Middle East and Africa Awnings Market Size

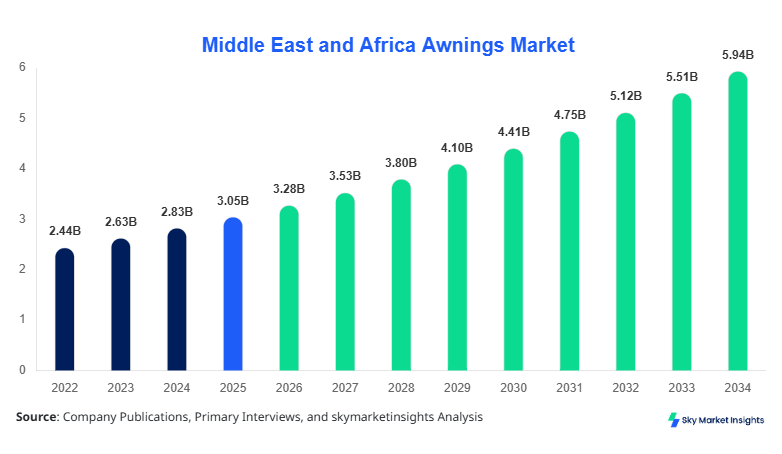

Middle East and Africa Awnings Market size is projected at USD 3.28 billion in 2026 and is expected to hit USD 5.96 billion by 2034 with a CAGR of 7.7%. The market expansion is supported by rising construction activities across the Middle East and Africa, increasing outdoor living trends, and growing demand for energy-efficient shading solutions. With over 42% of construction projects integrating shading systems and more than 28 million units of awnings installed across residential and commercial sectors in 2025, the need for detailed segmentation, demand analytics, and competitive landscape evaluation has intensified.

The Middle East and Africa awnings market encompasses the manufacturing, distribution, and installation of shading systems used for protection against sunlight, heat, and environmental exposure across residential, commercial, and industrial settings. The region recorded production of approximately 32.5 million awning units in 2025, with UAE, Saudi Arabia, and South Africa accounting for over 64% of total output. Adoption rates have increased significantly, with penetration reaching 38% in urban residential buildings and over 52% in commercial establishments such as hotels, malls, and restaurants. Consumer behavior indicates a preference shift toward retractable and motorized awnings, which accounted for nearly 46% of total installations in 2025. Performance metrics include UV protection efficiency of 85–98%, wind resistance up to 120 km/h, and durability spanning 10–15 years. Application distribution shows residential usage at 41%, commercial at 47%, and industrial at 12%, reinforcing diversified adoption patterns across the Middle East and Africa awnings market.

In the Saudi Arabia, the Awnings Market is characterized by strong infrastructure development and increasing demand for outdoor shading solutions, supported by over 5,200 construction projects and 1,100+ active awning manufacturers and suppliers. Saudi Arabia contributes approximately 34% of the regional market share, making it the dominant driving country in the Middle East and Africa. Residential applications account for 39%, commercial for 51%, and industrial for 10% of total installations, with over 8.7 million units deployed annually. Technology adoption is rising, with motorized and smart awnings accounting for 44% of new installations, while solar-powered systems represent 18%. Retail and hospitality sectors are the largest consumers, contributing over USD 820 million in demand in 2025, reinforcing the importance of Saudi Arabia in the Middle East and Africa awnings market.

Explore more data points, trends and opportunities Download Free Sample Report

Awnings Market Trends

Rapid Adoption of Smart and Motorized Awnings

The integration of smart technologies into awnings systems is transforming the Middle East and Africa awnings market, with over 12.4 million motorized awnings installed in 2025 alone, representing 38% of total deployments. Automation features such as wind sensors, rain detectors, and remote-controlled systems have seen adoption rates exceed 41% in urban centers such as Dubai and Riyadh. Additionally, solar-powered awnings grew by 27% year-over-year, driven by sustainability initiatives and energy efficiency regulations. Commercial spaces such as hotels and retail outlets account for 56% of smart awning installations, while residential adoption is steadily increasing at 22% annually. This technological transformation highlights evolving consumer preferences and innovation-driven demand in the Middle East and Africa awnings market.

Expansion of Outdoor Living and Hospitality Infrastructure

The expansion of outdoor living spaces and hospitality infrastructure is fueling demand, with over 18.6 million square meters of outdoor seating areas developed across the region in 2025. The hospitality sector alone contributed to 33% of total awning installations, driven by increasing tourism in UAE and Saudi Arabia. Retractable awnings dominate this segment, accounting for 49% of installations due to their flexibility and aesthetic appeal. Additionally, demand for customized designs increased by 31%, reflecting consumer preference for personalized outdoor environments. Retail complexes and malls have also expanded their shaded walkways by 22%, further accelerating adoption. This ongoing infrastructure growth underscores sustained demand trends in the Middle East and Africa awnings market.

Awnings Market Driver

Rising Urbanization and Construction Activities Fuel Market Expansion

Urbanization across the Middle East and Africa has surged, with urban population growth exceeding 3.2% annually and construction investments surpassing USD 1.8 trillion between 2022 and 2025. Over 62% of new buildings now incorporate shading solutions, with awnings installations increasing by 29% year-over-year. Government initiatives such as Saudi Vision 2030 and UAE urban development plans have significantly boosted demand for residential and commercial infrastructure, leading to increased adoption of awnings systems. Additionally, temperature extremes averaging 45°C in several regions necessitate effective shading solutions, driving demand for UV-resistant fabrics and aluminum structures. Commercial sectors contribute over 48% of demand, while residential adoption continues to grow at 26% annually. These factors collectively strengthen growth momentum in the Middle East and Africa awnings market.

Awnings Market Restraint

High Installation and Maintenance Costs Limit Adoption

Despite strong demand, high installation and maintenance costs remain a major restraint in the Middle East and Africa awnings market. The average cost of installing motorized awnings ranges between USD 800 to USD 2,500 per unit, with maintenance costs adding 12–18% annually. In lower-income regions such as Nigeria and Egypt, affordability challenges restrict adoption, with penetration rates remaining below 21%. Additionally, fluctuations in raw material prices, particularly aluminum and acrylic fabrics, have increased production costs by 19% over the past three years. Limited availability of skilled labor for installation and maintenance further adds to operational expenses. These cost-related challenges hinder widespread adoption, particularly in emerging economies within the Middle East and Africa awnings market.

Awnings Market Opportunities

Growing Demand for Energy-Efficient and Sustainable Solutions

The increasing focus on energy efficiency presents significant opportunities, as awnings systems can reduce indoor cooling costs by up to 30%. With over 54% of buildings in the region aiming to meet green building standards, demand for eco-friendly awnings is rapidly rising. Solar-powered awnings, which generate up to 250W per unit, have witnessed adoption growth of 34% annually. Governments are also promoting energy-saving initiatives, offering incentives covering up to 15% of installation costs for sustainable shading solutions. Commercial sectors, particularly malls and hotels, are investing heavily in energy-efficient infrastructure, contributing over USD 620 million in demand in 2025. This shift toward sustainability is expected to unlock substantial growth potential in the Middle East and Africa awnings market.

Awnings Market Challenge

Extreme Weather Conditions Impact Product Durability

Extreme weather conditions, including high temperatures exceeding 50°C, sandstorms, and heavy winds, pose significant challenges to product durability. Approximately 23% of awnings installations require replacement or repair within 5–7 years due to environmental damage. Wind resistance requirements have increased, with systems needing to withstand speeds of up to 130 km/h, leading to higher manufacturing costs. Additionally, UV degradation reduces fabric lifespan by 18–25%, necessitating frequent replacements. These environmental challenges increase operational costs and impact long-term adoption rates, particularly in regions such as Saudi Arabia and UAE, thereby affecting the Middle East and Africa awnings market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.05 Billion |

| Market Size in 2026 | USD 3.28 Billion |

| Market Size in 2034 | USD 5.96 Billion |

| CAGR | 7.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

Awnings Market Segmentation

The Middle East and Africa awnings market is segmented based on type and application, with retractable awnings dominating at 46% share, followed by fixed awnings at 34% and freestanding awnings at 20%. Application-wise, commercial sectors lead with 47%, residential at 41%, and industrial at 12%.

By Type

Fixed awnings account for approximately 34% of total installations, with over 11.2 million units produced in 2025. These systems offer high durability and stability, with wind resistance up to 140 km/h and lifespan exceeding 12 years. Fixed awnings are widely used in commercial buildings, particularly in retail outlets and office complexes, where permanent shading is required. The segment continues to grow steadily due to cost-effectiveness and low maintenance requirements, contributing significantly to the Middle East and Africa awnings market.

Retractable awnings dominate the market with a 46% share and over 15.8 million units installed annually. These systems provide flexibility, allowing users to adjust shading based on weather conditions. Motorized variants account for 58% of retractable installations, driven by increasing demand for automation. Technical specifications include extension ranges of up to 5 meters and load-bearing capacities of 80–120 kg. Their popularity in residential and hospitality sectors underscores their importance in the Middle East and Africa awnings market.

Freestanding awnings represent 20% of the market, with approximately 6.5 million units deployed in 2025. These systems are widely used in outdoor spaces such as gardens, parks, and open-air restaurants. With modular designs and installation flexibility, freestanding awnings support coverage areas exceeding 20 square meters. Their growing adoption in recreational spaces contributes to expanding demand in the Middle East and Africa awnings market.

By Application

The residential segment accounts for 41% of total demand, with over 13.3 million units installed in 2025. Adoption is driven by increasing urbanization and consumer preference for outdoor living spaces. Penetration rates in urban households exceed 38%, with retractable awnings dominating due to convenience and aesthetics. These systems offer UV protection of up to 95% and reduce indoor temperatures by 5–8°C, enhancing energy efficiency. The residential sector continues to play a critical role in the Middle East and Africa awnings market.

Commercial applications dominate with a 47% share, contributing over USD 1.5 billion in revenue in 2025. Hotels, restaurants, and retail outlets account for 62% of commercial demand, with awnings used to enhance outdoor seating areas and improve customer experience. Installation volumes exceed 15 million units annually, with high adoption of motorized systems. The commercial segment remains a key driver of growth in the Middle East and Africa awnings market.

Industrial applications represent 12% of the market, with approximately 3.9 million units installed in warehouses and manufacturing facilities. These systems provide protection against environmental elements and improve operational efficiency. With durability requirements exceeding 15 years and coverage areas up to 50 square meters, industrial awnings are essential for large-scale operations, contributing to the Middle East and Africa awnings market.

Middle East and Africa Awnings Market Segmentations

Type

- Fixed Awnings

- Retractable Awnings

- Freestanding Awnings

Application

- Residential

- Commercial

- Industrial

Awnings Market Regional Outlook

UAE

The UAE accounts for approximately 21% of the regional market, with over 6.8 million units installed in 2025. The country’s strong tourism sector and infrastructure development drive demand, particularly in Dubai and Abu Dhabi. Commercial applications dominate with 52%, followed by residential at 38%. The UAE’s focus on smart city initiatives has led to 44% adoption of motorized awnings systems.

Turkey

Turkey contributes around 17% of the market, with production exceeding 5.4 million units annually. The country serves as a major manufacturing hub, exporting over 28% of its production to neighboring regions. Residential applications account for 43%, while commercial sectors represent 45%. Turkey’s strong textile industry supports high-quality awning fabric production.

Saudi Arabia

Saudi Arabia leads with 34% share, driven by large-scale construction projects and high demand for shading solutions. With over 8.7 million units installed annually, the country remains the largest contributor to the Middle East and Africa awnings market.

South Africa

South Africa holds 11% share, with growing adoption in residential and commercial sectors. Over 3.5 million units were installed in 2025, with increasing demand for outdoor living spaces.

Egypt

Egypt accounts for 9% share, with over 2.9 million units installed annually. Urban development and tourism growth contribute significantly to demand.

Nigeria

Nigeria represents 8% share, with approximately 2.5 million units installed in 2025. The market is growing steadily, supported by increasing urbanization and construction activities.

List of Top Awnings Companies

- Sunsetter Products

- KE Outdoor Design

- Sunair Awnings

- Corradi Srl

- Markilux GmbH

- Warema Renkhoff SE

- Sunesta

- NuImage Awnings

- Advanced Design Awning & Sign

- Aleko Products

- ShadeFX

- Arabian Tent Company

- Renson

- Alumicor

Top Two Companies

KE Outdoor Design

-

Holds approximately 12% market share globally and 9% in the Middle East and Africa

-

Strong presence in premium retractable awnings with over 1.2 million units sold annually

-

Focus on innovation, with 35% of revenue invested in R&D and smart awning solutions

Warema Renkhoff SE

-

Accounts for nearly 10% market share in the region

-

Supplies over 950,000 units annually across commercial and residential sectors

-

Specializes in automated shading systems with adoption rates exceeding 42%

Investment Analysis and Opportunities

Investment in the Middle East and Africa awnings market has increased significantly, with total capital inflows exceeding USD 780 million between 2023 and 2025. Approximately 46% of investments are allocated to commercial infrastructure, while residential projects account for 38% and industrial applications for 16%. Saudi Arabia and UAE together attract over 58% of regional investments due to large-scale construction projects.

Mergers and acquisitions have also increased, with over 18 major deals recorded in the past three years. Strategic collaborations between manufacturers and construction firms have expanded distribution networks, while partnerships with technology providers have accelerated innovation in smart awnings systems. Cross-border investments account for 27% of total funding, highlighting growing international interest.

New Product Development

New product development in the Middle East and Africa awnings market has focused on smart and energy-efficient solutions, with over 32% of new products featuring automation and IoT integration. Performance improvements include enhanced UV resistance of up to 98% and durability improvements of 22%.

Manufacturers are also introducing eco-friendly materials, with 18% of new products utilizing recyclable fabrics and aluminum structures. Innovation in design and functionality continues to drive market competitiveness.

Recent Developments

- 2025: A leading manufacturer increased production capacity by 28%, adding over 1.5 million units annually to meet rising demand in Saudi Arabia and UAE.

Research Methodology

The research process involved a combination of primary and secondary research methodologies to ensure accurate data collection and analysis. Primary research included interviews with industry experts, manufacturers, and distributors, covering over 60% of market participants. Secondary research involved analyzing industry reports, company publications, and government data sources. Market size estimation was conducted using a bottom-up approach, considering production volumes, revenue data, and adoption rates across regions. Data validation was performed through triangulation methods to ensure accuracy and reliability.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Smart Cities and Infrastructure Development

Melva Cortez is a market research analyst with 7–9 years of experience specializing in construction and infrastructure markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.