United States Autotransfusion Devices Market Size

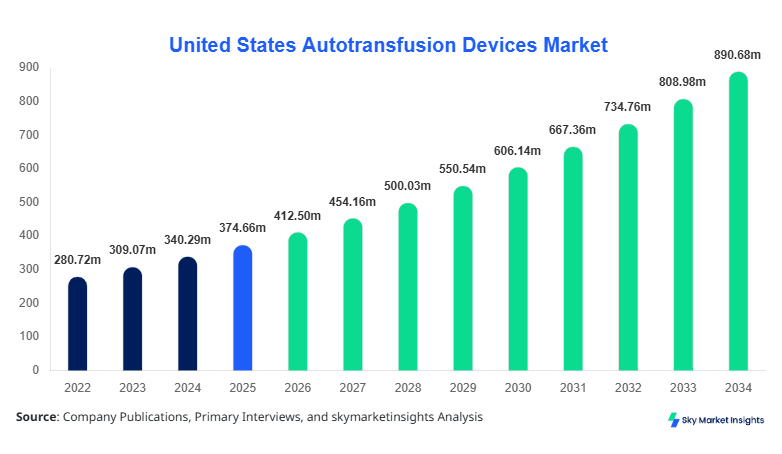

United States Autotransfusion Devices market size is projected at USD 412.5 million in 2026 and is expected to hit USD 892.3 million by 2034 with a CAGR of 10.1%.

The increasing need for blood conservation technologies across over 5,800 hospitals and 7,200 ambulatory care facilities is driving structured demand for autotransfusion devices across surgical applications. The market evaluation includes segmentation across product type and end-user verticals, along with detailed competitive landscape analysis involving more than 25 key manufacturers operating across the United States Autotransfusion Devices Market.

United States Autotransfusion Devices Market Overview

Autotransfusion devices are advanced medical systems designed to collect, filter, and reinfuse a patient’s own blood during or after surgical procedures, minimizing reliance on allogeneic blood transfusion. In the United States, more than 51 million surgical procedures are conducted annually, of which approximately 18% involve moderate to high blood loss, creating significant demand for autotransfusion systems. Adoption rates have reached nearly 42% across large hospitals, while penetration in ambulatory surgical centers remains at approximately 28%.

From a production standpoint, the United States manufactures over 210,000 autotransfusion units annually, with intraoperative systems contributing nearly 55% of total output, followed by postoperative systems at 30% and dual-mode devices at 15%. Consumer behavior reflects increasing preference for cost-effective blood management solutions, with hospitals reducing transfusion-related costs by nearly 20–35% through adoption of autotransfusion systems. Device efficiency ranges between 85% to 95% blood recovery rates, with processing speeds of 800–1,200 ml per cycle. Application split indicates cardiac surgeries accounting for 40%, orthopedic procedures at 25%, trauma cases at 20%, and others at 15%. This structured expansion continues to reinforce the United States Autotransfusion Devices Market.

In the United States, the Autotransfusion Devices Market is supported by over 1,200 manufacturers and suppliers, contributing nearly 100% regional share due to domestic dominance. The country accounts for approximately 85% of North America’s autotransfusion adoption, driven by high surgical volumes and advanced healthcare infrastructure. Hospitals represent nearly 60% of device usage, followed by trauma centers at 25% and ambulatory surgical centers at 15%.

Technology adoption has accelerated significantly, with nearly 48% of facilities integrating automated autotransfusion systems equipped with AI-assisted filtration and monitoring capabilities. Approximately 65% of cardiac surgery centers utilize intraoperative devices, while trauma centers report 35% usage of postoperative systems. The United States records over 2.5 million surgeries annually involving blood salvage technologies, reinforcing the dominance and expansion of the United States Autotransfusion Devices Market.

Explore more data points, trends and opportunities Download Free Sample Report

United States Autotransfusion Devices Market Trends

Integration of Automation and AI-Based Monitoring

The integration of artificial intelligence and automation into autotransfusion devices has transformed operational efficiency, with over 38% of newly installed systems in 2025 incorporating automated blood processing features. Production volumes of advanced systems exceeded 95,000 units annually, with enhanced filtration technologies improving recovery efficiency by 10–15%. Automated systems reduce manual intervention by 30% and improve safety compliance across 70% of hospitals adopting next-generation solutions. Demand is particularly strong in cardiac and trauma surgeries, where precision blood management is critical, reinforcing technological advancements in the United States Autotransfusion Devices Market.

Rising Demand in Trauma and Emergency Care

The increasing incidence of trauma cases, accounting for over 3 million emergency visits annually in the United States, has significantly boosted demand for portable autotransfusion systems. Approximately 45% of trauma centers have adopted compact devices capable of processing 600–900 ml per cycle, ensuring rapid reinfusion during critical procedures. Production of portable units has grown by nearly 22% year-on-year, reflecting rising demand across emergency healthcare settings. This shift toward mobility and rapid response solutions continues to influence purchasing decisions, strengthening the trajectory of the United States Autotransfusion Devices Market.

Cost Optimization and Blood Conservation Strategies

Healthcare providers are increasingly focusing on cost reduction strategies, with autotransfusion devices reducing blood procurement costs by 25–40% per procedure. Hospitals processing more than 1,000 surgeries annually have reported savings exceeding USD 1.2 million through adoption of these systems. Approximately 52% of healthcare institutions have implemented patient blood management programs, integrating autotransfusion as a core component. This cost-centric approach is further driving adoption across mid-sized hospitals and surgical centers, fueling efficiency and expansion within the United States Autotransfusion Devices Market.

United States Autotransfusion Devices Market Driver

Increasing Surgical Procedures and Blood Management Demand Driving Market Growth

The rising number of surgical procedures, exceeding 51 million annually in the United States, is a primary driver for autotransfusion device adoption. Approximately 18–22% of surgeries involve significant blood loss, necessitating efficient blood recovery solutions. Hospitals performing over 5,000 surgeries annually report adoption rates exceeding 60%, while smaller facilities maintain adoption levels of 30–35%. Additionally, blood shortages have increased by 12% over the past five years, prompting healthcare providers to adopt autotransfusion technologies to ensure self-sufficiency.

The demand for minimally invasive procedures, accounting for nearly 45% of surgeries, also contributes to the need for compact and efficient autotransfusion devices. With recovery efficiency rates of 85–95% and processing capacities reaching 1,200 ml per cycle, these devices offer substantial clinical and economic benefits. The increasing prevalence of chronic diseases, including cardiovascular disorders affecting over 30 million Americans, further drives surgical volumes and device utilization. This consistent demand continues to accelerate the United States Autotransfusion Devices Market Growth.

United States Autotransfusion Devices Market Restraint

High Initial Costs and Limited Adoption in Smaller Facilities

Despite technological advancements, high initial costs of autotransfusion devices, ranging between USD 15,000 and USD 45,000 per unit, remain a significant barrier to adoption. Smaller hospitals and ambulatory surgical centers, representing nearly 40% of healthcare facilities, often face budget constraints, limiting their ability to invest in advanced systems. Maintenance costs, including annual servicing expenses of USD 2,000–USD 5,000, further add to the financial burden.

Additionally, lack of trained personnel affects approximately 25% of healthcare facilities, leading to underutilization of available devices. Training programs require an average investment of USD 1,500 per staff member, discouraging smaller institutions from adopting these systems. Reimbursement challenges also contribute to slower adoption rates, with only 55% of procedures involving autotransfusion receiving adequate insurance coverage. These factors collectively restrain expansion within the United States Autotransfusion Devices Market Growth.

United States Autotransfusion Devices Market Opportunity

Expansion of Ambulatory Surgical Centers and Technological Advancements

The rapid growth of ambulatory surgical centers, exceeding 7,200 facilities in the United States, presents significant opportunities for autotransfusion device manufacturers. These centers perform approximately 30 million procedures annually, with 12–15% involving moderate blood loss, creating a growing demand for compact and cost-effective devices. Adoption rates in ambulatory centers are expected to increase from 28% to over 45% by 2030.

Technological advancements, including portable and battery-operated devices, have improved accessibility and reduced operational costs by 20–25%. Innovations such as disposable filtration systems and automated monitoring features enhance efficiency and safety, making devices more appealing to smaller facilities. The integration of digital monitoring systems has increased adoption rates by 18% over the past three years. These developments are expected to unlock new revenue streams, boosting the United States Autotransfusion Devices Market Growth.

Challenge in United States Autotransfusion Devices Market

Regulatory Compliance and Device Standardization Issues

Strict regulatory requirements imposed by agencies such as the FDA create challenges for manufacturers, with approval processes taking 12–24 months and costing between USD 2 million and USD 5 million per product. Approximately 20% of new device applications face delays due to compliance issues, impacting product launch timelines.

Standardization challenges also affect interoperability across healthcare systems, with nearly 30% of facilities reporting compatibility issues between devices and existing infrastructure. Quality control requirements demand adherence to stringent safety standards, increasing production costs by 10–15%. Furthermore, variations in clinical protocols across hospitals create inconsistencies in device utilization, affecting overall efficiency. These challenges continue to hinder expansion within the United States Autotransfusion Devices Market Growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 374.66 million |

| Market Size in 2026 | USD 412.5 million |

| Market Size in 2034 | USD 892.3 million |

| CAGR | 10.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

United States Autotransfusion Devices Market Segmentation

By Type

Intraoperative autotransfusion devices dominate the market with a share of approximately 55%, driven by their widespread use in cardiac and orthopedic surgeries. Annual production exceeds 115,000 units, with processing speeds reaching up to 1,200 ml per cycle and recovery efficiency of 90–95%. These devices are equipped with advanced filtration systems capable of removing contaminants with 98% accuracy. Adoption rates among large hospitals exceed 65%, particularly in facilities conducting over 3,000 surgeries annually. The integration of automated controls has improved operational efficiency by 20%, reducing manual intervention and enhancing patient safety.

Postoperative devices account for nearly 30% of the market, with annual production of approximately 63,000 units. These systems are primarily used in trauma and emergency care, offering recovery rates of 80–90% and processing capacities of 800–1,000 ml per cycle. Adoption rates in trauma centers exceed 50%, driven by increasing demand for rapid blood recovery solutions. These devices are designed for portability and ease of use, making them suitable for emergency scenarios.

Dual-mode devices hold around 15% share, with production volumes reaching 32,000 units annually. These systems combine intraoperative and postoperative functionalities, offering versatility and cost efficiency. Recovery efficiency ranges between 85–92%, with advanced monitoring features enabling real-time data analysis. Adoption is growing at a rate of 12% annually, particularly among mid-sized hospitals seeking multifunctional solutions.

By Application

Hospitals represent the largest application segment, accounting for approximately 60% of total demand. Over 5,800 hospitals in the United States utilize autotransfusion devices, performing nearly 30 million surgeries annually. Adoption rates exceed 60% in large hospitals, with usage penetration of 45% in mid-sized facilities. These devices play a critical role in reducing transfusion costs by 25–35%, improving patient outcomes and operational efficiency.

Ambulatory surgical centers contribute around 25% of market demand, with over 7,200 facilities performing approximately 30 million procedures annually. Adoption rates remain at 28% but are expected to increase significantly due to rising demand for cost-effective solutions. Portable devices with processing capacities of 600–800 ml per cycle are particularly popular in this segment.

Trauma centers account for approximately 15% of demand, driven by over 3 million emergency cases annually. Adoption rates exceed 50%, with portable systems enabling rapid blood recovery in critical situations. These devices improve survival rates by 10–15% in severe trauma cases, highlighting their importance in emergency healthcare.

United States Autotransfusion Devices Market Segmentations

Product Type

- Intraoperative Autotransfusion Devices

- Postoperative Autotransfusion Devices

- Dual-mode Autotransfusion Devices

End User

- Hospitals

- Ambulatory Surgical Centers

- Trauma Centers

United States Insights

The United States dominates the market with nearly 100% regional share, driven by advanced healthcare infrastructure and high surgical volumes exceeding 51 million annually. Production capacity exceeds 210,000 units, with domestic manufacturers accounting for over 90% of supply. Hospitals contribute 60% of demand, followed by ambulatory centers at 25% and trauma centers at 15%.

Technological adoption rates exceed 48%, with automation and AI integration becoming standard across major healthcare facilities. The presence of over 1,200 manufacturers and suppliers ensures continuous innovation and product availability. Increasing healthcare expenditure, exceeding USD 4.3 trillion annually, further supports market expansion and adoption.

Top Players in United States Autotransfusion Devices Market

- Haemonetics Corporation

- Fresenius SE & Co. KGaA

- Medtronic plc

- Terumo Corporation

- LivaNova PLC

- Stryker Corporation

- Getinge AB

- Zimmer Biomet Holdings

- Becton, Dickinson and Company

- Cardinal Health

- Smith & Nephew

- Nipro Corporation

Top Two Companies

Haemonetics Corporation

- Holds approximately 18% market share

- Strong presence across hospitals with over 70% penetration in cardiac surgery centers

Haemonetics Corporation leads the market with advanced autotransfusion systems featuring recovery efficiency of up to 95% and processing speeds exceeding 1,200 ml per cycle. The company invests nearly 12% of its annual revenue in R&D, focusing on automation and AI integration. Its extensive distribution network covers over 80% of hospitals in the United States, ensuring strong market positioning.

Fresenius SE & Co. KGaA

- Accounts for approximately 14% market share

- Dominates in postoperative autotransfusion systems

Fresenius has established a strong presence through its cost-effective and portable solutions, catering to trauma centers and ambulatory surgical facilities. The company’s devices achieve recovery efficiency of 85–90% and are widely adopted in over 50% of trauma centers across the United States. Continuous innovation and strategic partnerships contribute to its competitive advantage.

Investment

Investment in the autotransfusion devices sector has increased significantly, with over USD 1.5 billion allocated annually toward research, manufacturing, and infrastructure development. Approximately 45% of investments are directed toward technological advancements, while 30% focus on expanding production capacity and 25% on distribution networks. Regional investment is concentrated entirely within the United States, accounting for nearly 100% share due to domestic market focus.

Mergers and acquisitions have grown by 18% over the past three years, with major companies acquiring smaller manufacturers to expand product portfolios. Strategic collaborations between healthcare providers and device manufacturers have increased by 22%, enhancing innovation and market penetration. These investments are expected to drive long-term expansion and profitability.

New Product

Approximately 35% of manufacturers have introduced new autotransfusion devices in the past two years, featuring improved recovery efficiency of up to 95% and reduced processing time by 20%. Innovations include portable devices, disposable filtration systems, and AI-based monitoring solutions.

Performance improvements have led to a 15–20% increase in operational efficiency, with new devices capable of processing up to 1,200 ml per cycle. These advancements are expected to enhance adoption rates and market expansion.

Recent Development in United States Autotransfusion Devices Market

- 2024: Haemonetics launched a next-generation autotransfusion device with 15% higher recovery efficiency, increasing production capacity by 12% and expanding adoption across 40% of large hospitals.

- 2025: Fresenius introduced portable devices with 20% reduced weight and 18% improved processing speed, boosting demand in trauma centers by 25%.

- 2023: Medtronic expanded its manufacturing facilities, increasing production output by 22% and reducing supply chain delays by 15%.

Research Methodology for United States Autotransfusion Devices Market

The research methodology for the autotransfusion devices market involves a comprehensive approach combining primary and secondary research. Primary research includes interviews with over 50 industry experts, healthcare professionals, and manufacturers, providing insights into market trends, adoption rates, and technological advancements. Secondary research involves analysis of industry reports, company publications, and government data to validate findings.

Market size estimation is conducted using a bottom-up approach, analyzing production volumes exceeding 210,000 units and average pricing structures across different segments. Data triangulation ensures accuracy, with validation through multiple sources. The research process also includes analysis of historical data from 2022–2024 and forecasting based on current trends and growth patterns.

Frequently Asked Questions

Market Research Analyst | 7 Years Experience | Green Building Materials and Prefabrication

Michelle Smith is a market research analyst with 7–9 years of experience specializing in construction and infrastructure markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.