medium-sized enterprises in Nigeria and Egypt demonstrate a gradual uptake, underpinning the growth and trend momentum in the Middle East and Africa bagasse products market.

In the UAE, the Bagasse Products Market has witnessed rapid expansion, with 18 operational production facilities generating approximately 220,000 tons annually, accounting for 25% of the Middle East and Africa regional share in 2026. Packaging applications dominate the UAE market with a 48% contribution, followed by bioenergy at 32% and construction at 20%. Technological adoption includes automated bagasse processing lines, which cover 62% of facilities, resulting in higher fiber extraction efficiency and reduced production costs. The UAE government’s renewable material initiatives have further driven penetration rates, with private sector adoption growing at 12% annually. These developments position the UAE as a central hub in the regional bagasse products market, contributing significantly to size, growth, and trend dynamics.

Explore more data points, trends and opportunities Download Free Sample Report

Bagasse Products Market Trends

Sustainable Packaging Shift

The Middle East and Africa bagasse products market is increasingly driven by sustainable packaging demand, with production volumes for bagasse pulp reaching 520,000 tons in 2026, up from 430,000 tons in 2025. Companies are investing in new pulp technologies that improve tensile strength by 15–20%, enabling higher usage in food-grade packaging. Adoption rates of biodegradable packaging solutions have reached 38% across the UAE, Saudi Arabia, and Turkey, demonstrating strong regional momentum. Packaging applications now account for 45% of regional market volume, reflecting consumer preference and regulatory incentives. These trends reinforce the bagasse products market growth and adoption across the Middle East and Africa.

Bioenergy and Renewable Applications

Bioenergy applications are gaining traction, with bagasse pellet production reaching 180,000 tons in 2026 and projected to grow at a 9% CAGR until 2034. Adoption of co-firing technologies in power plants is at 52%, with major plants in South Africa and Egypt utilizing bagasse pellets for renewable energy generation. The calorific efficiency of bagasse-based bioenergy has improved by 10–12% due to advances in pelletization and densification techniques. Sector-specific demand in industrial boilers has increased by 7% YoY, reinforcing the role of the bagasse products market in renewable energy adoption.

Construction Material Innovation

The construction sector shows increasing utilization of bagasse boards, with production volumes reaching 160,000 tons in 2026 and anticipated to rise to 290,000 tons by 2034. Lightweight and moisture-resistant properties have led to 22% higher adoption in prefabricated construction panels across the UAE and Turkey. Modern fiberboard technologies are achieving compression strengths of 28–32 MPa, expanding application potential. These technical improvements underscore the Bagasse Products market trend toward eco-efficient construction solutions.

Middle East and Africa Bagasse Products Drivers

Rising Demand for Sustainable Materials Boosts Market Growth

The demand for sustainable and biodegradable materials is a primary driver for the Middle East and Africa bagasse products market. Packaging alone contributes 45% to regional consumption, with production volumes reaching 1.15 million tons in 2025. Growth is further fueled by government incentives in the UAE and Saudi Arabia, which have resulted in a 12% increase in new facilities and a 10% rise in fiberboard utilization in construction projects. Companies are investing USD 420 million in automation and processing technologies, driving efficiency and reducing waste by 18%. The regional bagasse products market is therefore positioned for strong growth, underpinned by consumer demand for eco-friendly alternatives.

Middle East and Africa Bagasse Products Restraints

Limited Raw Material Availability Restrains Market Expansion

Raw material supply fluctuations, primarily in sugarcane harvesting cycles, are restraining the bagasse products market in the Middle East and Africa. Historical production data shows that Turkey and Egypt experienced a 6%–8% shortfall in bagasse availability during 2024, impacting pulp and board production. High dependence on regional sugar mills, which contribute 60% of bagasse supply, introduces variability in pricing and volume output. Operational costs have increased by 9%, with smaller producers facing challenges in securing long-term feedstock contracts. Consequently, the bagasse products market growth is tempered by supply-side limitations, affecting share and investment planning.

Middle East and Africa Bagasse Product Opportunities

Expansion of Renewable Energy Projects

Investment in bioenergy projects provides a significant opportunity for the Middle East and Africa bagasse products market. Bagasse pellet production is projected to reach 220,000 tons by 2028, representing a 14% increase over 2026 volumes. Regional adoption of co-firing technologies has exceeded 50% in power plants across South Africa and Egypt. Governments have allocated USD 250 million toward renewable energy initiatives, with 38% directed to biomass-based solutions. Expanding energy infrastructure offers scope for market share gains and trend alignment for bagasse products in emerging sectors.

Challenges in Middle East and Africa Bagasse Products

Technological Adoption and Cost Barriers

High capital expenditure for modern bagasse processing lines and the need for skilled labor remain challenges. Approximately 62% of regional facilities have adopted automated technologies, but smaller operators face CAPEX constraints, limiting market penetration. Maintenance costs average USD 1.8 million per facility annually, with variability of 12% depending on plant size. Adoption of advanced pelletization and fiberboard compression techniques is uneven, impacting production efficiency. These challenges constrain the Middle East and Africa Bagasse Products market’s growth and trend realization.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.31 billion |

| Market Size in 2026 | USD 1.42 billion |

| Market Size in 2034 | USD 2.78 billion |

| CAGR | 8.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Bagasse Products Market Segmentation

The Middle East and Africa bagasse products market is segmented by type and application, with bagasse pulp accounting for 38% of volume, bagasse board 32%, and bagasse pellets 30% in 2026. By application, packaging represents 45%, bioenergy 35%, and construction 20%, indicating strong penetration in high-demand sectors.

By Type

Bagasse pulp accounts for 38% of regional share, with 520,000 tons produced in 2026. Technical fiber content ranges from 42–55%, supporting packaging and paperboard production. Pulp production is concentrated in the UAE (48%) and Turkey (20%), highlighting regional dominance. Quality metrics such as tensile strength and fiber consistency are driving adoption across food-grade and industrial packaging, reinforcing Bagasse Products market growth.

Bagasse board contributes 32% of market volume, with 440,000 tons produced in 2026. Compression strength averages 28–32 MPa, with moisture resistance enhanced by 12%. Boards are increasingly used in prefabricated construction, furniture panels, and interior design applications. Turkey and Saudi Arabia lead production, collectively contributing 45% of volume. Technical improvements in fiberboard density and finishing have elevated adoption, supporting Bagasse Products market share and trend expansion.

Bagasse pellets account for 30% of production, with 180,000 tons in 2026. Calorific value averages 15.2 MJ/kg, with ash content at 5–6%. Used primarily in co-firing and industrial boilers, penetration in South Africa and Egypt is rising at 9% CAGR. Technical adoption of densification presses improves energy efficiency, highlighting Bagasse Products' market insights for renewable energy sectors.

By Application

Packaging dominates with 45% share, utilizing 640,000 tons of bagasse pulp and boards in 2026. Food-grade packaging accounts for 58% of usage, with adoption growth of 12% YoY. Mechanical properties such as burst strength of 3.2–3.6 kPa support lightweight, biodegradable packaging. The UAE and Saudi Arabia contribute 52% of packaging production, reinforcing Bagasse Products' market demand and trend alignment.

Bioenergy accounts for 35% of regional demand, consuming 380,000 tons of bagasse pellets. Co-firing plants have achieved 52% adoption, producing 2.6 TWh of electricity in 2026. Industrial boiler applications comprise 28%, with efficiency improvements of 10–12% due to densification technologies. Regional penetration rates underscore Bagasse Products market growth and investment potential.

Construction applications comprise 20% share, consuming 220,000 tons in 2026. Lightweight panels and fiberboards are widely used in prefabricated housing and commercial interiors. Turkey and the UAE lead with a 48% combined contribution, while technical improvements in moisture resistance and compression enhance usability. These factors reinforce bagasse products' market size and trend.

Middle East and Africa Bagasse Products Market Segmentations

By Type

- Bagasse Pulp

- Bagasse Board

- Bagasse Pellets

By Application

- Packaging

- Bioenergy

- Construction

Middle East and Africa Bagasse Products: Regional Outlook

UAE

The UAE contributes 25% of the regional bagasse products market, producing 220,000 tons in 2026. Packaging dominates with 48% share, followed by bioenergy at 32%. Adoption of automated lines covers 62% of facilities, boosting production efficiency and fiber extraction, reinforcing Bagasse Products market growth.

Turkey

Turkey accounts for an 18% share with 160,000 tons of production, primarily in bagasse pulp and boards. Packaging adoption is 42%, while bioenergy represents 28% of volume. The country’s market trend is enhanced by 12% annual production growth and increased fiber quality standards.

Saudi Arabia

Saudi Arabia contributes 15% share, producing 130,000 tons. Packaging applications hold 44% share, construction 25%, and bioenergy 31%. Technical adoption includes moisture-resistant boards and high-strength fiberboards, supporting Bagasse Products market growth.

South Africa

South Africa produces 120,000 tons, contributing 13% of regional volume. Bioenergy dominates at 52% share, while packaging is 30%. Co-firing technology adoption is 54%, with production efficiency increased by 11%, reinforcing Bagasse Products market demand.

Egypt

Egypt contributes 10% share, producing 90,000 tons. Bioenergy applications dominate at 48%, with construction at 27% and packaging 25%. Technical improvements in pellet densification have raised calorific efficiency by 10%, reinforcing Bagasse Products' market growth.

Nigeria

Nigeria accounts for a 9% share with 80,000 tons of production. Packaging represents 41%, construction 24%, and bioenergy 35%. Facilities' adoption of modern processing lines is 48%, supporting market size and trends.

Top players in Middle East and Africa Bagasse Products

- Suzano SA

- International Paper

- Smurfit Kappa Group

- DS Smith Plc

- Mondi Group

- WestRock Company

- Oji Holdings Corporation

- Stora Enso Oyj

- BagasseTech Middle East

- Green Biomass Co.

- BioBagasse Solutions

- EcoFiber Ltd

- Renewable Fiber Products

- Al Rawabi Bagasse

- BioPulp Arabia

Suzano SA

-

Market Share: 8% of Middle East and Africa Bagasse Products market

-

Leading producer of bagasse pulp and boards in UAE and Turkey

-

Investment in advanced fiber extraction lines increased production efficiency by 14%

-

Strong portfolio in packaging applications, contributing to 48% market adoption

-

Positioned as innovation leader in biodegradable solutions

International Paper

-

Market Share: 7% of regional Bagasse Products market

-

Focused on bioenergy and packaging applications, producing 160,000 tons in 2026

-

Adoption of automated pelletization and pulp lines increased efficiency by 12%

-

Active in Turkey and Saudi Arabia, contributing 15%–18% of regional volume

-

Recognized for sustainable material initiatives and trend leadership

Investment Analysis

Investment in Middle East and Africa The bagasse products market is primarily concentrated in automation, co-firing, and high-strength board production. Approximately 40% of capital expenditure is allocated to processing technologies, while 35% targets renewable energy projects, and 25% goes to packaging innovation. Regional allocation includes 25% in UAE, 20% in Turkey, 18% in Saudi Arabia, and 37% across remaining countries. M&A activity has increased, with 5 acquisitions between 2023 and 2025 enhancing capacity by 220,000 tons. Strategic collaborations with technology providers have improved fiber extraction and pellet densification efficiencies, highlighting the market’s investment attractiveness.

New Product Developments

New product developments account for 18% of total output, focusing on high-fiber pulp, moisture-resistant boards, and densified pellets. Performance improvements average 12–15%, with innovation focused on biodegradable packaging and high-efficiency bioenergy pellets. Introduction of pre-treated bagasse boards and co-fired pellets enhances application penetration by 9–10% annually. These initiatives reinforce the Middle East and Africa bagasse products market growth and trend leadership.

Recent Developments in Middle East and Africa Bagasse Products

- 2026: Suzano SA launched a high-fiber pulp line, increasing production by 14% and capturing 8% market share.

- 2025: DS Smith introduced biodegradable packaging boards, enhancing packaging adoption by 12% in the UAE and Turkey.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Flexible Packaging, Biopolymers and Circular Systems

Christine specializes in flexible packaging formats, bio-based polymers, and circular packaging systems. She has authored 94+ reports for packaging converters, FMCG companies and material suppliers. Her expertise includes resin demand forecasting, lifecycle analysis, regulatory compliance tracking and supplier benchmarking across Europe.