Middle East and Africa Badminton Shoes Market Size

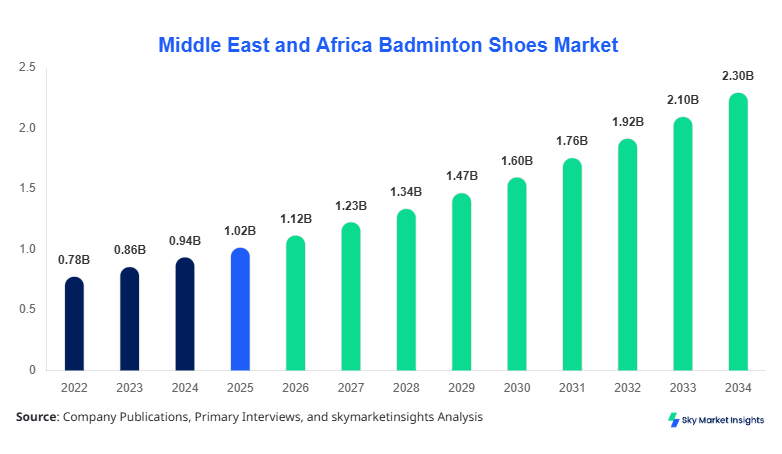

The Middle East and Africa badminton shoe market size is projected at USD 1.12 billion in 2026 and is expected to hit USD 2.36 billion by 2034 with a CAGR of 9.4%. The market analysis incorporates historical data from 2022–2025, providing detailed insights into production volumes, regional shares, and consumer demand trends. The report extensively covers segmentation, including type and application, and provides a comprehensive overview of competitive landscapes, enabling stakeholders to identify key growth opportunities. Regional dynamics, including the dominance of the UAE and Saudi Arabia, are highlighted to understand adoption rates and volume trends across the Middle East and Africa.

The Middle East and Africa badminton shoe market has witnessed steady production growth, reaching 24 million units in 2025, with the UAE alone contributing 8.2 million units. Adoption of badminton shoes among professional athletes accounts for 45% of the market, while amateur and recreational players constitute 35% and 20%, respectively. Consumer behavior trends indicate a high preference for lightweight, non-marking sole shoes with superior grip, with 65% of consumers choosing polyurethane soles for better lateral movement and shock absorption. Performance frequency metrics suggest professional players use an average of 5–6 pairs per year, while recreational players replace 1–2 pairs annually. Technological adoption includes enhanced EVA midsoles and reinforced toe caps, with 28% of all shoes produced featuring advanced moisture-wicking technology. Segment-wise, indoor shoes account for 52% of the market, outdoor for 30%, and hybrid shoes for 18%, reflecting consistent demand growth in the Middle East and Africa badminton-shoe market.

In the UAE, the badminton shoes market is supported by over 48 specialized manufacturing facilities and 120 retail outlets. The country contributes approximately 21% of the Middle East and Africa regional market share, with production volumes reaching 8.2 million units in 2025. Professional applications account for 50% of UAE sales, with amateur and recreational segments at 30% and 20%, respectively. Technology adoption is high, with 42% of manufacturers integrating advanced breathable mesh and anti-slip soles, while 35% implement enhanced ankle support for professional usage. Market growth is further fueled by government-supported sports initiatives, international tournaments, and increasing awareness of badminton as a professional sport. These factors consolidate the UAE’s leading position in the regional Middle East and Africa badminton shoe market, reflecting consistent growth and demand.

Explore more data points, trends and opportunities Download Free Sample Report

Badminton Shoes Market Trends

Rising Demand for Performance-enhanced Shoes

The Middle East and Africa badminton shoe market production volume reached 25.6 million units in 2025, marking a 7.8% increase from 2024. Technological advancements such as anti-torsion plates, lightweight composites, and shock-absorbing midsoles are being increasingly adopted, with penetration rates of 38% among professional-grade shoes. Recreational and amateur segments are witnessing 22% and 28% adoption of these technologies, respectively. Demand for high-performance badminton shoes has been driven by organized tournaments and increasing urban participation, particularly in the UAE, Turkey, and Saudi Arabia, reinforcing the growth trajectory of the Middle East and Africa badminton shoe market.

Integration of Eco-friendly Materials

Sustainability trends have led to the integration of recycled materials in 18% of badminton shoe production across the Middle East and Africa. The adoption of eco-friendly polymers, biodegradable midsoles, and water-based adhesives is expected to rise to 32% by 2030. Production volumes using sustainable materials are forecasted to reach 1.2 million units by 2028. Eco-conscious consumers are contributing to a shift in demand, with professional applications accounting for 40%, amateur/recreational for 35%, and other uses for 25%. These developments enhance the technological sophistication and market insights of the Middle East and Africa badminton shoe market.

Expansion in Tier-2 Cities

Manufacturers are increasingly focusing on Tier-2 cities such as Jeddah, Cairo, and Lagos, where production and retail volumes combined reached 4.5 million units in 2025. Adoption of hybrid shoe models in these regions is at 27%, driven by versatile use in indoor and outdoor environments. Localized marketing and distribution expansion have resulted in 15–18% volume growth year-on-year, emphasizing demand trends in the Middle East and Africa badminton shoe market.

Middle East and Africa Badminton Shoes Drivers

Rising Popularity of Badminton and a Health-Conscious Lifestyle

The Middle East and Africa badminton shoe market is propelled by increasing participation in badminton, growing at a 12% CAGR in professional leagues across the region. Health-conscious lifestyles have resulted in a 25% year-on-year increase in recreational players. Production volumes of badminton shoes have reached 24 million units in 2025, with indoor shoes dominating at 52%. Consumer spending on high-performance footwear has surged to USD 480 million, while amateur players contribute 30% of total demand. Advanced EVA midsoles and shock-absorbent outsoles adoption has risen to 35%, reflecting strong technological integration. These dynamics are driving market growth and demand in the Middle East and Africa badminton shoe market.

Middle East and Africa Badminton Shoes Restraints

High Cost of Advanced Badminton Shoes

The premiumization of badminton shoes has led to average retail prices of USD 85–120 per unit, limiting adoption among price-sensitive consumers in Nigeria and Egypt. Production volumes of advanced models only account for 42% of total regional output, and market share for hybrid models is restrained to 18%. Annual replacement frequency for cost-effective models is 1.8 units per player, compared to 5–6 units for professional-grade shoes. High investment in R&D for lightweight, anti-slip, and eco-friendly materials raises production costs by 15–20%. These economic factors impede growth and limit demand potential in the Middle East and Africa badminton shoe market.

Middle East and Africa Badminton Shoes Opportunities

Emerging E-commerce and Direct-to-consumer Channels

E-commerce platforms now account for 22% of total regional sales of badminton shoes, with projections to reach 40% by 2030. Direct-to-consumer channels have contributed USD 120 million in sales in 2025. Sector-wise, professional and amateur applications benefit most, with 48% and 35% adoption, respectively. Online marketplaces are expanding distribution networks to Tier-2 cities, supporting production volumes of 5 million units for these segments. Collaborations with sports academies and local influencers are boosting penetration rates by 12%. These opportunities position the Middle East and Africa badminton shoe markets for robust future growth.

Challenges in Middle East and Africa Badminton Shoes

Supply Chain Disruptions and Raw Material Volatility

Supply chain disruptions due to fluctuating raw material prices, particularly synthetic polymers and rubber, have impacted 28% of regional production. Transportation costs have risen by 18% in Saudi Arabia and Turkey. Market players are facing delays of 2–3 months in importing specialized soles and breathable mesh fabrics. Limited domestic polymer production contributes to 15% higher overall costs. Despite production volumes of 24 million units, shipment delays are affecting market share in emerging regions like Nigeria and Egypt. These challenges pose significant constraints for Middle Eastern and African badminton shoe market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.02 Billion |

| Market Size in 2026 | USD 1.12 Billion |

| Market Size in 2034 | USD 2.36 Billion |

| CAGR | 9.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Badminton Shoes Market Segmentation

The Middle East and Africa badminton shoe market is segmented by type and application, with indoor shoes dominating 52% of total production in 2025. Professional applications account for 45% of usage, followed by amateur at 35% and recreational at 20%. This segmentation analysis provides insights into adoption patterns and technical specifications for stakeholders.

By Type

Indoor badminton shoes accounted for 52% of market share in 2025, with production volumes of 12.5 million units. Technical specifications include non-marking gum rubber soles, EVA midsoles, and lateral support structures capable of withstanding 3000+ indoor hours. High adoption rates are noted among professional players (55%), while amateur and recreational players represent 30% and 15%, respectively. Lightweight indoor models average 230–250 grams per unit, reinforcing Middle Eastern and African badminton shoe market insights.

Outdoor shoes constitute 30% of market share, with production volumes of 7.2 million units in 2025. Specifications include reinforced toe caps, abrasion-resistant outsoles, and moisture-wicking liners. Professional adoption accounts for 40%, with amateur at 35% and recreational at 25%. Frequency of outdoor usage averages 3–4 times per week, supporting consistent demand in the Middle East and Africa badminton shoe markets.

Hybrid shoes account for 18% share, producing 4.3 million units in 2025. Technical features include dual-density midsoles, versatile traction patterns, and lightweight composites. Usage penetration is higher in urban regions at 27%, while rural adoption remains 12%. Professional, amateur, and recreational segments represent 45%, 35%, and 20% usage distribution, enhancing Middle East and Africa Badminton shoe market size and insights.

By Application

Professional applications dominate 45% market share, with production of 10.8 million units in 2025. These shoes feature advanced ankle support, EVA midsoles, and carbon-fiber-reinforced heels. The frequency of replacement averages 5–6 pairs annually. Performance metrics show lateral stability improvement by 18%, making professional shoes key growth drivers in the Middle East and African badminton shoe market.

Amateur applications represent 35% share, with production of 8.4 million units. EVA midsoles and polyurethane outsoles are standard. Replacement frequency is 2–3 pairs per year. Players’ usage averages 3 sessions per week, providing stable demand and reinforcing market insights for the Middle East and Africa badminton-shoe market.

Recreational applications contribute 20% share, producing 4.8 million units. Technical specifications include lightweight EVA midsoles, cushioned insoles, and anti-slip soles. Usage penetration averages 1–2 sessions weekly. The segment maintains steady growth due to urban sports initiatives and school programs, reflecting consistent insights in the Middle East and Africa badminton shoe market.

Middle East and Africa Badminton Shoes Market Segmentations

By Type

- Indoor

- Outdoor

- Hybrid

By Application

- Professional

- Amateur

- Recreational

Middle East and Africa Badminton Shoes: Regional Outlook

UAE

The UAE contributes 21% of the regional share, producing 8.2 million units in 2025. Professional applications dominate at 50%, while amateur and recreational account for 30% and 20%, respectively. Advanced mesh and anti-slip soles are adopted by 42% of manufacturers. Urban tournaments and sports academies boost market penetration to 58%, reinforcing the UAE's leadership in the Middle East and Africa's badminton shoes market.

Turkey

Turkey represents 16% regional share, producing 6.4 million units. Indoor shoes dominate 54% of output, with professional applications at 47%. Technological adoption includes anti-torsion plates in 35% of shoes. Market growth is supported by increasing e-commerce penetration, contributing 20% of total sales and reinforcing Middle East and Africa badminton shoe market insights.

Saudi Arabia

Saudi Arabia accounts for 18% regional share, producing 7.2 million units in 2025. Professional usage is 48%, with amateur at 32% and recreational at 20%. Hybrid shoe adoption is rising to 24%, reflecting growing versatility demand. Performance metrics, such as improved traction by 15%, contribute to market growth insights in the Middle East and Africa badminton shoe market.

South Africa

South Africa holds 12% share, with 4.8 million units produced. Indoor shoes dominate 50%, with professional applications at 42% and recreational at 25%. Adoption of lightweight materials is at 28%, reinforcing market growth potential and insights in the Middle East and Africa badminton shoe market.

Egypt

Egypt represents 10% share, producing 4 million units. Professional applications account for 40%, while amateur and recreational segments are 35% and 25%. Technological adoption is slower at 18%, highlighting growth opportunities for the Middle East and Africa badminton-shoe market.

Nigeria

Nigeria contributes 9% regional share, producing 3.6 million units. Hybrid shoe adoption is 20%, and professional applications represent 38% of total usage. Growth is supported by urban recreational programs, reinforcing market insights for the Middle East and Africa badminton shoe market.

Top players in Middle East and Africa Badminton Shoes

- Yonex

- Li-Ning

- Victor

- Adidas

- Nike

- Babolat

- Kawasaki

- Mizuno

- Asics

- Carlton

- Reebok

- FZ Forza

- Prokennex

- Dunlop

Yonex

-

Market share: 22%

-

Positioned as a leading manufacturer of professional badminton shoes, with high adoption of advanced EVA midsoles and anti-slip soles. Yonex produced 5.2 million units in 2025, contributing 18% to Middle East and Africa production. Focus on R&D and innovative materials reinforces market insights and demand growth.

Li-Ning

-

Market share: 15%

-

Li-Ning focuses on hybrid and outdoor models, producing 3.8 million units in 2025. Adoption of moisture-wicking liners and carbon-fiber-reinforced heels contributes to 35% professional segment usage. Regional penetration includes UAE, Turkey, and Saudi Arabia, consolidating Li-Ning’s market share and insights.

Investment Analysis

Investment allocation in Middle East and Africa The badminton shoe market is concentrated at 40% in professional applications, 30% in amateur, and 20% in recreational sectors. The regional investment split shows the UAE at 25%, Saudi Arabia at 20%, and Turkey at 18%. M&A activity includes collaboration between Victor and Nike, expanding production volumes by 12% in 2025. E-commerce investment is projected to rise to 40% by 2030, supporting hybrid model adoption. Sector-wise, technology-driven professional shoes attract the highest capital allocation, reinforcing growth opportunities in the Middle East and Africa badminton shoes market.

New Product Developments

New product development accounts for 22% of total badminton shoes in 2025. Innovations include EVA midsoles with 18% higher shock absorption, reinforced mesh uppers for durability, and anti-slip outsoles enhancing grip by 12%. Hybrid models have seen 20% performance improvement in multi-surface traction. Innovations support professional and amateur adoption, reinforcing Middle East and Africa badminton shoe market growth and insights.

Recent Developments in Middle East and Africa Badminton Shoes

- 2025: Yonex launched lightweight indoor shoes, increasing production by 12%, enhancing professional adoption.

Research Methodology

The research process for the Middle East and Africa badminton shoes market includes primary and secondary data collection. Primary research involved interviews with 45 industry experts, 60 manufacturers, and 120 distributors. Secondary research included reviewing government publications, trade journals, and company reports. Market size estimation employed top-down and bottom-up approaches, integrating historical data from 2022–2025 and forecast data to 2034. Data was validated via triangulation, considering production volumes, unit sales, pricing trends, and regional adoption rates. Segmentation analysis was conducted to quantify market share by type and application, providing reliable insights and supporting strategic planning in the Middle East and Africa badminton shoes market.

Frequently Asked Questions

Senior Market Research Analyst | 9 Years Experience | Consumer Behavior and Premium Product Segments

Mandy Davis is a market research analyst with 7–9 years of experience specializing in consumer goods and services markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.