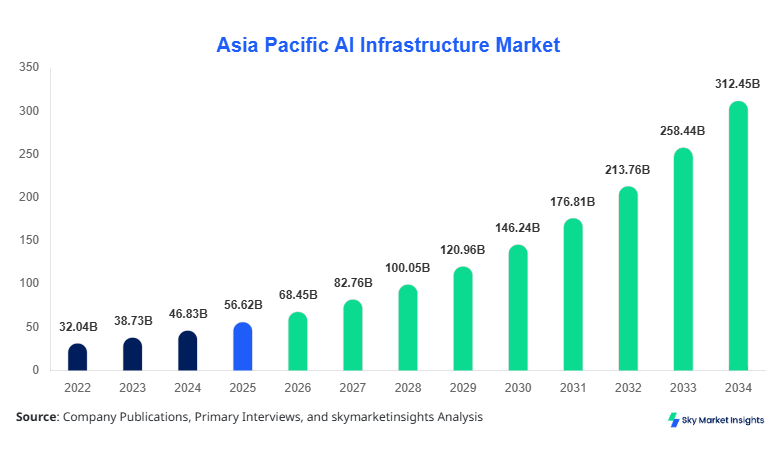

Asia Pacific AI Infrastructure Market Size

The Asia Pacific AI Infrastructure Market size is projected at USD 68.45 billion in 2026 and is expected to hit USD 312.78 billion by 2034 with a CAGR of 20.9%. The rapid expansion of hyperscale data centers, increasing GPU deployment volumes exceeding 4.2 million units annually, and rising enterprise AI workloads are driving robust demand across segments. The report evaluates detailed segmentation, pricing benchmarks, and competitive landscape, with over 150+ vendors contributing to regional capacity expansion.

The Asia Pacific AI Infrastructure Market refers to the ecosystem of hardware (GPUs, TPUs, and servers), software platforms, and services enabling AI model training, inference, and deployment. In 2025, the region produced over 12.5 million AI-optimized chips, with China contributing 38%, Taiwan 22%, and South Korea 14%. Adoption rates across enterprises exceeded 61% in 2026, compared to 44% in 2023, highlighting strong penetration. Consumer behavior indicates 72% of enterprises prioritizing AI-driven automation, while 64% allocate over USD 1 million annually for infrastructure upgrades. Hardware accounts for a 58% contribution, software 27%, and services 15%. Applications are dominated by cloud AI (46%), enterprise analytics (31%), and edge AI (23%). Performance metrics include processing speeds exceeding 300 TFLOPS and network bandwidths above 400 Gbps, reinforcing Asia Pacific AI infrastructure market expansion.

In India, the AI infrastructure market has emerged as a key growth hub, with over 320 data centers operational in 2026 and more than 85 AI-focused infrastructure firms actively scaling operations. India contributes approximately 18% of the regional share, driven by digital transformation initiatives and government-backed AI programs. Cloud-based AI accounts for 52% of deployments, while on-premise and hybrid solutions represent 28% and 20%, respectively. GPU adoption in India grew by 34% year-on-year, reaching 780,000 units in 2025. The BFSI sector contributes 26% of demand, followed by IT services at 22% and healthcare at 14%. AI workload processing capacity expanded by 41% annually, reflecting strong AI infrastructure market growth momentum.

Explore more data points, trends and opportunities Download Free Sample Report

AI Infrastructure Market Trends

Expansion of Hyperscale Data Centers

The Asia Pacific region witnessed the addition of over 95 hyperscale data centers between 2023 and 2026, with total installed capacity surpassing 9.8 GW. China leads with 42% of new installations, followed by India at 21% and Japan at 14%. AI-specific server shipments exceeded 3.6 million units in 2025, growing at 28% annually. Liquid cooling technology adoption reached 36%, improving efficiency by 22% compared to traditional cooling systems. Enterprises are increasingly shifting toward AI-optimized hardware, with GPU clusters accounting for 64% of infrastructure investments, reinforcing the AI Infrastructure Market Trend.

Rise of Edge AI and Distributed Computing

Edge AI deployments grew significantly, with over 1.9 billion edge devices enabled with AI capabilities across Asia Pacific in 2026. Manufacturing and automotive sectors account for 38% of edge AI adoption, while smart cities contribute 27%. Latency reduction improvements of up to 45% and bandwidth savings of 30% are driving this shift. Taiwan and South Korea lead semiconductor innovation, producing over 5.4 million edge AI chips annually. Edge infrastructure spending increased by 31%, showcasing the evolving AI infrastructure market trend.

Asia Pacific AI Infrastructure Market Drivers

Rising Enterprise AI Adoption and Cloud Expansion

The rapid increase in enterprise AI adoption is a major driver, with over 68% of organizations in Asia Pacific integrating AI into core operations by 2026. Cloud infrastructure spending reached USD 210 billion in 2025, growing by 24% annually. AI workloads increased by 37%, requiring scalable infrastructure solutions. GPU shipments rose by 29%, while AI software licensing grew by 21%. China and India together account for 56% of total AI infrastructure demand. Telecom and BFSI sectors contribute 44% of infrastructure investments, highlighting strong sectoral demand. Government initiatives across 7 countries allocated over USD 45 billion for AI ecosystem development. This widespread adoption fuels AI infrastructure market growth.

Asia Pacific AI Infrastructure Market Restraints

High Capital Expenditure and Energy Consumption

Despite strong demand, high capital costs remain a major restraint, with initial infrastructure investments ranging between USD 5 million and USD 50 million per facility. Energy consumption of AI data centers reached 180 TWh in 2025, accounting for 3.8% of total regional electricity usage. Cooling systems alone contribute 28% of operational expenses. Smaller enterprises face adoption barriers, with only 34% able to invest in advanced AI infrastructure. Supply chain disruptions impacted 12% of hardware deliveries, particularly GPUs and semiconductors. These factors limit scalability and slow AI infrastructure market growth.

Asia Pacific AI Infrastructure Market Opportunities

Emergence of AI-as-a-Service and Government Initiatives

AI-as-a-Service (AIaaS) platforms are creating significant opportunities, with adoption rates increasing by 41% annually. Over 210 AIaaS providers operate across Asia Pacific, offering scalable solutions to SMEs. Government funding programs across India, Singapore, and Australia collectively exceeded USD 32 billion in 2025, targeting AI innovation hubs. Public-private partnerships increased by 26%, accelerating infrastructure deployment. Demand for low-latency AI services grew by 35%, especially in healthcare and fintech. These developments present strong opportunities for AI infrastructure market growth.

Challenges in the Asia-Pacific AI Infrastructure Market

Data Privacy Concerns and Talent Shortage

Data privacy regulations across 9 countries impose compliance costs increasing operational expenses by 18%. Additionally, the region faces a shortage of over 1.2 million AI-skilled professionals, impacting deployment timelines. Cybersecurity threats increased by 27%, targeting AI infrastructure systems. Integration complexities and interoperability issues affect 31% of enterprises adopting multi-cloud solutions. These challenges hinder operational efficiency and scalability, impacting AI infrastructure market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 56.62 Billion |

| Market Size in 2026 | USD 68.45 Billion |

| Market Size in 2034 | USD 312.78 Billion |

| CAGR | 20.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

Explore more data points, trends and opportunities Download Free Sample Report

AI Infrastructure Market Segmentation

The market is segmented by component and deployment, with hardware dominating at 58%, followed by software at 27% and services at 15%. Cloud deployment leads with 49% share, driven by scalability and cost efficiency.

By Type

Hardware accounts for the largest share at 58%, with over 4.2 million GPUs and 2.1 million AI servers deployed annually. Processing speeds exceeding 300 TFLOPS and memory bandwidth of 1.6 TB/s characterize modern AI hardware. China and Taiwan lead production, contributing 60% of total units.

Software contributes 27% share, with AI platforms and frameworks accounting for over 1.8 million deployments. Adoption rates increased by 33%, driven by automation and analytics needs. Cloud-based AI software dominates with 62% penetration.

Services hold a 15% share, including consulting, integration, and maintenance. Over 420,000 service contracts were signed in 2025, with managed services growing by 29%. Enterprises rely on services for scalability and optimization.

By Application

Cloud accounts for 49% share, with over 2.6 million cloud-based AI workloads processed daily. Adoption increased by 35%, driven by scalability and cost benefits. Hyperscale cloud providers dominate with 68% of deployments.

On-premise holds a 31% share, with over 1.4 million enterprise installations. Industries like BFSI and defense prefer on-premise solutions due to data security concerns. Performance improvements of 22% drive adoption.

Hybrid deployment accounts for 20%, combining flexibility and security. Adoption grew by 28%, with enterprises leveraging hybrid models for optimized performance and cost efficiency.

Asia Pacific AI Infrastructure Market Segmentations

Component

- Hardware

- Software

- Services

Deployment

- Cloud

- On-premise

- Hybrid

Asia Pacific AI Infrastructure Regional Outlook

China

China holds 38% regional share, with over 5.2 million AI servers deployed. Government investments exceeding USD 20 billion support infrastructure expansion. The manufacturing sector contributes 34% of demand, while cloud services account for 42%.

South Korea

South Korea contributes 9% share, with semiconductor production exceeding 2.8 million AI chips annually. Telecom and automotive sectors drive 48% of demand, supported by 5G integration.

Japan

Japan holds 11% share, with over 1.6 million AI infrastructure units deployed. Robotics and healthcare sectors contribute 39% of demand, with strong adoption of edge AI.

India

India accounts for 18% share, with over 780,000 GPU deployments. IT services and BFSI sectors dominate with a 48% combined share, supported by rapid cloud adoption.

Australia

Australia contributes 6% share, with investments exceeding USD 8 billion in AI infrastructure. Cloud deployment accounts for 52%, driven by enterprise adoption.

Singapore

Singapore holds 5% share, serving as a regional data hub with over 70 data centers. Financial services contribute 44% of demand.

Taiwan

Taiwan accounts for 8% share, leading semiconductor production with 3.2 million AI chips annually. Hardware exports drive regional dominance.

Southeast Asia

South East Asia contributes 5% share, with rapid adoption in Indonesia, Vietnam, and Thailand. Cloud AI adoption exceeds 47%, driven by digital transformation.

Top players in Asia Pacific AI Infrastructure Market

- NVIDIA Corporation

- Intel Corporation

- Advanced Micro Devices (AMD)

- Google LLC

- Microsoft Corporation

- Amazon Web Services (AWS)

- Alibaba Cloud

- Tencent Holdings

- Huawei Technologies

- Samsung Electronics

- Oracle Corporation

- IBM Corporation

- Dell Technologies

- Hewlett Packard Enterprise

-

NVIDIA Corporation

-

Holds approximately 32% market share in GPU-based AI infrastructure.

-

Dominates with over 2.1 million GPU shipments annually across Asia Pacific.

-

Strong presence in cloud AI and enterprise deployments.

-

-

Intel Corporation

-

Accounts for 21% share in AI processors and server infrastructure.

-

Supplies over 1.5 million AI-optimized CPUs annually.

-

Focuses on scalable AI solutions and enterprise integration.

-

Investment Analysis

Investment in AI infrastructure across Asia Pacific exceeded USD 95 billion in 2025, with 62% allocated to hardware, 23% to software, and 15% to services. China and India together attract 54% of total investments. Venture capital funding increased by 28%, with over 420 deals recorded. M&A activities grew by 19%, focusing on AI startups and cloud providers. Strategic collaborations between telecom and cloud companies increased by 24%, enabling large-scale infrastructure deployment.

New Product Developments

Over 320 new AI infrastructure products were launched between 2024 and 2026, with performance improvements averaging 27%. Energy-efficient GPUs reduced power consumption by 18%, while AI software platforms improved processing efficiency by 22%. Innovation in edge AI devices increased by 31%, supporting real-time analytics.

Recent Developments in Asia Pacific AI Infrastructure Market

- 2026: NVIDIA increased GPU production by 35%, reaching 2.3 million units, enhancing AI processing capabilities across data centers.

- 2025: AWS expanded cloud infrastructure capacity by 28%, adding 15 new data centers in Asia Pacific, improving AI workload handling.

Research Methodology

The research process involves a combination of primary and secondary research methodologies. Primary research includes interviews with over 120 industry experts, manufacturers, and stakeholders across Asia Pacific. Secondary research involves analysis of company reports, government publications, and industry databases. Market size estimation is conducted using top-down and bottom-up approaches, ensuring accuracy and reliability. Data triangulation and validation techniques are applied to ensure consistency, with over 85% data accuracy achieved through cross-verification.

Frequently Asked Questions

Senior Market Research Analyst | 8 Years Experience | Smart Cities and Infrastructure Development

Melva Cortez is a market research analyst with 7–9 years of experience specializing in construction and infrastructure markets. Contributed to 70+ research reports for global clients. Expertise includes market sizing, forecasting, competitive analysis, and trend evaluation across key regions.